Chapter 3: Accounting Transactions

Learning Objectives

At the completion of this chapter the student should be able to:

• Explain what accounting transactions result in costs or revenues being recorded to the job cost

ledger.

• Explain the difference between recording an expense or revenue and the recording the

associated cash flow when using the percentage of completion accounting method.

• Explain when retention becomes a revenue and how keep uncollectible retention separate from

Instructional Hints

• The question is often raised, “Do construction managers really need to understand how

accounting transactions are made to be in order to be good construction managers? Is not

handling accounting transactions what we hire accountants for?” I use the teaching of

and 3-24 (which show bills being charge to a job) and Example 3-13 (which show the client being

billed) can help the student understand the timing deference between costs and revenues. It is

3-24, and 3-28 can be used to teach the students when this happens.

o It is important for financial managers in construction companies to understand that when using

percentage of completion accounting system the recording of a bill to the accounting systems

does not create a cash flow until the bill is paid. Examples 3-1, 3-2, 3-13, and 3-14 (which shows

how to record bills) and Examples 3-3 and 3-15 (which shows how to record payments) can be

this point. Examples 3-2, 3-13, and 3-14 can be used to help the student understand how

retention is kept separate until it becomes collectable.

o It is important for financial managers in construction companies to understand how to

accumulate the funds needed to pay for a jobsite employee’s vacation by billing each

construction project each pay period for the accrued vacation. Examples 3-5 and 3-9 can help

lease.

Activities

• Invite a construction accountant from industry to discuss construction accounting. Be sure they

discuss the unique characteristics of construction accounting, including job costing and

allocation of equipment costs.

Instruction Resources

• The figures from this chapter in electronic format and PowerPoint slides can be found at the

instructor’s website.

Solutions to the Textbook Problems

1. When the changes to the asset accounts are not equal to the changes to the liability and net

worth accounts on the balance sheet we know that the transactions are incorrect or additional

2. Invoice charged to a job without retention, invoiced charged to a job with retention, labor

charged to a job, labor charged to general overhead, recording office rent, recording office depreciation,

recording general overhead invoices, billing a client, loan payment, equipment depreciation, recording a

3. Paying invoices, paying an employee’s wages, paying payroll taxes, paying for benefits, receiving

payment from a client, purchase of equipment with a loan (if it includes a cash down payment), loan

4. Vacation time for jobsite employees, billing for retention, equipment charged to a job, purchase

5. An underbilling is where the company’s costs and profits (when the profits are uniformly

6. An overbilling is where the company’s billings to the client exceed the costs and profits (when

7. The solutions are as follows:

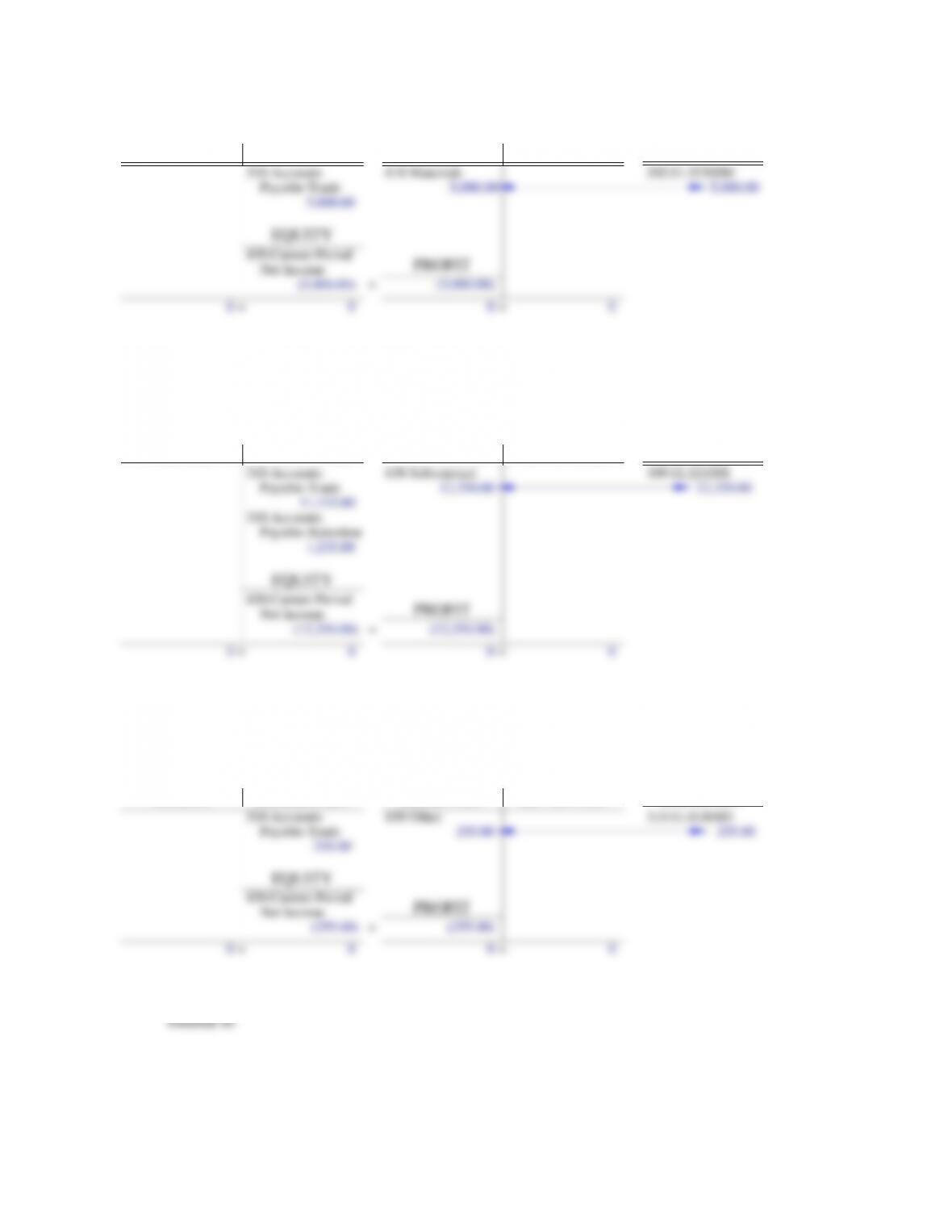

Invoice A:

BALANCE SHEET

ASSETS LIABILITIES

310 Accounts

5,000.00

INCOME STATEMENT

EXPENSES REVENUES EXPENSES

430 Current Period

Net Income

(5,000.00)

0

PROFIT

=

JOB COST

5,000.00 5,000.00

(5,000.00)

=0 =0 0

610 Materials 302.01.32300M

EQUITY

Payable-Trade

Invoice B:

BALANCE SHEET

ASSETS LIABILITIES

310 Accounts

11,115.00

INCOME STATEMENT

EXPENSES REVENUES EXPENSES

430 Current Period

Net Income

(12,350.00)

0

PROFIT

=

JOB COST

12,350.00 12,350.00

(12,350.00)

=0 =0 0

630 Subcontract 309.02.22100S

EQUITY

310 Accounts

1,235.00

Payable-Trade

Payable-Retention

Invoice C:

BALANCE SHEET

ASSETS LIABILITIES

310 Accounts

255.00

INCOME STATEMENT

EXPENSES REVENUES EXPENSES

430 Current Period

Net Income

(255.00)

0

PROFIT

=

JOB COST

255.00 255.00

(255.00)

=0 =0 0

650 Other 315.01.01800O

EQUITY

Payable-Trade

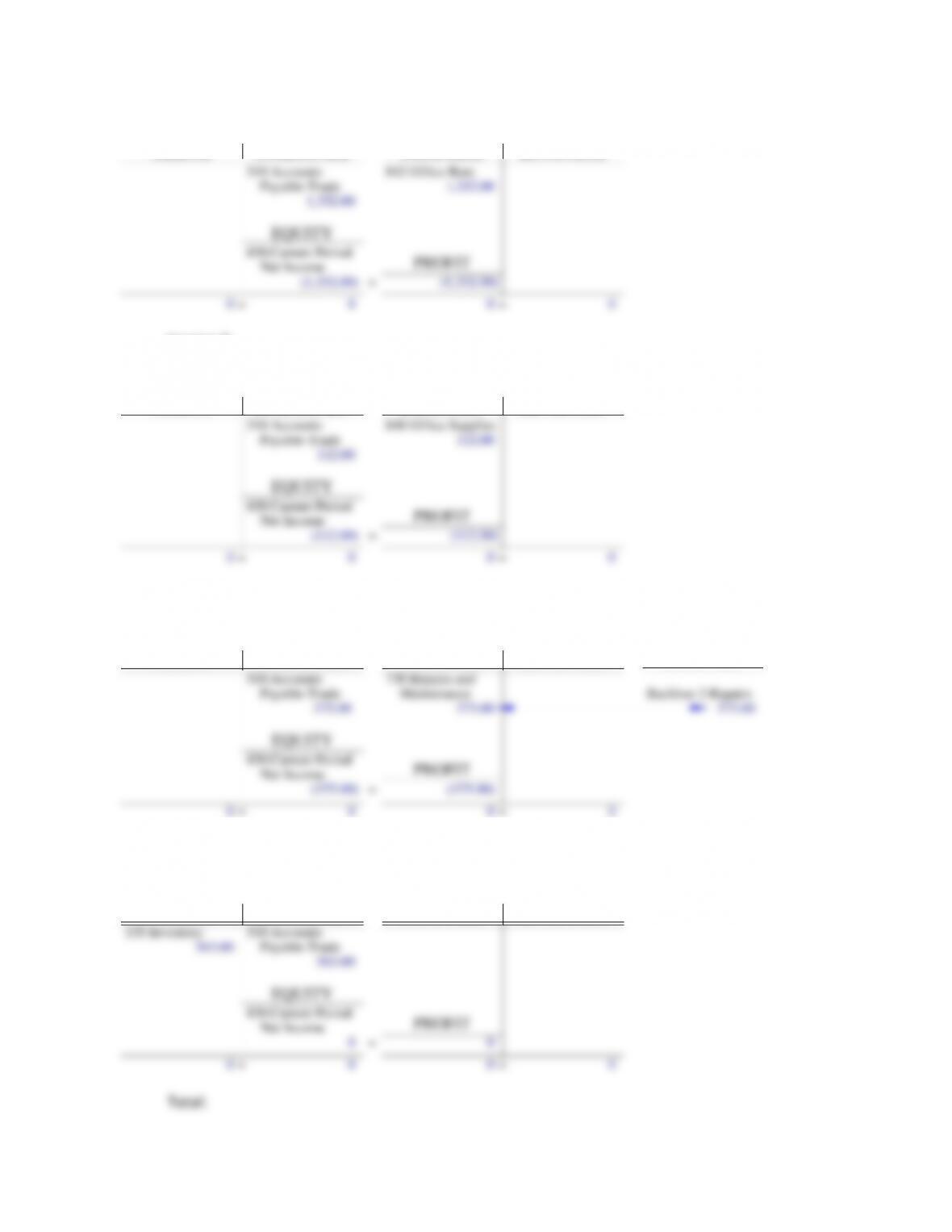

BALANCE SHEET

ASSETS LIABILITIES

310 Accounts

1,352.00

INCOME STATEMENT

EXPENSES REVENUES

430 Current Period

Net Income

(1,352.00)

0

PROFIT

=

1,352.00

(1,352.00)

=0 =0 0

842 Office Rent

EQUITY

Payable-Trade

Invoice E:

BALANCE SHEET

ASSETS LIABILITIES

310 Accounts

112.00

INCOME STATEMENT

EXPENSES REVENUES

430 Current Period

Net Income

(112.00)

0

PROFIT

=

112.00

(112.00)

=0 =0 0

840 Office Supplies

EQUITY

Payable-Trade

Invoice F:

BALANCE SHEET

ASSETS LIABILITIES

310 Accounts

375.00

INCOME STATEMENT

EXPENSES REVENUES EXPENSES

430 Current Period

Net Income

(375.00)

0

PROFIT

=

EQUIPMENT

375.00 375.00

(375.00)

=0 =0 0

730 Repairs and Backhoe 2-Repairs

EQUITY

Payable-Trade Maintenance

Invoice G:

BALANCE SHEET

ASSETS LIABILITIES

310 Accounts

563.00

INCOME STATEMENT

EXPENSES REVENUES

430 Current Period

Net Income 0

0

PROFIT

=0

=0 =0 0

EQUITY

130 Inventory

563.00 Payable-Trade

BALANCE SHEET

ASSETS LIABILITIES

310 Accounts

18,772.00

INCOME STATEMENT

EXPENSES REVENUES

EXPENSES

430 Current Period

Net Income

(19,444.00)

563.00

PROFIT

=

EQUIPMENT

5,000.00 5,000.00

(19,444.00)

=0 =563.00 0

610 Materials 302.01.32300M

EQUITY

130 Inventory

563.00 Payable-Trade

311 Accounts

1,235.00

Payable-Retention 12,350.00 12,350.00

630 Subcontract 309.02.22100S

255.00 255.00

650 Other 315.01.01800O

375.00 375.00

730 Repairs Backhoe 2 – Repairs

112.00

840 Office Supplies

1,352.00

842 Office Rent

8. The accrued payroll equals the wages paid to the employees less the deduction withheld from

the employees paycheck and is calculated as follows:

The accrued taxes equals the social security, Medicare, SUTA, and FUTA paid by the employer

plus the social security, Medicare, federal withholdings, and state withholdings withheld from the

costs for Employee 3 will be taken out of accrued vacation. Accrued vacation is calculated as follows:

must be divided up between the general overhead categories. The employee’s wages are $500. The

employee benefits include the health insurance premium paid by the employer and the allowance for

vacation, which is calculated as follows:

The employee taxes include the social security, Medicare, SUTA, and FUTA paid by the employer

and is calculated as follows:

BALANCE SHEET

ASSETS LIABILITIES

340 Accrued Payroll

1,200.57

INCOME STATEMENT

EXPENSES REVENUES EXPENSES

430 Current Period

Net Income

(2,028.66)

0

PROFIT

=

JOB COST

1,373.21 813.62

(2,028.66)

=0 =0 0

620 Labor 302.01.01100L

EQUITY

342 Accrued Taxes

621.26

343 Accrued

Insurance 573.50

344 Accrued

Vacation(366.67)

500.00

820 Employee

Wages & Salaries

73.20

821 Employee

Benefits

57.25

825 Employee

Taxes

25.00

830 Insurance

139.90

302.01.06110L

419.69

302.01.06210L

9. The accrued payroll from Problem 2 is $1,200.57. The solution is as follows:

BALANCE SHEET

ASSETS LIABILITIES

340 Accrued Payroll

(1,200.57)

INCOME STATEMENT

EXPENSES REVENUES EXPENSES

430 Current Period

Net Income 0

(1,200.57)

PROFIT

=

JOB COST

0

=0 =(1,200.57) 0

EQUITY

110 Cash (1,200.57)

10. Because the concrete invoice was previously entered into the accounting system, there is no

change to the job cost ledger. The solution is as follows:

BALANCE SHEET

ASSETS LIABILITIES

310 Accounts

(5,000.00)

INCOME STATEMENT

EXPENSES REVENUES EXPENSES

430 Current Period

PROFIT

JOB COST

EQUITY

342 Accrued Taxes

(2,273.80)

343 Accrued

Insurance

(1,732.00)

Payable-Trade

110 Cash(9,005.80)

11. The $118,268 needs to be moved from accounts receivable-retention to accounts receivable-

trade and has been previously recognized as income; therefore, it should not be included as income. The

solution is as follows:

BALANCE SHEET

ASSETS LIABILITIES

120 Accounts

Receivable –

368,264.00

INCOME STATEMENT

EXPENSES REVENUES REVENUE

430 Current Period

Net Income

249,996.00

249,996.00

PROFIT

=

JOB COST

249,996.00 249,996.00

249,996.00

=249,996.00 =249,996.00 249,996.00

500 Revenue 313 Revenue

EQUITY

121 Accounts

Retention

(118,268.00)

Receivable –

Trade

12. The solution is as follows:

BALANCE SHEET

ASSETS LIABILITIES

110 Cash

368,264.00

INCOME STATEMENT

EXPENSES REVENUES EXPENSES

430 Current Period

Net Income 0

0

PROFIT

=

JOB COST

0

=0 =0 0

EQUITY

(368,264.00)

120 Accounts

Receivable –

Trade

13. The construction equipment account will see an increase of $115,200 as a result of the purchase

of the new loader and a decrease of $95,000 as a result of the sale of the old loader for a net change of

BALANCE SHEET

ASSETS LIABILITIES

380 Long-Term

Liabilities

100,000.00

INCOME STATEMENT

EXPENSES REVENUES EXPENSES

Net Income

PROFIT

EQUIPMENT

220 Construction

Equipment

20,200.00

910 Other Income

3,430.00

14. The lease is considered an operating lease and no changes will occur until a lease payment is

made.

15. The lease is considered a capital lease. The solution is as follows:

BALANCE SHEET

ASSETS LIABILITIES

350 Capital Lease

Payable

55,000.00

INCOME STATEMENT

EXPENSES REVENUES EXPENSES

430 Current Period

Net Income 0

55,000.00

PROFIT

=

EQUIPMENT

0

=0 =55,000.00 0

EQUITY

260 Capital Leases

55,000.00

16. The reduction in the loan principal is $1,042 ($1,312 – $270). The interest on the lease is $358

($1,050 – $692). The total interest is $628 ($270 + $358). The solution is as follows:

BALANCE SHEET

ASSETS LIABILITIES

350 Capital Lease

Payable

( 692.00)

INCOME STATEMENT

EXPENSES REVENUES EXPENSES

430 Current Period

Net Income

( 628.00)

(2,362.00)

PROFIT

=

EQUIPMENT

( 628.00)

=0 =(2,362.00) 0

EQUITY

110 Cash (2,362.00) 881 Interest

628.00

Expense

380 Long-Term

Liabilities

(1,042.00)

17. The solution is as follows:

BALANCE SHEET

ASSETS LIABILITIES INCOME STATEMENT

EXPENSES REVENUES EXPENSES

430 Current Period

Net Income

PROFIT

=

EQUIPMENT

917.00 917.00

Payments Truck 11-Rent and

EQUITY

250 Less Acc.

Depreciation

4,420.00

Lease Payments

260 Capital Leases

( 917.00) 1,920.00 1,920.00

720 Depreciation Loader 3

Depreciation

710 Rent and Lease

2,500.00

819 Depreciation

18. The solution is as follows:

BALANCE SHEET

ASSETS LIABILITIES INCOME STATEMENT

EXPENSES REVENUES EXPENSES

430 Current Period

Net Income50.00

0

PROFIT

=

JOB COST

50.00

50.00

=0 =

0 0

to Employees

EQUITY

340 Accrued Payroll

(50.00)

Costs Charged

798 Equipment

Because 798 Equipment Costs Charged to Employees and 799 Equipment Costs Charged to Jobs are a contra

accounts, they are subtracted rather than added when totaling the column.

600 00 650.00

to Jobs Equipment Costs

Allocated

Costs Charged

799 Equipment

640 Equipment

600.00

EXPENSES

EQUIPMENT

302.01.01100E

600.00

Truck 22

19. The solution is as follows:

BALANCE SHEET

ASSETS LIABILITIES

130 Inventory

(200.00)

INCOME STATEMENT

EXPENSES REVENUES EXPENSES

430 Current Period

Net Income

(200.00)

(200.00)

PROFIT

=

JOB COST

200.00 200.00

(200.00)

=0 =(200.00) 0

610 Materials 302.01.06110M

EQUITY

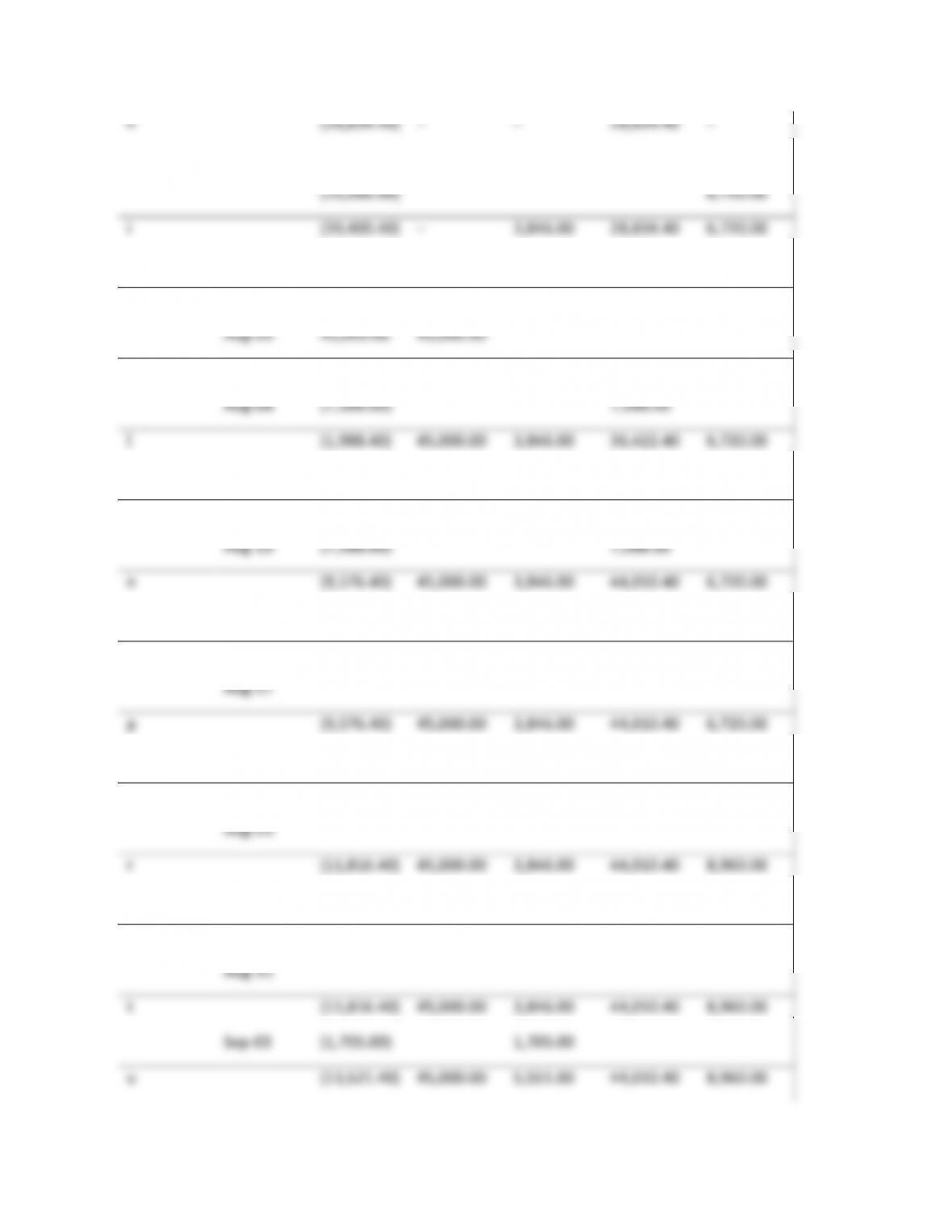

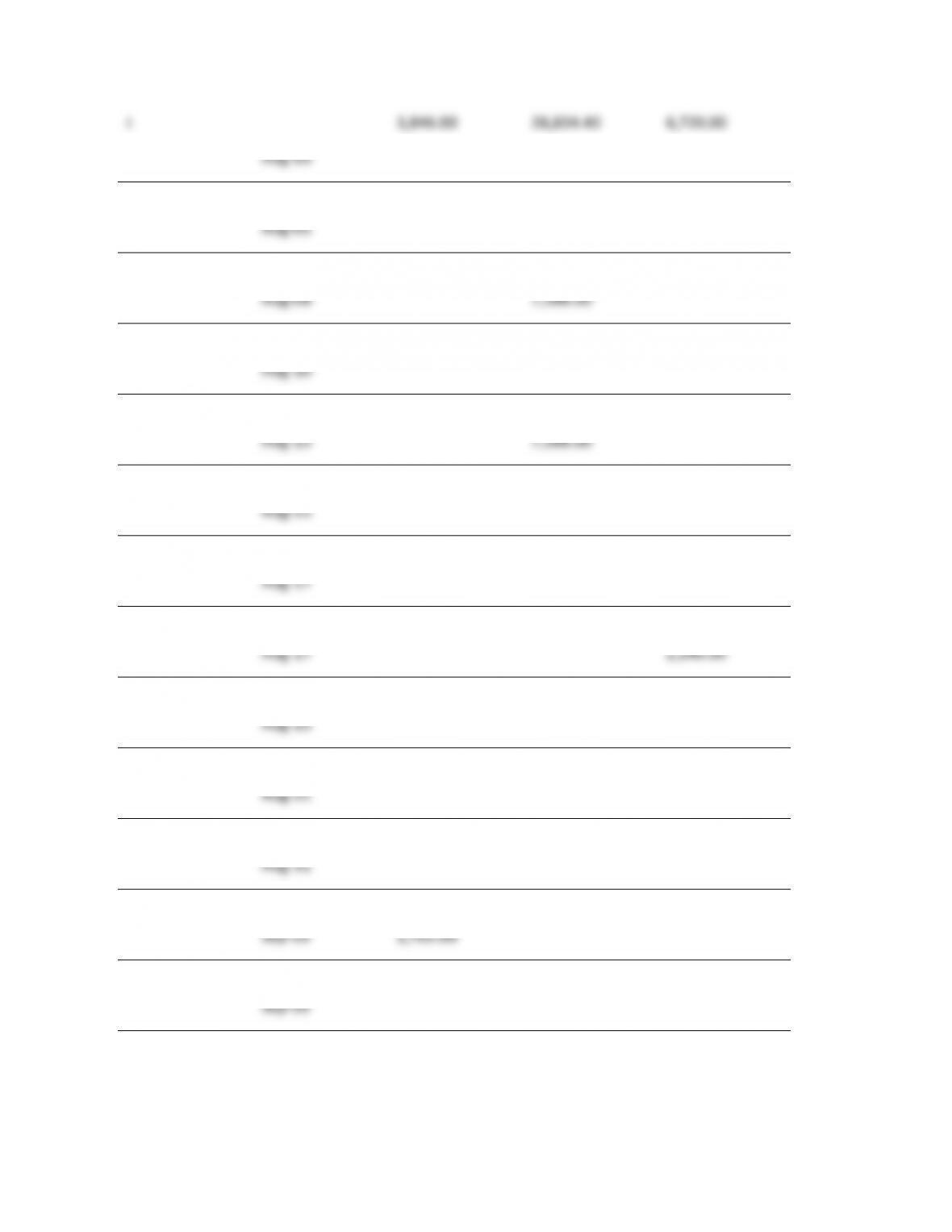

20. The accounts on the balance sheet are as follows after each transaction:

Balance Sheet

Date

110 Cash

120

Accounts

Receivabl

e

310

Accounts

Payable

340

Accrued

Payroll

342

Accrued

Taxes

343

Accrued

Insuran

ce

430

Current

Period Net

Income

Jul–11

4,299.52

602.88

425.92

(6,070.40)

142.08

38.08

268.16

288.00

5.76

a

4,299.52

1,018.88

752.00

(6,070.40)

Jul–13

(4,299.52)

(4,299.52

)

b

(4,299.52)

–

–

–

1,018.88

752.00

(6,070.40)

Jul–18

5,374.40

753.60

532.40

(7,588.00)

177.60

47.60

335.20

360.00

7.20

c

(4,299.52)

–

–

5,374.40

2,292.48

1,692.0

0

(13,658.40

)

Jul–20

(5,374.40)

(5,374.40

)

d

(9,673.92)

–

–

–

2,292.48

1,692.0

0

(13,658.40

)

Jul–25

5,374.40

753.60

532.40

(7,588.00)

177.60

47.60

335.20

360.00

7.20

e

(9,673.92)

–

–

5,374.40

3,566.08

2,632.0

0

(21,246.40

)

Jul–27

(5,374.40)

(5,374.40

)

f

(15,048.32

)

–

–

–

3,566.08

2,632.0

0

(21,246.40

)

Jul–31

(3,566.08)

(3,566.08

)

(2,632.00)

(2,632.0

0)

g

(21,246.40

)

–

–

–

–

–

(21,246.40

)

Aug–01

5,374.40

753.60

532.40

(7,588.00)

177.60

47.60

335.20

360.00

7.20

h

(21,246.40

)

–

–

5,374.40

1,273.60

940.00

(28,834.40

)

Aug–02

3,846.00

6,720.00

(10,566.00

)

i

(21,246.40

)

–

10,566.00

5,374.40

1,273.60

940.00

(39,400.40

)

Aug–03

(5,374.40)

(5,374.40

)

j

(26,620.80

)

–

10,566.00

–

1,273.60

940.00

(39,400.40

)

Aug–05

45,000.00

45,000.00

k

(26,620.80

)

45,000.00

10,566.00

–

1,273.60

940.00

5,599.60

Aug–08

5,374.40

753.60

532.40

(7,588.00)

177.60

47.60

335.20

360.00

7.20

l

(26,620.80

)

45,000.00

10,566.00

5,374.40

2,547.20

1,880.0

0

(1,988.40)

Aug–10

(5,374.40)

(5,374.40

)

m

(31,995.20

)

45,000.00

10,566.00

–

2,547.20

1,880.0

0

(1,988.40)

Aug–15

5,374.40

753.60

532.40

(7,588.00)

177.60

47.60

335.20

360.00

7.20

n

(31,995.20

)

45,000.00

10,566.00

5,374.40

3,820.80

2,820.0

0

(9,576.40)

Aug–15

(10,566.00

)

(10,566.0

0)

o

(42,561.20

)

45,000.00

–

5,374.40

3,820.80

2,820.0

0

(9,576.40)

Aug–17

(5,374.40)

(5,374.40

)

p

(47,935.60

)

45,000.00

–

–

3,820.80

2,820.0

0

(9,576.40)

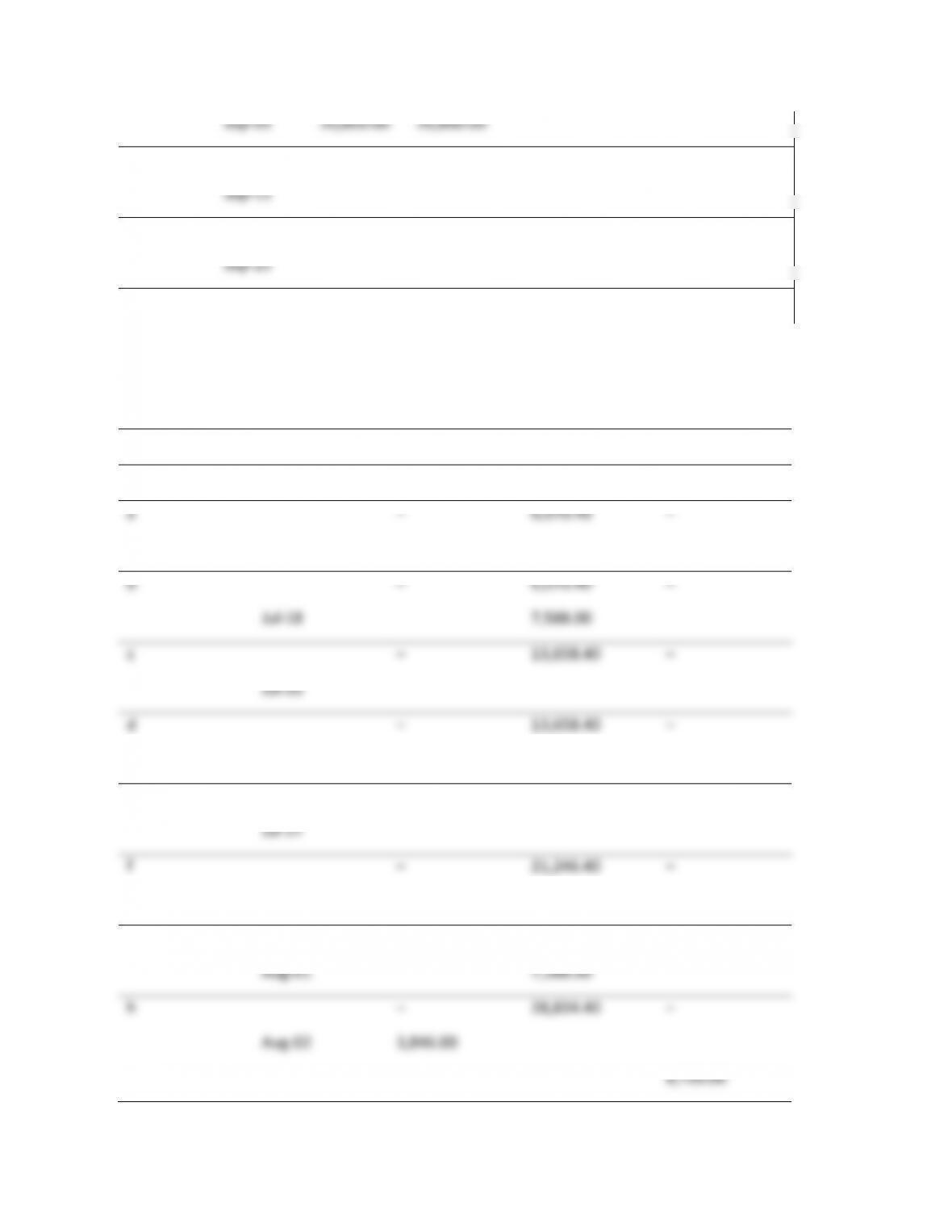

Balance Sheet

Date

110 Cash

120

Accounts

Receivabl

e

310

Accounts

Payable

340

Accrued

Payroll

342

Accrued

Taxes

343

Accrued

Insuranc

e

430 Current

Period Net

Income

Aug–17

2,240.00

(2,240.00)

q

(47,935.6

0)

45,000.00

2,240.00

–

3,820.80

2,820.00

(11,816.40)

Aug–25

45,000.00

(45,000.00

)

r

(2,935.60)

–

2,240.00

–

3,820.80

2,820.00

(11,816.40)

Aug–31

(3,820.80)

(3,820.80

)

(2,820.00)

(2,820.0

0)

s

(9,576.40)

–

2,240.00

–

–

–

(11,816.40)

Aug–31

(2,240.00)

(2,240.00

)

t

(11,816.4

0)

–

–

–

–

–

(11,816.40)

Sep-03

1,705.00

(1,705.00)

u

(11,816.4

0)

–

1,705.00

–

–

–

(13,521.40)

Sep-05

20,800.00

20,800.00

v

(11,816.4

0)

20,800.00

1,705.00

–

–

–

7,278.60

Sep-15

(1,705.00)

(1,705.00

)

w

(13,521.4

0)

20,800.00

–

–

–

–

7,278.60

Sep-25

20,800.00

(20,800.00

)

x

7,278.60

–

–

–

–

–

7,278.60

The accounts on the income sheet are as follows after each transaction:

Income Statement

Date

Profit

500

Revenue

610

Materials

620 Labor

640

Equipment

Jul–11

(6,070.40)

6,070.40

a

(6,070.40)

–

–

6,070.40

–

Jul–13

b

(6,070.40)

–

–

6,070.40

–

Jul–18

(7,588.00)

7,588.00

c

(13,658.40)

–

–

13,658.40

–

Jul–20

d

(13,658.40)

–

–

13,658.40

–

Jul–25

(7,588.00)

7,588.00

e

(21,246.40)

–

–

21,246.40

–

Jul–27

f

(21,246.40)

–

–

21,246.40

–

Jul–31

g

(21,246.40)

–

–

21,246.40

–

Aug–01

(7,588.00)

7,588.00

h

(28,834.40)

–

–

28,834.40

–

Aug–02

3,846.00

(10,566.00)

6,720.00

i

(39,400.40)

–

3,846.00

28,834.40

6,720.00

Aug–03

j

(39,400.40)

–

3,846.00

28,834.40

6,720.00

Aug–05

45,000.00

45,000.00

k

5,599.60

45,000.00

3,846.00

28,834.40

6,720.00

Aug–08

(7,588.00)

7,588.00

l

(1,988.40)

45,000.00

3,846.00

36,422.40

6,720.00

Aug–10

m

(1,988.40)

45,000.00

3,846.00

36,422.40

6,720.00

Aug–15

(7,588.00)

7,588.00

n

(9,576.40)

45,000.00

3,846.00

44,010.40

6,720.00

Aug–15

o

(9,576.40)

45,000.00

3,846.00

44,010.40

6,720.00

Aug–17

p

(9,576.40)

45,000.00

3,846.00

44,010.40

6,720.00

Aug–17

(2,240.00)

2,240.00

q

(11,816.40)

45,000.00

3,846.00

44,010.40

8,960.00

Aug–25

r

(11,816.40)

45,000.00

3,846.00

44,010.40

8,960.00

Aug–31

s

(11,816.40)

45,000.00

3,846.00

44,010.40

8,960.00

Aug–31

t

(11,816.40)

45,000.00

3,846.00

44,010.40

8,960.00

Sep-03

(1,705.00)

1,705.00

u

(13,521.40)

45,000.00

5,551.00

44,010.40

8,960.00

Sep-05

20,800.00

20,800.00

v

7,278.60

65,800.00

5,551.00

44,010.40

8,960.00

Sep-15

w

7,278.60

65,800.00

5,551.00

44,010.40

8,960.00

Sep-25

x

7,278.60

65,800.00

5,551.00

44,010.40

8,960.00

The accounts on the job cost ledger are as follows after each transaction:

Job Cost

Date

1005.0611M

1005.0611L

1005.0611E

Jul–11

6,070.40

a

–

6,070.40

–

Jul–13

b

–

6,070.40

–

Jul–18

7,588.00

c

–

13,658.40

–

Jul–20

d

–

13,658.40

–

Jul–25

7,588.00

e

–

21,246.40

–

Jul–27

f

–

21,246.40

–

Jul–31

g

–

21,246.40

–

Aug–01

7,588.00

h

–

28,834.40

–

Aug–02

3,846.00

6,720.00

i

3,846.00

28,834.40

6,720.00

Aug–03

j

3,846.00

28,834.40

6,720.00

Aug–05

k

3,846.00

28,834.40

6,720.00

Aug–08

7,588.00

l

3,846.00

36,422.40

6,720.00

Aug–10

m

3,846.00

36,422.40

6,720.00

Aug–15

7,588.00

n

3,846.00

44,010.40

6,720.00

Aug–15

o

3,846.00

44,010.40

6,720.00

Aug–17

p

3,846.00

44,010.40

6,720.00

Aug–17

2,240.00

q

3,846.00

44,010.40

8,960.00

Aug–25

r

3,846.00

44,010.40

8,960.00

Aug–31

s

3,846.00

44,010.40

8,960.00

Aug–31

t

3,846.00

44,010.40

8,960.00

Sep-03

1,705.00

u

5,551.00

44,010.40

8,960.00

Sep-05

v

5,551.00

44,010.40

8,960.00

Sep-15

w

5,551.00

44,010.40

8,960.00

Sep-25

x

5,551.00

44,010.40

8,960.00

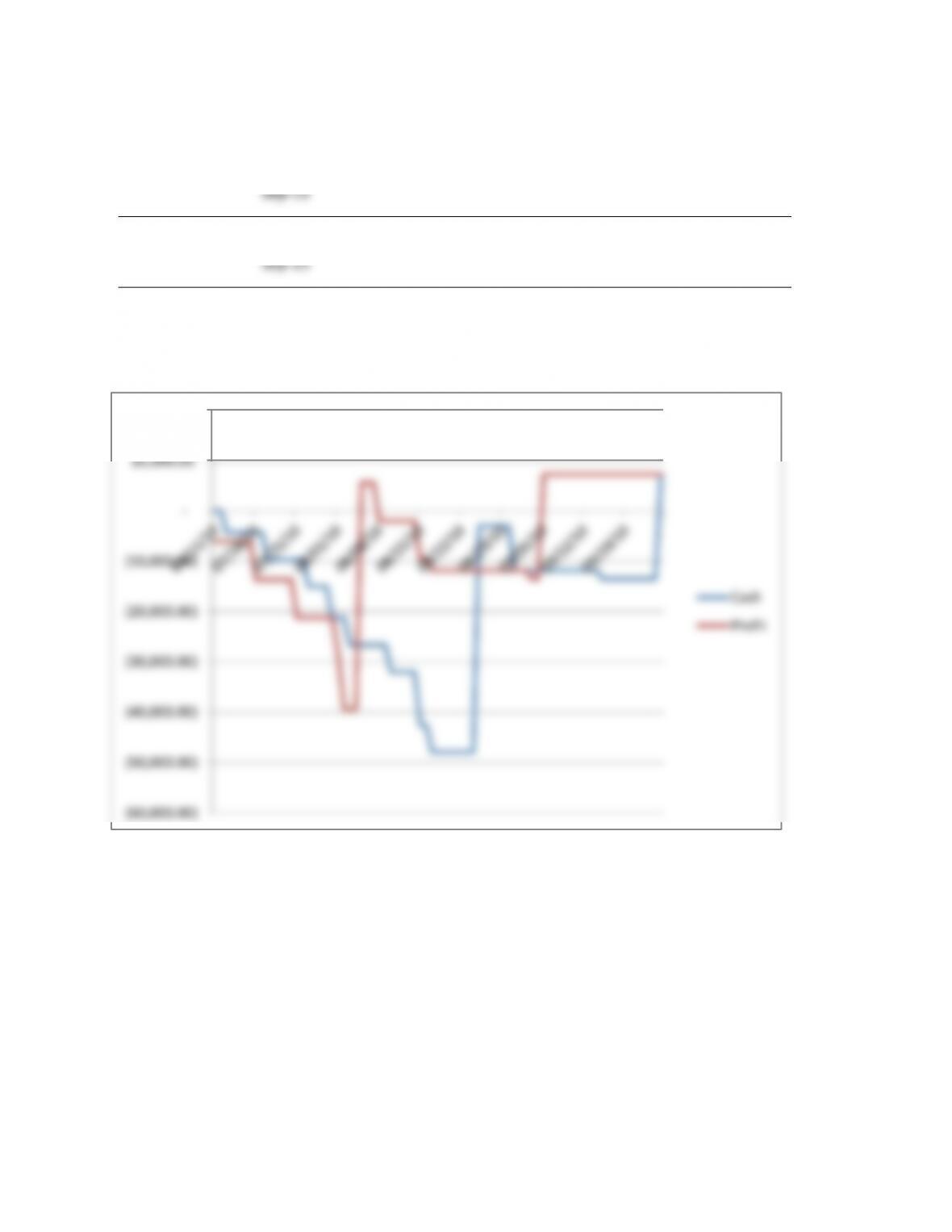

The cash and profits are as follows.

(60,000.00)

(50,000.00)

(40,000.00)

(30,000.00)

(20,000.00)

(10,000.00)

–

10,000.00

20,000.00

Cash

Profit