1

2

3

4

7

8

9

10

15

16

18

19

20

A B C D E F G

10 Chapter model 12/12/2018

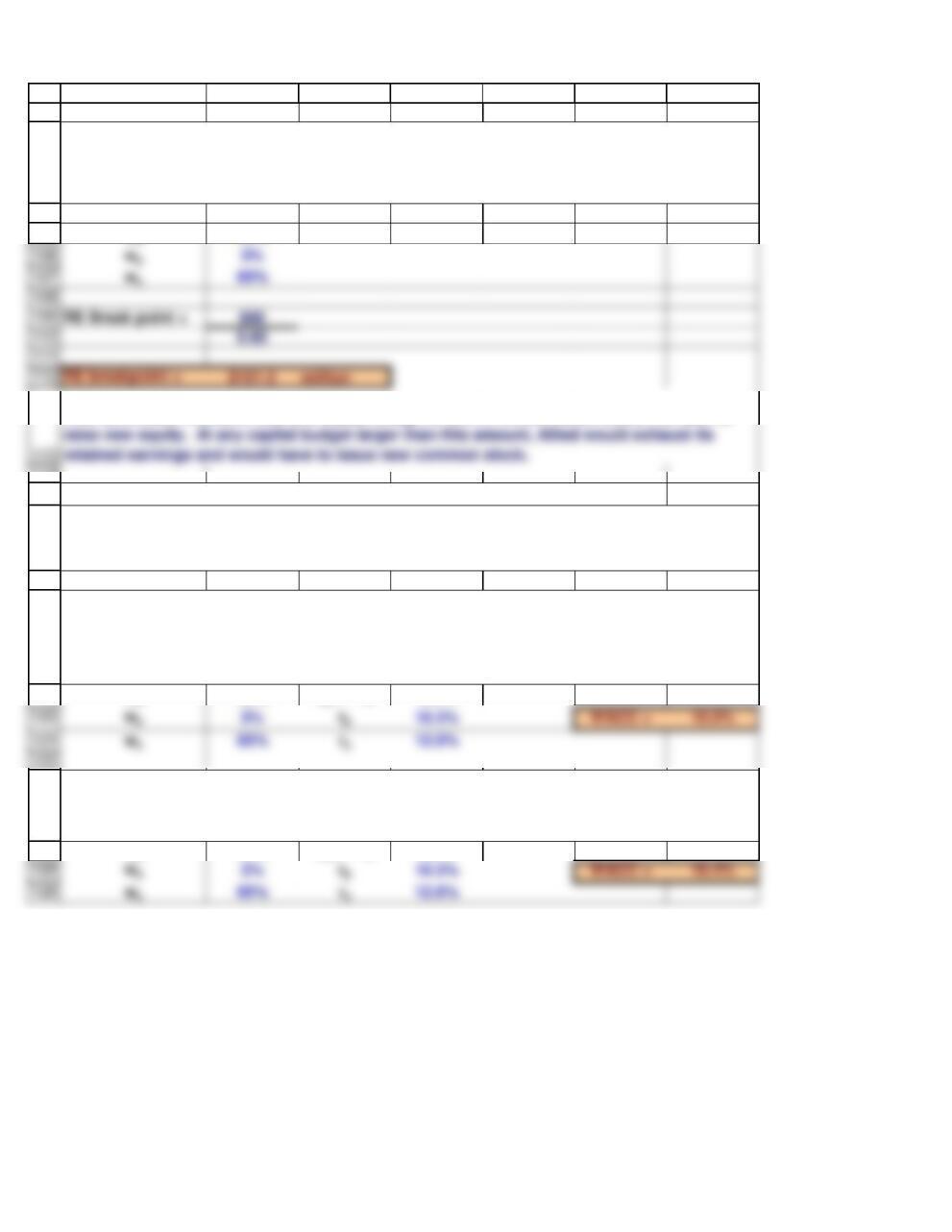

COST OF DEBT, rd (1 − T) (Section 10-3)

EXAMPLE

COST OF PREFERRED STOCK, rp (Section 10-4)

EXAMPLE

Preferred dividend $10.00

The cost of capital is a vital element in the capital budgeting process. For a project to be

accepted, it must provide a return that exceeds its cost of capital, or hurdle rate. The cost of

capital also serves three other purposes: (1) It is used to help determine the EVA, (2)

The relevant cost of debt is the after-tax cost of new debt, taking into account the tax

The cost of preferred stock is simply the preferred dividend divided by the price the company

What is the cost of preferred stock for a company that pays a preferred dividend of $10 per

share if the company could sell new preferred for $97.50 per share?

Chapter 10. The Cost of Capital

rs = rRF + (RPM) bi

36

Market risk premium 5.0%

24

25

27

28

29

30

32

33

34

38

39

40

0.50 7.0%

1.00 9.5%

41

43

47

48

53

54

56

A B C D E F G

COST OF RETAINED EARNINGS, rs (Section 10-5)

THE CAPM APPROACH

rs = rRF + (rM − rRF ) bi

EXAMPLE

Risk-free rate 4.5%

Beta

rs

0.00 4.5%

2.00 14.5%

In regards to Allied, the risk-free rate equals 4.5%, the market risk premium is 5%, and the

firm’s beta is 1.50. What is the company’s cost of equity from retained earnings?

We could use an Excel Data Table to calculate rs at different betas:

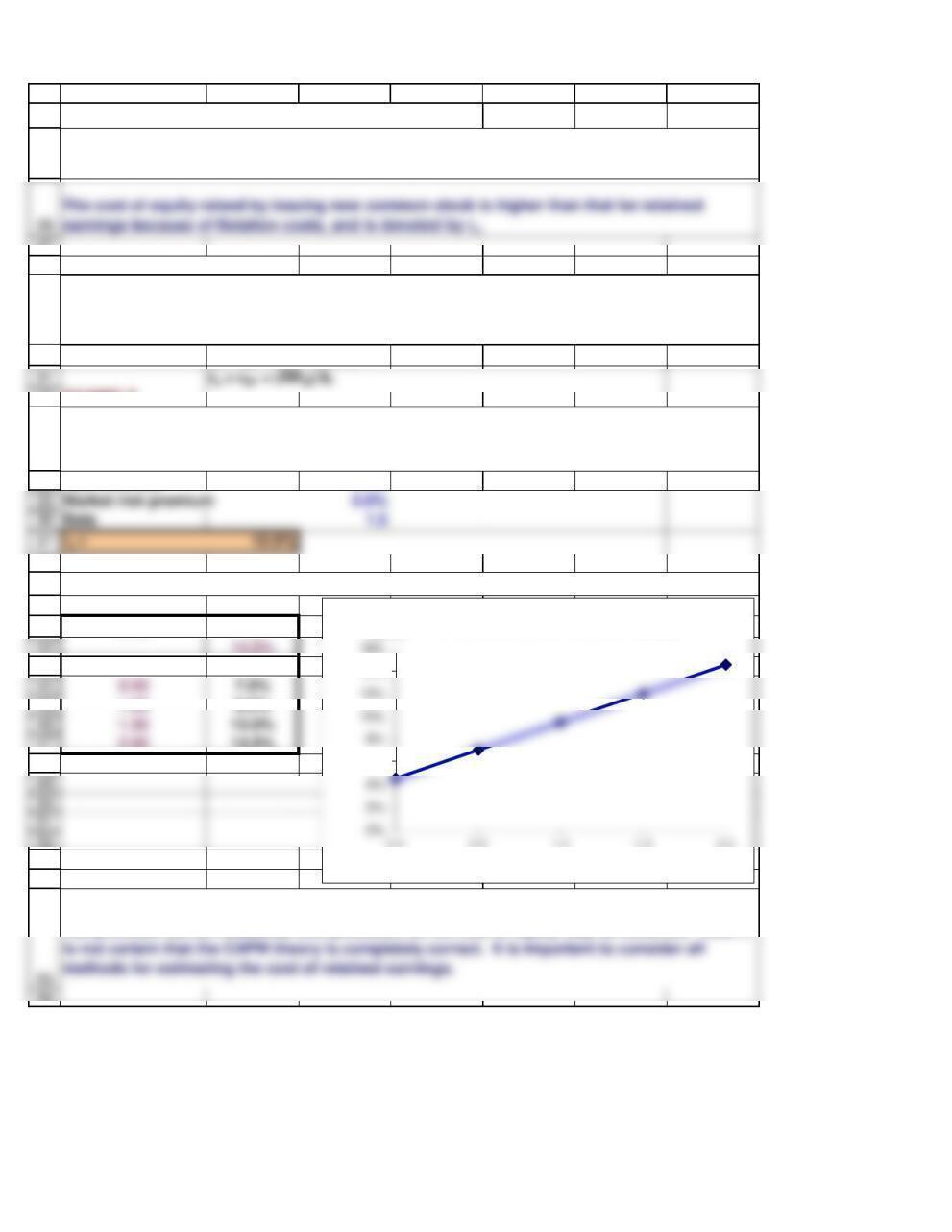

The cost of retained earnings is simply an opportunity cost equal to the return investors

expect to earn on the firm’s common stock, or rs.

Recall that the CAPM equation was that of the Security Market Line. The required return of a

stock, or in this case the cost of equity, can be determined using the risk-free rate, market

risk premium, and the stock’s beta.

The CAPM seems to produce a precise cost of equity value, but neither beta nor the market

risk premium can be measured with precision, so the cost of equity may be incorrect. Also, it

6%

14%

0.0 0.5 1.0 1.5 2.0

Cost of

Equity

Beta

Effect of Beta on Cost of Equity

Minimum RP 3%

Maximum RP 5%

57

59

60

61

62

65

66

68

69

70

71

72

73

74

75

76

A B C D E F G

BOND-YIELD-PLUS-RISK-PREMIUM APPROACH

EXAMPLE

Bond yield 8%

Equity RP 4%

rs = Bond yield + RP

Low

estimate

Expected rs

High

estimate

THE DISCOUNTED CASH FLOW APPROACH

EXAMPLE

P0$23.06

D1$1.21 rs = D1/P0+ g

g5.5%

rs10.7%

The simplest DCF model assumes that growth is expected to remain constant. In this case,

the next expected dividend is easy to estimate, and the stock price can be determined readily.

However, it is not easy to determine the marginal investor’s expected future growth rate.

Moreover, many, if not most, companies are not expected to grow at a constant rate, and if

nonconstant growth is assumed, then the growth rate must be an average of expected future

rates.

Suppose a firm’s stock trades at $23.06 per share and its expected dividend is $1.21. If the

expected growth rate is 5.5%, what is the firm’s cost of equity?

If the appropriate equity premium lies between 3% and 5%, what is the cost of equity for

Allied, whose bonds yield 8%?

This approach consists of adding a judgmental risk premium to the yield on the firm’s own

long-term debt. It is logical that a firm with risky, low-rated debt would also have risky, high-

82

83

84

85

86

87

91

93

94

96

97

98

A B C D E F G

COST OF NEW COMMON STOCK, re (Section 10-6)

EXAMPLE

P0$23.06 re, new stock 11.3%

% Flotation cost 0.6%

Retained Earnings Breakpoint

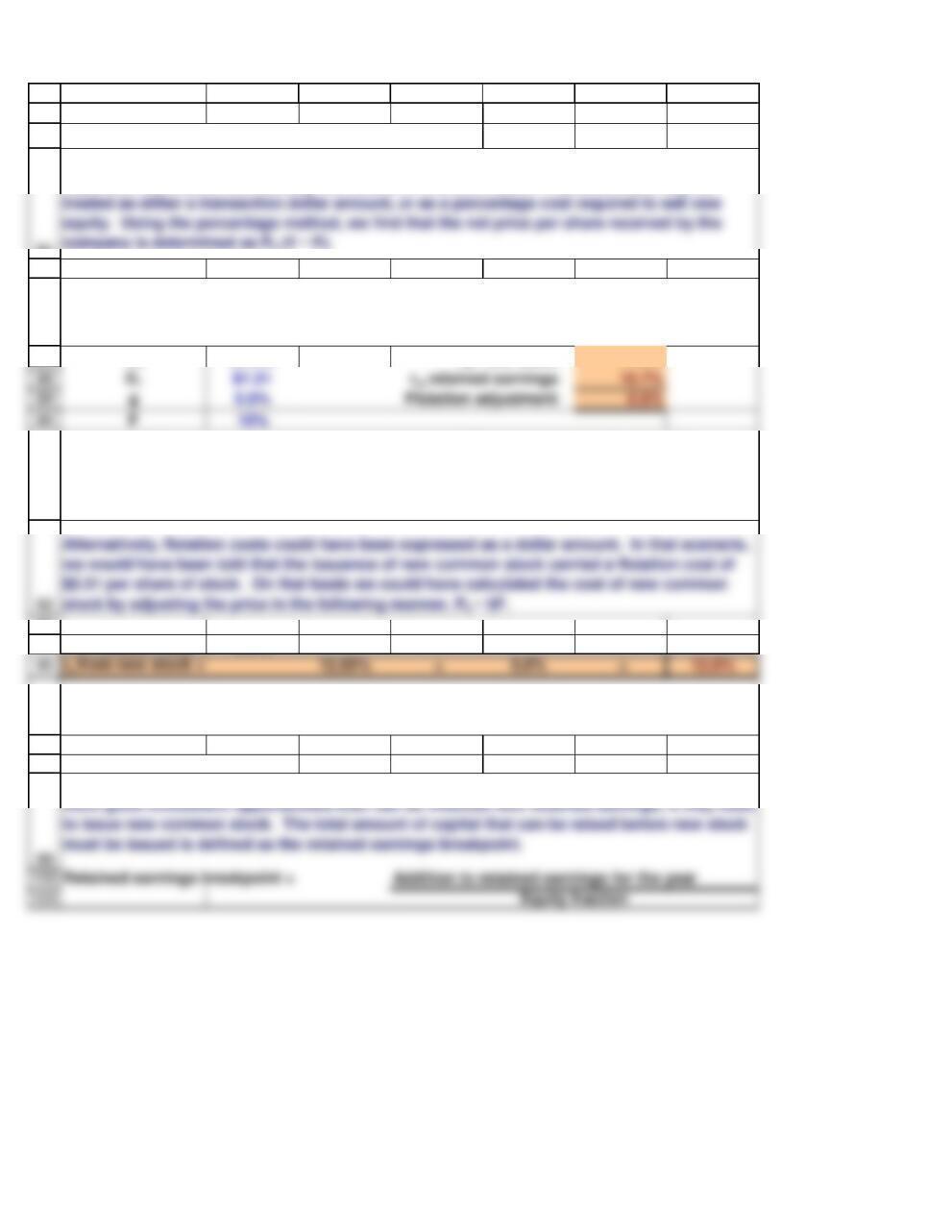

Either manner of flotation cost adjustment is acceptable, it just depends upon the type of

information you are given.

Firms should utilize retained earnings to the greatest extent possible. However, if a firm has

Flotation costs are the fees charged by investment bankers plus accounting and legal

expenses associated with issuing new shares of common stock. Flotation costs may be

If Allied incurred a flotation cost of 10% for issuing new stock, how much higher would its

cost of equity from new common stock be than its cost of retained earnings?

Using the DCF method, Investors require a return of 10.7% on the money they invest.

However, the firm will receive less than investors invest due to flotation costs, so it must earn

more than 10.7% to provide that return to investors. It turns out that if the firm can earn

11.3% on the funds it receives, it can provide the 10.7% required by investors.

102

103

104

105

wp2% rp10.3% WACC = 10.0%

wc65% rs12.0%

114

115

116

117

118

119

123

124

125

wp2% rp10.3% WACC = 10.4%

wc65% re12.6%

A B C D E F G

EXAMPLE

RE addition $66

wd33%

COMPOSITE, OR WEIGHTED AVERAGE, COST OF CAPITAL (Section 10-7)

EXAMPLES

wd33% rd(1 – T) 6.0%

wd33% rd(1 – T) 6.0%

The weighted average cost of capital (WACC) is calculated using the firm’s target capital

structure together with its after-tax cost of debt, cost of preferred stock, and cost of common

equity.

A firm’s target capital structure consists of 33% debt, 2% preferred stock, and 65% common

equity. Using the relevant costs calculated previously, and assuming that all equity will

come from retained earnings, what is the firm’s WACC? (For the cost of equity, use the

midpoint of the range chosen by Allied.)

If Allied’s addition to retained earnings in 2020 is expected to be $66 milion; and its target

capital structure consists of 33% debt, 2% preferred, and 65% equity. What is its retained

earnings breakpoint?

This calculation indicates that at a capital budget of $101.5 million Allied would not have to

The WACC will increase if the firm expands so rapidly that it exhausts all of its retained

earnings for the year and must issue new common stock. Here is the WACC in this case:

wp2%

wc65%

1

2

3

4

5

6

7

8

18

19

20

A B C D E F G H I J K L M N O

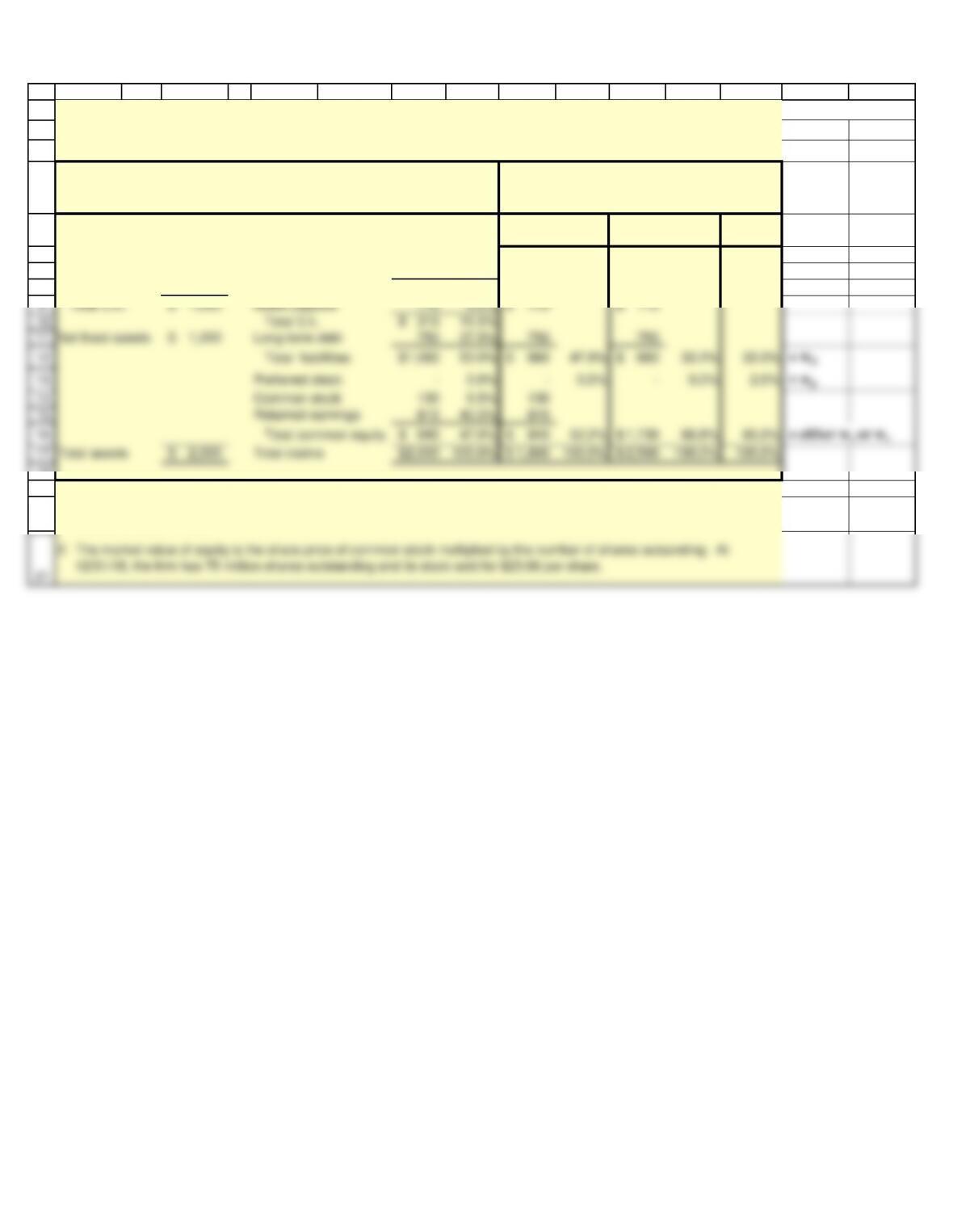

Table 10.1. Allied Food Products: Capital Structure Used to Calculate the WACC 12/12/2018

(Dollars in Millions)

Assets

Target %

(3)

Cash 10$ Accounts payable 60$ 3.0%

Receivables 375 Accruals 140 7.0%

Inventories 615 Spontaneous debt 200$ 10.0%

Notes:

Assets and Claims Against Assets at Book Value on 12/31/18

Investor-Supplied Capital: Payables and

Accruals Are Excluded Because They Come

from Operations, Not from Investors

Claims

Book Value

(1)

Market Value

(2)

1. The market value calculations assume that the company‘s debt is trading at par, so the market value of debt equals

the book value of debt.

1

2

3

4

5

6

7

A B C D E F G H

SECTION 10-3 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

Tax rate 25%

Maturity 20

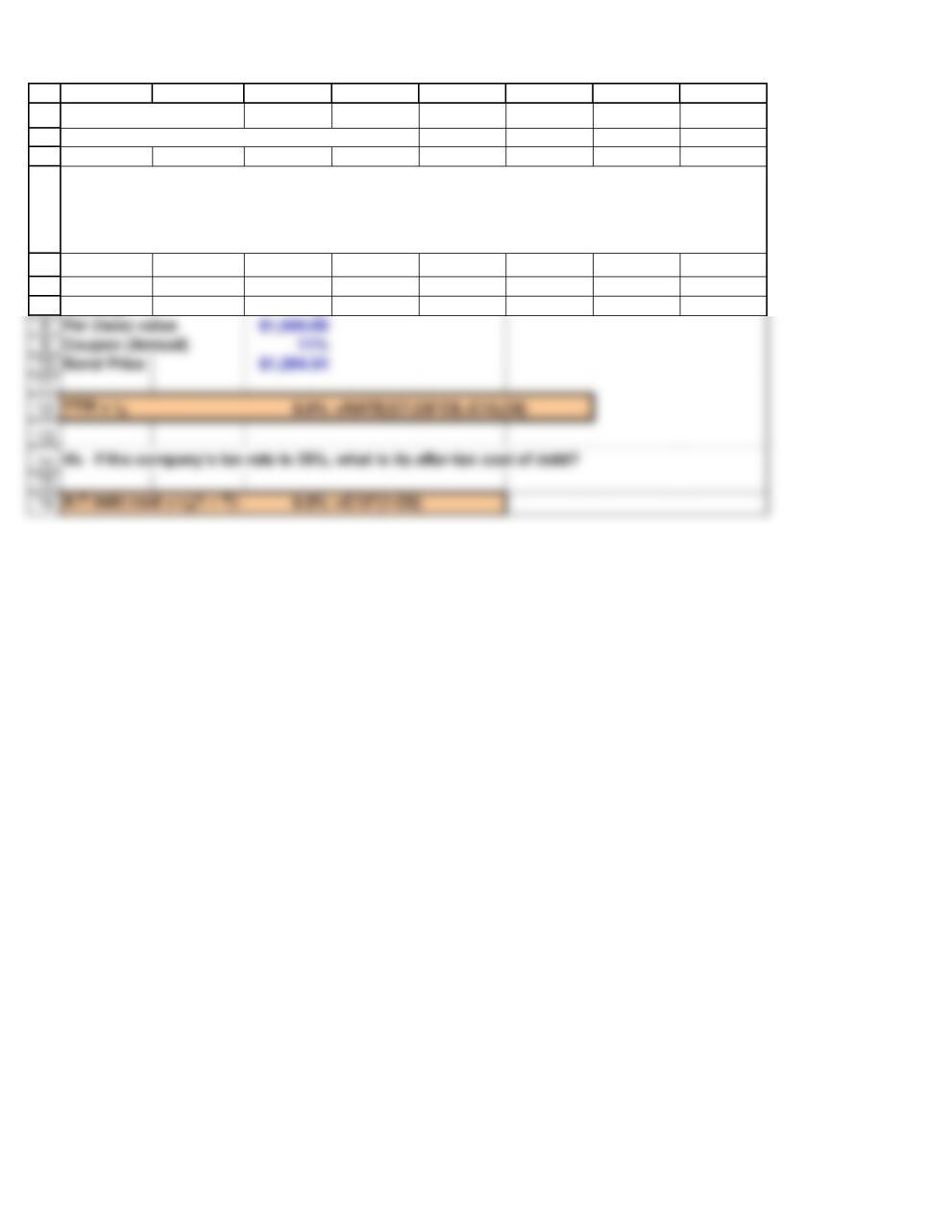

4a. A company has outstanding 20-year, noncallable bonds with a face value of $1,000, an 11%

annual coupon, and a market price of $1,294.54. If the company was to issue new debt, what

would be a reasonable estimate of the interest rate on that debt?

Par (face) value $1,000.00

Bond Price $1,294.54

1

2

3

4

5

6

A B C D E F G H

SECTION 10-4 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

Preferred stock price $80

2. A company’s preferred stock currently trades at $80 per share and pays a $6 annual

dividend per share. Ignoring flotation costs, what is the firm’s cost of preferred stock?

1

2

3

4

5

6

7

P0$25.00

10

11

12

13

17

18

19

20

A B C D E F G H

SECTION 10-5 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

rRF 5.5%

RPM = rM – rRF 6.0%

D1$1.00

Bond yield 6.5%

6a. Suppose you are an analyst with the following data: rRF = 5.5%; rM – rRF = 6%; b = 0.8; D1 =

$1.00; P0 = $25.00; g = 6%; rd = firm’s bond yield = 6.5%. What is this firm’s cost of equity using

the CAPM approach?

6b. Suppose you are an analyst with the following data: rRF = 5.5%; rM – rRF = 6%; b = 0.8; D1 =

$1.00; P0 = $25.00; g = 6%; rd = firm’s bond yield = 6.5%. What is this firm’s cost of equity using

the DCF approach?

6c. Suppose you are an analyst with the following data: rRF = 5.5%; rM – rRF = 6%; b = 0.8; D1 =

$1.00; P0 = $25.00; g = 6%; rd = firm’s bond yield = 6.5%. What is this firm’s cost of equity using

the bond-yield-plus-risk-premium approach? Use the mid-range of the judgmental risk

premium.

1

2

3

12

13

A B C D E F G H

SECTION 10-6 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

3. A firm’s common stock has D1 = $1.50; P0 = $30; g = 5%; and F = 4%. If the firm must issue

4. Suppose Firm A plans to retain $100 million of earnings for the year. It wants to finance its

capital budget using a target capital structure of 46% debt, 3% preferred, and 51% common

equity. How large could its capital budget be before it must issue new common stock?

1

2

3

4

5

6

7

8

14

15

16

17

18

19

26

A B C D E F G H

SECTION 10-7 12/12/2018

SOLUTIONS TO SELF-TEST QUESTIONS

wd0.46

wp0.03

wc0.51

wd0.46

wp0.03

wc0.51

2. Firm A has the following data: Target capital structure of 46% debt, 3% preferred, and 51%

common equity; Tax rate = 25%; rd = 7%; rp = 7.5%; rs = 11.5%; and re = 12.5%. What is the firm’s

WACC if it does not issue any new stock?

3. What is Firm A’s WACC if it issues new common stock?

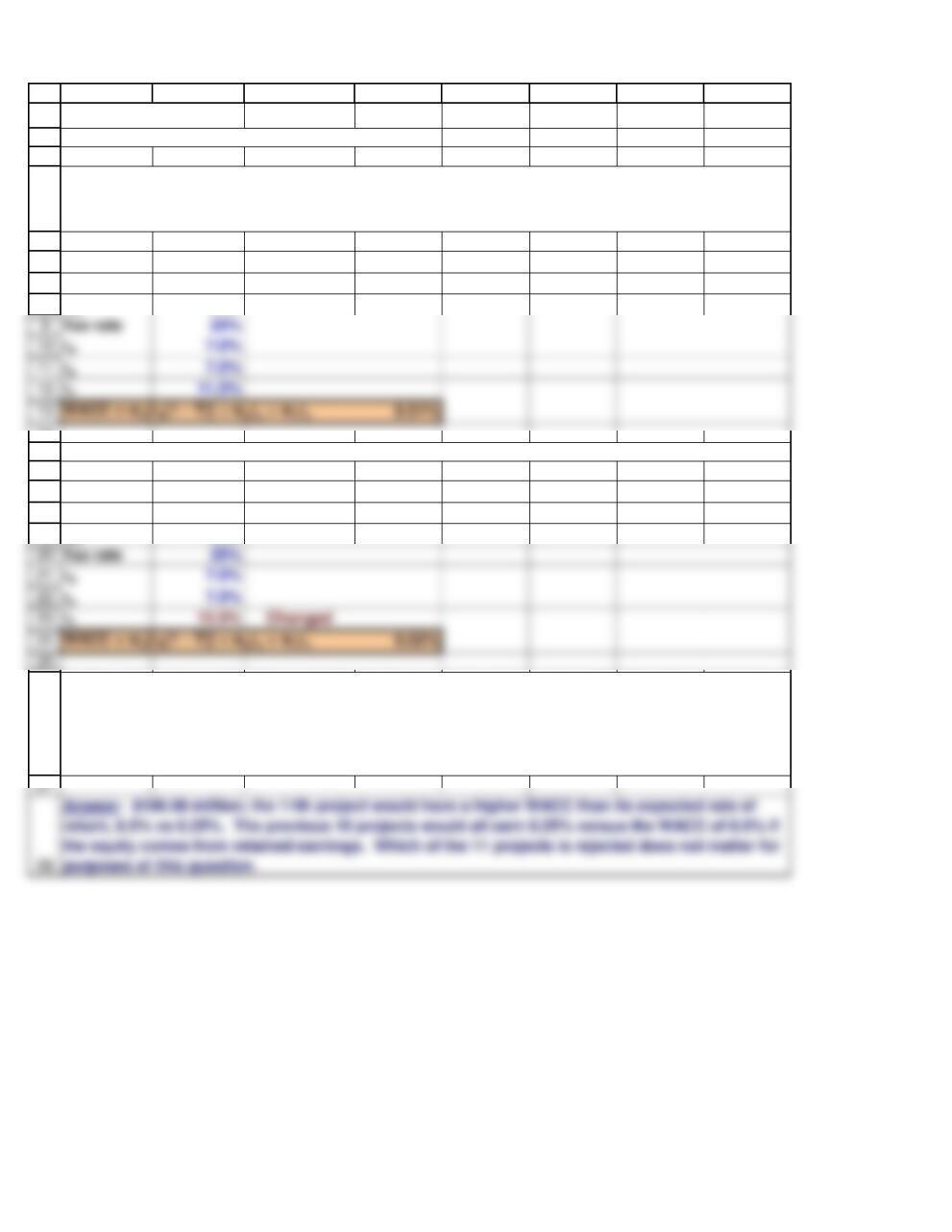

4. Firm A has 11 equally risky capital budgeting projects, each costing $19.608 million and each

having an expected rate of return of 8.25%. Firm A’s retained earnings breakpoint is $196.08

million. The firm’s WACC using retained earnings is 8.0% but it increases to 8.5% if new equity

must be issued. The company invests in projects where the expected return exceeds the cost of

capital. How much capital should Firm A raise and invest? Why?