Chapter 10: The Cost of Capital

Comprehensive/Spreadsheet Problem

271

c.

d. (1) WACC using retained earnings

wd28.2%

wp7.1% Note that we used the MV cap. structure excluding current liabilities

(2) WACC using new common stock

wp7.1%

wd × rd( 1 – T) + wp × rp + wc × re = WACC

re = rs+ Differential

272

Integrated Case

Chapter 10: The Cost of Capital

Integrated Case

10–22

Coleman Technologies Inc.

Cost of Capital

Coleman Technologies is considering a major expansion program that has

been proposed by the company’s information technology group. Before

proceeding with the expansion, the company must estimate its cost of capital.

2. The current price of Coleman’s 12% coupon, semiannual payment,

3. The current price of the firm’s 10%, $100.00 par value, quarterly

dividend, perpetual preferred stock is $111.10.

4. Coleman’s common stock is currently selling for $50.00 per share. Its last

1.2, the yield on T-bonds is 7%, and the market risk premium is

5. Coleman’s target capital structure is 30% debt, 10% preferred stock, and

60% common equity.

Chapter 10: The Cost of Capital

Integrated Case

273

To structure the task somewhat, Lehman has asked you to answer the

following questions.

A. (1) What sources of capital should be included when you estimate

Coleman’s WACC?

Answer: [Show S10–1 through S10–4 here.] The WACC is used primarily for

making long-term capital investment decisions, i.e., for capital

budgeting. Thus, the WACC should include the types of capital used to

pay for long-term assets, and this is typically interest-bearing debt,

preferred stock (if used), and common stock. Total debt consists of

A. (2) Should the component costs be figured on a before-tax or an after-

tax basis?

Answer: [Show S10-5 here.] Stockholders are concerned primarily with

those corporate cash flows that are available for their use, namely,

those cash flows available to pay dividends or to reinvest. Since

274

Integrated Case

Chapter 10: The Cost of Capital

A. (3) Should the costs be historical (embedded) costs or new (marginal)

costs?

Answer: [Show S10-6 and S10-7 here.] In financial management, the cost

of capital is used primarily to make decisions that involve raising

marginal costs rather than historical costs.

B. What is the market interest rate on Coleman’s debt and its

component cost of debt?

Answer: [Show S10-8 through S10–12 here.] Coleman’s 12% bond with 15

years to maturity is currently selling for $1,153.72. Thus, its yield

to maturity is 10%:

0 1 2 3 29 30

| | | | • • • | |

-1,153.72 60 60 60 60 60

1,000

Enter N = 2 × 15 = 30, PV = -1153.72, PMT = [(0.12)($1,000)]/2 =

60, and FV = 1000, and then press the I/YR button to find rd/2 =

Chapter 10: The Cost of Capital

Integrated Case

275

Optional Question

Should you use the nominal cost of debt or the effective annual cost?

Answer: Our 10% pre-tax estimate is the nominal cost of debt. Since the

firm’s debt has semiannual coupons, its effective annual rate is

10.25%:

C. (1) What is the firm’s cost of preferred stock?

Answer: [Show S10-13 and S10-14 here.] Since the preferred issue is

perpetual, its cost is estimated as follows:

rp =

p

p

P

D

=

10.111$

)100($1.0

=

10.111$

10$

= 0.090 = 9.0%.

C. (2) Coleman’s preferred stock is riskier to investors than its debt, yet

the preferred’s yield to investors is lower than the yield to maturity

on the debt. Does this suggest that you have made a mistake?

(Hint: Think about taxes.)

276

Integrated Case

Chapter 10: The Cost of Capital

Answer: [Show S10-15 and S10-16 here.] Corporate investors own most

preferred stock, so 50% of preferred dividends received by

corporations are nontaxable. (The new tax law passed in December

D. (1) Why is there a cost associated with retained earnings?

Answer: [Show S10-17 and S10-18 here.] Coleman’s earnings can either be

retained and reinvested in the business or paid out as dividends. If

earnings are retained, Coleman’s shareholders forgo the

D. (2) What is Coleman’s estimated cost of common equity using the

CAPM approach?

Answer: [Show S10-19 and S10–20 here.] The CAPM estimate for Coleman’s

cost of common equity is 14.2%:

rs = rRF + (rM – rRF)b

Chapter 10: The Cost of Capital

Integrated Case

277

E. What is the estimated cost of common equity using the DCF

approach?

Answer: [Show S10-21 and S10-22 here.] Since Coleman is a constant

growth stock, the constant growth model can be used:

s

r

=

s

r

ˆ

=

gP

D

0

1

+

=

05.0

50$

)05.1(19.4$

P

)g1(D

0

0++

+

F. What is the bond-yield-plus-risk-premium estimate for Coleman’s

cost of common equity?

Answer: [Show S10–23 here.] The bond–yield–plus–risk–premium estimate is

14%:

G. What is your final estimate for rs?

Answer: [Show S10–24 here.] The following table summarizes the rs

estimates:

278

Integrated Case

Chapter 10: The Cost of Capital

Method Estimate

CAPM 14.2%

H. Explain in words why new common stock has a higher cost than

retained earnings.

Answer: [Show S10-25 here.] The company is raising money to make an

investment. The money has a cost, and this cost is based primarily

on the investors’ required rate of return, considering risk and

alternative investment opportunities. So, the new investment must

I. (1) What are two approaches that can be used to adjust for flotation

costs?

Chapter 10: The Cost of Capital

Integrated Case

279

Answer: The first approach is to include the flotation costs as part of the

project’s up-front cost. This reduces the project’s estimated return.

I. (2) Coleman estimates that if it issues new common stock, the flotation

cost will be 15%. Coleman incorporates the flotation costs into the

DCF approach. What is the estimated cost of newly issued common

stock, considering the flotation cost?

Answer: [Show S10–26 here.]

re =

)F1(P

)g1(D

0

0

−

+

+ g

J. What is Coleman’s overall, or weighted average, cost of capital

(WACC)? Ignore flotation costs.

Answer: [Show S10-27 here.] Coleman’s WACC is 11.6%.

A-T

Capital Structure Component

Weights Costs = Product

0.1 9.0 0.9

1.0 WACC = 11.6%

280

Integrated Case

Chapter 10: The Cost of Capital

K. What factors influence Coleman’s composite WACC?

Answer: [Show S10-28 here.] There are factors that the firm cannot control

and those that they can control that influence WACC.

Factors the firm cannot control:

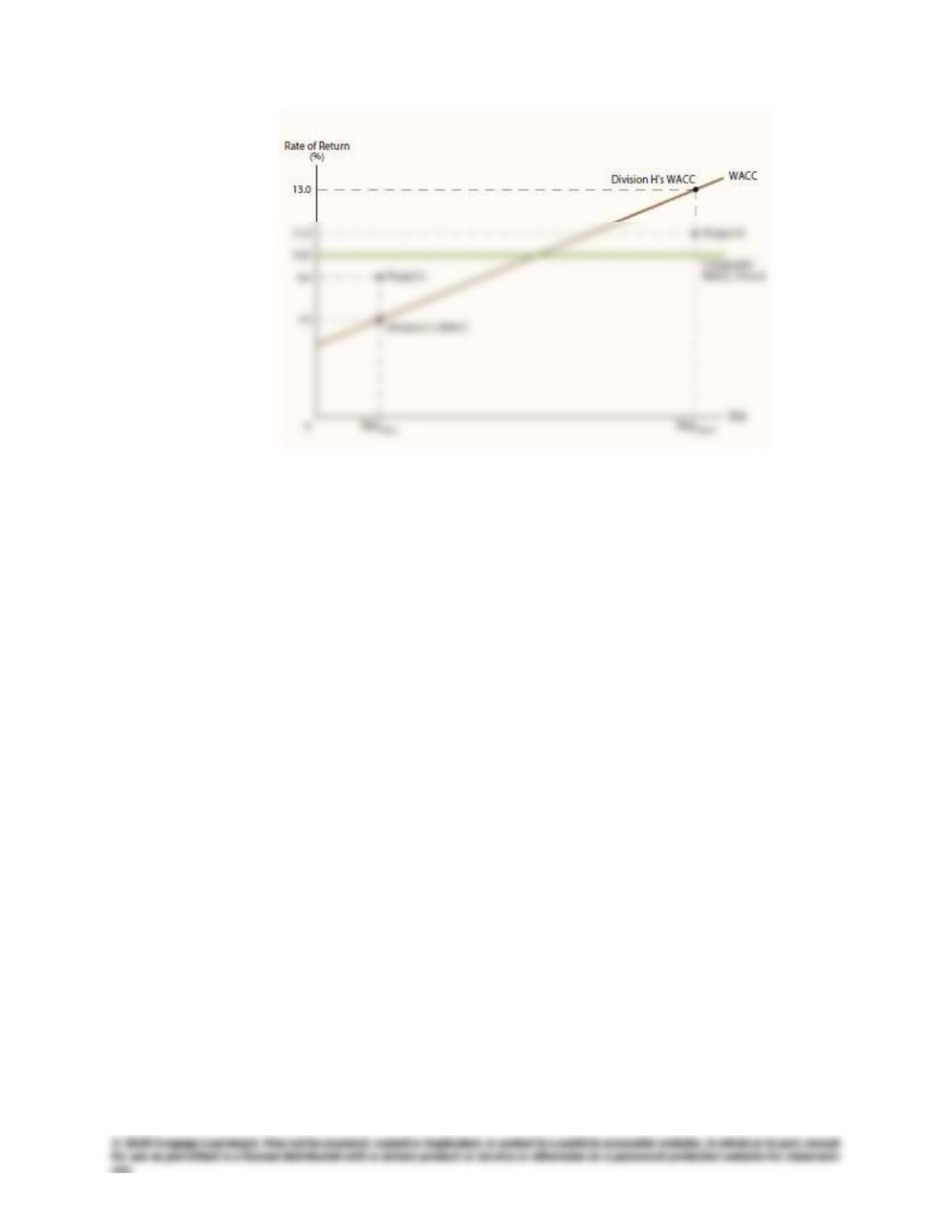

L. Should the company use the composite WACC as the hurdle rate for

each of its projects? Explain.

Answer: [Show S10–29 through S10–31 here.] No. The composite WACC

reflects the risk of an average project undertaken by the firm.

Chapter 10: The Cost of Capital

Integrated Case

281