Appendix 12F Real Options

Answers and Solutions

12F–1

Web Appendix 12F

Real Options: Investment Timing, Growth, and

Flexibility

Answers to Questions

12F-1 An investment timing option is an option as to when to begin a project. Often, if a firm can delay a

decision when more information is available, it can increase a project’s expected NPV and reduce its

risk.

12F-2 When making go versus wait decisions, financial managers need to consider several other factors.

First, if a firm decides to wait, it may lose strategic advantages associated with being the first

supplier in a new line of business, and this could reduce the cash flows. On the other hand, waiting

may enable the company to avoid a costly mistake. In general, the more uncertainty there is about

12F-3 A failure to consider growth options in evaluating a project’s profitability would cause it to

underestimate the project’s NPV. The growth option should have value and by not including it, the

project’s NPV is lower by the NPV of the growth option(s) not considered.

12F-4 A flexibility option is an investment that permits operations to be altered depending on how

conditions change during a project’s life. Many projects offer flexibility options that permit the firm

to change inputs, outputs, or both. A plant can be made more flexible to allow the production of a

12F-5 Flexibility options tend to reduce the risk of a bad outcome, and this increases the expected NPV

and reduces risk. Of course, flexibility options do have costs, but those costs can be compared with

the benefits of the options.

12F-6 a. An abandonment option is the option of discontinuing a project if operating cash flows turn out

to be lower than expected. This option can both raise expected profitability and lower project

risk. In the case of poor cash flows, the project can be shut down rather than continuing to

operate and to realize negative cash flows, fixed assets are sold, and some cash is recovered.

12F–2

Answers and Solutions

Appendix 12F Real Options

on the delay. Second, there might be valuable first mover advantages to a project that will be

lost if the project is delayed.

c. Growth options exist if an investment creates the opportunity to make other potentially

profitable investments that would not otherwise be possible. A common example of a growth

12F-7 Failure to recognize a growth option implies that a project with a negative conventional NPV was

rejected despite having an embedded growth option whose consideration would cause the NPV to

be positive. As a result, failure to recognize the value of a growth option implies that the capital

budget is below the optimal level because a value-adding project (albeit because of a real option)

has been rejected. This argument holds when considering the failure to recognize all real options.

Appendix 12F Real Options

Answers and Solutions

12F–3

Solutions to Problems

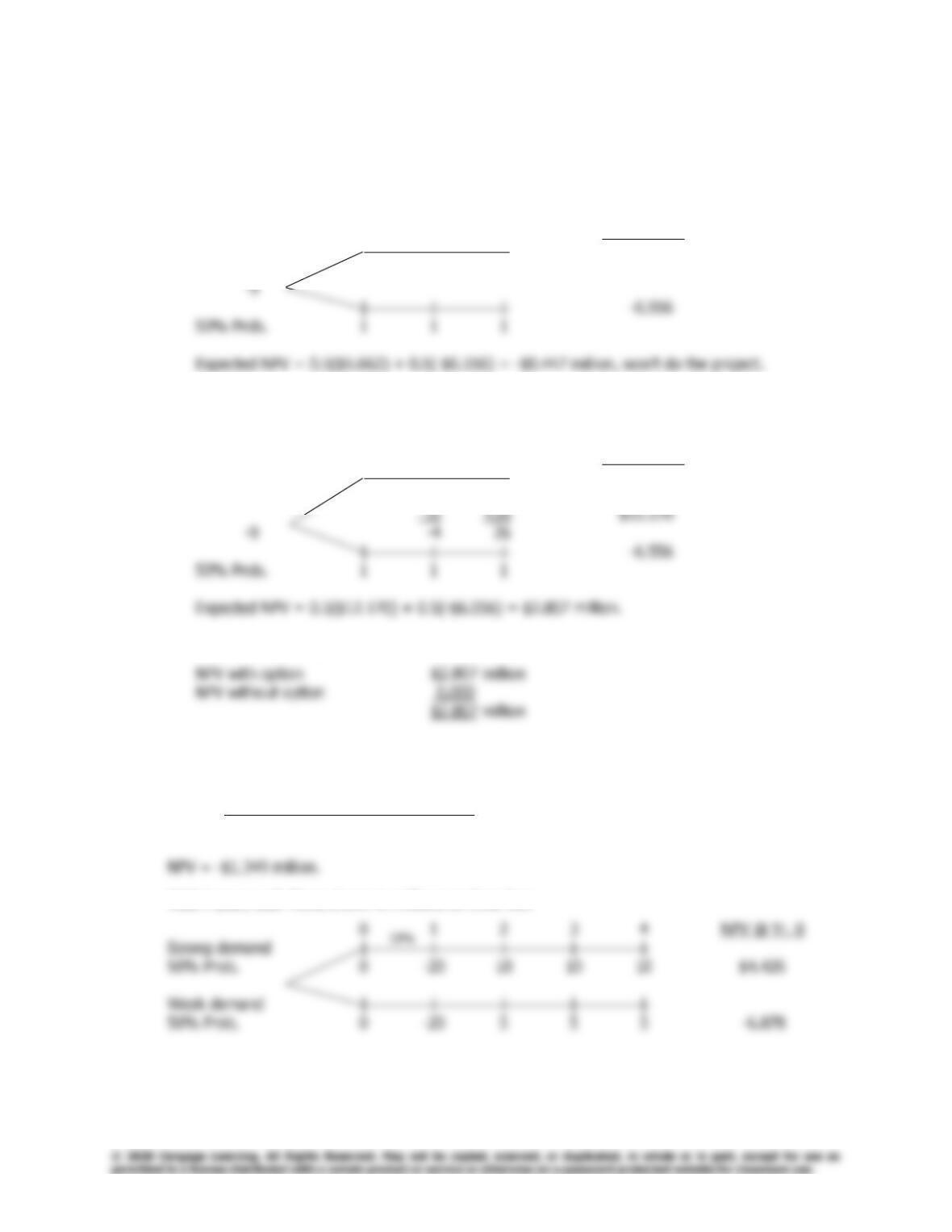

12F-1 a. WACC = 11%; cash flows shown in millions on time line:

0 1 2 3 NPV @ Yr. 0

50% Prob. | | |

6 6 6 $5.662

b. If the project is hugely successful, $10 million will be spent at the end of Year 2, and the new

venture will be sold for $20 million at the end of Year 3.

0 1 2 3 NPV @ Yr. 0

50% Prob. | | |

6 6 6

c. Value of growth option:

12F-2 Expected cash flows shown in millions on time line:

0 1 2 3

| | | |

–20 7.5 7.5 7.5

Wait 1 year; cash flows shown in millions on time line:

10%

12F–4

Answers and Solutions

Appendix 12F Real Options

12F-3 a. Cash flows shown in millions on time line:

0 1 2 3 4

| | | | |

-8 4 4 4 4

b. Wait 2 years, cash flows shown in millions on time line:

c. The investment timing option has a value of $0. Since the difference between the project with

d. There is a danger that oil prices will decline causing the company to receive less revenue for

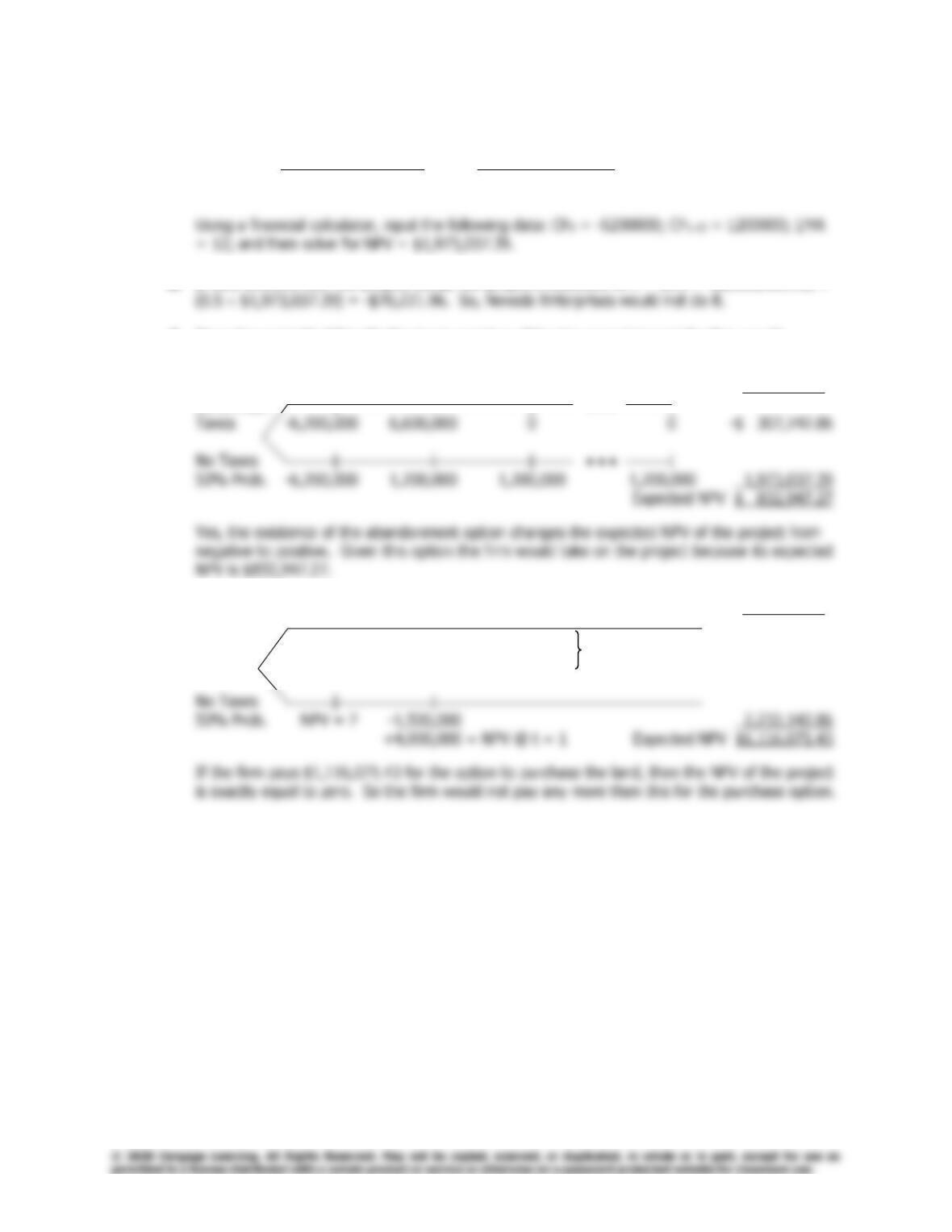

12F-4 a. Cash flows if tax imposed:

0 1 14 15

| | • • • | |

-6,200,000 600,000 600,000 600,000

12%

10%

Appendix 12F Real Options

Answers and Solutions

12F–5

b. Cash flows if tax not imposed:

0 1 14 15

| | • • • | |

-6,200,000 1,200,000 1,200,000 1,200,000

c. If they proceed with the project today, the project’s expected NPV = (0.5 –$2,113,481.31) +

d. Since the project’s NPV with the tax is negative, if the tax were imposed the firm would

abandon the project. Thus, the decision tree looks like this:

0 1 2 15 NPV @ Yr. 0

50% Prob. | | | • • • |

e. 0 1 NPV @ Yr. 0

50% Prob. | |

Taxes NPV = ? -1,500,000 wouldn’t do $ 0.00

+300,000 = NPV @ t = 1

12%

12%

12%