Chapter 11: The Basics of Capital Budgeting

Comprehensive/Spreadsheet Problem

301

Comprehensive/Spreadsheet Problem

Note to Instructors:

The solution to this problem is not provided to students at the back of their text. Instructors

can access the

Excel

file on the textbook’s website.

11–23 a. Project A:

Using a financial calculator, enter the following data:

CF0 = -30; CF1 = 5; CF2 = 10; CF3 = 15; CF4 = 20; I/YR = 10; and solve for NPVA = $7.74;

IRRA = 19.19%.

Calculate MIRRA at WACC = 10%:

Step 1: Calculate the NPV of the uneven cash flow stream, so its FV can then be calculated.

With a financial calculator, enter the cash flow stream into the cash flow registers,

then enter I/YR = 10, and solve for NPV = $37.739.

Payback A (cash flows in millions):

Annual

Period Cash Flows Cumulative

0 ($30) ($30)

4 20 20

PaybackA = 3 years.

Discounted Payback A (cash flows in millions):

Annual Discounted @10% Cumulative

Period Cash Flows Cash Flows Cash Flows

0 ($30) ($30.00) ($30.00)

Project B:

Using a financial calculator, enter the following data:

Calculate MIRRB at WACC = 10%:

Step 1: Calculate the NPV of the uneven cash flow stream, so its FV can then be calculated.

With a financial calculator, enter the cash flow stream into the cash flow registers,

then enter I/YR = 10, and solve for NPV = $36.55.

Step 2: Calculate the FV of the cash flow stream as follows:

Payback B (cash flows in millions):

Annual

Period Cash Flows Cumulative

0 ($30) ($30)

1 20 (10)

PaybackB = 2 years.

Discounted Payback B (cash flows in millions):

Annual Discounted @10% Cumulative

Period Cash Flows Cash Flows Cash Flows

0 ($30) ($30.00) ($30.00)

Summary:

Project A Project B

NPV $7.74 $6.55

MIRR 16.50% 15.57%

Payback 3 years 2 years

Discounted Payback 3.43 years 2.59 years

Chapter 11: The Basics of Capital Budgeting

Comprehensive/Spreadsheet Problem

303

d. WACC NPVA NPVB

0% $20.00 $14.00

5 13.24 9.96

15 3.21 3.64

22.52 (2.23) 0

-5

20

25

NPV

($)

Project A

e. At WACC = 5% and the two projects are mutually exclusive, NPVA > NPVB so choose Project

A. This doesn’t change our recommendation. At WACC = 15% and the two projects are

mutually exclusive, NPVB > NPVA so choose Project B. This does change our

recommendation. Both decisions can be made from looking at the NPV profile in part d.

304

Comprehensive/Spreadsheet Problem

Chapter 11: The Basics of Capital Budgeting

i. The cutoff chosen for both payback periods is arbitrary—but usually based on specific

information the firm has on past projects. However, the criteria for the NPV and the IRR

methods are not arbitrary.

j. The MIRR is the discount rate at which the present value of a project’s cost is equal to the

present value of its terminal value, where the terminal value is found as the sum of the

Chapter 11: The Basics of Capital Budgeting

Integrated Case

305

11–24

Allied Components Company

Basics of Capital Budgeting

You recently went to work for Allied Components Company, a supplier of auto

repair parts used in the after–market with products from Daimler AG, Ford,

Toyota, and other automakers. Your boss, the chief financial officer (CFO), has

just handed you the estimated cash flows for two proposed projects. Project L

involves adding a new item to the firm’s ignition system line; it would take

some time to build up the market for this product, so the cash inflows would

increase over time. Project S involves an add–on to an existing line, and its cash

flows would decrease over time. Both projects have 3-year lives because Allied

is planning to introduce entirely new models after 3 years.

Here are the projects’ after-tax cash flows (in thousands of dollars):

0 1 2 3

| | | |

Project L –100 10 60 80

Project S –100 70 50 20

Depreciation, salvage values, net operating working capital requirements, and

tax effects are all included in these cash flows. The CFO also made subjective

risk assessments of each project, and he concluded that both projects have

risk characteristics that are similar to the firm’s average project. Allied’s

WACC is 10%. You must determine whether one or both of the projects

should be accepted.

A. What is capital budgeting? Are there any similarities between a firm’s

capital budgeting decisions and an individual’s investment decisions?

1. Estimate the cash flows—interest and maturity value or

2. Assess the riskiness of the cash flows.

3. Determine the appropriate discount rate, based on the riskiness

5. If the PV of the inflows is greater than the PV of the outflows

(the NPV is positive), or if the calculated rate of return (the IRR)

is higher than the project cost of capital, accept the project.

B. What is the difference between independent and mutually exclusive

projects? Between projects with normal and nonnormal cash flows?

Chapter 11: The Basics of Capital Budgeting

Integrated Case

307

-100.00 10 60 80

49.59

18.79 = NPVL

308

Integrated Case

Chapter 11: The Basics of Capital Budgeting

the project’s NPV, $18.78 (note the penny rounding difference). The

NPV of Project S is NPVS = $19.98.

C. (2) What is the rationale behind the NPV method? According to NPV,

which project(s) should be accepted if they are independent?

Mutually exclusive?

(3) to still have $18.78 left over on a present value basis. This

$18.78 if Project L is accepted. Similarly, Allied’s shareholders gain

$19.98 in value if Project S is accepted.

If Projects L and S are independent, then both should be

accepted, because both add to shareholders’ wealth, hence to the

stock price. If the projects are mutually exclusive, then Project S

should be chosen over L, because S adds more to the value of the firm

than L does.

Chapter 11: The Basics of Capital Budgeting

Integrated Case

309

C. (3) Would the NPVs change if the WACC changed? Explain.

-100.00 10 60 80

43.02

0.06 $0 if IRRL = 18.1% is used as the discount rate.

Therefore, IRRL ≈ 18.1%.

A financial calculator is extremely helpful when calculating IRRs.

The cash flows are entered sequentially, and then the IRR button is

pressed. For Project S, IRRS ≈ 23.6%. Note that with many

calculators, you can enter the cash flows into the cash flow register,

also enter WACC = I/YR, and then calculate both NPV and IRR by

pressing the appropriate buttons.

D. (2) How is the IRR on a project related to the YTM on a bond?

than 23.6%.

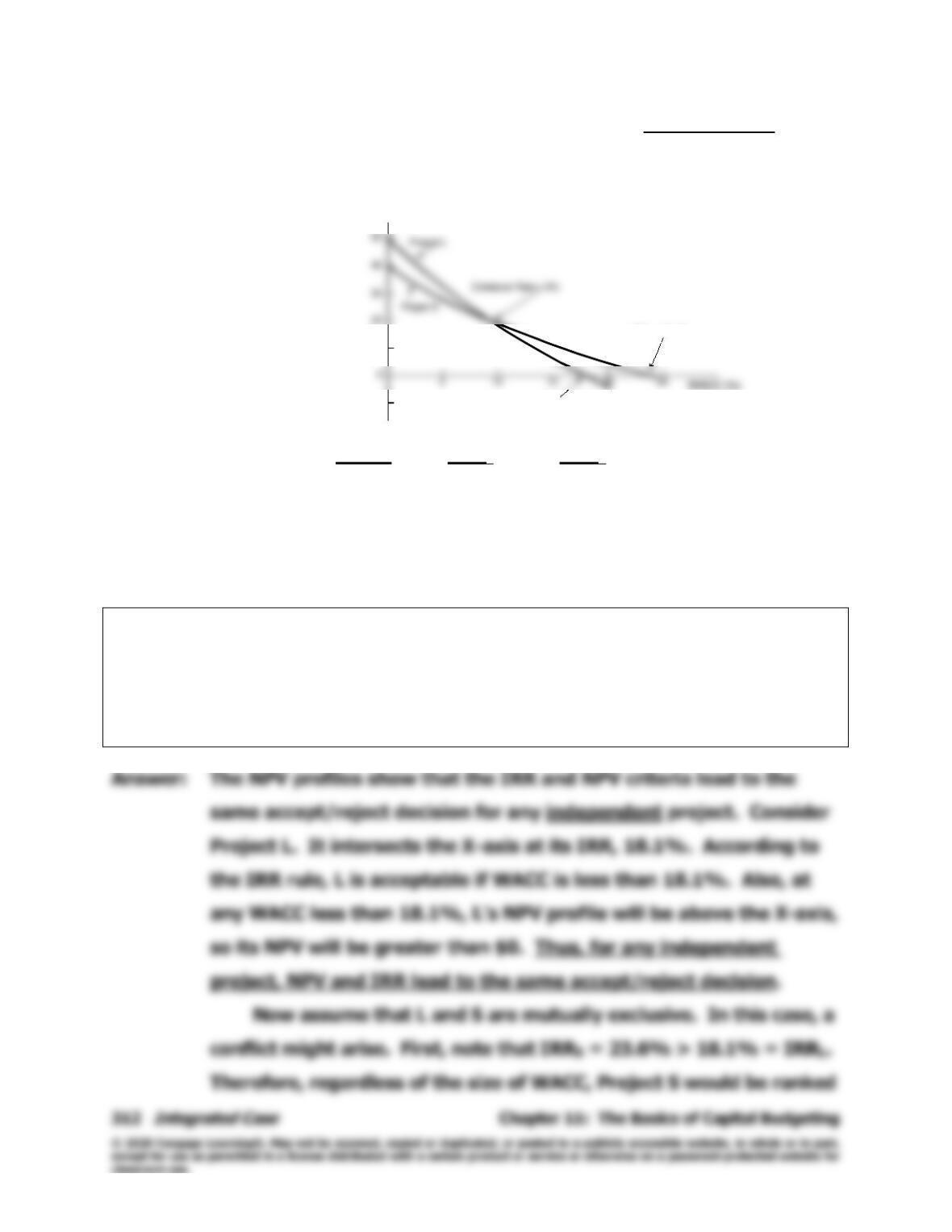

E. (1) Draw NPV profiles for Projects L and S. At what discount rate do

the profiles cross?

1. The Y-intercept is the project’s NPV when WACC = 0%. This is

$50 for L and $40 for S.

23.6% for S.

3. NPV profiles are curves rather than straight lines. To see this,

4. From the figure below, it appears that the crossover rate is

between 8% and 9%.

NPV

($)

10

–10

IRRS= 23.6%

IRRL= 18.1%

NPV

($)

10

–10

IRRS= 23.6%

IRRL= 18.1%

NPV

($)

10

–10

IRRS= 23.6%

IRRL= 18.1%

WACC NPVL NPVS

0% $50 $40

5 33 29

10 19 20

15 7 12

20 (4) 5

E. (2) Look at your NPV profile graph without referring to the actual NPVs

and IRRs. Which project(s) should be accepted if they are

independent? Mutually exclusive? Explain. Are your answers

correct at any WACC less than 23.6%?

Chapter 11: The Basics of Capital Budgeting

Integrated Case

313

they both implicitly assume some discount rate. Inherent in the NPV

calculation is the assumption that cash flows can be reinvested at

the project’s cost of capital, while the IRR calculation assumes

reinvestment at the IRR rate.

F. (3) Which method is best? Why?

Chapter 11: The Basics of Capital Budgeting

Integrated Case

315

12.10

TV of inflows = 158.10

PV of TV = 100.00 MIRR = ?

$100 =

10.158$

158.1, and then press I/YR to get the answer, MIRRL = 16.5%. We

could calculate MIRRS similarly: MIRRS = 16.9%. Thus, Project S is

ranked higher than L. This result is consistent with the NPV decision.

G. (2) What are the MIRR’s advantages and disadvantages as compared to

the NPV?

316

Integrated Case

Chapter 11: The Basics of Capital Budgeting

where executives from DuPont and Hershey, among others, all

reported a switch from IRR to MIRR.

H. (1) What is the payback period? Find the paybacks for Projects L and S.

–100 10 60 80

–90 –30 50

Project L’s $100 investment has not been recovered at the end of

Year 2, but it has been more than recovered by the end of Year 3.

Thus, the recovery period is between 2 and 3 years. If we assume

that the cash flows occur evenly over the year, then the investment

is recovered $30/$80 = 0.375 ≈ 0.4 into Year 3. Therefore,

PaybackL = 2.4 years. Similarly, PaybackS = 1.6 years.

H. (2) What is the rationale for the payback method? According to the

payback criterion, which project(s) should be accepted if the firm’s

maximum acceptable payback is 2 years, if Projects L and S are

independent? If Projects L and S are mutually exclusive?

Chapter 11: The Basics of Capital Budgeting

Integrated Case

317

318

Integrated Case

Chapter 11: The Basics of Capital Budgeting

yields over the cost of capital, the payback merely tells us when we

get our investment back. Discounted payback does consider the

time value of money, but it still fails to consider cash flows after the

payback period and it gives us no specific decision rule for

-0.8 5.0 -5.0

The project is estimated to be of average risk, so its WACC is 10%.

I. (1) What is Project P’s NPV? What is its IRR? Its MIRR?

-800,000 5,000,000 -5,000,000

NPVP = -$386,776.86.

Chapter 11: The Basics of Capital Budgeting

Integrated Case

319

We can find the NPV by entering the cash flows into the cash flow

register, entering I/YR = 10, and then pressing the NPV button.

However, calculating the IRR presents a problem. With the cash

flows in the register, press the IRR button. An HP–10BII financial

calculator will give the message “error–soln.” This means that

Project P has multiple IRRs. An HP–17BII will ask for a guess. If

you guess 10%, the calculator will show IRR = 25%. If you guess

a high number, such as 200%, it will show the second IRR, 400%.1

The MIRR of Project P = 5.6%, and it is found by calculating the

discount rate that equates the terminal value ($5.5 million) to the

present value of costs ($4.93 million).

I. (2) Draw Project P’s NPV profile. Does Project P have normal or

nonnormal cash flows? Should this project be accepted? Explain.

Since Project P’s NPV is negative, the project should be

rejected, even though both IRRs (25% and 400%) are greater than

the project’s 10% WACC. The MIRR of 5.6% also supports the

–250

–250

–250

–250