Module 17 krugman 1

Module 17

Making Decisions

What’s New in the Fourth Edition?

• Updated Teaching Tips

• Updated Business Cases

• Handouts for use in class

Module Objectives

• Why does good decision making depend on accurately defining costs and benefits?

• What is the difference between explicit and implicit costs?

• What is the difference between accounting profit and economic profit and why is economic profit

the correct basis for decisions?

• What are the three types of economic decisions?

Teaching Tips

Costs, Benefits, and Profits

Creating Student Interest

• Use Handout 17-1 to have students brainstorm the costs of going to college or Handout 9-7 to

consider the implicit and explicit costs of raising children.

Presenting the Material

• Use Handout 17-2 or 17-4 to have students consider the costs, both implicit and explicit, of

operating a business.

Making “How Much” Decisions: The Role of Marginal Analysis

Creating Student Interest

• Ask students to estimate how long they plan to spend studying for their next economics exam. You

can have them write their estimates on a small slip of paper and collect them. Look at the estimates

and determine a rough estimate of the average. Have them consider whether this is the optimal

number of hours (minutes?) to study. Why wouldn’t they want to study longer? Why not stop

studying earlier? Ask for suggestions of what they would need to consider to determine the

optimal number of hours to study. They need to know their goal for the class, the benefits of

Presenting the Material

Module 17 krugman 2

• Use Handout 17-3 for students to think about the marginal decision involved in the optimal choice

of output for a business.

Sunk Costs

Creating Student Interest

• Have students consider the following scenario. Two friends have purchased memberships to a

fitness center. They have agreed to work out together every Monday, Thursday, and Saturday.

Leslie paid $600 for her annual membership; Amy, who waited for a special membership

promotion, paid $100. In both cases, the fee was paid in full, in advance, and is nonrefundable.

After the first few months of their agreement, Leslie and Amy’s school starts having a special

concert every Saturday so Amy decides she is only going to work out twice a week. Leslie tells

Amy that because she paid $600 for her membership, she is going to continue going to the gym

every Saturday, even though it means missing the concert. Ask the students if they think the

friends made the best decision and why.

Presenting the Material

• Give the class the following additional information about Leslie and Amy (from the preceding

scenario). Leslie and Amy both love to attend concerts. They are music majors and get great

enjoyment from listening to all kinds of music. Both of the friends stay very fit carrying around

their instruments and neither much enjoys working out. Leslie especially hates working out if her

best friend Amy isn’t with her.

Now have the students think about the following questions:

1. If Leslie continues going to the gym every Saturday, how much does the gym

2. If Leslie stops going to the gym every Saturday, how much does the gym membership

3. What does Leslie gain from going to the gym alone on Saturday? (Nothing—she is

5. Since the $600 is a sunk cost (Leslie cannot get it back no matter what she does), she

6. Make sure students see the difference between sunk costs and explicit costs. Explicit

Common Student Pitfalls

Module 17 krugman 3

• Total cost versus marginal cost. Students may be inclined to think that if marginal cost is

decreasing, then so is total cost. Remind them that marginal cost is extra cost so that as long as

marginal cost is positive, total cost will increase.

• Muddled at the margin. Students may confuse the idea of setting marginal benefit equal to

Module Outline

I. Costs, Benefits, and Profits

A. Explicit versus implicit costs

1. The true cost of anything (its opportunity cost) is what you must give up to get it.

Opportunity cost can be divided into explicit cost and implicit cost.

2. In considering the cost of an activity, you should include the cost of using any of your

own resources for that activity.

B. Accounting profit versus economic profit

1. Companies report their accounting profit, which is not necessarily equal to their

economic profit.

2. Businesses can face implicit costs for two reasons. First, a business’s capital could

have been put to use in some other way. Second, the owner devotes time and energy to

the business that could have been used elsewhere.

3. Forgone interest earnings from financial assets used to pay for college are used to

illustrate implicit cost of capital.

C. Making “either-or” decisions

1. An either-or decision requires you to choose between two projects.

II. Making “How Much” Decisions: The Role of Marginal Analysis

A. Marginal analysis involves comparing the benefit of doing a little bit more of some activity

B. Marginal cost

1. For the production of some goods, the shape of the marginal cost curve changes as

more output is produced. Marginal cost may first decrease, then become constant, then

increase.

2. The simple case is to assume increasing marginal cost.

C. Marginal benefit

1. In some cases marginal benefit is constant, such as when the perfectly competitive

firm takes market price as given. Each unit sold yields the same price, or marginal

benefit.

2. The example in this Module assumes decreasing marginal benefit.

D. Marginal analysis

1. The profit of an activity is the difference between the marginal benefit and the

marginal cost. Profit can be calculated for each unit of a good produced.

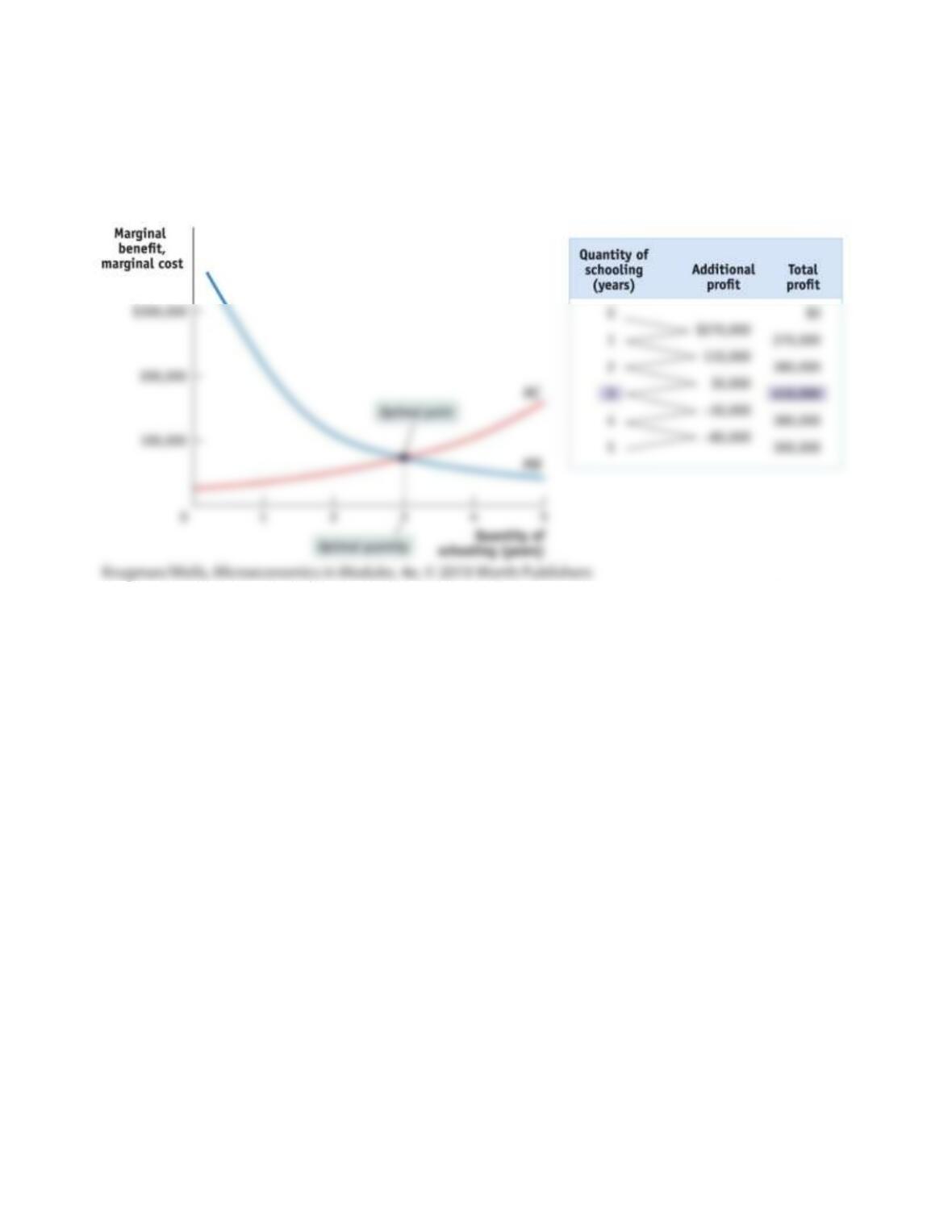

2. The optimal quantity is the quantity that generates the highest possible profit.

Module 17 krugman 4

3. Total profit is the sum of the profit earned in each individual year for the schooling

example, or for all of the units of the good produced.

4. Text Figure 17-3 illustrates the optimal quantity as the quantity whose marginal

benefit is equal to marginal cost.

Figure 17-3

5. According to the profit-maximizing principle of marginal analysis, when faced with a

profit-maximizing “how much” decision, the optimal quantity is the largest quantity at

which the marginal benefit is greater than or equal to marginal cost.

E. A principle with many uses

1. The principle of marginal analysis can be applied to a variety of “how much”

decisions, including those whose benefits and costs are not measured in dollars.

2. Some examples:

a. A consumer has to decide how to allocate a weekly budget between restaurant

meals and mocha lattes.

b. A producer has to decide on the size of a new store.

c. A physician has to decide on the optimal dosage of a drug by considering the

marginal cost in terms of side effects versus the marginal benefit in terms of

fighting the disease.

III. Sunk Costs

A. A sunk cost should be ignored in decisions about future actions.

B. The choice between replacing parts on a car or selling the car and buying another car is used

in the text to illustrate sunk costs.

Case Studies in the Text

Economics in Action

Module 17 krugman 5

The Cost of a Life—This EIA considers the “marginal cost of a life” and the role it can or does play in

policy decisions.

Ask students the following questions:

2. Can we make an efficient decision about using our resources for a particular policy (like

Module 17 krugman 6

Handout 17-1

Date_________ Name____________________________ Class________ Professor________________

College Opportunity Costs?

Consider the costs of attending college. Write the costs in the appropriate column and estimate the

amount of each cost. Sum the implicit costs. Sum the explicit costs. Then, calculate the opportunity

cost of attending college.

Implicit cost

Estimate

Explicit cost

Estimate

Total implicit costs

Total explicit costs

Module 17 krugman 7

Handout 17-2

Date_________ Name____________________________ Class________ Professor________________

Explicit and Implicit Costs

Consider the following scenario and answer the questions that follow.

Larry has decided to quit his job working at Quickie-lube and become an entrepreneur. He had been

earning $2,500 per month performing oil changes. Since he has his own garage, which he had been

renting out for $400 per month, he has decided to open his own oil-changing business. His monthly

costs and revenue are shown in the following list. Note: we are assuming no depreciation.

Price of oil change = $25

Oil changes per month = 200

Cost of oil = $5 per oil change

Equipment rental = $200 per month

Other expenses = $1,000 per month

1. What is Larry’s total revenue for the month?

2. What are Larry’s explicit costs for the month?

3. If an accountant figured Larry’s profit, what would it equal?

4. What costs does Larry have that are not considered by the accountant?

5. If an economist calculated Larry’s profit, what would it equal?

6. What does the negative economic profit signal to Larry?

Module 17 krugman 8

Answers

Larry has decided to quit his job working at Quickie-lube and become an entrepreneur. He had been

earning $2,500 per month performing oil changes. Since he has his own garage, which he had been

renting out for $400 per month, he has decided to open his own oil-changing business. His monthly

costs and revenue are shown in the following list. Note: we are assuming no depreciation.

Price of oil change = $25

Oil changes per month = 200

Cost of oil = $5 per oil change

Equipment rental = $200 per month

Other expenses = $1,000 per month

Have the class work through the answers to each of the following questions:

6. What does the negative economic profit signal to Larry? (His accounting profit is $2,800. If

Module 17 krugman 9

Handout 17-3

Date_________ Name____________________________ Class________ Professor________________

Carpet Cleaning

Sam begins to clean carpets for family and friends. He is trying to determine the optimal quantity of

carpets to clean. In the table below, calculate Sam’s marginal costs and marginal benefits. Also,

calculate his total gain at each quantity of carpets cleaned.

Quantity of

carpets

cleaned

Total

cost

Marginal

cost

Total

benefit

(price)

Marginal

benefit

Total

net gain

0

$ 0

$—

$ 0

$—

$—

1

20

60

2

42

110

3

68

150

4

100

180

5

140

200

What is Sam’s optimal number of carpets cleaned? Is this the point of maximum total net gain?

What is happening to marginal benefits as the number of carpets cleaned increases? Why is this

happening?

What is happening to marginal costs as the number of carpets cleaned increases? Why is this

happening?

Module 17 krugman 10

Answers:

Sam begins to clean carpets for family and friends. He is trying to determine the optimal quantity of

carpets to clean. In the table below, calculate Sam’s marginal costs and marginal benefits. Also,

calculate his total gain at each quantity of carpets cleaned.

Quantity of

carpets

cleaned

Total

cost

Marginal

cost

Total

benefit

(price)

Marginal

benefit

Total

net gain

0

$ 0

$—

$ 0

$—

$—

What is Sam’s optimal number of carpets cleaned? Is this the point of maximum total net gain?

What is happening to marginal benefits as the number of carpets cleaned increases? Why is this

happening?

What is happening to marginal costs as the number of carpets cleaned increases? Why is this

happening?

Module 17 krugman 11

Handout 17-4

Date_________ Name____________________________ Class________ Professor________________

Ski Rental Costs

Calculate the accounting profit and economic profit for the following case study.

The owner of Crested Butte Ski Rentals purchased $150,000 worth of skis for rentals. The revenue from

the rentals is $300,000. Utilities are $20,000 per year and wages are $50,000. There is an outstanding

loan, and the interest owing per year is $12,000. If the skis had not been purchased, the owner could

earn $11,500 in annual interest income on the $150,000 otherwise used to buy the skis. The owner

was offered a managerial position at another ski shop for $40,000 a year.

Accounting profit

Accounting profit

Economic profit

Accounting profit

Revenues:

Revenues:

Costs:

Costs:

Total cost:

Total cost:

Total accounting

profit:

Total economic

profit:

Should the owner continue in business? Why?

Module 17 krugman 12

Answers

Accounting profit

Accounting profit

Economic profit

Accounting profit

Costs:

Costs:

Total cost:

Total cost:

profit:

profit:

Should the owner continue in business? Why?

Revenues:

Revenues:

Module 17 krugman 13

Handout 17-5

Date_________ Name____________________________ Class________ Professor________________

Expensive Babies

In her book The Price of Motherhood, Ann Crittenden claims the total cost for a college-educated

couple to have a child is $1 million over the child’s lifetime. She discusses the following items as the

costs of an educated woman having a child. Classify these as explicit or implicit costs of having a child.

1. Unearned social security credits

2. Forgone promotions

3. Salary while not working

4. Expenses for baby’s room

5. Loss of experience at work

6. Depreciation of work skills

7. Food and clothing for the child

8. Loss of pension benefits

9. Awards given for excellence in your paid job

10. Babysitting fees

11. Preschool expenses

12. Earnings from paid work contributed by an employer to a retirement account

13. Doctor visits/medical expenses

14. Costs of decorating child’s room

15. Lost training opportunities at work

Module 17 krugman 14

Answers