Basic Econometrics, Gujarati and Porter

CHAPTER 10:

MULTICOLLINEARITY: WHAT HAPPENS IF THE REGRESSORS ARE

CORRELATED?

10.1 If X

k

is a perfect linear combination of the remaining explanatory

10.2 (a) No. Variable X

3i

is an exact linear combination of X

2i

, because

3 2

2 1.

i i

X X

= −

10.3 (a) Although the numerical values of the intercept and the slope

coefficients of PGNP and FLR have changed, their signs have not.

Also, these variables are still statistically significant. These changes

are due to the addition of the TFR variable, suggesting that there may

10.4 The relation may be rewritten as:

32

1 2 3 12.3 2 13.2 3

1 1

i i i i i

X X X X X

λ

λ

β β

λ λ

= − − = +

Therefore,

2 1

12.3 12.3 21.3

1 2

ˆ ˆ

( )( ) 1

r sqrt

λ λ

β β λ λ

= = − − = ±

10.5 (

a

) Yes. Economic time series data tend to move in the same

10.6 When wealth is removed from the model, the model is misspecified

and the income effect coefficient is biased. Hence, what one

observes in Eq. (10.6.4 ) is a biased estimate of the income

coefficient. The nature of the bias is as follows:

111

10.7 As discussed in Question 10.5, economic variables are often

10.8 (

a

) Yes. This is because the coefficient of correlation is zero

(

b

) It will be a combination, as shown below:

(c) No, for the following reasons:

10.9

(a) The correlation coefficient between labor and capital is about

112

will change the values of the other coefficients

(c) False. As noted in the chapter (see Eq. 7.5.6), the variance of

an OLS estimator is given by the following formula:

Basic Econometrics, Gujarati and Porter

10.13 (a) Referring to Eq. (7.11.5), we see that if all the r

2

‘s are zero,

10.14 (a) Consider Eq. (7.11.5). If all the zero-order, or gross, correlations

10.15

(a) If there is perfect multicollinearity, (

X‘X

) becomes singular

10.16

(a) Since in the case of perfect multicollinearity the (

X’X

) matrix

Basic Econometrics, Gujarati and Porter

114

10.19

(a) Since the third regressor, (

1

t t

M M

−

−) is a linear combination of

(b) If we re-specify the model as

10.20

Recall that

10.21

When there is perfect collinearity,

23

1

r

=

. Therefore, the

10.22

Recall that

ˆ ˆ ˆ ˆ ˆ ˆ

( ) [var( ) var( ) 2cov( , )]

se

β β β β β β

+ = + +

10.23

(a) Ceteris paribus, as

2

k

σ

increases, the variance of the estimated

Basic Econometrics, Gujarati and Porter

10.24

(a) Given the relatively high R

2

of 0.97, the significant F value and

(b) A priori, capital is expected to have positive impact on output. It

(c) It is a Cobb-Douglas type production function, as the given

(e) This equation implicitly assumes that there are constant returns

(g) As mentioned in (e), the author is trying to find out if there are

Basic Econometrics, Gujarati and Porter

116

Empirical Exercises

10.26

(a) The regression results of the modified model are:

ˆ

20.995 0.710

Y Z

= +

10.27

(a)

Dependent Variable: LIMPORTS

Method: Least Squares

Date: 11/11/00 Time: 10:16

Sample: 1970 1998

Included observations: 29

Variable Coefficient

Std. Error

t-Statistic

Prob.

C 1.975260

0.782070

2.525683

0.0180

Basic Econometrics, Gujarati and Porter

117

Variable Coefficient Std. Error t-Statistic Prob.

R-squared 0.992005 Mean dependent var 13.08472

(c)

Dependent Variable: LN_IMPORTS

Sample: 1975 2005

Included observations: 31

Dependent Variable: LN_IMPORTS

Sample: 1975 2005

Included observations: 31

R-squared 0.962795 Mean dependent var 13.08472

Basic Econometrics, Gujarati and Porter

118

Dependent Variable: LN_GDP

Sample: 1975 2005

Included observations: 31

Variable Coefficient Std. Error t-Statistic Prob.

R-squared 0.985573 Mean dependent var 8.569723

Adjusted R-squared 0.985075 S.D. dependent var 0.586128

(d) The best solutions here would be to express imports and GDP in real terms by

dividing each by CPI (recall the ratio method discussed in the chapter). The results

are as follows:

Dependent Variable: LN(IMP/CPI)

Variable Coefficient Std. Error t-Statistic Prob.

C 1.442445 0.221017 6.526390 0.0000

R-squared 0.970841 Mean dependent var 8.299204

10.28

(a) Since there are five explanatory variables, there will be five

Basic Econometrics, Gujarati and Porter

119

Dependent Variable R

2

10.29

(a) and (c)Examining the correlation coefficients between the

possible explanatory variables, one observes a very high correlation

:

Dependent Variable: LY

Method: Least Squares

Sample: 1971 1986

Included observations: 16

Variable Coefficient

Std. Error

t-Statistic

Prob.

C -22.10374

8.373593

-2.639696

0.0216

(b) If we include all the X variables, we obtain the following results:

Basic Econometrics, Gujarati and Porter

Dependent Variable: LOG(Y)

Method: Least Squares

Sample: 1971 1986

Included observations: 16

Variable Coefficient

Std. Error

t-Statistic

Prob.

LOG(X2) 1.790153

0.873240

2.050012

0.0675

LOG(X4) 2.127199

1.257839

1.691154

0.1217

LOG(X6) 0.277792

2.036975

0.136375

0.8942

R-squared 0.854803

Mean dependent var 9.204273

10.30

First, we present the correlation matrix of the regressors:

RATE ERSP ERNO NEIN ASSET AGE DEP SCHOOL

ERSP 0.571693 1.000000 -0.040994 0.234426 0.274094 -0.015300 –0.692881 0.549108

NEIN 0.701787 0.234426 0.359094 1.000000 0.987510 0.502432 -0.520832 0.539173

AGE 0.044173 -0.015300 0.775494 0.502432 0.417086 1.000000 -0.048360 -0.331067

Note: Treat the last row in the preceding table as the last column

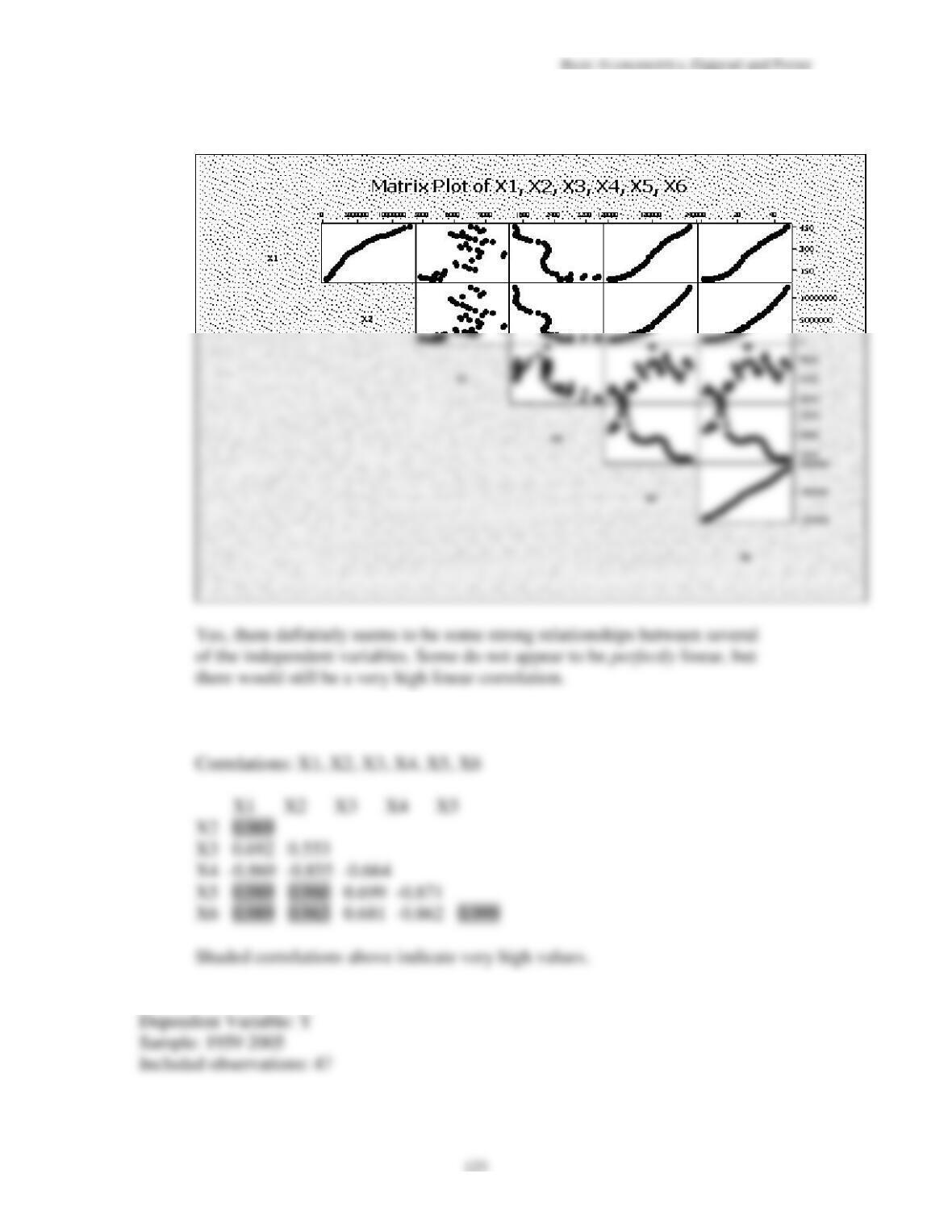

As this table shows, the pairwise, or gross, correlations range from

Basic Econometrics, Gujarati and Porter

121

(a)

Regressing hours of work on all the regressors, we get the

following results:

Dependent Variable: HRS

Method: Least Squares

Sample: 1 35

Included observations: 35

Variable Coefficient

Std. Error

t-Statistic

Prob.

C 1904.578

251.9333

7.559849

0.0000

RATE -93.75255

47.14500

-1.988600

0.0574

R-squared 0.825555

Mean dependent var 2137.086

Adjusted R-squared 0.771879

S.D. dependent var 64.11542

(c)

To save space, we will compute the VIF and TOL only

(d)

Not all the variables are necessary in the model. Using one

10.31

This is for a class project.

Basic Econometrics, Gujarati and Porter

122

Dependent Variable: Y

Method: Least Squares

Sample: 1947 1961

Included observations: 15

Variable Coefficient Std. Error t-Statistic Prob.

C -3017441. 939728.1 -3.210973 0.0124

X1 –20.51082 87.09740 -0.235493 0.8197

R-squared 0.9955 Adjusted R-squared 0.9921

S.E. of regression 295.6219

10.33

(a)

(b)

The correlation matrix for the independent variables is:

(c) and (d)

Basic Econometrics, Gujarati and Porter

Variable Coefficient Std. Error t-Statistic Prob.

C -11304.74 9963.786 -1.134583 0.2633

X1 87.45286 6.649853 13.15110 0.0000

R-squared 0.999398 Mean dependent var 101822.8

10.34

(a)

(b)

Dependent Variable: TASTE

Basic Econometrics, Gujarati and Porter

125

Variable Coefficient Std. Error t-Statistic Prob.

R-squared 0.587826 Mean dependent var 24.53333

Adjusted R-squared 0.557294 S.D. dependent var 16.25538

(c)

Variable Coefficient Std. Error t-Statistic Prob.

R-squared 0.651702 Mean dependent var 24.53333

Adjusted R-squared 0.625903 S.D. dependent var 16.25538

(d)

Dependent Variable: TASTE

Sample: 1 30

Included observations: 30

Variable Coefficient Std. Error t-Statistic Prob.

C -34.13491 15.67628 -2.177488 0.0387

Basic Econometrics, Gujarati and Porter

126

R-squared 0.655190 Mean dependent var 24.53333

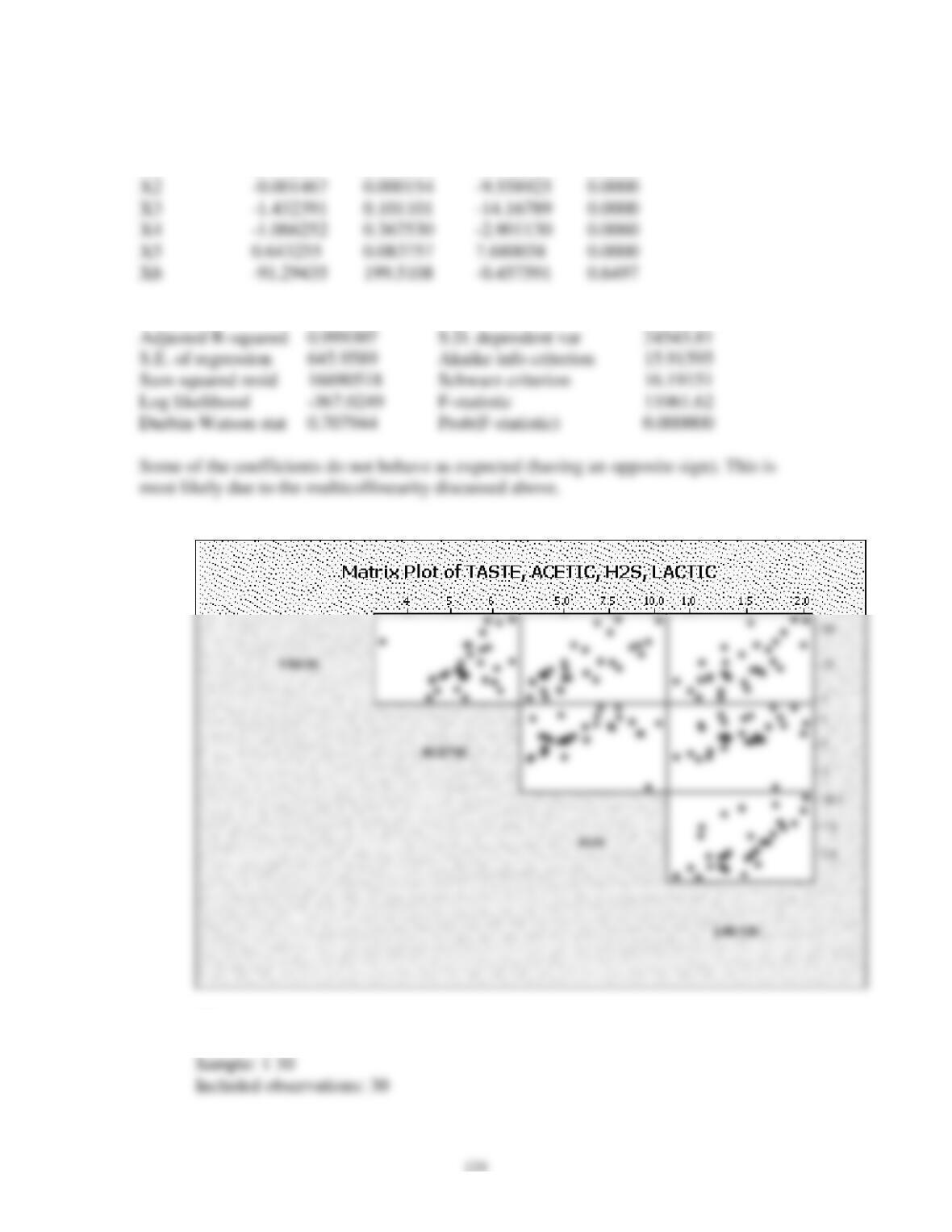

(e) and (f) It very well may be that the Acetic variable is highly linearly related to H2S. It