Chapter 10: The Cost of Capital

Learning Objectives

259

Chapter 10

The Cost of Capital

Learning Objectives

After reading this chapter, students should be able to do the following:

◆ Explain why the weighted average cost of capital (WACC) is used in capital budgeting.

260

Lecture Suggestions

Chapter 10: The Cost of Capital

Lecture Suggestions

Chapter 10 uses the rate of return concepts covered in previous chapters, along with the concept of the

weighted average cost of capital (WACC), to develop a corporate cost of capital for use in capital

budgeting. We begin with an overview of the WACC using Allied’s capital structure to differentiate

among book value, market value, and target capital structure weights that might be used in calculating

the firm’s WACC. We next explain how to estimate the cost of each capital component, and how to put

DAYS ON CHAPTER: 3 OF 56 DAYS (50-minute periods)

Chapter 10: The Cost of Capital

Answers and Solutions

261

10-1 Probable Effect on

rd(1 – T) rs WACC

a. The corporate tax rate is lowered. + 0 +

b. The Federal Reserve tightens credit. + + +

c. The firm uses more debt; that is, it increases

its debt ratio. + + 0

i. Investors become more risk-averse. + + +

j. The firm is an electric utility with a large investment in

nuclear plants. Several states are considering a ban

on nuclear power generation. + + +

10-2 An increase in the risk-free rate will increase the cost of debt. Remember from Chapter 6, r = rRF

10-3 Each firm has an optimal capital structure, defined as that mix of debt, preferred, and common

equity that causes its stock price to be maximized. A value-maximizing firm will determine its

optimal capital structure, use it as a target, and then raise new capital in a manner designed to

keep the actual capital structure on target over time. The target proportions of debt, preferred

stock, and common equity, along with the costs of those components, are used to calculate the

10-4 In general, failing to adjust for differences in risk would lead the firm to accept too many risky

projects and reject too many safe ones. Over time, the firm would become more risky, its WACC

10-5 The cost of retained earnings is lower than the cost of new common equity; therefore, if new

common stock had to be issued then the firm’s WACC would increase.

The calculated WACC does depend on the size of the capital budget. A firm calculates its

retained earnings breakpoint (and any other capital breakpoints for additional debt and

Chapter 10: The Cost of Capital

Answers and Solutions

263

Solutions to End-Of-Chapter Problems

10-1 rd(1 – T) = 10%(0.75) = 7.50%. The coupon rate is not the correct measure of rd. The relevant

10-2 Pp = $57.00; Dp = $6.00; rp = ?

10-3 30% Debt; 70% Common equity; rd = 9%; T = 25%; WACC = 10.50%; rs = ?

The firm uses no preferred stock, so the WACC equation includes only the component costs of

debt and common equity.

WACC = (wd)(rd)(1 – T) + (wc)(rs)

10-4 P0 = $30; D1 = $1.00; g = 4%; rs = ?

1

P

D

b. F = 10%; re = ?

10-5 Projects A, B, C, D, and E would be accepted since each project’s return is greater than the firm’s

10-6 a. D0 = $2.00; P0 = $22; g = 6%; D1 = D0 × (1 + g) = $2.00 × (1.06) = $2.12

rs =

0

1

P

D

+ g =

22$

12.2$

+ 6% = 9.6% + 6% = 15.6%.

264

Answers and Solutions

Chapter 10: The Cost of Capital

10-7 a. D1 = $3.18; g = 6%; P0 = $36; P0 (1 – F) = $32.40

rs =

0

1

P

D

+ g

b. $32.40 = P0 (1 – F)

$32.40 = $36 (1 – F)

c. re = D1/[P0(1 – F)] + g = $3.18/$32.40 + 6% = 9.81% + 6% = 15.81%.

10-8 Debt = 35%, Common equity = 65%.

0

P

D

The firm uses no preferred stock, so the WACC equation includes only the component costs of

debt and common equity.

10-9 BV total debt = Short-term debt + Long-term debt = MV total debt = $1,167; P0 = $4.00; Shares

outstanding = 576; T = 25%

Chapter 10: The Cost of Capital

Answers and Solutions

265

The firm uses no preferred stock, so the WACC equation includes only the component costs of

debt and common equity.

WACC = wdrd(1 – T) + wcrs

10-10 If the investment requires $8.2 million, that means it requires $4.51 million (55% × $8.2 million)

of common equity and $3.69 million (45% × $8.2 million) of debt. (The firm has no preferred

10–11 D0 = $2.00; g = 7%; D1 = $2.00(1.07) = $2.14; P0 = $24.75

rs = D1/P0 + g

= $2(1.07)/$24.75 + 7%

wd = 0.22973 = 22.973%.

10-12 a. rd = 9%, rd(1 – T) = 9%(0.75) = 6.75%.

wd = 35%; D0 = $2.20; g = 6%; P0 = $26; T = 25%.

b. The firm uses no preferred stock, so the WACC equation includes only the component costs of

debt and common equity.

c. The firm’s WACC is 12.09% and each of the projects is equally risky and as risky as the firm’s

266

Answers and Solutions

Chapter 10: The Cost of Capital

10-13 If the firm’s dividend yield (D1/P0) is 5% and its stock price is $46.75, the next expected annual

dividend can be calculated.

Dividend yield = D1/P0

5% = D1/$46.75

10–14 Dp = $11; Pp (1 – F) = $103.08

10-15 a. Examining the DCF approach to the cost of retained earnings, the expected growth rate can

be determined from the cost of common equity, price, and expected dividend. However,

first, this problem requires that the formula for WACC be used to determine the cost of

common equity because we are given the WACC, the cost of debt, the tax rate, and the

b. Given in problem that NI = $1.1 billion (or $1,100 million) and Common Equity = 0.6 × $10

billion = $6 billion (or $6,000 million).

From the formula for the long-run growth rate:

g = (1 – Div. payout ratio) ROE

= (1 – Div. payout ratio) (NI/Equity)

Chapter 10: The Cost of Capital

Answers and Solutions

267

10–16 a. We use the information regarding the firm’s earnings to calculate the past growth in

earnings. With a financial calculator, input N = 5, PV = -4.42, PMT = 0, FV = 6.50, and then

solve for I/YR = g = 8.02% 8%.

10–17 a. rs = 9%; D1 = $3.60; P0 = $60. Use the DCF equation to solve for g.

rs=

0

1

P

D

+ g

b. Current EPS (given) $5.400 Alternatively:

Less: Dividends per share 3.600 EPS1 = EPS0(1 + g) = $5.40(1.03) = $5.562.

Retained earnings per share $1.800

10–18 a. rd(1 – T) = 0.10(1 – 0.25) = 7.5%.

b. WACC: After-Tax Weighted

Component Weight Cost = Cost

Debt 0.15 7.50% 1.125%

Preferred stock 0.10 10.00 1.000

268

Answers and Solutions

Chapter 10: The Cost of Capital

10-19 a. If all project decisions are independent, the firm should accept all projects whose returns exceed

their risk-adjusted costs of capital. Average–risk projects will be evaluated at the firm’s WACC of

10%. High-risk projects will be evaluated at 12%, obtained by adding 2% to the firm’s WACC;

while low–risk projects will be evaluated at 8%, obtained by subtracting 2% from the firm’s

WACC. The appropriate costs of capital are summarized below:

Required Rate of Cost of

Project Investment Return Capital

A $4 million 14.0% 12%

B 5 million 11.5 12

b. With only $13 million to invest in its capital budget, Ziege must choose the best combination

of Projects A, C, E, F, and H. Collectively, the projects would account for an investment of

$21 million, so naturally not all these projects may be accepted. Looking at the excess return

created by the projects (rate of return minus the cost of capital), we see that the excess

c. Since Projects A, F, and H are already accepted projects, we must adjust the costs of capital

for the other two value producing projects (C and E).

Required Rate of Cost of

Project Investment Return Capital

C $3 million 9.5% 8% + 1% = 9%

10–20 a. After-tax cost of new debt: rd(1 – T) = 0.09(1 – 0.25) = 6.75%.

Cost of common equity: Calculate g as follows:

Chapter 10: The Cost of Capital

Answers and Solutions

269

b. The firm uses no preferred stock, so the WACC equation includes only the component costs

of debt and common equity.

WACC calculation:

Target After-Tax Weighted

Component Weight Cost = Cost

Debt 0.40 6.75% 2.70%

270

Comprehensive/Spreadsheet Problem

Chapter 10: The Cost of Capital

Comprehensive/Spreadsheet Problem

Note to Instructors:

The solution to this problem is not provided to students at the back of their text. Instructors

can access the

Excel

file on the textbook’s website.

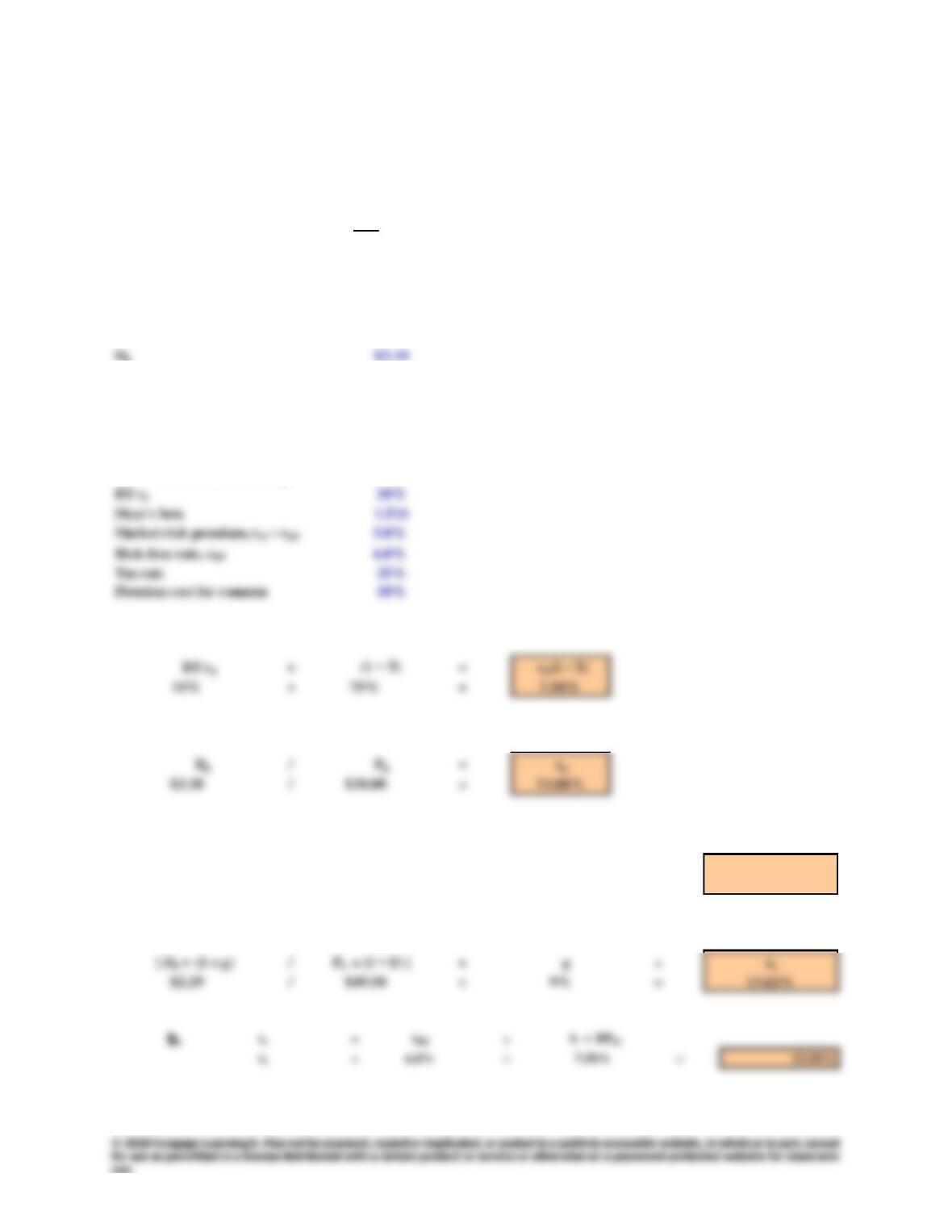

10-21 a.

INPUT DATA

EPS $3.20

P0$55.00

g9%

Common shares outstanding 50,000

Pp$30.00

Dp$3.30

Preferred shares outstanding 10,000

Cost of debt

Cost of preferred stock

Cost of common equity from retained earnings

[ D0 × (1 + g) ] / P0 + g = rs

$2.29 / $55.00 + 9% = 13.16%

Cost of common equity from new common stock