Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Module 24 krugman 1

Module 24

Perfect Competition

What’s New in the Fourth Edition?

• Updated cases

• Handouts to use in the classroom

Module Objectives

• What is perfect competition and why do economists consider it an important benchmark?

• What factors make a firm or an industry perfectly competitive?

• How does a perfectly competitive industry determine the profit-maximizing output level?

• What determines if a firm is profitable or unprofitable?

Teaching Tips

Production and Profits

Creating Student Interest

• Ask students, “What is the goal of a firm?” You will probably get a response like, “to make

money.” Push them to be more specific: “What do you call the money that a firm makes?” Here

you need to make sure they distinguish between revenue and profit. Finally, make sure they

understand the goal is to maximize profit—not just earn some. (Be sure to note that some firms

may have other goals—nonprofit firms or firms that also have social goals.) But point out that

many (most?) firms have the goal of maximizing profits and that is the assumption of our models.

• Now ask students to imagine they are opening a business. How should they decide what and where

to produce? Some students are likely to suggest producing a good in some location where they can

make a profit or where there is not a lot of competition. This can serve as a preview for the idea

that firms will enter industries in which existing firms are earning a positive profit. Next ask

students what happens if profit is zero or negative? Many are sure to have forgotten about

accounting versus economic profit and will interpret zero or negative profit as bad. Remind

students of the difference between economic and accounting profit before moving on. For

example, accounting profit can be positive even though economic profit is negative.

Presenting the Material

• Use Handout 24-1 to helps students see the process of finding the profit maximizing quantity of

output.

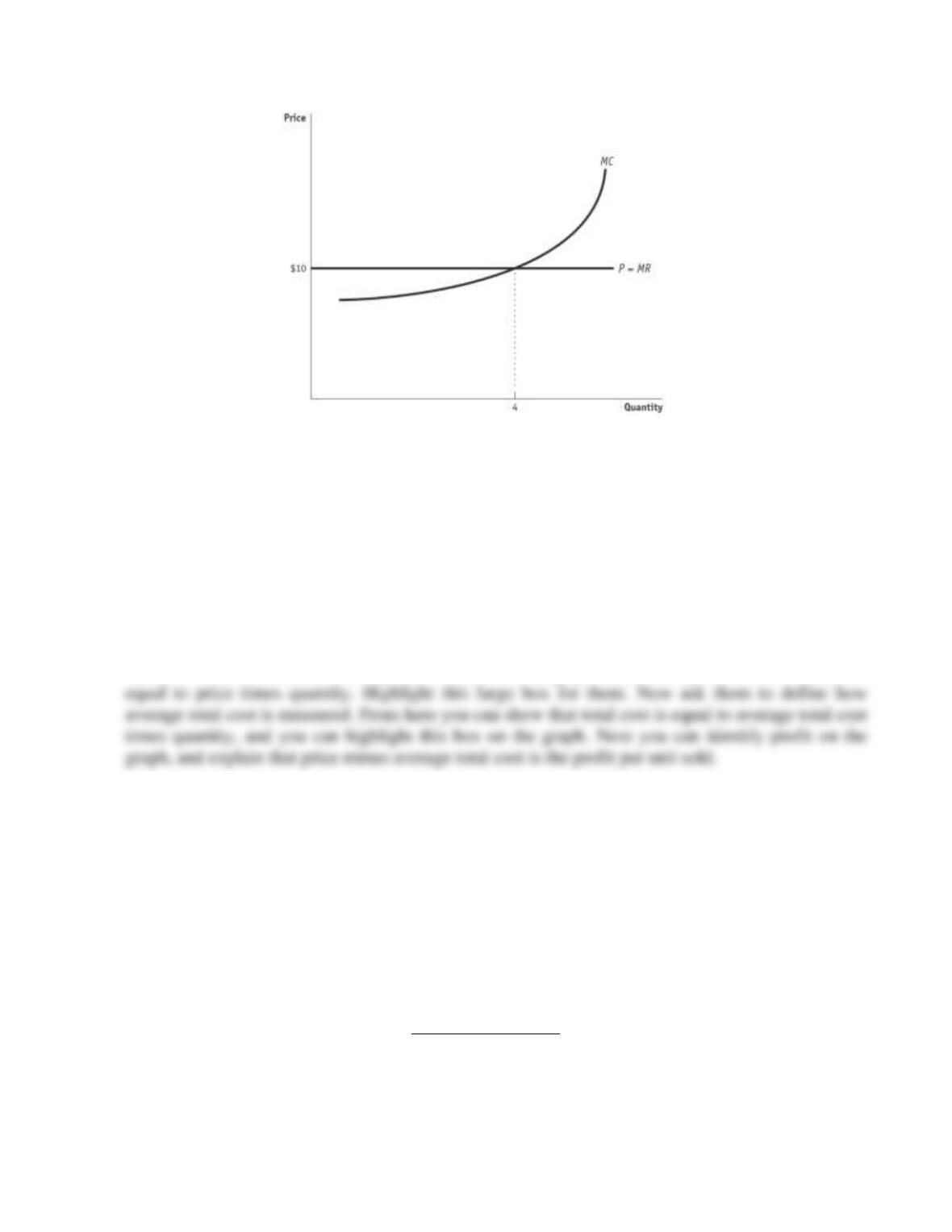

• In the following graph, the maximum profit quantity is shown where marginal cost is equal to

price.

Module 24 krugman 2

• Show the students that at marginal units, like the 2nd or the 3rd, that MR is greater than MC, so

that the addition to TR is greater than the addition to TC by producing and selling that unit,

increasing profit (a good thing). Show that this happens until MR = MC, where the addition to

profit is 0. Then show the 5th unit, where MR < MC, so that additions to TC are greater than

additions to TR, lowering profit (a bad thing). So, the stopping rule is MR = MC.

• Draw a supply and demand graph to remind students that price is determined in the market. The

perfectly competitive firm takes the market price as given because they are small relative to the

total market and they produce a standard good. Now draw a cost curve graph to illustrate average

total cost and marginal cost. Draw in a market price that lies above ATC and explain that the firm

can produce and sell all they want at this going market price. Remind them that price is equal to

marginal revenue. Identify the profit-maximizing output.

• Students should be able to identify total revenue on the graph because they know total revenue is

Module Outline

I. Production and Profits

A. Total revenue, TR, is equal to the market price multiplied by the quantity of output, or TR =

P × Q.

B. Profit equals the difference between total revenue and total cost, or Profit = TR – TC.

C. The optimal output rule

1. Marginal revenue is the change in total revenue generated by an additional unit of

output.

Change in total revenue

Marginal revenue Change in output

Change in total revenue generated by one

additional unit of output

=

=

Module 24 krugman 3

2. The optimal output rule says that profit is maximized by producing the quantity of

output at which the marginal revenue of the last unit produced is equal to its marginal

cost.

D. The optimal output rule for a price-taking firm

1. The price-taking firm’s optimal output rule says that a price-taking firm’s profit is

maximized by producing the quantity of output at which the marginal cost of the last

unit produced is equal to the market price.

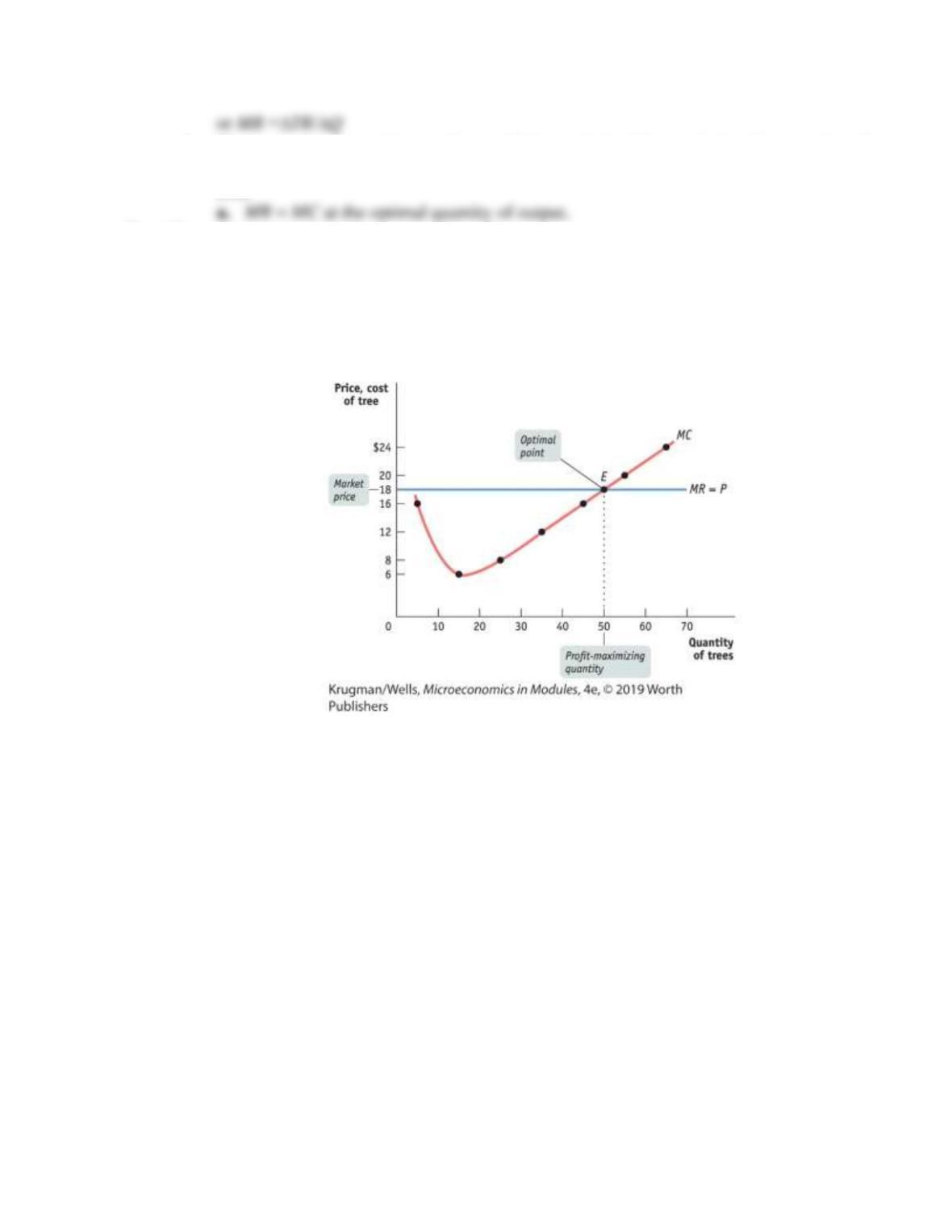

a. For a perfectly competitive industry, P = MC at the price-taking firm’s optimal

quantity of output. This is illustrated in text Figure 24-1, shown here.

Figure 24-1

2. Whenever a firm is a price-taker, its marginal revenue curve (MR) is a horizontal line

at the market price.

E. Produce or shut down?

1. If TR > TC, the firm is profitable. If TR = TC, the firm breaks even. If TR < TC, the

firm incurs a loss.

2. For profit per unit of output, Profit/Q = TR/Q – TC/Q

a. TR/Q is average revenue, or the market price.

b. TC/Q is average total cost.

3. If P > ATC, the firm is profitable. If P = ATC, the firm breaks even. If P < ATC, the

firm incurs a loss.

4. Total profit can be expressed in terms of profit per unit.

a. Profit = TR – TC = (TR/Q – TC/Q) × Q.

b. Equivalently, Profit = (P – ATC) × Q.

5. The break-even price of a price-taking firm is the market price at which it earns zero

profits. This is illustrated in text Figure 24-2, shown next.

Module 24 krugman 4

Figure 24-2

6. The rule for determining whether a producer of a good is profitable depends on a

comparison of the market price of the good to the producer’s break-even price—its

minimum average total cost.

a. Whenever market price exceeds minimum average total cost, the producer is

profitable.

b. Whenever the market price equals minimum average total cost, the producer

breaks even.

c. Whenever market price is less than minimum average total cost, the producer is

unprofitable.

Web Resources

Module 24 krugman 5

Handout 24-1

Date_________ Name____________________________ Class________ Professor________________

Maximizing Profit

Part 1

Complete column (1) in the table below.

Q

TR

(1)

MR

TC

(2)

MC

(3)

Total profit

0

0

—

20

—

1

30

40

2

60

56

3

90

76

4

120

105

5

150

130

6

180

170

1. What do the abbreviations Q, TR, and TC stand for?

2. How much is the company’s fixed cost?

3. What price does the company face in the market?

4. Calculate total profits at every output level.

5. What quantity will maximize profits?

Module 24 krugman 6

Part 2

Complete columns (2) and (3) in the table above.

1. What do the abbreviations MR and MC stand for?

2. Define MR and MC.

3. Calculate MR and MC to complete the table.

4. Based on the optimal output rule, what quantity will maximize profits?

Module 24 krugman 7

Answers

Part 1

Complete column (1) in the table below.

Q

TR

(1)

MR

TC

(2)

MC

(3)

Total profit

0

0

—

20

—

–20

1. What do the abbreviations Q, TR, and TC stand for?

2. How much is the company’s fixed cost?

3. What price does the company face in the market?

4. Calculate total profits at every output level.

5. What quantity will maximize profits?

Part 2

Complete columns (2) and (3) in the table above.

1. What do the abbreviations MR and MC stand for?

2. Define MR and MC.

Module 24 krugman 8

3. Calculate MR and MC to complete the table.

See table.

4. Based on the optimal output rule, what quantity will maximize profits?

Module 24 krugman 9

Handout 24-2

Date_________ Name____________________________ Class________ Professor________________

A Perfectly Competitive Industry?

Are the following industries perfectly competitive? Why or why not?

• Fast-food industry

• Cellular telephone service

• The U.S. stock market

• Wholesale flowers

• eBay

Module 24 krugman 10

Answers