Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

1

2

3

4

5

6

7

8

9

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

A B C D E F G H I J K L M N O P Q R S

12/10/2012

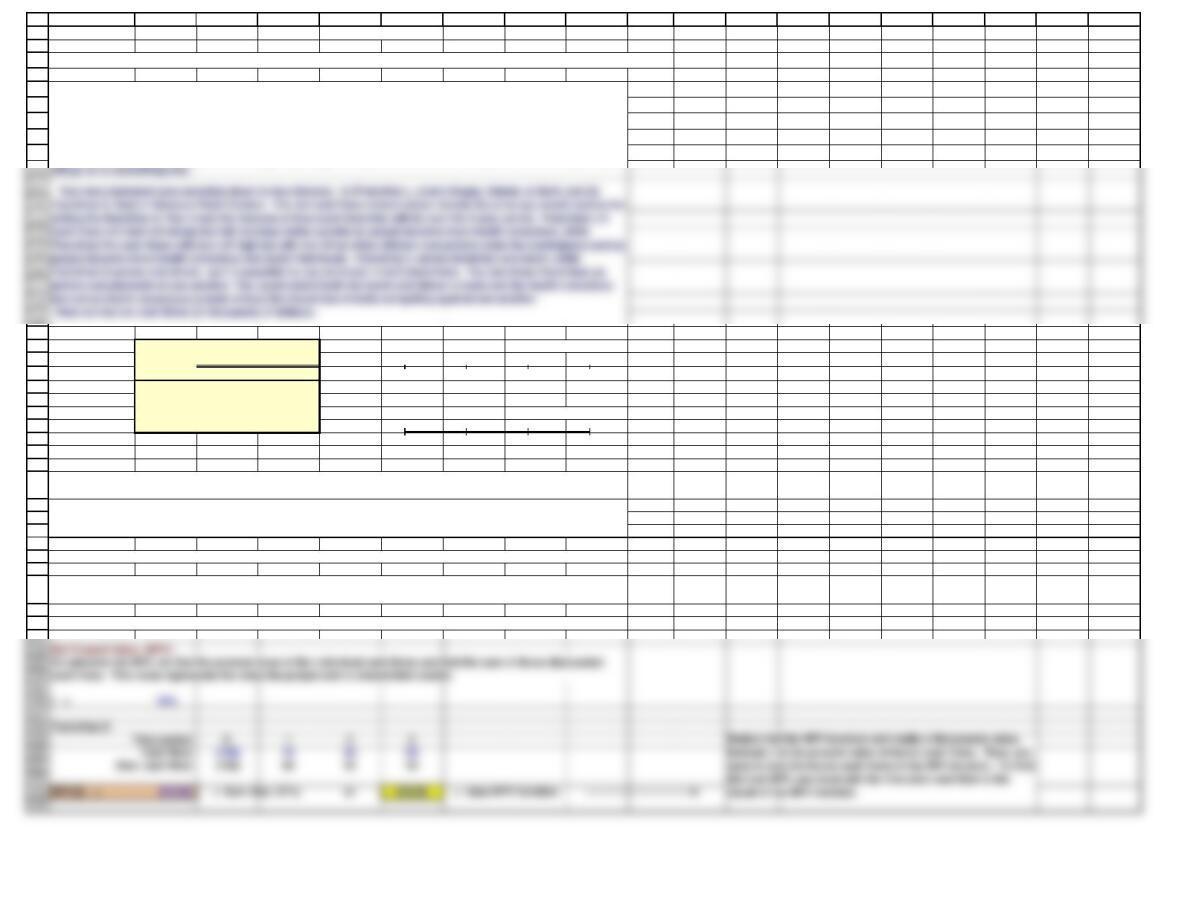

Situation

Franchise S

Year (t) Franchise S Franchise L 0 1 2 3

0($100) ($100) (100) 70 50 20

170 10

250 60 Franchise L

320 80

0 1 2 3

(100) 10 60 80

Chapter 10. Mini Case

Expected

Net Cash Flows

You have just graduated from the MBA program of a large university, and one of your favorite courses was "Today's

Entrepreneurs." In fact, you enjoyed it so much you have decided you want to "be your own boss." While you were in

the master's program, your grandfather died and left you $1 million to do with as you please. You are not an inventor,

and you do not have a trade skill that you can market; however, you have decided that you would like to purchase at

least one established franchise in the fast-foods area, maybe two (if profitable). The problem is that you have never

been one to stay with any project for too long, so you figure that your time frame is three years. After three years you

Depreciation, salvage values, net working capital requirements, and tax effects are all included in these cash flows.

You also have made subjective risk assessments of each franchise and concluded that both franchises have risk

characteristics that require a return of 10%. You must now determine whether one or both of the franchises should

be accepted.

c. (1.) Define the term net present value (NPV). What is each franchise's NPV?

a. What is capital budgeting? Answer: See Chapter 10 Mini Case Show

b. What is the difference between independent and mutually exclusive projects? Answer: See Chapter 10 Mini Case

Show

55

56

57

58

59

60

61

62

63

72

73

74

75

76

77

78

81

82

83

84

85

86

87

88

89

90

103

104

105

106

107

108

109

A B C D E F G H I J K L M N O P Q R S

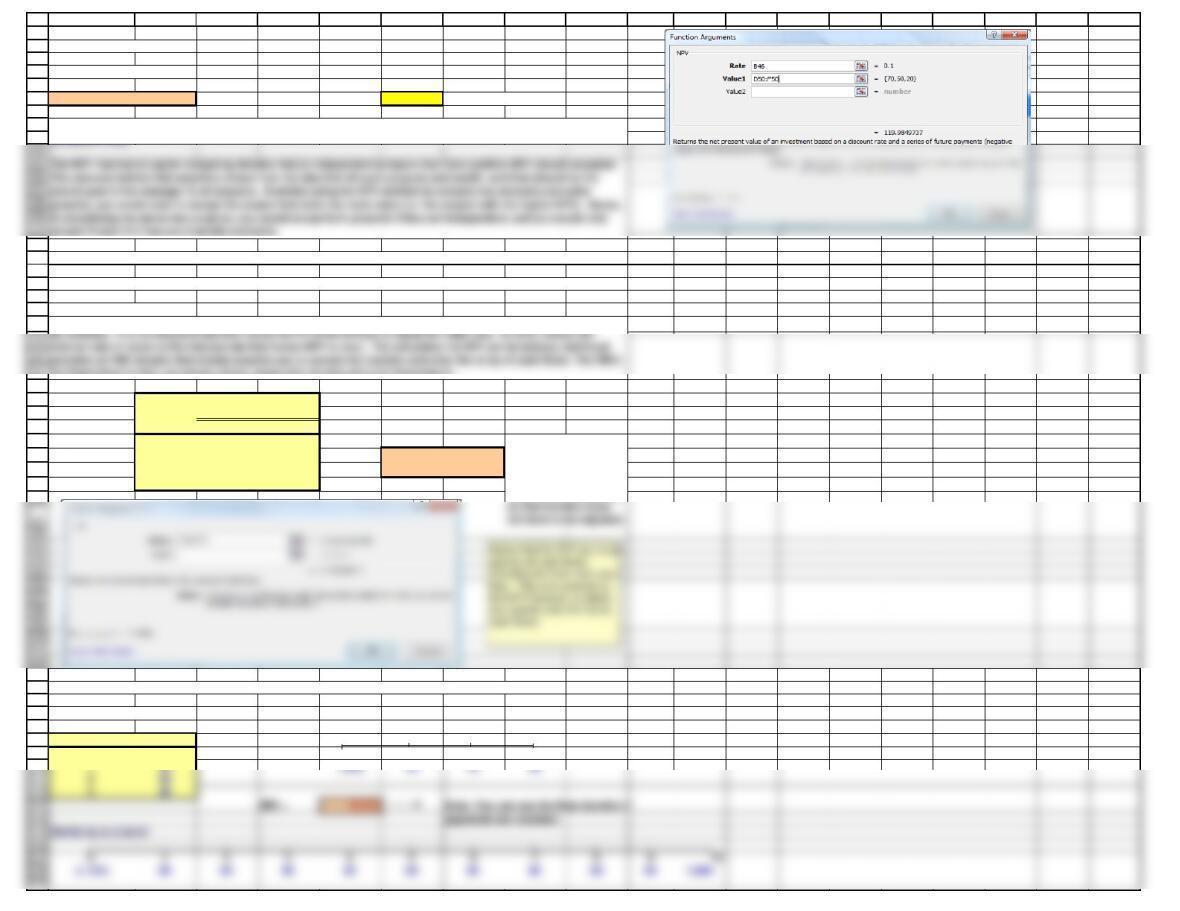

Franchise L

Time period: 0 1 2 3

Cash flow: (100) 10 60 80

Disc. cash flow: (100) 950 60

NPV(L) = $18.78 $18.78 = Uses NPV function.

Internal Rate of Return (IRR)

Year (t) Franchise S Franchise L

0($100) ($100)

170 10

IRR S = 23.56%

250 60

IRR L = 18.13%

320 80

Constant Cash Flows

Year (t) Cash Flow

0($100) 0 123

(2.) What is the rationale behind the NPV method? According to NPV, which franchise or franchises should be

accepted if they

Expected

The IRR function

assumes payments

occur at end of periods,

(3.) Would the NPVs change if the cost of capital changed? Answer: See Chapter 10 Mini Case Show

The internal rate of return is defined as the discount rate that equates the present value of a project's cash inflows to

for Franchises S and L are shown below, along with the data entry for Franchise S.

d. (1.) Define the term internal rate of return (IRR). What is each franchise's IRR?

(2.) How is the IRR on a project related to the YTM on a bond?

net cash flows

120

121

A B C D E F G H I J K L M N O P Q R S

IRR = 7.08%

122

123

124

125

126

127

128

129

130

135

136

137

138

139

140

141

142

143

144

145

155

156

157

158

159

160

161

162

170

171

172

173

174

175

176

180

A B C D E F G H I J K L M N O P Q R S

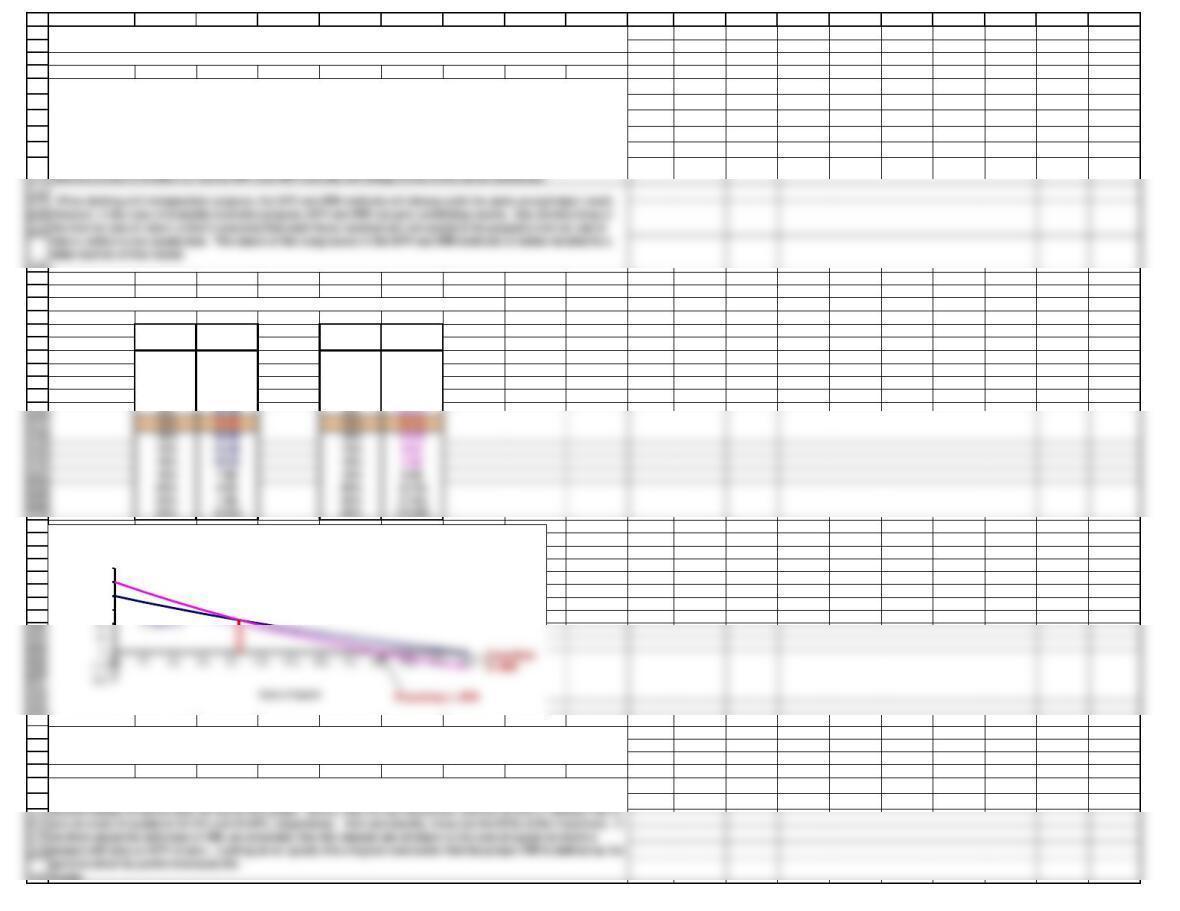

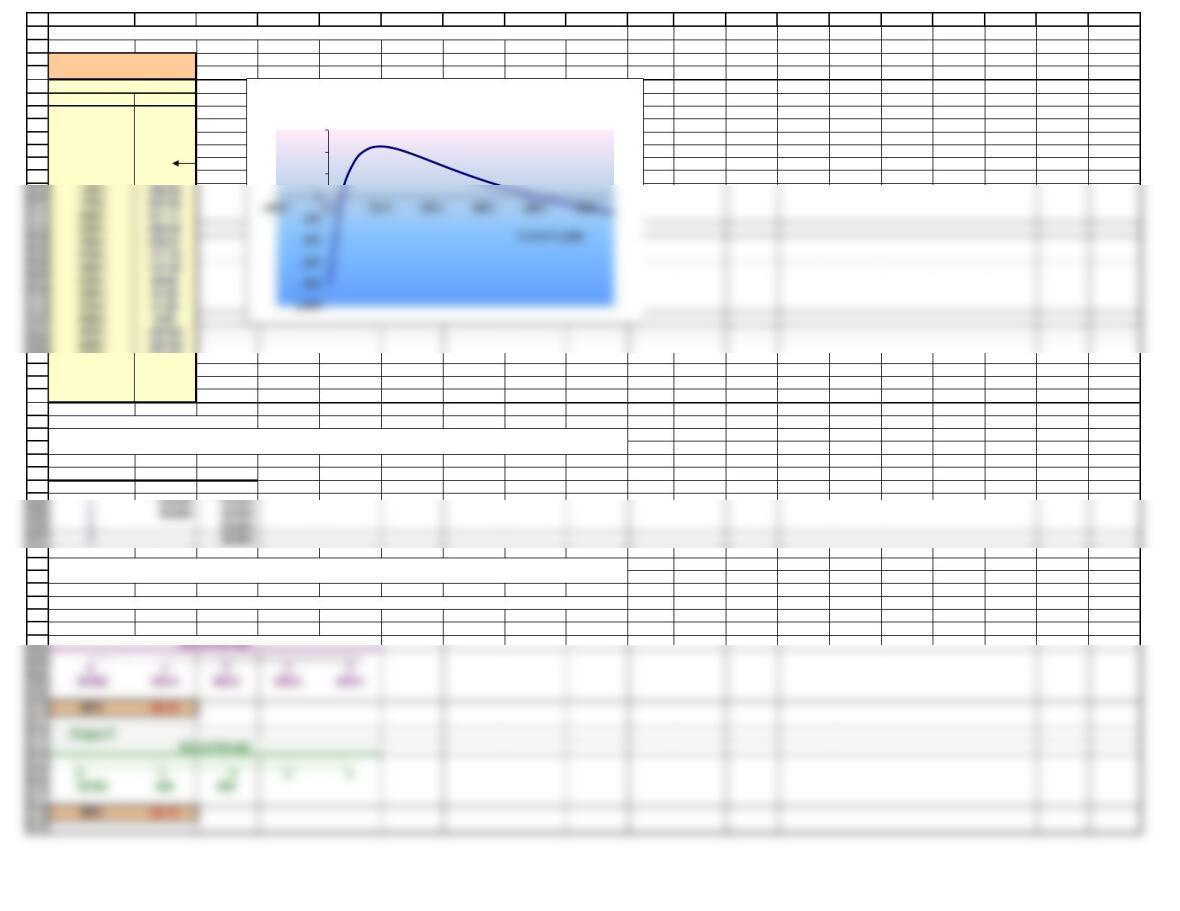

NPV Profiles

e. Draw NPV profiles for Franchises L and S. At what discount rate do the profiles cross?

Franchise S Franchise L

r$19.98 r$18.78

0% 40.00 0% 50.00

2% 35.53 2% 42.86

4% 31.32 4% 36.21

6% 27.33 6% 30.00

(3.) What is the logic behind the IRR method? According to IRR, which franchises should be accepted if they are

independent?

The IRR method of capital budgeting maintains that projects should be accepted if their IRR is greater than the cost

of capital. Strict adherence to the IRR method would further dictate that mutually exclusive projects should be

chosen on the basis of the greatest IRR. In this scenario, both franchises have IRRs that exceed the cost of capital

(10%) and both should be accepted, if they are independent. If, however, the franchises are mutually exclusive, we

would choose Franchise S. Recall, that this was our determination using the NPV method as well. The question that

Previously, we had discussed that in some instances the NPV and IRR methods can give conflicting results. First, we

X-axis.

(4.) Would the franchises' IRRs change if the cost of capital changed?

(2.) Look at your NPV profile graph without referring to the actual NPVs and IRRs. Which franchise or franchises

should be accepted if they are independent? Mutually exclusive? Explain. Are your answers correct at any cost of

capital less than 23.6%?

30

40

50

60

NPV ($)

NPV Profile of Franchises S and L

Project L

Crossover Rate =

8.7%

181

182

183

184

185

191

192

193

194

195

196

197

198

199

200

201

202

203

204

212

213

214

215

216

217

218

219

220

221

A B C D E F G H I J K L M N O P Q R S

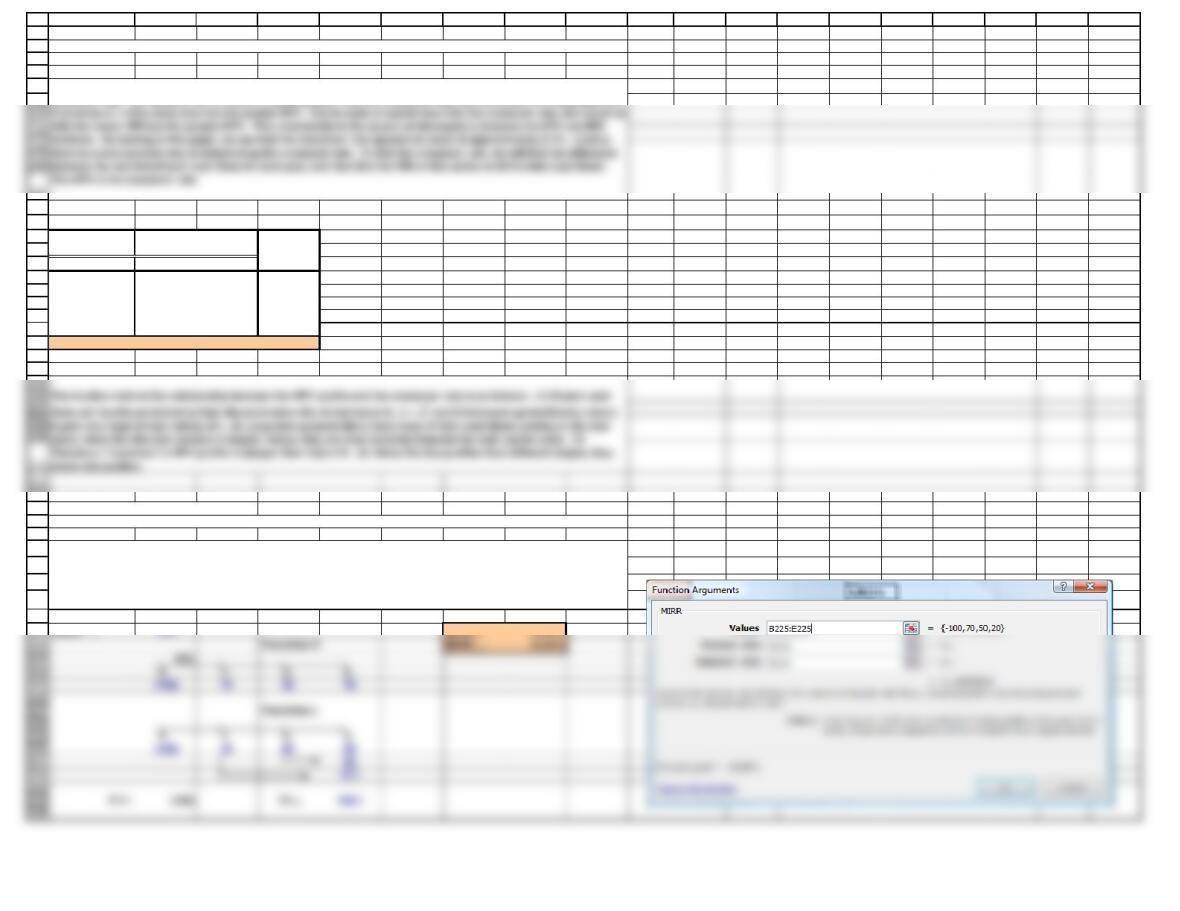

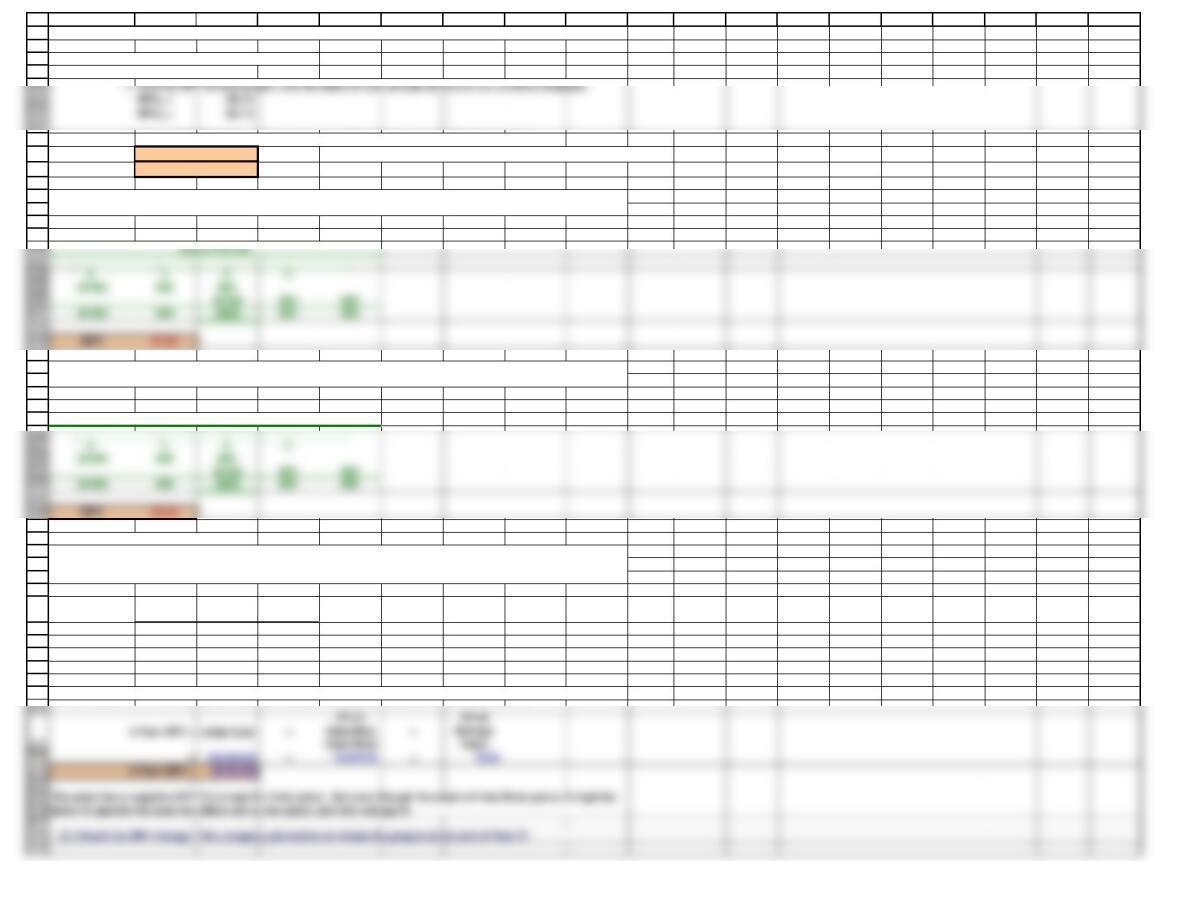

Cash Flow

Year (t) Franchise S Franchise L Differential

0($100) ($100) 0

170 10 60

250 60 (10)

320 80 (60)

IRR = Crossover rate = 8.68%

Modified Internal Rate of Return (MIRR)

WACC = 10%

MIRRS = 16.89%

f. What is the underlying cause of ranking conflicts between NPV and IRR?

The modified internal rate of return is the discount rate that causes a project's cost (or cash outflows) to equal the

present value of the project's terminal value. The terminal value is defined as the sum of the future values of the

project's cash inflows, compounded at the project's cost of capital. To find MIRR, calculate the PV of the outflows

and the FV of the inflows and then find the discount rate that equates the two. Or, you can solve using Excel's MIRR

function.

g. Define the term modified IRR (MIRR). Find the MIRRs for Franchises L and S.

Expected

Net Cash Flows

Looking further at the NPV profiles, we see that the two franchises profiles intersect at a point we shall call the

crossover rate. We observe that at costs of capital greater than the crossover rate, the franchise with the greater IRR

236

237

238

239

240

241

252

253

254

255

256

257

258

259

260

278

279

280

281

282

283

A B C D E F G H I J K L M N O P Q R S

PROFITABILITY INDEX

h. What does the profitability index (PI) measure? What are the PI's for Franchises S and L?

i. (1.) What is the payback period? Find the paybacks for Franchises L and S.

Payback Period

The profitability index is the present value of all future cash flows divided by the intial cost. It measures the PV per

dollar of investment.

(3.) What is the difference between the regular and discounted payback periods?

The payback period is defined as the expected number of years required to recover the investment, and it was the

first formal method used to evaluate capital budgeting projects. First, we identify the year in which the cumulative

cash inflows exceed the initial cash outflows. That is the payback year. Then we take the previous year and add to it

the fraction calculated as the unrecovered balance at the end of that year divided by the following year's cash flow.

Generally speaking, the shorter the payback period, the better the investment.

(2.) What is the rationale for the payback method? According to the payback criterion, which franchise or

franchises should be accepted if the firm's maximum acceptable payback is 2 years, and if Franchise L and S are

independent? If they are mutually exclusive?

Answer: See Chapter 12 Mini Case Show

298

299

300

A B C D E F G H I J K L M N O P Q R S

Discounted Payback: 1.9

301

302

303

304

305

306

307

308

309

316

317

318

319

320

333

334

335

336

337

338

339

340

357

A B C D E F G H I J K L M N O P Q R S

Franchise L

Time period: 0 1 2 3 4

Cash flow: (100) 10 60 80 0

Disc. cash flow: (100) 950 60 0

Disc. cum. cash flow: (100) (91) (41) 19 19

Discounted Payback: 2.7

Multiple IRRs

NPVM = ($386.78)

IRR M 1 = 25.0% MIRR = 5.6%

(4.) What is the main disadvantage of discounted payback? Is the payback method of any real usefulness in capital

We will solve this IRR twice, the first time using the default guess of 10%, and the second time we will enter a guess

of 200%. Notice, that the first IRR calculation is exactly as it was above.

j. As a separate project (Project P), you are considering sponsoring a pavilion at the upcoming World's Fair. The

pavilion would cost $800,000, and it is expected to result in $5 million of incremental cash inflows during its 1 year of

358

359

360

361

362

363

364

365

366

367

368

369

383

384

385

386

387

388

389

390

391

392

393

398

399

400

401

402

403

404

A B C D E F G H I J K L M N O P Q R S

r = 25.0%

NPV = 0.00

NPV

r$0.0

0% (800.00)

25% 0.00

50% 311.11

75% 424.49

100% 450.00 Max.

125% 434.57

475% (81.66)

500% (105.56)

525% (128.00)

550% (149.11)

PROJECTS WITH UNEQUAL LIVES

Year Project T Project R

0($100,000) ($100,000)

Project T r: 10.0%

k. In an unrelated analysis, you have the opportunity to choose between the following two mutually exclusive

projects, Project T (which lasts for two years) and Project F (which lasts for four years):

(1.) What is each project’s initial NPV without replication?

The projects provide a necessary service, so whichever one is selected is expected to be repeated into the

foreseeable future. Both projects have a 10% cost of capital.

(3.) Draw Project P's NPV profile. Does Project P have normal or nonnormal cash flows? Should this project be accepted?

200

400

600

NPV ($)

Multiple Rates of Return

420

421

422

423

428

429

430

431

432

433

434

435

444

445

446

447

448

449

457

458

459

460

461

462

463

464

465

466

467

468

469

A B C D E F G H I J K L M N O P Q R S

Equivalent Annual Annuity (EAA) Approach

Here are the steps in the EAA approach.

2. Convert the NPV into an annuity payment with a life equal to the life of the project.

EAAT = $1.95 Note: we used Excel's PMT function by using the function wizard.

EAAF = $2.38

Project T

Project T

ECONOMIC LIFE VS. PHYSICAL LIFE

Year

Operating

Cash Flow

Salvage

Value

0($5,000) $5,000

1$2,100 $3,100

2$2,000 $2,000

3$1,750 $0

(3.) Now apply the replacement chain approach to determine the projects’ extended NPVs. Which project should

be chosen?

l. You are also considering another project which has a physical life of 3 years; that is, the machinery will be totally

worn out after 3 years. However, if the project were terminated prior to the end of 3 years, the machinery would have

a positive salvage value. Here are the project’s estimated cash flows:

(1.) Using the 10% cost of capital, what is the project's NPV If it is operated for the full 3 years?

End of Period:

(2.) What is each project’s equivalent annual annuity?

(4.) Now assume that the cost to replicate Project T in 2 years will increase to $105,000 because of inflationary

pressures.

480

481

482

A B C D E F G H I J K L M N O P Q R S

2-Year NPV =

Initial Cost +

PV of

Operating

Cash Flow

+

PV of

Salvage

Value

=($5,000.00) +$3,561.98 +$1,652.89

2-Year NPV = $214.88