Answers and Solutions: 11 – 1

Chapter 11

Cash Flow Estimation

and Risk Analysis

ANSWERS TO END-OF-CHAPTER QUESTIONS

11-1 a. Project cash flow, which is the relevant cash flow for project analysis, represents the

actual flow of cash, which includes investments in capital and working capital, but does

not include interest expenses or noncash charges like depreciation (except to the extent

that depreciation affects taxes). In other words, project cash flow is the free cash flow

generated by the project. Accounting income, on the other hand, reports accounting

data as defined by Generally Accepted Accounting Principles (GAAP).

c. Net operating working capital changes are the increases in current operating assets

resulting from accepting a project less the resulting increases in current operating

liabilities, or accruals and accounts payable. A net operating working capital change

must be financed just as a firm must finance its increases in fixed assets. Salvage value

is the market value of an asset after its useful life. Salvage values and their tax effects

must be included in project cash flow estimation.

Answers and Solutions: 11 – 2

d. Stand-alone risk is the risk a project would have if it was held in isolation. Corporate

(within-firm) risk is the risk that a project contributes to a company after taking into

consideration the cash flows of the company’s other projects; because projects are not

perfectly correlated, corporate risk usually will be less than stand-alone risk. Market

(beta) risk is the risk that a company contributes to a well diversified portfolio.

f. A risk-adjusted discount rate incorporates the risk of the project’s cash flows. The cost

of capital to the firm reflects the average risk of the firm’s existing projects. Thus, new

projects that are riskier than existing projects should have a higher risk-adjusted

discount rate. Conversely, projects with less risk should have a lower risk-adjusted

discount rate. This adjustment process also applies to a firm’s divisions. Risk

differences are difficult to quantify, thus risk adjustments are often subjective in nature.

A project’s cost of capital is its risk-adjusted discount rate for that project.

with strategic issues. Finally, they are also called embedded options because they are a

part of another project.

i. Investment timing options give companies the option to delay a project rather than

implement it immediately. This option to wait allows a company to reduce the

11-2 Only cash can be spent or reinvested, and since accounting profits do not represent cash,

they are of less fundamental importance than cash flows for investment analysis. Recall

that in the stock valuation chapters we focused on dividends and free cash flows, which

represent cash flows, rather than on earnings per share, which represent accounting profits.

11-3 Since the cost of capital includes a premium for expected inflation, failure to adjust cash

flows means that the denominator, but not the numerator, rises with inflation, and this

lowers the calculated NPV.

11-4 Capital budgeting analysis should only include those cash flows which will be affected by

the decision. Sunk costs are unrecoverable and cannot be changed, so they have no bearing

11-5 When a firm takes on a new capital budgeting project, it typically must increase its

investment in receivables and inventories, over and above the increase in payables and

Answers and Solutions: 11 – 4

11-6 Scenario analysis analyzes a limited number of outcomes. Although the base case scenario

may be the most likely, or expected outcome, the bad and good scenarios are frequently

worst case and best case scenarios, that is, when everything goes bad together, or

11-7 The costs associated with financing are reflected in the weighted average cost of capital.

To include interest expense in the capital budgeting analysis would “double count” the

cost of debt financing.

11-8 Daily cash flows would be theoretically best, but they would be costly to estimate and

probably no more accurate than annual estimates because we simply cannot forecast

11-9 In replacement projects, the benefits are generally cost savings, although the new

machinery may also permit additional output. The data for replacement analysis are

generally easier to obtain than for new products, but the analysis itself is somewhat more

complicated because almost all of the cash flows are incremental, found by subtracting

the new cost numbers from the old numbers. Similarly, differences in depreciation and

any other factor that affects cash flows must also be determined.

Answers and Solutions: 11 – 5

11-10 Stand-alone risk is the project’s risk if it is held as a lone asset. It disregards the fact that

it is but one asset within the firm’s portfolio of assets and that the firm is but one stock in

a typical investor’s portfolio of stocks. Stand-alone risk is measured by the variability of

11-11 It is often difficult to quantify market risk. On the other hand, we can usually get a good

idea of a project’s stand-alone risk, and that risk is normally correlated with market risk:

The higher the stand-alone risk, the higher the market risk is likely to be. Therefore,

firms tend to focus on stand-alone risk, then deal with corporate and market risk by

making subjective, judgmental modifications to the calculated stand-alone risk.

Answers and Solutions: 11 – 6

SOLUTIONS TO END-OF-CHAPTER PROBLEMS

11-1 a. Equipment $ 17,000,000

NWC Investment 5,000,000

11-2 Operating Cash Flows: t = 1

Sales revenues $18,000,000

Operating costs 9,000,000

11-3 Equipment’s original cost $12,000,000

Depreciation (80%) 9,000,000

Book value $ 3,000,000

Answers and Solutions: 11 – 7

11-4 Cash outflow = $40,000.

Increase in annual after-tax cash flows: CF = $9,000.

11-5 a. The MACRS rates are 33.33%, 44.45%, 14.81%, and 7.41%. The first MACRS

depreciation expense is 33.33%($1,700,000) = $566,610. The others are calculated

similarly. The applicable depreciation values are as follows for the two scenarios:

Scenario 1 Scenario 2

Year (Straight Line) (MACRS)

1 $425,000 $566,610

2 425,000 755,650

3 425,000 251,770

4 425,000 125,970

b. To find the difference in net present values under these two methods, we must

determine the difference in incremental cash flows each method provides. The

depreciation expenses cannot simply be subtracted from each other, as there are tax

Answers and Solutions: 11 – 8

cash flows that represent the benefit from depreciation expense and solve for net

present value based upon a WACC of 10%.

CF0 = 0; CF1 = 56644; CF2 = 132260; CF3 = -69292; CF4 = -119612; and I/YR = 10.

Solve for NPV = $27,043.62

So, all else equal the use of the accelerated depreciation method will result in a higher

NPV (by $27,043.62) than would the use of a straight-line depreciation method.

11-6 a. The net cost is $1,118,000:

Price ($1,080,000)

Modification (22,500)

Increase in NWC (15,500)

Cash outlay for new machine ($1,118,000)

Answers and Solutions: 11 – 9

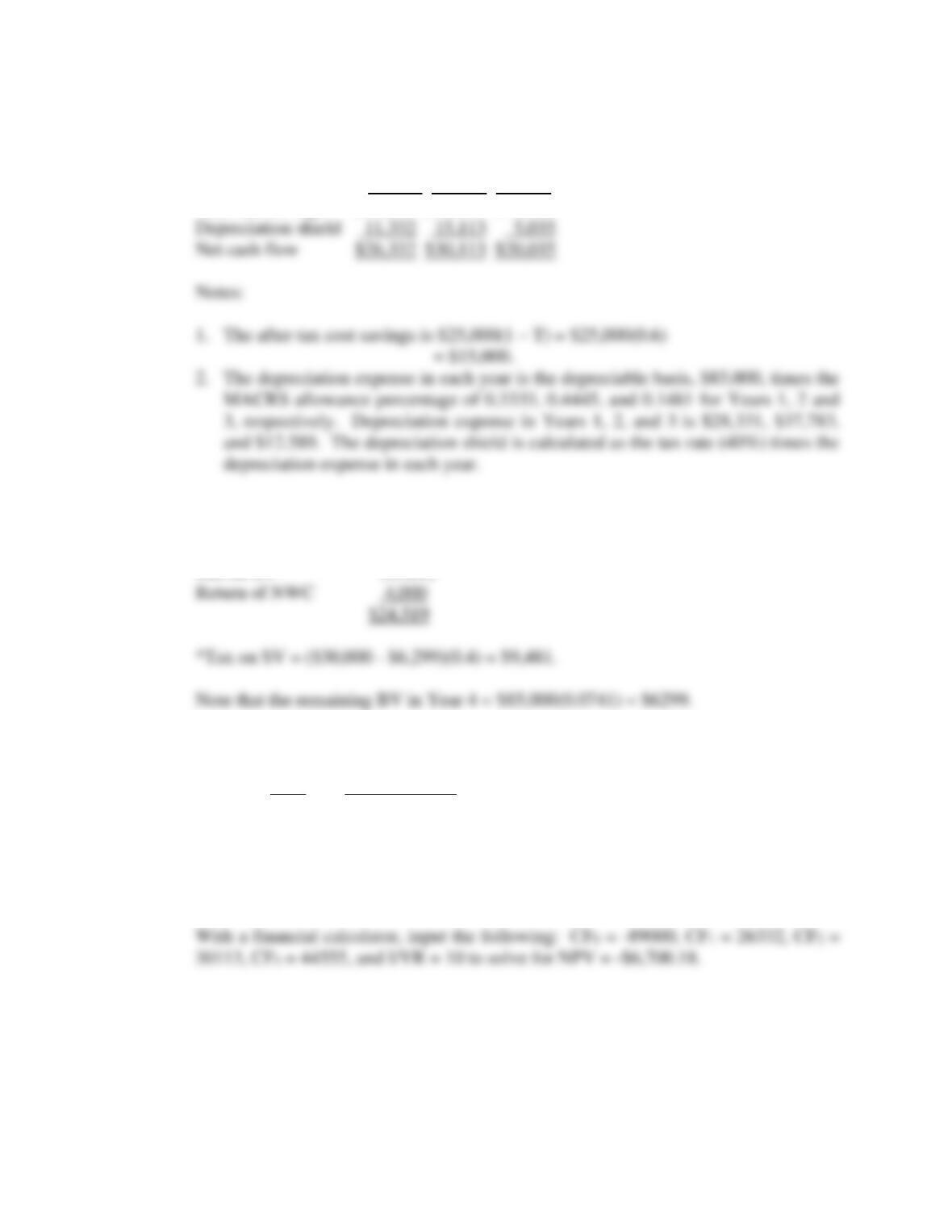

2. The depreciation expense in each year is the depreciable basis, $1,102,500, times

the MACRS allowance percentages of 0.3333, 0.4445, and 0.1481 for Years 1, 2,

and 3, respectively. Depreciation expense in Years 1, 2, and 3 is $367,463,

$490,061, and $163,280. The depreciation tax savings is calculated as the tax rate

(35%) times the depreciation expense in each year.

c. The terminal year cash flow is $473,343:

d. The project has an NPV of $78,790; thus, it should be accepted.

Year Net Cash Flow PV @ 12%

0 ($1,118,000) ($1,118,000)

11-7 a. The net cost is $89,000:

Price ($70,000)

Modification (15,000)

Change in NWC (4,000)

($89,000)

Answers and Solutions: 11 – 10

b. The operating cash flows follow:

Year 1 Year 2 Year 3

After-tax savings $15,000 $15,000 $15,000

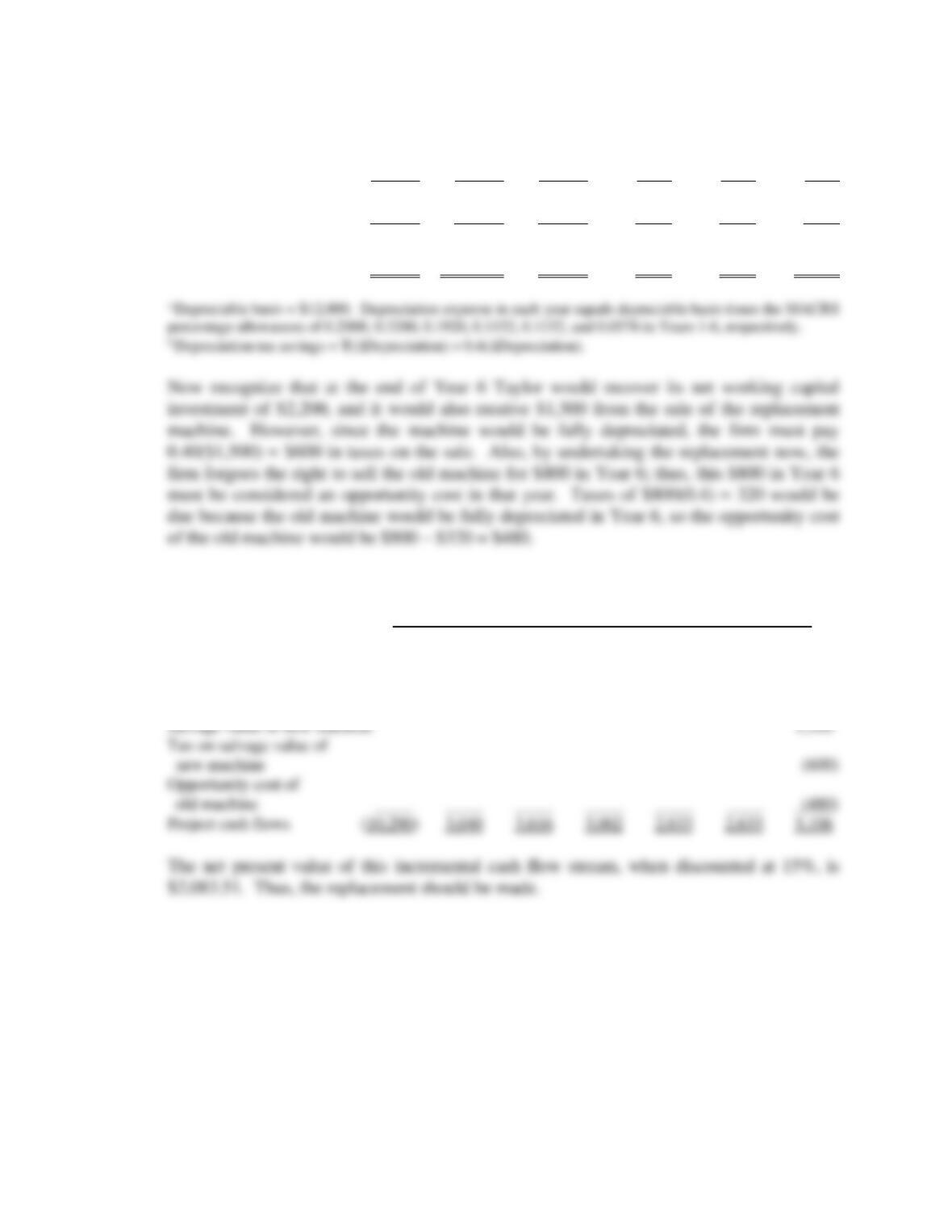

c. The additional end-of-project cash flow is $24,519:

Salvage value $30,000

Tax on SV* (9,481)

d. The project has an NPV of -$6,700. Thus, it should not be accepted.

Year Net Cash Flow

0 ($89,000)

1 26,332

2 30,113

3 44,555

With a financial calculator, input the following: CF0 = -89000, CF1 = 26332, CF2 =

Answers and Solutions: 11 – 11

11-8 a. Sales = 1,000($138) $138,000

Cost = 1,000($105) 105,000

Net before tax $ 33,000

Taxes (34%) 11,220

Net after tax $ 21,780

Not considering inflation, NPV is -$4,800. This value is calculated as

After adjusting for expected inflation, we see that the project has a positive NPV and

should be accepted. This demonstrates the bias that inflation can induce into the

capital budgeting process: Inflation is already reflected in the denominator (the cost

of capital), so it must also be reflected in the numerator.

A more straightforward way to calculate the present value without having to calculate

a real required rate of return is to use the constant growth formula, instead. Here, the

present value of all of the future cash flows is:

Answers and Solutions: 11 – 12

b. If part of the costs were fixed, and hence did not rise with inflation, then sales

revenues would rise faster than total costs. However, when the plant wears out and

11-9 First determine the net cash flow at t = 0:

Purchase price ($12,000)

Sale of old machine 4,150

Tax on sale of old machine (240)a

Change in net working capital (2,200)b

Total investment ($10,290)

Answers and Solutions: 11 – 13

Depreciation:

Year 1 2 3 4 5 6

Newa $2,400 $8,840 $2,304 $1,382 $1,382 $691

Old 650 650 650 650 650 325

Change $1,750 $3,190 $1,654 $732 $732 $366

Depreciation tax savingsb $ 700 $ 1,276 $ 662 $293 $293 $ 146

Finally, place all the cash flows on a time line:

0 1 2 3 4 5 6

| | | | | | |

Net investment (10290)

After-tax revenue increase 2,340 2,340 2,340 2,340 2,340 2,340

Depreciation tax savings 700 1,276 662 293 293 146

Working capital recovery 2,200

15%

Answers and Solutions: 11 – 14

11–10 1. Net investment at t = 0:

Cost of new machine $182,500

Net investment outlay (CF0) $182,500

2. After-tax

Year Earnings T(Dep) Annual CFt

1 $28,200 $ 14,600 $42,800

2 28,200 23,360 51,560

Notes:

a. The after-tax earnings are $47,000(1 – T) = $47,000(0.6) = $28,200.

b. Find Dep over Years 1-8:

The old machine was fully depreciated; therefore, Dep = Depreciation on the new machine.

Dep Dep

Year Rate Basis Depreciation

1 0.2000 $182,500 $36,500

3. Now find the NPV of the replacement machine:

Place the cash flows on a time line:

0 1 2 3 4 5 6 7 8

Answers and Solutions: 11 – 15

11-11 E(NPV) = 0.05(-$70) + 0.20(-$25) + 0.50($12) + 0.20($20) + 0.05($30)

= -$3.5 + -$5.0 + $6.0 + $4.0 + $1.5

= $3.0 million.

Answers and Solutions: 11 – 16

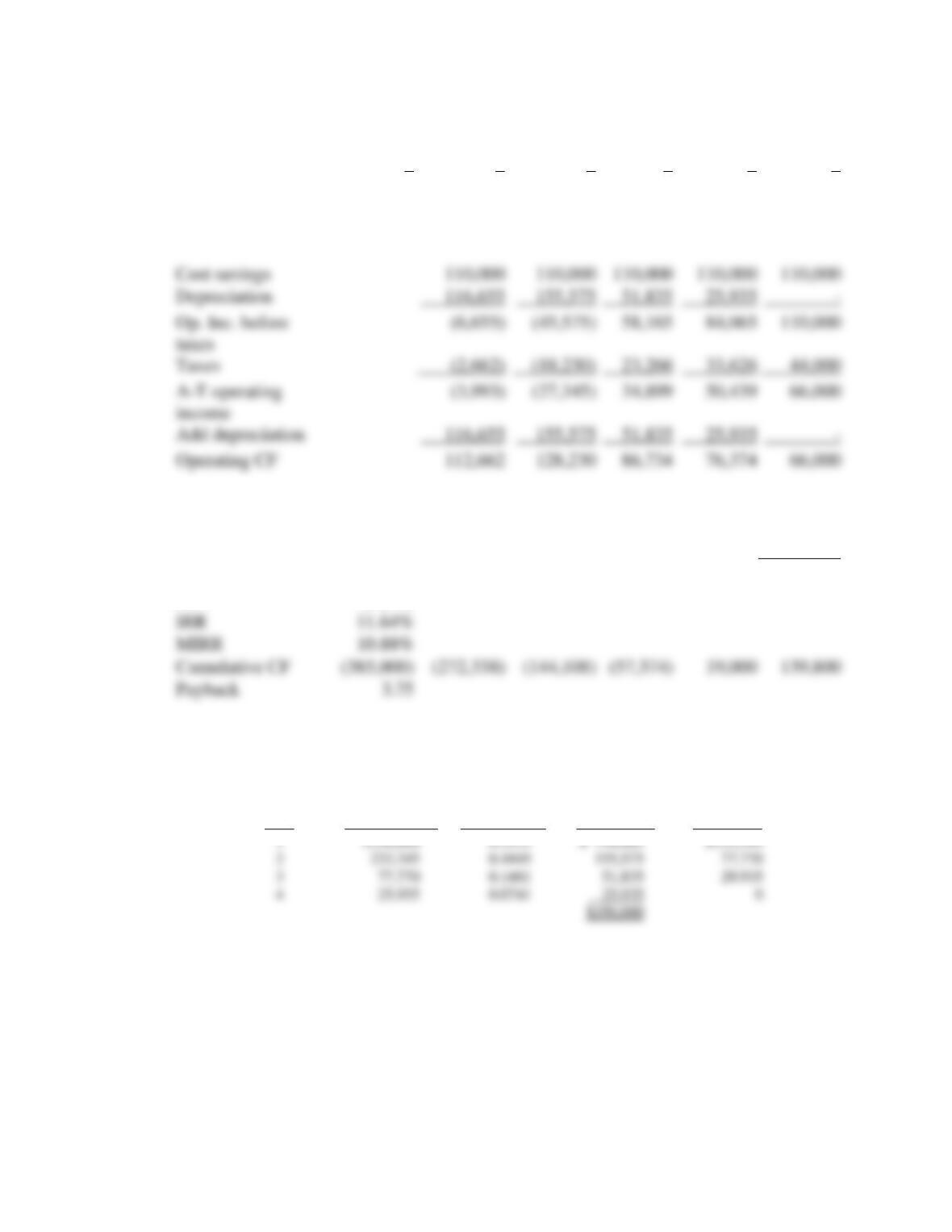

11-12 a.

0

1

2

3

4

5

Machine cost

(350,000)

Net working

capital

(35,000)

Return of NWC

35,000

Sale of machine

33,000

Tax on sale

(13,200)

Total CF

(385,000)

112,662

128,230

86,734

76,374

120,800

NPV

15,732

Cumulative CF

(385,000)

(272,338)

(144,108)

(57,374)

19,000

139,800

Payback

Notes:

a Depreciation Schedule, Basis = $250,000

MACRS Rate

Basis =

Year Beg. Bk. Value MACRS Rate Depreciation Ending BV

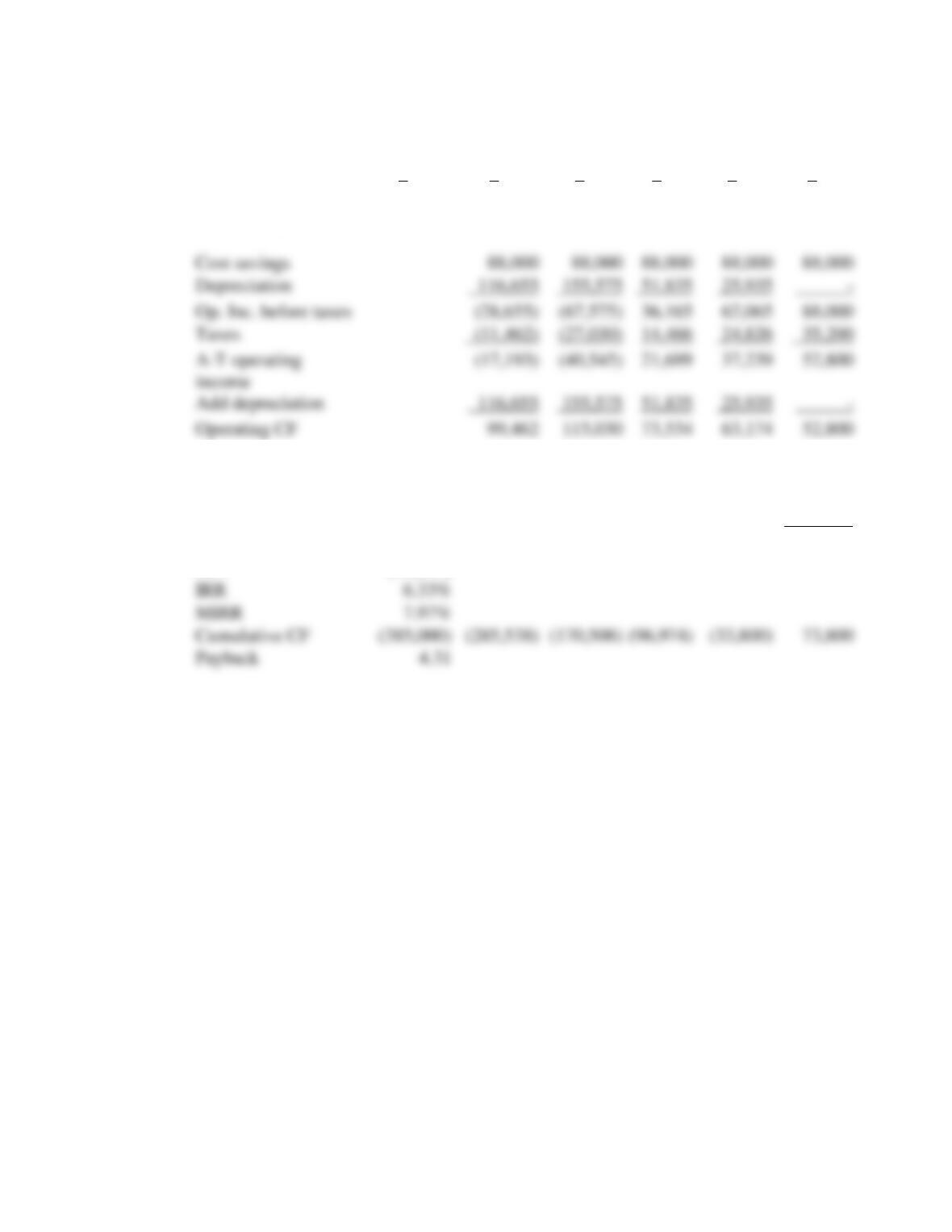

Cost savings

110,000

110,000

110,000

110,000

110,000

Depreciation

Op. Inc. before

taxes

(45,575)

84,065

Taxes

A-T operating

income

(27,345)

50,439

Add depreciation

Operating CF

112,662

128,230

86,734

76,374

66,000

Answers and Solutions: 11 – 17

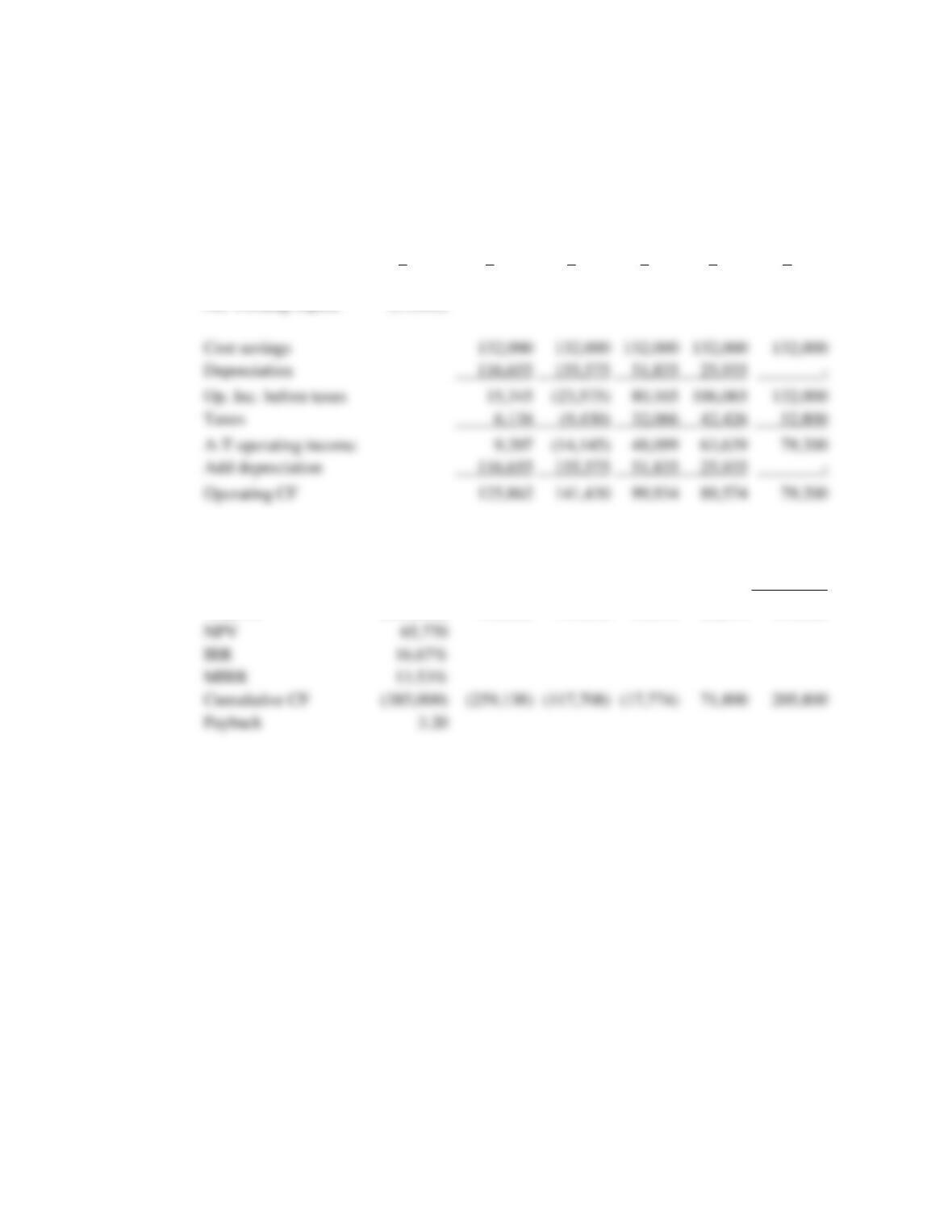

b. If savings increase by 20%, then savings will be (1.2)($110,000) = $132,000.

If savings decrease by 20%, then savings will be (0.8)($110,000) = $88,000.

(1) Savings increase by 20%:

0

1

2

3

4

5

Machine cost

(350,000)

Net working capital

(35,000)

Return of NWC

35,000

Sale of machine

33,000

Tax on sale

(13,200)

Total CF

(385,000)

125,862

141,430

99,934

89,574

134,000

NPV

IRR

MIRR

Cumulative CF

(385,000)

71,800

205,800

Payback

Cost savings

132,000

132,000

132,000

132,000

132,000

Depreciation

155,575

51,835

25,935

Op. Inc. before taxes

15,345

80,165

106,065

132,000

Taxes

32,066

42,426

A-T operating income

9,207

48,099

63,639

79,200

Add depreciation

155,575

51,835

25,935

Operating CF

125,862

141,430

99,934

89,574

79,200

Answers and Solutions: 11 – 18

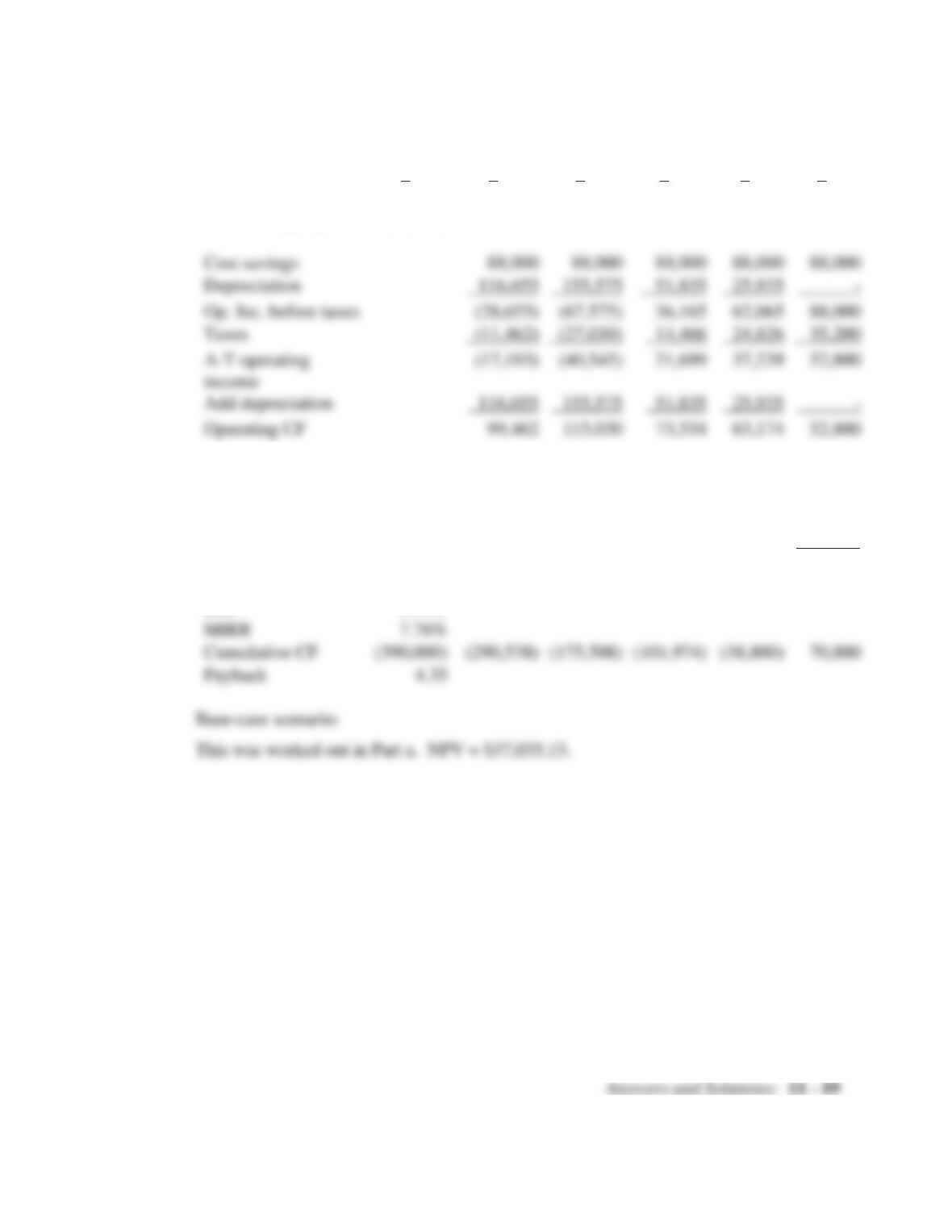

(2) Savings decrease by 20%:

0

1

2

3

4

5

Machine cost

(350,000)

Net working capital

(35,000)

Return of NWC

35,000

Sale of machine

33,000

Tax on sale

(13,200)

Total CF

(385,000)

99,462

115,030

73,534

63,174

107,600

NPV

(34,307)

IRR

MIRR

Cumulative CF

(385,000)

(170,508)

(96,974)

73,800

Payback

Cost savings

88,000

88,000

Op. Inc. before taxes

(28,655)

(67,575)

36,165

88,000

Operating CF

73,534

52,800

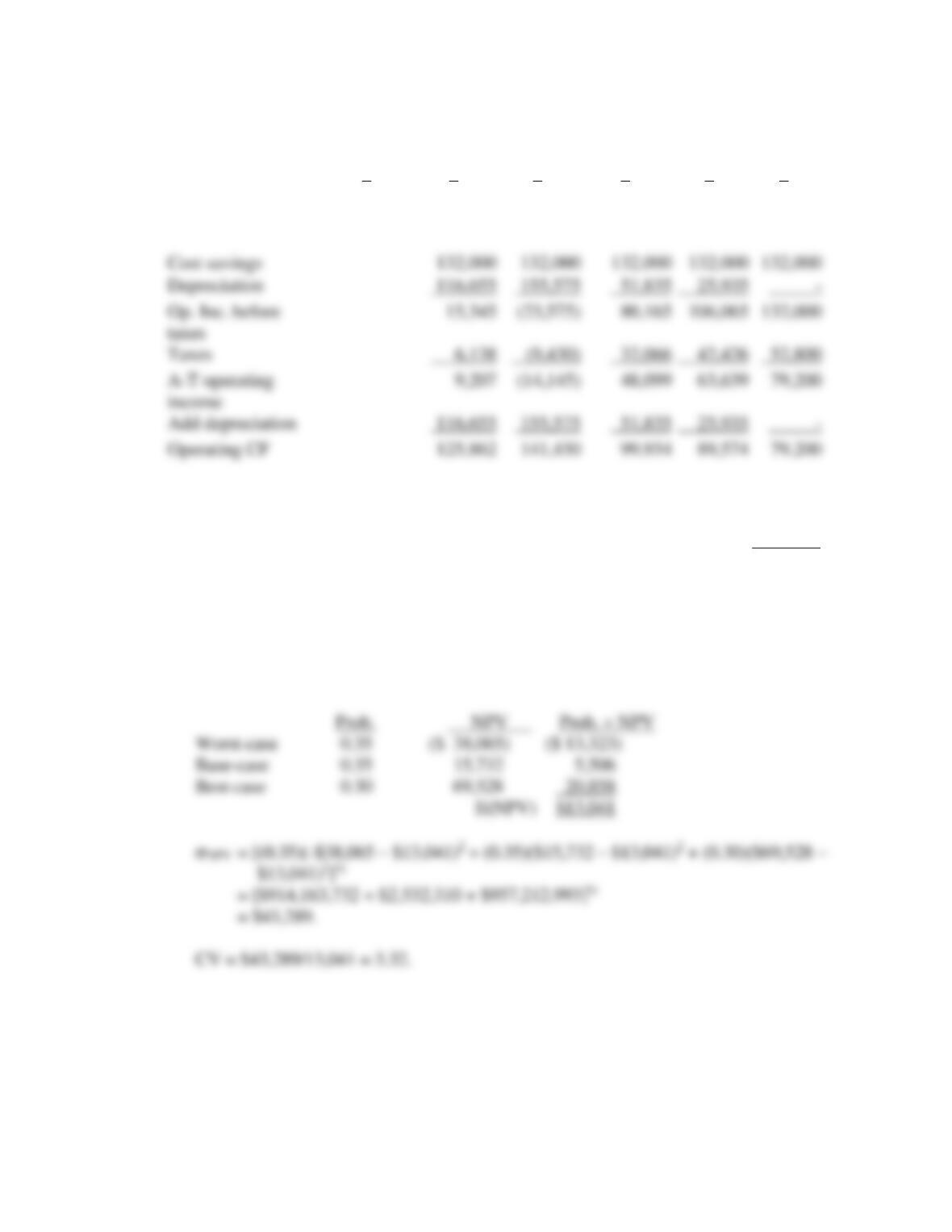

c. Worst-case scenario:

0

1

2

3

4

5

Machine cost

(350,000)

Net working capital

(40,000)

Cost savings

88,000

88,000

88,000

88,000

88,000

Op. Inc. before taxes

(67,575)

36,165

62,065

88,000

A-T operating

Operating CF

99,462

115,030

73,534

63,174

52,800

Return of NWC

40,000

Sale of machine

28,000

Tax on sale

(11,200)

Total CF

(390,000)

99,462

115,030

73,534

63,174

109,600

NPV

(38,065)

IRR

5.99%

MIRR

7.76%

Cumulative CF

(390,000)

(175,508)

(101,974)

(38,800)

70,800

Payback

Answers and Solutions: 11 – 20

Best-case scenario:

0

1

2

3

4

5

Machine cost

(350,000)

Net working capital

(30,000)

Return of NWC

30,000

Sale of machine

38,000

Tax on sale

(15,200)

Total CF

(380,000)

125,862

141,430

99,934

89,574

132,000

NPV

69,528

IRR

17.15%

MIRR

13.76%

Cumulative CF

(380,000)

(254,138)

(112,708)

(12,774)

76,800

208,800

Payback

3.14

Cost savings

132,000

132,000

132,000

132,000

132,000

Depreciation

Taxes

Add depreciation

Operating CF

125,862

141,430

99,934

89,574

79,200

Answers and Solutions: 11 – 21

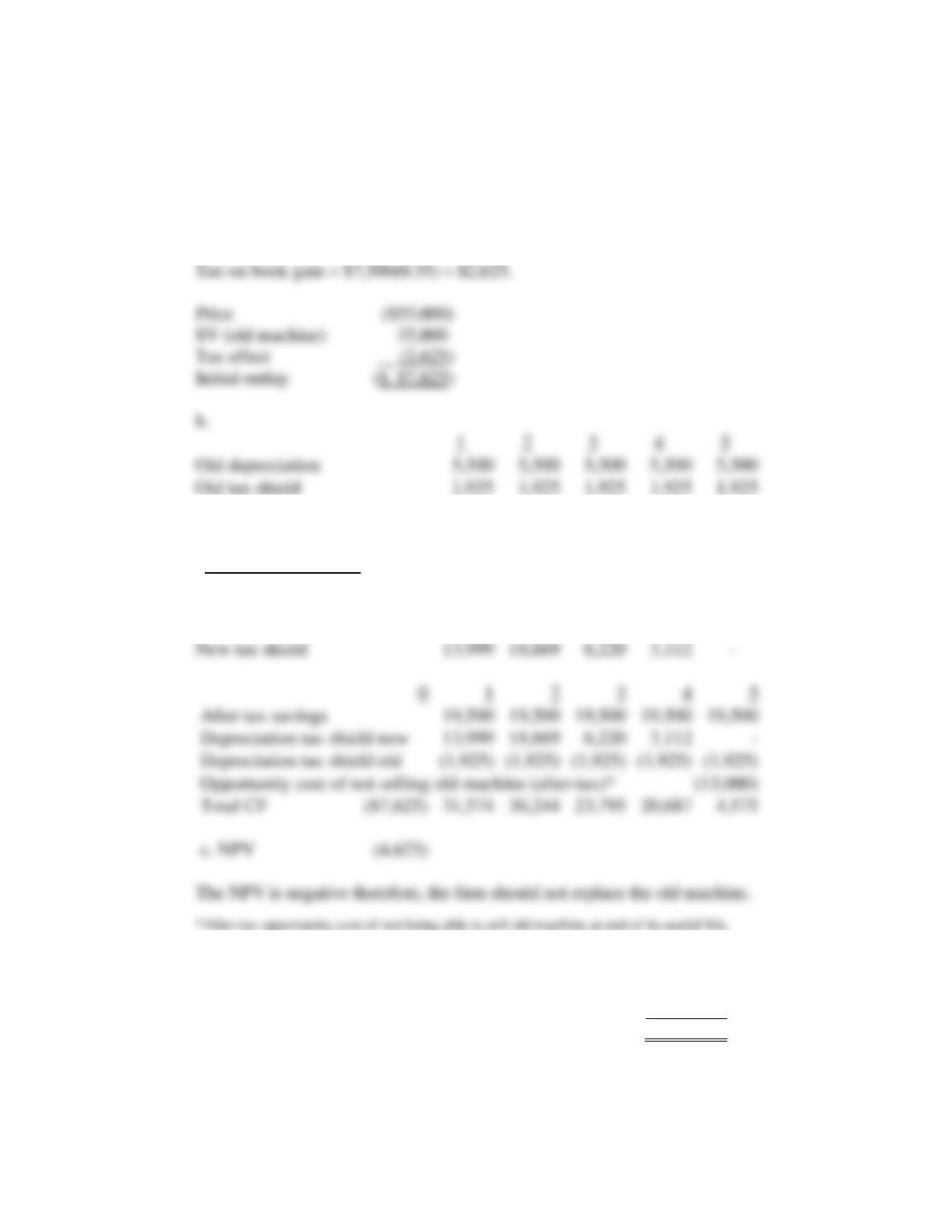

11-13 a. Old depreciation = $5,500 per year.

Book value = $55,000 – 5($5,500) = $27,500.

Gain = $35,000 – $27,500 = $7,500.

Basis

120,000

New depreciation

39,996

53,340

17,772

8,892

–

New tax shield

13,999

18,669

6,220

3,112

–

After tax savings

19,500

19,500

19,500

19,500

19,500

Depreciation tax shield new

13,999

18,669

6,220

3,112

Depreciation tax shield old

(1,925)

(1,925)

(1,925)

(1,925)

(1,925)

Opportunity cost of not selling old machine (after-tax)*

(13,000)

Total CF

36,244

23,795

20,687

4,575

11-14 a. Cost of new machine ($775,000)

Salvage value, old 135,000

Savings due to loss on sale ($450,000 – $135,000) 0.35 110,250

Cash outlay for new machine ($ 529,750)

MACRS Rate

33.33%

44.45%

14.81%

7.41%

0.00%

Old depreciation

5,500

5,500

5,500

5,500

5,500

Old tax shield

1,925

1,925

1,925

1,925

1,925

Answers and Solutions: 11 – 22

shield

c. CFt = (Operating expenses)(1 – T) + (Depreciation)(T).

0

1

2

3

4

5

After tax cost savings

120,250

120,250

120,250

120,250

120,250

shield

Salvage value

Incremental Depreciation tax

22,750

55,300

20,580

(252)

(252)

e. 1. If the expected life of the old machine decreases, the new machine will look better

as cash flows attributable to the new machine would increase. On the other hand, a

serious complication arises: the two projects now have unequal lives, and an

estimate must be made about the action to be taken when the old machine is

scrapped. Will it be replaced, and at what cost and with what savings?

2. The higher capital cost should be used in the analysis.

Old depreciation

90,000

90,000

90,000

90,000

90,000

Old tax shield

31,500

31,500

31,500

31,500

31,500

Basis

MACRS depreciation rate

New depreciation

155,000

248,000

148,800

89,280

89,280

Incremental depreciation

158,000

58,800

Incremental depreciation tax

22,750

55,300

(252)

(252)

Answers and Solutions: 11 – 23

11-15 a. Expected annual cash flows:

Project A: Probable

Probability Cash Flow = Cash Flow

0.2 $6,000 $1,200

Coefficient of variation:

CV =

Project A:

σA =

NPV Expected

=

valueExpected

deviation Standard NPV

$474.34. = (0.2)

)

($750 + (0.6)

)

($0 + (0.2)

)

(-$750 222

Answers and Solutions: 11 – 24

b. Project B is the riskier project because it has the greater variability in its probable

cash flows, whether measured by the standard deviation or the coefficient of

variation. Hence, Project B is evaluated at the 12 percent cost of capital, while

Project A requires only a 10 percent cost of capital.

11-16 a. First, note that with symmetric probability distributions, the middle value of each

distribution is the expected value. Therefore,

Expected Values

Sales (units) 200

Sales price $13,500

Using a financial calculator, input the following: CF0 = -4000000, CF1 = 900000, and

Nj = 8, to solve for IRR = 15.29%.

Expected IRR = 15.29% ≈ 15.3%.

=+

1t t

Assuming complete independence between the distributions, and normality, it would

be possible to derive σIRR statistically. Alternatively, we could employ simulation to

develop a distribution of IRRs, hence σIRR. There is no easy way to get σIRR.

life should be used.

(2) a. Estimate unit sales. The 16 indicates sales of 100 units.

b. Estimate the sales price. The 58 indicates a sales price of $13,500.

(4) Repeat the process for Year 3. Sales will be 100 units with a random number of

19; the price will be $13,500 with a random number of 62; and the cost will be

$5,000 with a random number of 6:

[100($13,500) – 100($5,000)](0.6) = $510,000 = CF3.

Answers and Solutions: 11 – 26

4000000, CF1 = 510000, CF2 = 780000, CF3 = 510000, and solve for IRR =

-31.55%.

b. NPV = – $4,000,000.

With a financial calculator, input the following: CF0 = -4000000, CF1 =

321 )15.1(

000,510$

)15.1(

000,780$

)15.1(

000,510$++

Answers and Solutions: 11 – 27

(6) & (7) The computer would store NPVs and IRRs for the different trials, then

display them as frequency distributions:

Probability

of occurrence

X

XX

XXXX

XXXXXXXX

XXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXX

Answers and Solutions: 11 – 28

11-17 a. The resulting decision tree is:

NPV

t = 0 t = 1 t = 2 t = 3 P NPV Product

$3,000,000 0.24 $881,718 $211,612

($1,000,000) P = 0.5

P = 0.80 1,500,000 0.24 (185,952) (44,628)

The NPV of the top path is:

– – – $10,000 = $881,718.

3

)12.1(

000,000,3$

2

)12.1(

000,000,1$

1

)12.1(

000,500$

b. σ2NPV = 0.24($881,718 – $117,779)2 + 0.24(-$185,952 – $117,779)2

+ 0.12(-$376,709 – $117,779)2 + 0.4(-$10,000 – $117,779)2

= 198,078,470,853.

Answers and Solutions: 11 – 30

SOLUTION TO SPREADSHEET PROBLEM

11-18 The detailed solution for the problem is available in the file Ch 11 P18 Build a Model

Solution.xls at the textbook’s Web site.

Mini Case: 11 – 31

MINI CASE

Shrieves Casting Company is considering adding a new line to its product mix, and the

capital budgeting analysis is being conducted by Sidney Johnson, a recently graduated MBA.

The production line would be set up in unused space in Shrieves’ main plant. The

machinery’s invoice price would be approximately $200,000, another $10,000 in shipping

charges would be required, and it would cost an additional $30,000 to install the equipment.

The machinery has an economic life of 4 years, and Shrieves has obtained a special tax ruling

that places the equipment in the MACRS 3-year class. The machinery is expected to have a

salvage value of $25,000 after 4 years of use.

The new line would generate incremental sales of 1,250 units per year for 4 years at an

incremental cost of $100 per unit in the first year, excluding depreciation. Each unit can be

sold for $200 in the first year. The sales price and cost are expected to increase by 3% per

year due to inflation. Further, to handle the new line, the firm’s net working capital would

have to increase by an amount equal to 12% of sales revenues. The firm’s tax rate is 40%,

and its overall weighted average cost of capital is 10%.

a. Define “incremental cash flow.”

a. 1. Should you subtract interest expense or dividends when calculating project cash

flow?

Answer: The cash flow statement should not include interest expense or dividends. The return

a. 2. Suppose the firm had spent $100,000 last year to rehabilitate the production line

site. Should this cost be included in the analysis? Explain.

Answer: The $100,000 cost to rehabilitate the production line site was incurred last year, and

Mini Case: 11 – 32

a. 3. Now assume that the plant space could be leased out to another firm at $25,000

per year. Should this be included in the analysis? If so, how?

Answer: If the plant space could be leased out to another firm, then if Shrieves accepts this

a. 4. Finally, assume that the new product line is expected to decrease sales of the

firm’s other lines by $50,000 per year. Should this be considered in the analysis?

If so, how?

Answer: If a project affects the cash flows of another project, this is an “externality” that must be

b. Disregard the assumptions in part a. What is Shrieves’ depreciable basis? What

are the annual depreciation expenses?

Answer: The asset’s depreciable basis includes shipping and installation costs. Thus, the asset’s

Mini Case: 11 – 33

c. Calculate the annual sales revenues and costs (other than depreciation). Why is it

important to include inflation when estimating cash flows?

Answer: With an inflation rate of 3%, the annual revenues and costs are:

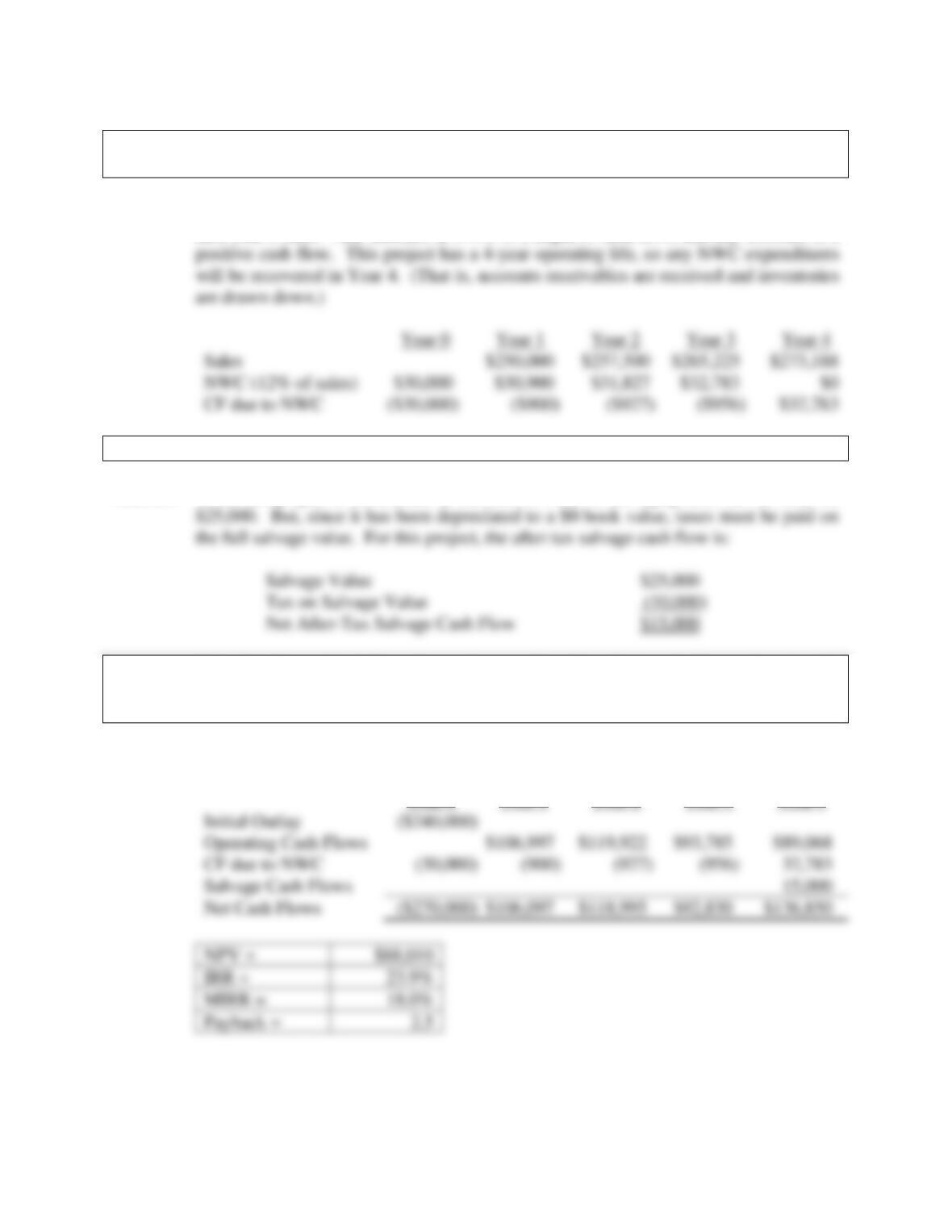

d. Construct annual incremental operating cash flow statements.

Answer:

Year 1

Year 2

Year 3

Year 4

Sales

$250,000

$257,500

$265,225

$273,188

Costs

Depreciation

Op. EBIT

$118,807

Taxes (40%)

EBIT(1 – T)

Depreciation

Net Operating CF

$106,997

$119,922

Mini Case: 11 – 34

e. Estimate the required net working capital for each year, and the cash flow due to

investments in net working capital.

Answer: The project requires a level of net working capital in the amount equal to 12% of the

next year’s sales. Any increase in NWC is a negative cash flow, and any decrease is a

f. Calculate the after-tax salvage cash flow.

Answer: When the project is terminated at the end of Year 4, the equipment can be sold for

g. Calculate the net cash flows for each year. Based on these cash flows, what are the

project’s NPV, IRR, MIRR, PI, payback, and discounted payback? Do these

indicators suggest the project should be undertaken?

Answer: The net cash flows are:

Year 0

Year 1

Year 2

Year 3

Year 4

Initial Outlay

($240,000)

Operating Cash Flows

$93,785

CF due to NWC

(30,000)

(900)

(927)

(956)

Salvage Cash Flows

NPV =

IRR =

MIRR =

Payback =

Sales

CF due to NWC

Mini Case: 11 – 35

h. What does the term “risk” mean in the context of capital budgeting; to what

extent can risk be quantified; and when risk is quantified, is the quantification

based primarily on statistical analysis of historical data or on subjective,

judgmental estimates?

Answer: Risk throughout finance relates to uncertainty about future events, and in capital

budgeting, this means the future profitability of a project. For certain types of projects,

Mini Case: 11 – 36

i. 1. What are the three types of risk that are relevant in capital budgeting?

2. How is each of these risk types measured, and how do they relate to one another?

Answer: Here are the three types of project risk:

• Stand-alone risk is the project’s total risk if it were operated independently. Stand–

i. 3. How is each type of risk used in the capital budgeting process?

Answer: Because management’s primary goal is shareholder wealth maximization, the most

Mini Case: 11 – 37

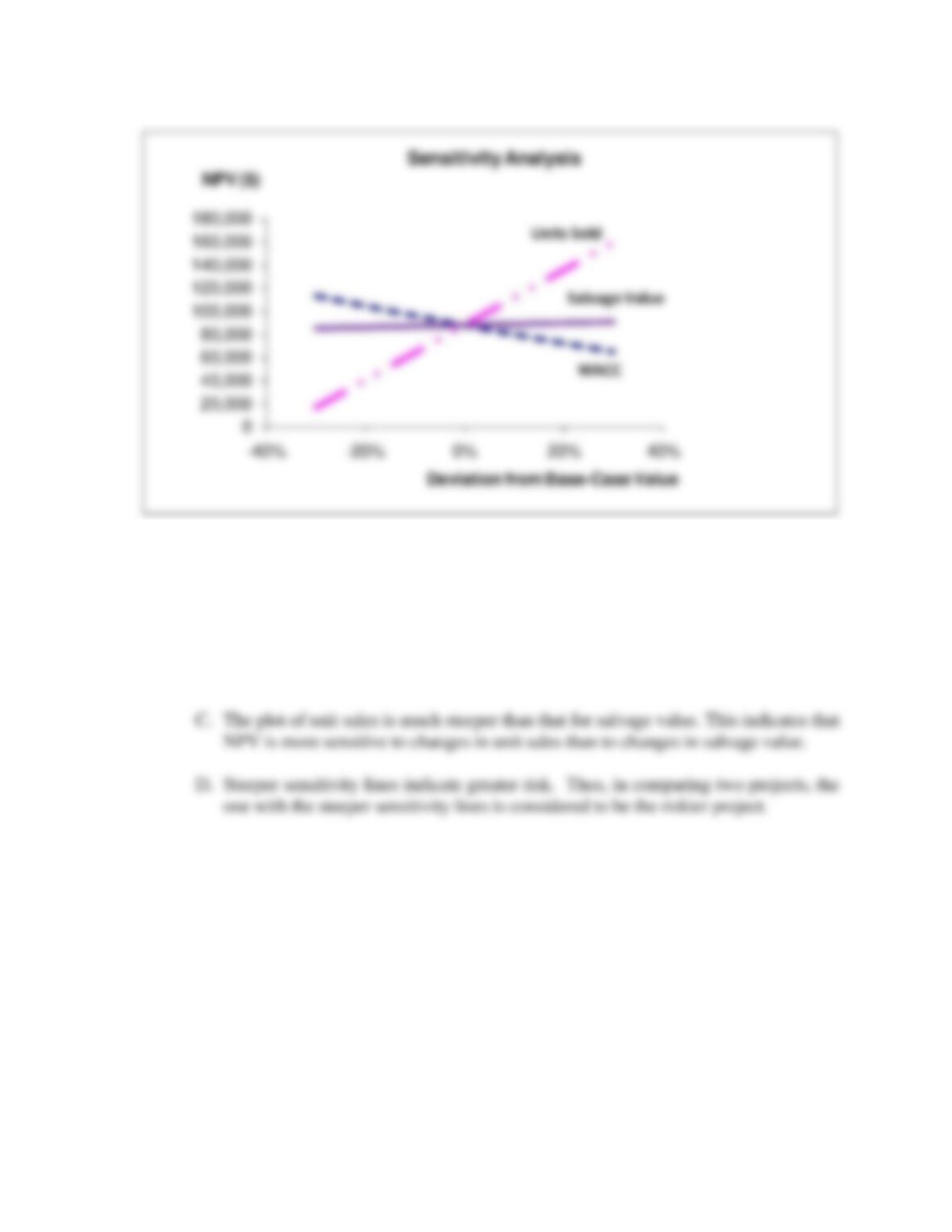

j. 1. What is sensitivity analysis?

Answer: Sensitivity analysis measures the effect of changes in a particular variable, say

revenues, on a project’s NPV. To perform a sensitivity analysis, all variables are fixed

j. 2. Perform a sensitivity analysis on the unit sales, salvage value, and cost of capital

for the project. Assume each of these variables can vary from its base-case, or

expected, value by 10%, 20%, and 30%. Include a sensitivity diagram, and

discuss the results.

Answer: The sensitivity data are given here in tabular form:

Mini Case: 11 – 38

A. The sensitivity lines intersect at 0% change and the base-case NPV, $88,030. Since

all other variables are set at their base-case, or expected, values the zero change

situation is the base case and gives the base-case NPV, $88,030.

B. The plots for unit sales and salvage value are upward sloping, indicating that higher

variable values lead to higher NPVs. Conversely, the plot for cost of capital is

downward sloping, because a higher cost of capital leads to a lower NPV.

Mini Case: 11 – 39

j. 3. What is the primary weakness of sensitivity analysis? What is its primary

usefulness?

Answer: The two primary disadvantages of sensitivity analysis are (1) that it does not reflect the

effects of diversification and (2) that it does not incorporate any information about the

k. Assume that Sidney Johnson is confident of her estimates of all the variables that

affect the project’s cash flows except unit sales and sales price. If product

acceptance is poor, unit sales would be only 900 units a year and the unit price

would only be $160; a strong consumer response would produce sales of 1,600

units and a unit price of $240. Sidney believes that there is a 25% chance of poor

acceptance, a 25% chance of excellent acceptance, and a 50% chance of average

acceptance (the base case).

k. 1. What is scenario analysis?

Answer: Scenario analysis examines several possible situations, usually worst case, most likely

Mini Case: 11 – 40

k. 2. What is the worst-case NPV? The best-case NPV?

k. 3. Use the worst-, base-, and best-case NPVs and probabilities of occurrence to find

the project’s expected NPV, standard deviation, and coefficient of variation.

Answer: We used a spreadsheet model to develop the scenarios, which are summarized below:

Scenario

Probability

Unit Sales

Unit Price

NPV

l. Are there problems with scenario analysis? Define simulation analysis, and

discuss its principal advantages and disadvantages.

Answer: Scenario analysis examines several possible scenarios, usually worst case, most likely

case, and best case. Thus, it usually considers only 3 possible outcomes. Obviously

Mini Case: 11 – 41

m. 1. Assume that Shrieves’ average project has a coefficient of variation in the range of

0.2 to 0.4. Would the new line be classified as high risk, average risk, or low risk?

What type of risk is being measured here?

Answer: The project has a CV of 1.15, which is above the average range of 0.2 to 0.4, so it falls

m. 2. Shrieves typically adds or subtracts 3 percentage points to the overall cost of

capital to adjust for risk. Should the new line be accepted?

Answer: Since the project is judged to have above-average risk, its differential risk-adjusted, or

m. 3. Are there any subjective risk factors that should be considered before the final

decision is made?

Answer: A numerical analysis such as this one may not capture all of the risk factors inherent in

Mini Case: 11 – 42

n. What is a real option? What are some types of real options?

Answer: Real options exist when managers can influence the size and risk of a project’s cash

flows by taking different actions during the project’s life in response to changing