Chapter 10

COMPETITIVE MARKETS

QUESTIONS AND ANSWERS

Q10.1 Historically, the Regional Bell Operating Companies (RBOCs) had a monopoly on the

provision of local voice phone service. Regulation has now been eased to permit

competition from Competitive Local Exchange Carriers (CLECs), cable companies,

satellite operators and wireless competitors. Is the local phone service market likely to

become a vigorously competitive market?

Q10.1 ANSWER

The local voice phone service market is not one likely to support dozens of competitors

in each local market, but competition among the few can become vigorous in this

market. Market structure is described in terms of the complete array of industry

Q10.2 One way of inferring competitive conditions in a market is to consider the lifestyle

enjoyed by employees and owners. In vigorously competitive markets, employee

compensation tends to be meager and profits are apt to be slim. Describe the perfectly

competitive market structure and provide some examples.

Q10.2 ANSWER

Perfect competition is a market structure characterized by a large number of buyers and

Competitive Markets 289

Q10.3 Competitive firms are sometimes criticized for costly but superfluous product

differentiation. Is there an easy means for determining if such efforts are in fact

wasteful?

Q10.3 ANSWER

Q10.4 The Worker Adjustment and Retraining Notification Act (WARN) requires employers

with 100 or more employees to provide notification 60 calendar days in advance of plant

closings and mass layoffs. Advance notice gives workers and their families transition

time to adjust to the prospective loss of employment, seek other jobs, or get necessary

training. Some employers complain that WARN reduces necessary flexibility and makes

them reluctant to open new production facilities. How are barriers to entry and exit

similar? How are they different?

Q10.4 ANSWER

A barrier to entry is defined as any factor or industry characteristic that creates an

advantage for incumbents over new arrivals. Legal rights such as patents and local,

290 Chapter 10

Whereas barriers to entry have the potential to impede competition by making

entry or growth difficult, competitive forces can also be diminished through barriers to

exit. A barrier to exit is any restriction on the ability of incumbents to redeploy assets

from use in one industry or line of business to another. During the late 1980s, for

example, several state governments initiated legal proceedings in order to impede plant

Q10.5 “A higher minimum wage means some low wage workers will get fired because there

will be less money available for labor costs. An international minimum wage, scaled

according to the working conditions and cost of living in a particular country, would

allow local workers to benefit without significant trade disruption.” Discuss this

statement and explain why the demand curve is apt to be horizontal in the unskilled

labor market.

Q10.5 ANSWER

In competitive markets, the demand curve tends to be horizontal because homogeneous

products are offered by several competitors. In product markets, firms are price takers in

Competitive Markets 291

paid more.

Q10.6 “For smaller firms managed by their owners in competitive markets, profit

considerations are apt to dominate almost all decisions. However, managers of giant

corporations have little contact with stockholders, and often deviate from profit–

maximizing behavior. Get real. Look at Tyco, for Pete’s sake.” Discuss this statement.

Q10.6 ANSWER

This is, of course, a controversial subject. Most analysts concede that profit

maximization is a prime concern of owner-managers that run small businesses in hotly

competitive markets. In vigorously competitive markets, productive efficiency is

Q10.7 “If excess profits are rampant in the oil business, why aren’t the stockholders of industry

giants like Exxon Mobil, Chevron Texaco, and Royal Dutch Petroleum making huge

stock-market profits?” Discuss this statement.

Q10.7 ANSWER

The stock market is a forward-looking device. If anticipated profits rise, stock prices go

292 Chapter 10

Q10.8 “Airline passenger service is a terrible high-fixed cost business featuring fierce price

competition. With uniform safety, customers pick the lowest airfare with the most

convenient departures. Except for pilots, nobody in the airline business makes any

money.” Use the competitive firm short-run supply curve concept to explain entry and

exit in the airline passenger business. Why are pilots so well paid?

Q10.8 ANSWER

An individual airline will supply output so long as it is profitable to do so. Profits are

maximized by setting MR = MC. Because P = MR in a competitive industry, perfectly

Competitive Markets 293

Q10.9 Suppose that a competitive firm long-run supply curve is given by the expression QF = –

500 + 10P. Does this mean that the firm will supply -500 units of output at a zero

price? If so, what does output of -500 units mean?

Q10.9 ANSWER

Taken literally, a competitive firm long-run supply curve given by the expression QF = –

Q10.10 The long-run supply curve for a given competitive firm can be written as QF = -250 +

8P or P = $31.25 + $0.125QF. Explain why the amount supplied by 50 such

competitors is determined by multiplying the first expression by 50 rather than by

multiplying the second expression by a similar amount.

Q10.10 ANSWER

The amount supplied in a competitive market is simply the sum of output produced by

all established competitors. In a market comprised of 50 firms with identical costs, the

SELF-TEST PROBLEMS AND SOLUTIONS

ST10.1 Market Supply. In some markets, cutthroat competition can exist even when the market

is dominated by a small handful of competitors. This usually happens when fixed costs

294 Chapter 10

are high, products are standardized, price information is readily available, and excess

capacity is present. Airline passenger service in large city-pair markets, and electronic

components manufacturing are good examples of industries where price competition

A. Using each firm’s marginal cost curve, calculate the profit-maximizing short-run supply

from each firm at the competitive market prices indicated in the following table. For

simplicity, assume price is greater than average variable cost in every instance.

Market Supply is the Sum of Firm Supply Across all Competitors

Firm One

Supply

Firm Two

Supply

Firm Three

Supply

Market Supply

Price

2,500P

500P

5,000P

+ Q2 + Q3)

$0

5

10

15

20

25

30

40

45

50

55

60

Competitive Markets 295

ST10.1 SOLUTION

A. The marginal cost curve constitutes the short-run supply curve for firms in perfectly

competitive markets so long as price is greater than average variable cost.

Market Supply is the Sum of Firm Supply Across all Competitors

Firm One

Supply

Firm Two

Supply

Firm Three

Supply

Market Supply

Price

2,500P

500P

5,000P

+ Q2 + Q3)

$0

-12,500

-7,500

-5,000

-25,000

5

0

-5,000

20,000

15,000

10

12,500

-2,500

45,000

55,000

15

25,000

0

70,000

95,000

20

37,500

2,500

95,000

135,000

25

50,000

5,000

120,000

175,000

30

62,500

7,500

145,000

215,000

35

75,000

10,000

170,000

255,000

40

87,500

12,500

195,000

295,000

45

100,000

15,000

220,000

335,000

296 Chapter 10

B.

Market Supply is the Sum of Firm Supply Across all Competitors

$70

$80

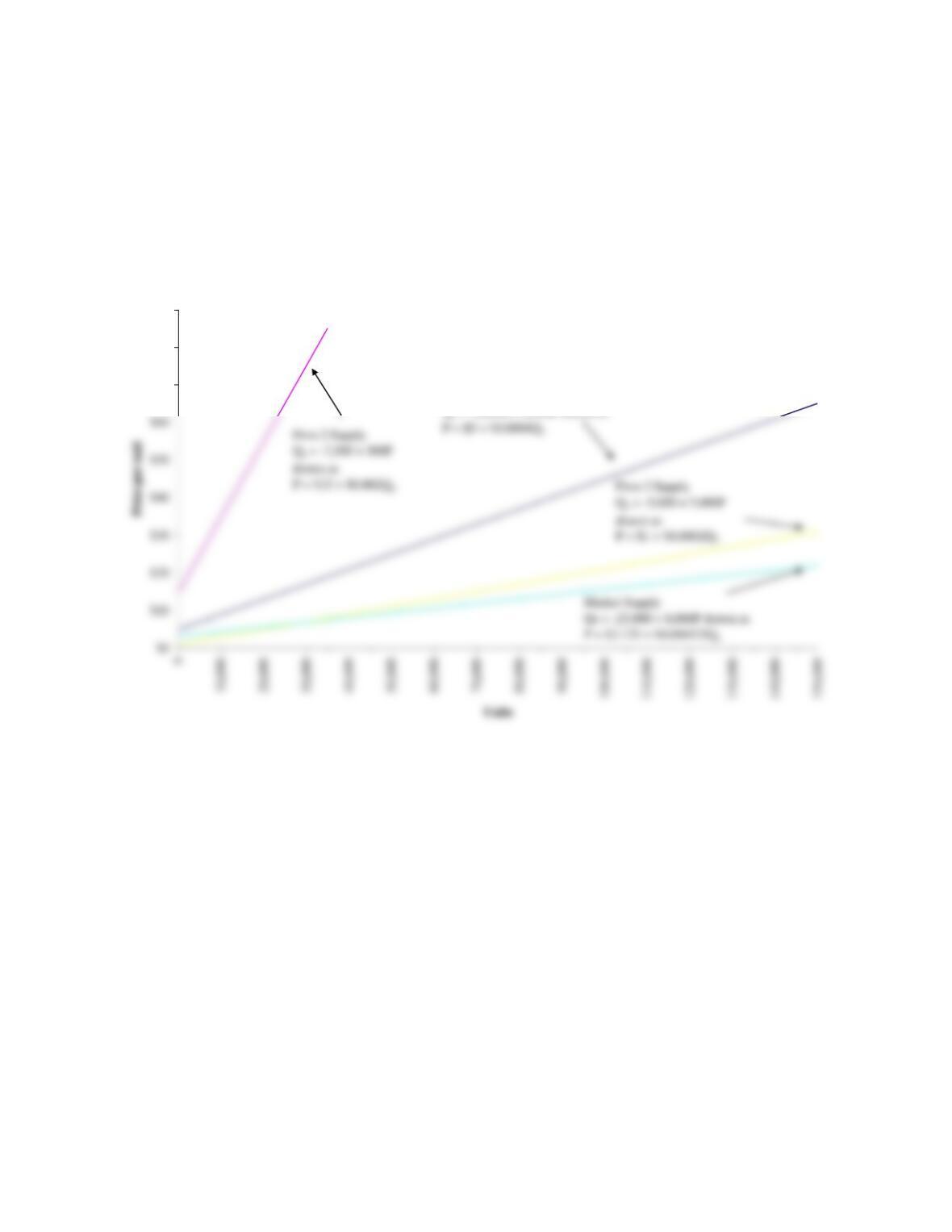

$90

Firm 1 Supply

Q1 = -12,500 + 2,500P drawn as

Market supply is the total amount supplied by all

competitors.

ST10.2 Competitive Market Equilibrium. Competitive market prices are determined by the

interplay of aggregate supply and demand; individual firms have no control over price.

Market demand reflects an aggregation of the quantities that customers will buy at each

or equivalently, when output is expressed as a function of price

QD = 400,000 – 10,000P

Assume market supply is provided by five competitors producing a standardized product

(Q). Firm supply schedules are as follows:

Q1 = 18 +2P (Firm 1)

A. Calculate the optimal quantity supplied by each firm at the competitive market prices

indicated in the following table. Then, assume there are actually 1,000 firms just like

each one illustrated in the table. Use this information to complete the Partial Market

Supply and Total Market Supply columns.

Quantity Supplied by

Firm (000)

Price

1

+ 2

+ 3

+ 4

+ 5

= Partial Market Supply ×

1,000

= Total Market

Supply (000)

$1

298 Chapter 10

B. Sum the individual firm supply curves to derive the market supply curve. Plot the market

demand and market supply curve with price as a function of output to illustrate the

equilibrium price and level of output. Verify that this is indeed the market equilibrium

price-output combination algebraically.

ST9.2 SOLUTION

A.

Quantity Supplied by Firm

(000)

Price

1

+ 2

+ 3

+ 4

+ 5

= Partial Market Supply ×

1,000

= Total

Market

Supply (000)

$1

20

18

52

32

18

140

140,000

2

22

24

64

44

26

180

180,000

6

30

48

112

92

58

340

340,000

7

32

54

124

104

66

380

380,000

The data in the table illustrate the process by which an industry supply curve is

constructed. First, suppose that each of five firms in an industry is willing to supply

Competitive Markets 299

B. To find the market supply curve, simply sum each individual firm’s supply curve, where

quantity is expressed as a function of the market price:

Plotting the market demand curve and the market supply curve allows one to determine

P = $6

To find the market equilibrium quantity, set equal the market demand and market

supply curves where price is expressed as a function of quantity, and QD = QS:

300 Chapter 10

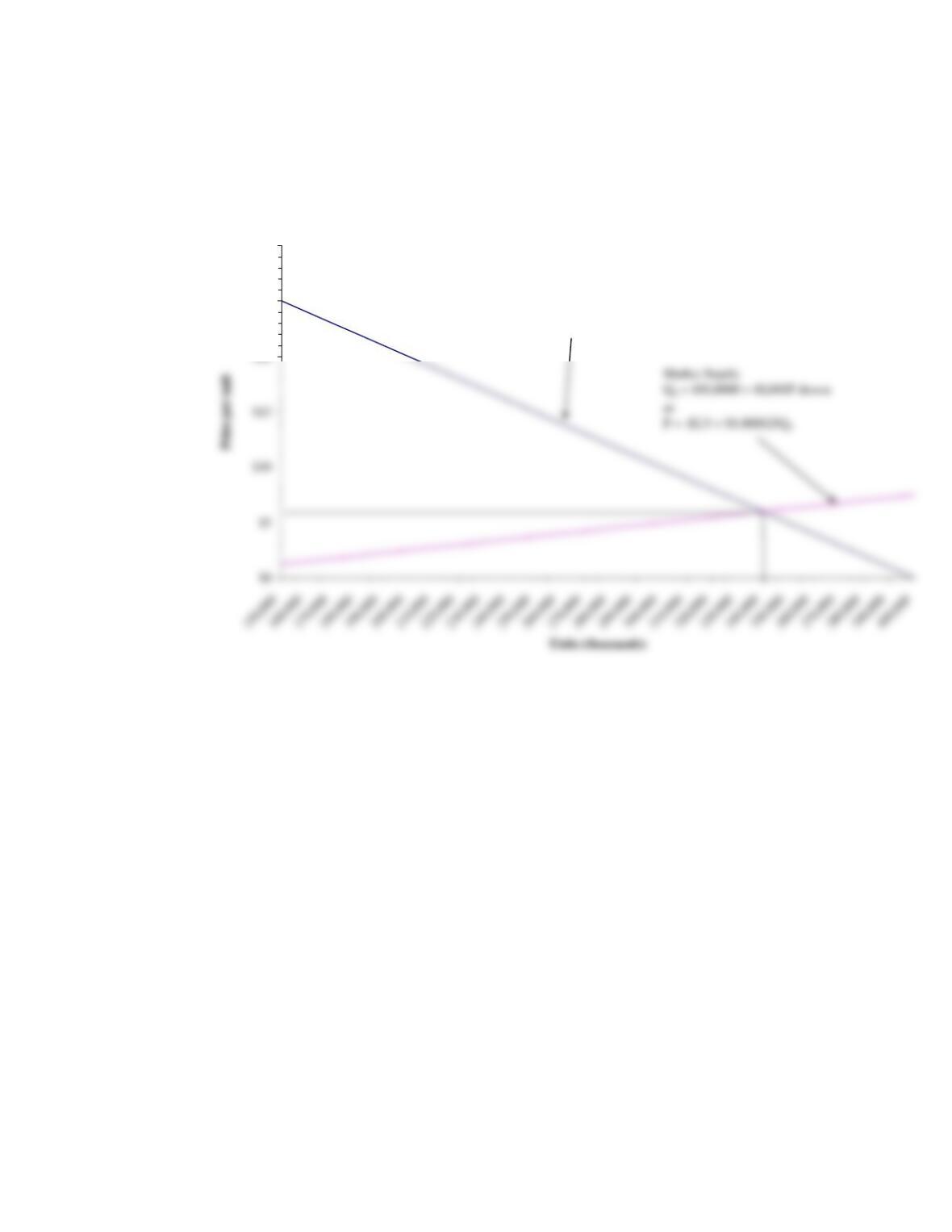

Market Equilibrium

$20

$25

$30

Market Demand

QD = 400,0000 – 10,000P drawn as

P = $40 – 0.0001QD

PROBLEMS AND SOLUTIONS

P10.1 Competitive Markets Concepts. Indicate whether each of the following statements is

true or false, and explain why.

A. In long-run equilibrium, every firm in a perfectly competitive industry earns zero

profit.

B. Perfect competition exists in a market when all firms are price takers as opposed

to price makers.

C. In competitive markets, P > MC at the profit-maximizing output level.

D. Downward-sloping industry demand curves characterize perfectly competitive

markets.

E. A firm might show accounting profits in a competitive market but be suffering

economic losses.

Competitive Markets 301

P10.1 SOLUTION

marginal revenue and marginal cost are equal. With price constant, average revenue

equals marginal revenue. Therefore, maximum profits result when market price is set

equal to marginal cost for firms in a perfectly competitive industry

insufficient to provide an adequate return to the firm’s stockholders. In such instances,

firms are unable to replace plant and equipment and will exit the industry in the long

run.

P10.2 Short-run Firm Supply. Mankato Paper, Inc., produces uncoated paper used in a wide

variety of industrial applications. Newsprint, a major product, is sold in a perfectly

competitive market. The following relation exists between the firm’s newsprint output

and total production costs:

Total Output

(tons)

Total Cost

0

$25

1

75

2

3

4

5

302 Chapter 10

Total Output

(tons)

Total Cost

7

600

A. Construct a table showing Mankato’s marginal cost of newsprint production.

B. What is the minimum price necessary for Mankato to supply one ton of newsprint?

C. How much newsprint would Mankato supply at industry prices of $75 and $100

per ton?

P10.2 SOLUTION

A.

Total

Output

Total

Cost

Marginal

Cost

0

$25

—

C. In a perfectly competitive market, P = MR. Therefore, Mankato will supply output so

P10.3 Short-run Firm Supply. Florida is the biggest sugar-producing state, but Michigan and

Minnesota are home to thousands of sugar beet growers. Sugar prices in the United

States average about 20¢ per pound, or more than double the world-wide average of

less than 10¢ per pound given import quotas that restrict imports to about 15% of the

U.S. market. Still, the industry is perfectly competitive for U.S. growers who take the

1

2

135

3

205

4

285

5

375

6

475

7

600

Competitive Markets 303

market price of 20¢ as fixed. Thus, P = MR = 20¢ in the U.S. sugar market. Assume

that a typical sugar grower has fixed costs of $30,000 per year. Total variable cost

(TVC), total cost (TC), and marginal cost (MC) relations are:

TVC = $15,000 + $0.02Q + $0.00000018Q2

A. Using the firm’s marginal cost curve, calculate the profit-maximizing short-run

supply curve for a typical grower.

B. Calculate the average variable cost curve for a typical grower, and verify that

average variable costs are less than price at this optimal activity level.

P10.3 SOLUTION

A. The marginal cost curve constitutes the short-run supply curve for firms in perfectly

B. The average variable cost curve is determined by dividing total variable cost by output: