367

Chapter 20: Engineering Economics

20.1 Compute the future value of the following deposits made today:

(a) $10,000 at 6.75% compounding annually for 10 years

(b) $10,000 at 6.75% compounding quarterly for 10 years

(c) $10,000 at 6.75% compounding monthly for 10 years

SOLUTION

20.2 Compute the interest earned on the deposits made in Problem 20.1.

SOLUTION

20.3 How much money do you need to deposit in a bank today if you are planning to

have $5000 in 4 years by the time you get out of college? The bank offers a

6.75% interest rate that compounds monthly.

368

SOLUTION

20.4 How much money do you need to deposit in a bank each month if you are

planning to have $5000 in 4 years by the time you get out of college? The bank

offers a 6.75% interest rate that compounds monthly.

SOLUTION

1

12

0675.0

1

11

)12)(4(

m

i

20.5 Determine the effective rate corresponding to the following nominal rates

(a) 6.25% compounding monthly

(b) 9.25% compounding monthly

(c) 16.9% compounding monthly

SOLUTION

0625.0

12

m

i

12

eff m

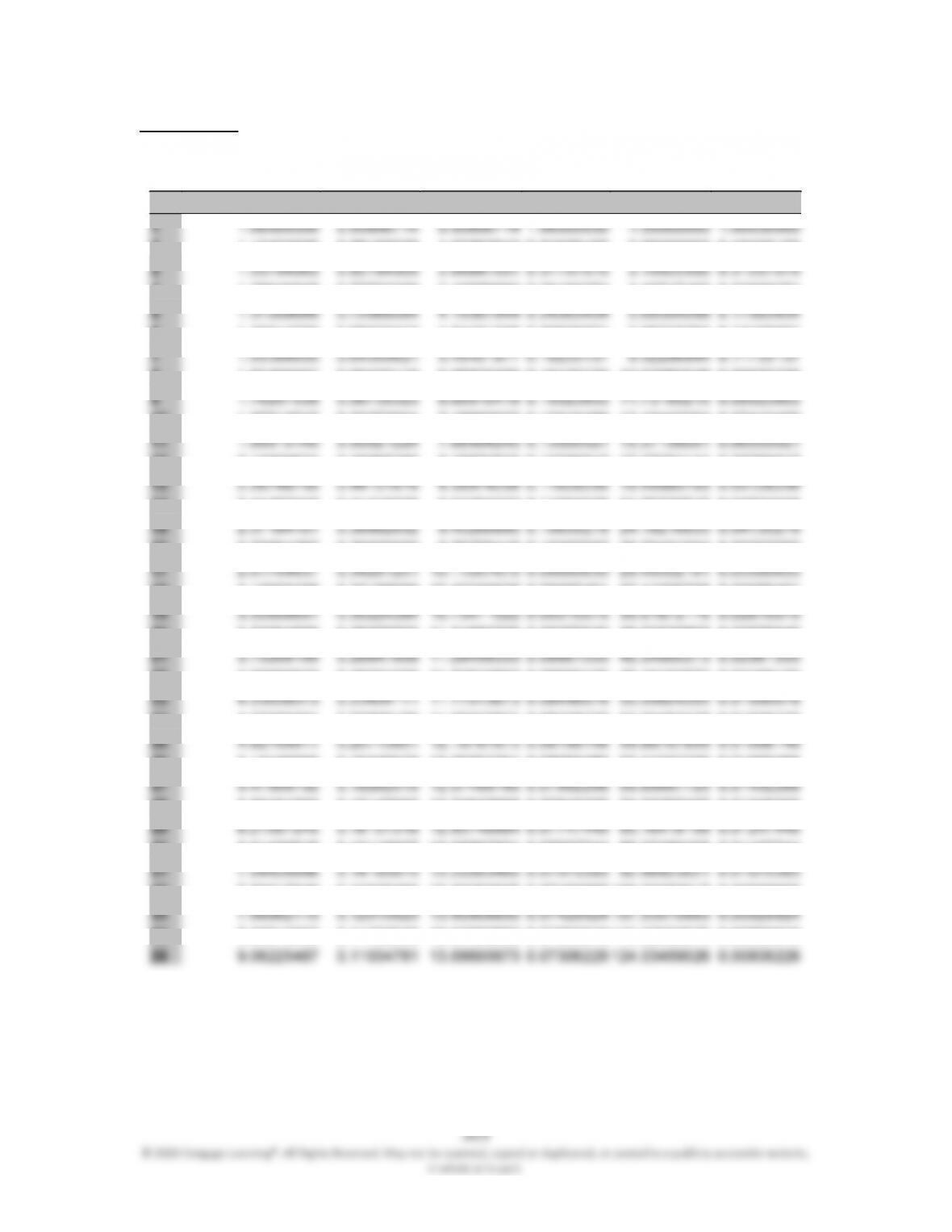

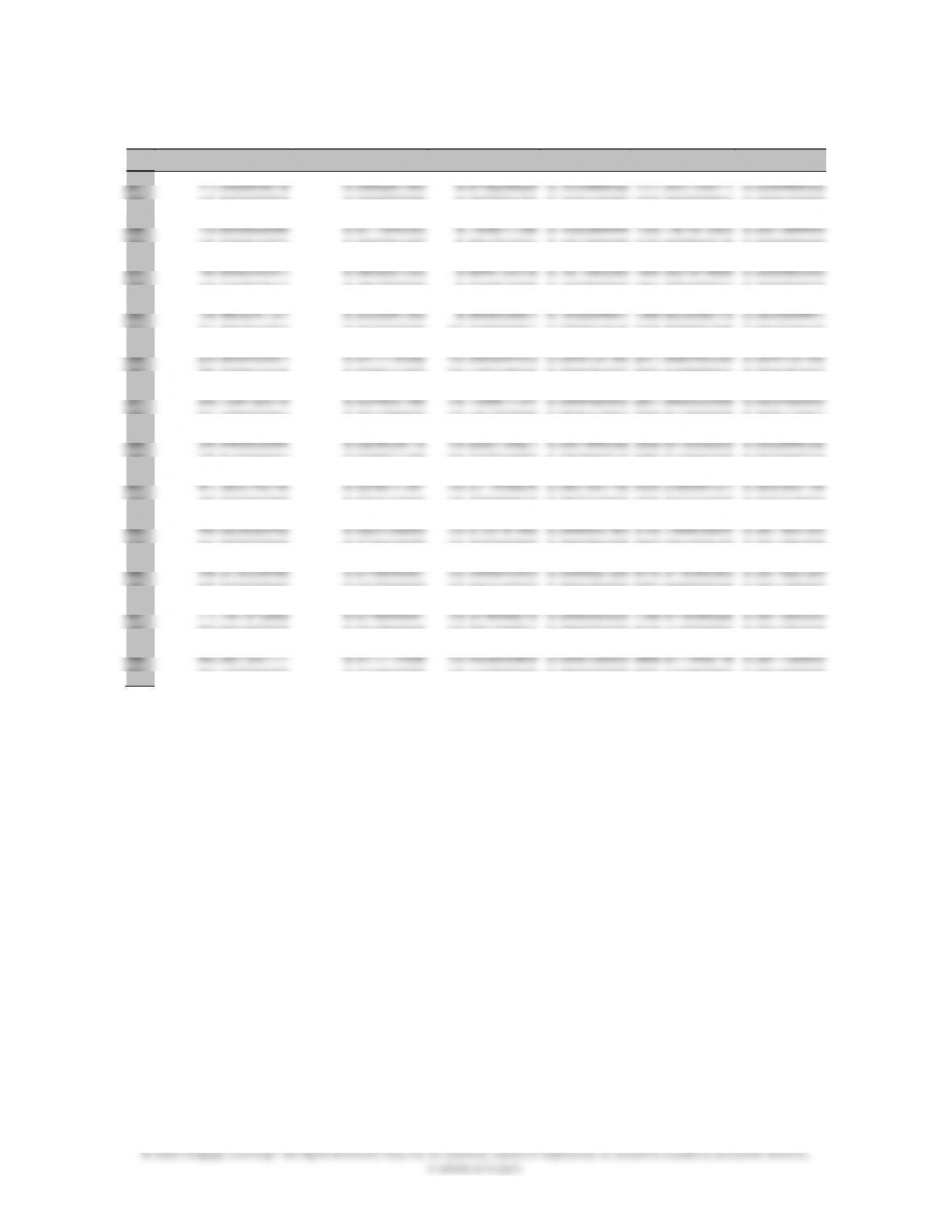

20.6 Using Excel or a spreadsheet of your choice, create interest-time factor tables,

similar to Table 20.9, for i = 6.5%, and i = 6.75%.

SOLUTION

The Interest-Time Factors for i =

6.5%

n (F/P, i, n)

(P/F, i, n)

(P/A, i, n)

(A/P, i, n)

(F/A, i, n)

(A/F, i, n)

1

2

1.13422500

0.88165928

1.82062642

0.54926150

2.06500000

0.48426150

3

4

1.28646635

0.77732309

3.42579860

0.29190274

4.40717462

0.22690274

5

6

1.45914230

0.68533412

4.84101356

0.20656831

7.06372764

0.14156831

7

8

1.65499567

0.60423119

6.08875096

0.16423730

10.07685648

0.09923730

9

10

1.87713747

0.53272604

7.18883022

0.13910469

13.49442254

0.07410469

11

12

2.12909624

0.46968285

8.15872532

0.12256817

17.37071141

0.05756817

13

14

2.41487418

0.41410025

9.01384233

0.11094048

21.76729515

0.04594048

15

16

2.73901067

0.36509533

9.76776418

0.10237757

26.75401034

0.03737757

17

18

3.10665438

0.32188969

10.43246638

0.09585461

32.41006738

0.03085461

19

20

3.52364506

0.28379703

11.01850725

0.09075640

38.82530867

0.02575640

21

22

3.99660632

0.25021228

11.53519562

0.08669120

46.10163573

0.02169120

23

24

4.53305081

0.22060198

11.99073871

0.08339770

54.35462778

0.01839770

25

26

5.14149955

0.19449579

12.39237251

0.08069480

63.71537769

0.01569480

27

28

5.83161733

0.17147902

12.74647668

0.07845305

74.33257427

0.01345305

29

30

6.61436616

0.15118607

13.05867591

0.07657744

86.37486405

0.01157744

31

32

7.50217946

0.13329460

13.33392925

0.07499665

100.03353017

0.00999665

33

34

8.50915950

0.11752042

13.57660892

0.07365610

115.52553076

0.00865610

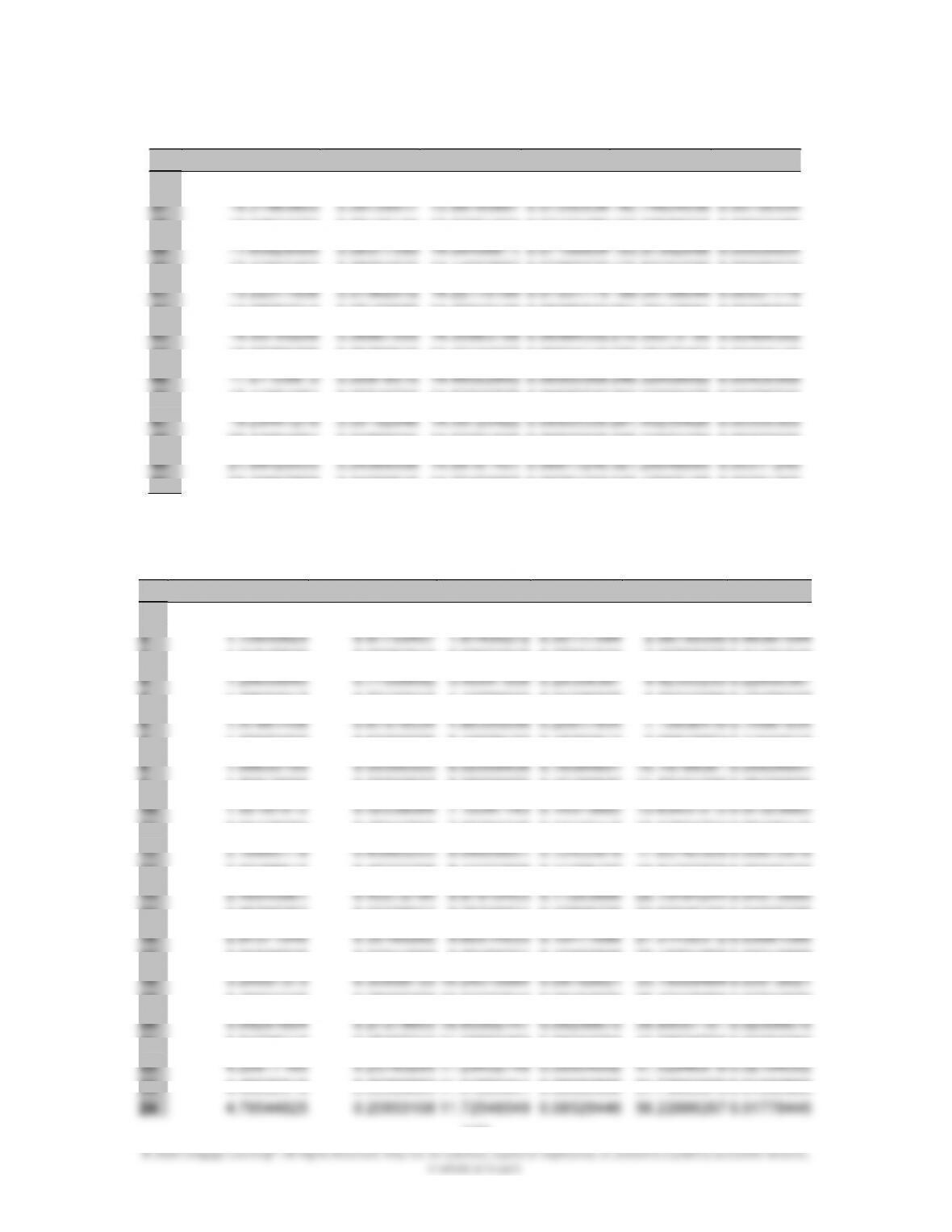

35

370

The Interest-Time Factors for i =

6.5

% (continued)

n (F/P, i, n)

(P/F, i, n)

(P/A, i, n)

(A/P, i, n)

(F/A, i, n)

(A/F, i, n)

36

9.65130143

0.10361297

13.79056970

0.07251332

133.09694513

0.00751332

37

38

10.94674737

0.09135134

13.97921021

0.07153480

153.02688259

0.00653480

39

40

12.41607453

0.08054075

14.14552687

0.07069373

175.63191590

0.00569373

41

42

14.08262214

0.07100950

14.29216149

0.06996842

201.27110981

0.00496842

43

44

15.97286209

0.06260619

14.42144327

0.06934119

230.35172453

0.00434119

45

46

18.11681951

0.05519733

14.53542575

0.06879743

263.33568475

0.00379743

47

48

20.54854961

0.04866524

14.63591946

0.06832505

300.74691704

0.00332505

49

50

23.30667868

0.04290616

14.72452067

0.06791393

343.17967198

0.00291393

The Interest

–

Time Factors for i = 6.75%

n (F/P, i, n)

(P/F, i, n)

(P/A, i, n)

(A/P, i, n)

(F/A, i, n)

(A/F, i, n)

1

1.06750000

0.93676815

0.93676815

1.06750000

1.00000000

1.00000000

2

3

1.21647630

0.82204643

2.63634915

0.37931243

3.20705625

0.31181243

4

5

1.38624317

0.72137416

4.12779022

0.24226037

5.72212099

0.17476037

6

7

1.57970207

0.63303076

5.43658132

0.18393912

8.58817874

0.11643912

8

9

1.80015936

0.55550637

6.58509075

0.15185820

11.85421276

0.08435820

10

11

2.05138285

0.48747605

7.59294748

0.13170116

15.57604224

0.06420116

12

13

2.33766615

0.42777708

8.47737659

0.11796102

19.81727629

0.05046102

14

15

2.66390207

0.37538917

9.25349371

0.10806729

24.65040105

0.04056729

16

17

3.03566625

0.32941698

9.93456331

0.10065868

30.15801858

0.03315868

18

19

3.45931245

0.28907478

10.53222542

0.09494670

36.43425856

0.02744670

20

21

3.94208113

0.25367312

11.05669459

0.09044294

43.58638706

0.02294294

22

23

4.49222319

0.22260693

11.51693441

0.08682866

51.73663979

0.01932866

24

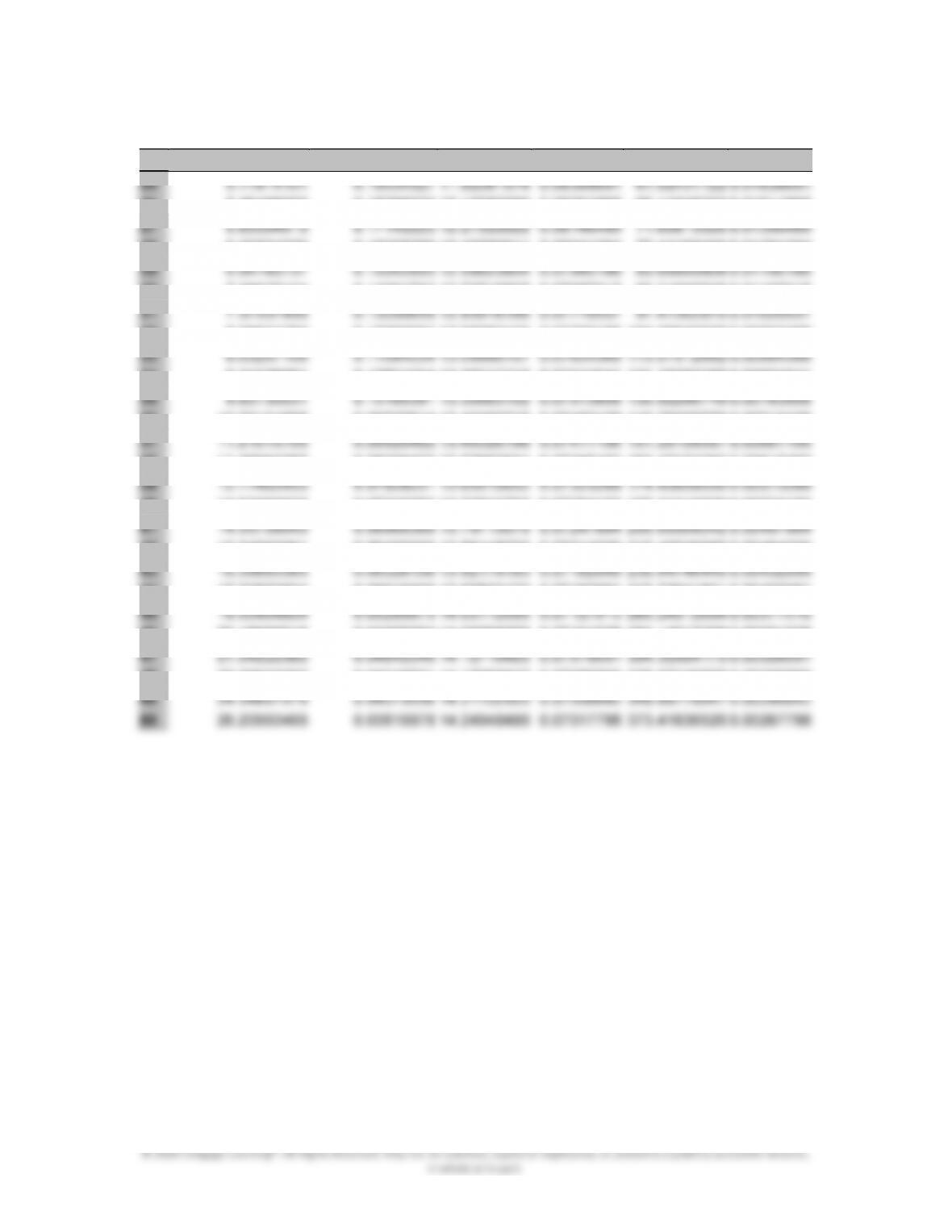

371

The Interest-Time Factors for i = 6.75%

(continued)

n (F/P, i, n)

(P/F, i, n)

(P/A, i, n)

(A/P, i, n)

(F/A, i, n)

(A/F, i, n)

25

26

5.46468303

0.18299323

12.10380399

0.08261865

66.14345223

0.01511865

27

28

6.22731370

0.16058289

12.43580911

0.08041294

77.44168439

0.01291294

29

30

7.09637424

0.14091703

12.72715507

0.07857215

90.31665545

0.01107215

31

32

8.08671762

0.12365957

12.98282123

0.07702486

104.98840920

0.00952486

33

34

9.21526961

0.10851554

13.20717712

0.07571641

121.70769788

0.00821641

35

36

10.50131808

0.09522614

13.40405716

0.07460428

140.76026779

0.00710428

37

38

11.96684265

0.08356423

13.57682621

0.07365492

162.47174292

0.00615492

39

40

13.63689033

0.07333050

13.72843702

0.07284150

187.21319009

0.00534150

41

42

15.54000361

0.06435005

13.86148075

0.07214236

215.40746085

0.00464236

43

44

17.70870824

0.05646939

13.97823122

0.07153981

247.53641831

0.00403981

45

46

20.18006915

0.04955384

14.08068379

0.07101928

284.14917258

0.00351928

47

48

22.99632392

0.04348521

14.17058947

0.07056869

325.87146555

0.00306869

49

50

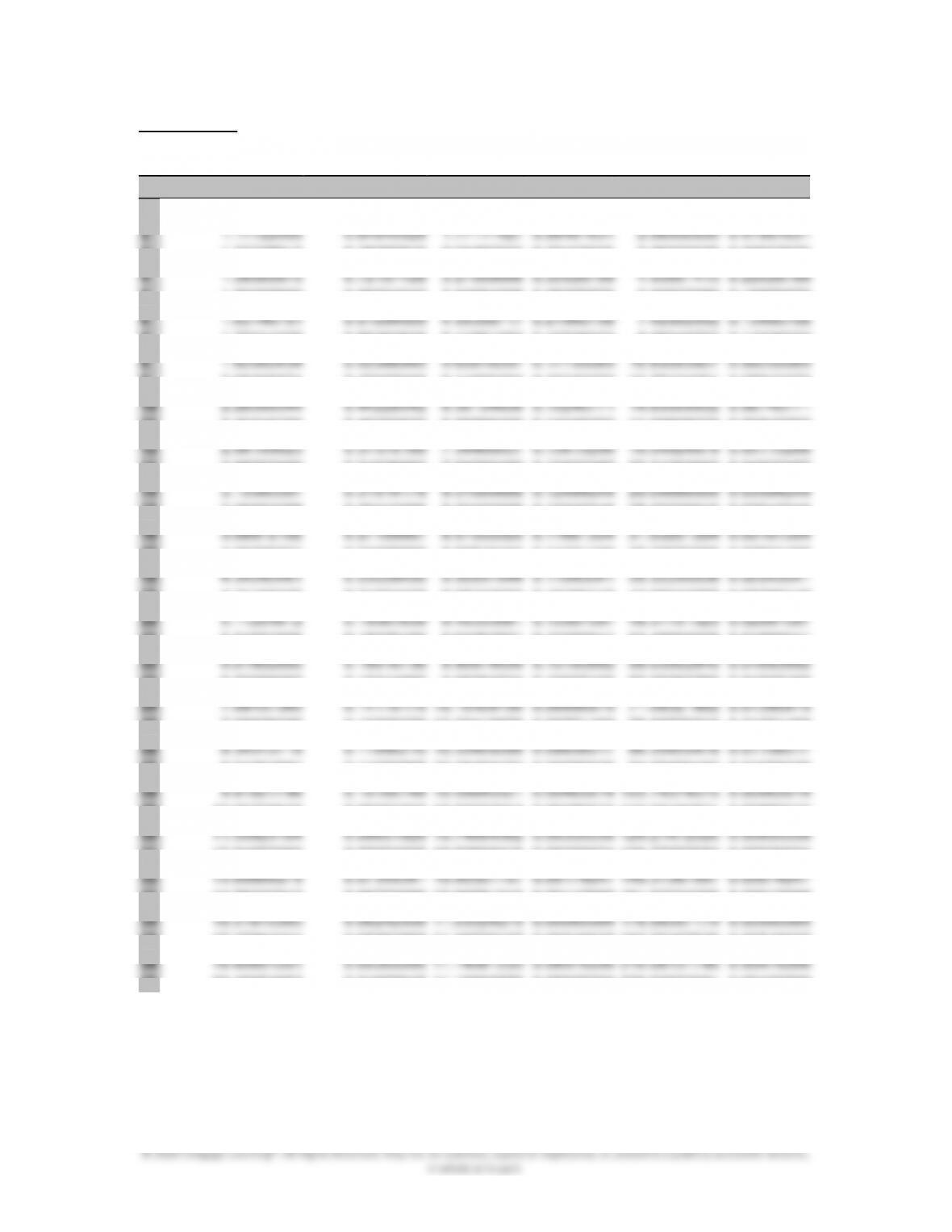

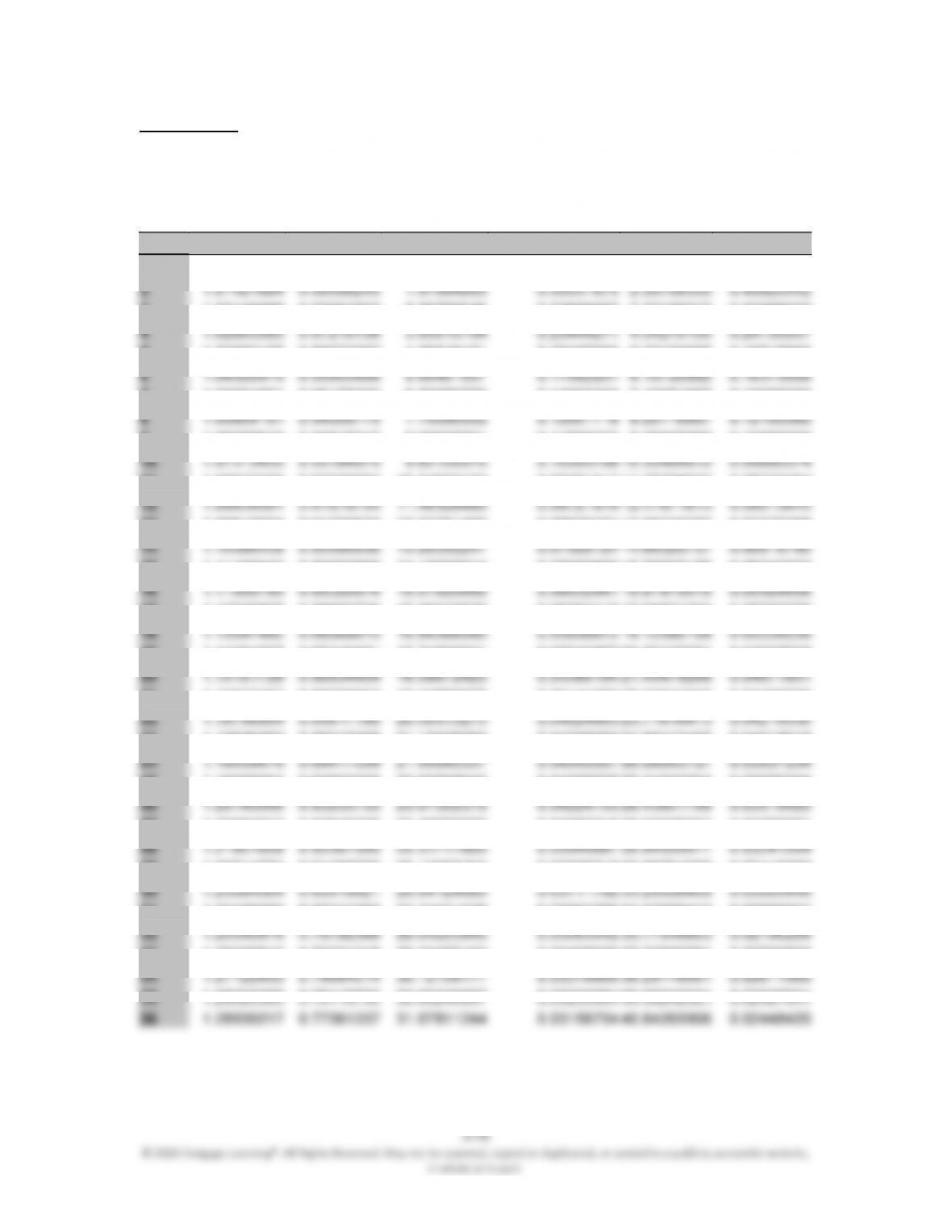

20.7 Using Excel or a spreadsheet of your choice, create interest-time factor tables,

similar to Table 20.9, for i = 7.5%, and i = 7.75%.

372

SOLUTION

The Interest

–

Time Factors for i = 7.5%

n (F/P, i, n)

(P/F, i, n)

(P/A, i, n)

(A/P, i, n)

(F/A, i, n)

(A/F, i, n)

1

2

1.15562500

0.86533261

1.79556517

0.55692771

2.07500000

0.48192771

3

4

1.33546914

0.74880053

3.34932627

0.29856751

4.47292188

0.22356751

5

6

1.54330153

0.64796152

4.69384642

0.21304489

7.24402034

0.13804489

7

8

1.78347783

0.56070223

5.85730355

0.17072702

10.44637101

0.09572702

9

10

2.06103156

0.48519393

6.86408096

0.14568593

14.14708750

0.07068593

11

12

2.38177960

0.41985413

7.73527827

0.12927783

18.42372799

0.05427783

13

14

2.75244405

0.36331347

8.48915373

0.11779737

23.36592066

0.04279737

15

16

3.18079315

0.31438699

9.14150674

0.10939116

29.07724206

0.03439116

17

18

3.67580409

0.27204932

9.70600908

0.10302896

35.67738785

0.02802896

19

20

4.24785110

0.23541315

10.19449136

0.09809219

43.30468134

0.02309219

21

22

4.90892293

0.20371067

10.61719101

0.09418687

52.11897237

0.01918687

23

24

5.67287406

0.17627749

10.98296680

0.09105008

62.30498744

0.01605008

25

26

6.55571508

0.15253866

11.29948452

0.08849961

74.07620112

0.01349961

27

28

7.57594824

0.13199668

11.57337763

0.08640520

87.67930991

0.01140520

29

30

8.75495519

0.11422103

11.81038627

0.08467124

103.39940252

0.00967124

31

32

10.11744509

0.09883918

12.01547757

0.08322599

121.56593454

0.00822599

33

34

11.69197248

0.08552877

12.19294976

0.08201461

142.55963310

0.00701461

35

36

13.51153570

0.07401083

12.34652224

0.08099447

166.82047600

0.00599447

37

38

373

The Interest-Time Factors for i = 7.5%

(continued)

n (F/P, i, n)

(P/F, i, n)

(P/A, i, n)

(A/P, i, n)

(F/A, i, n)

(A/F, i, n)

39

16.78533858

0.05957580

12.53898931

0.07975124

210.47118102

0.00475124

40

41

19.39755689

0.05155288

12.64596155

0.07907663

245.30075857

0.00407663

42

43

22.41630168

0.04461039

12.73852811

0.07850201

285.55068912

0.00350201

44

45

25.90483863

0.03860283

12.81862898

0.07801146

332.06451511

0.00301146

46

47

29.93627915

0.03340428

12.88794287

0.07759190

385.81705528

0.00259190

48

49

34.59511259

0.02890582

12.94792244

0.07723247

447.93483451

0.00223247

50

The Interest

–

Time Factors for i = 7.75%

1

2

1.16100625

0.86132181

1.82307806

0.55884777

2.07750000

0.48134777

3

4

1.34793551

0.74187525

3.45720809

0.30024243

4.48949048

0.22274243

5

6

1.56496155

0.63899333

4.92617562

0.21467748

7.28982651

0.13717748

7

8

1.81693015

0.55037889

6.25086544

0.17236735

10.54103414

0.09486735

9

10

2.10946726

0.47405334

7.44961707

0.14735335

14.31570652

0.06985335

11

12

2.44910467

0.40831248

8.53853668

0.13098130

18.69812474

0.05348130

13

14

2.84342583

0.35168844

9.53177085

0.11954129

23.78613969

0.04204129

15

16

3.30123516

0.30291692

10.44174681

0.11117757

29.69335684

0.03367757

17

18

3.83275465

0.26090895

11.27938321

0.10485853

36.55167288

0.02735853

19

20

4.44985210

0.22472657

12.05427515

0.09996473

44.51422066

0.02246473

21

22

5.16630610

0.19356190

12.77485651

0.09610161

53.75878840

0.01860161

23

24

5.99811367

0.16671908

13.44854244

0.09300585

64.49178932

0.01550585

25

26

6.96384746

0.14359878

14.08185436

0.09049497

76.95287048

0.01299497

374

The Interest-

Time Factors for i = 7.75%

(continued)

n (F/P, i, n)

(P/F, i, n)

(P/A, i, n)

(A/P, i, n)

(F/A, i, n)

(A/F, i, n)

27

7.50354564

0.13327033

14.38519091

0.08941658

83.91671794

0.01191658

28

29

8.71166339

0.11478864

14.96848114

0.08754971

99.50533401

0.01004971

30

31

10.11429564

0.09886996

15.52447829

0.08600313

117.60381469

0.00850313

32

33

11.74276045

0.08515885

16.05735567

0.08471416

138.61626388

0.00721416

34

35

13.63341828

0.07334918

16.57079114

0.08363452

163.01184872

0.00613452

36

37

15.82848383

0.06317724

17.06802807

0.08272643

191.33527519

0.00522643

38

39

18.37696865

0.05441594

17.55192890

0.08195993

224.21895034

0.00445993

40

41

21.33577546

0.04686963

18.02502202

0.08131102

262.39710271

0.00381102

42

43

24.77096866

0.04036984

18.48954304

0.08076028

306.72217623

0.00326028

44

45

28.75924943

0.03477142

18.94747097

0.08029186

358.18386361

0.00279186

46

47

33.38966833

0.02994938

19.40055994

0.07989274

417.93120430

0.00239274

48

49

38.76561362

0.02579606

19.85036706

0.07955213

487.29824027

0.00205213

50

20.8 Using Excel or a spreadsheet of your choice, create interest-time factor tables,

similar to Table 20.9, for i = 8.5%, and i = 9.5%.

375

SOLUTION

The Interest

–

Time Factors for i = 8.5%

n (F/P, i, n)

(P/F, i, n)

(P/A, i, n)

(A/P, i, n)

(F/A, i, n)

(A/F, i, n)

1

1.08500000

0.92165899

0.92165899

1.08500000

1.00000000

1.00000000

2

3

1.27728913

0.78290810

2.55402237

0.39153925

3.26222500

0.30653925

4

5

1.50365669

0.66504542

3.94064208

0.25376575

5.92537283

0.16876575

6

7

1.77014225

0.56492635

5.11851352

0.19536922

9.06049702

0.11036922

8

9

2.08385571

0.47987968

6.11906264

0.16342372

12.75124361

0.07842372

10

11

2.45316703

0.40763633

6.96898439

0.14349293

17.09608276

0.05849293

12

13

2.88792956

0.34626883

7.69095490

0.13002287

22.21093603

0.04502287

14

15

3.39974288

0.29413989

8.30423658

0.12042046

28.23226916

0.03542046

16

17

4.00226231

0.24985869

8.82519194

0.11331198

35.32073306

0.02831198

18

19

4.71156325

0.21224378

9.26772022

0.10790140

43.66544998

0.02290140

20

21

5.54657005

0.18029160

9.64362821

0.10369541

53.48905936

0.01869541

22

23

6.52956092

0.15314965

9.96294524

0.10037193

65.05365790

0.01537193

24

25

7.68676236

0.13009378

10.23419078

0.09771168

78.66779242

0.01271168

26

27

9.04904881

0.11050885

10.46460174

0.09556025

94.69469193

0.01056025

28

29

10.65276649

0.09387233

10.66032554

0.09380577

113.56195871

0.00880577

30

31

12.54070303

0.07974035

10.82658416

0.09236524

135.77297684

0.00736524

32

33

14.76322913

0.06773586

10.96781343

0.09117588

161.92034266

0.00617588

34

35

17.37964241

0.05753858

11.08778137

0.09018937

192.70167539

0.00518937

36

37

20.45974953

0.04887645

11.18968878

0.08936799

228.93822981

0.00436799

376

The Interest-Time Factors for i = 8.5%

(continued)

n (F/P, i, n)

(P/F, i, n)

(P/A, i, n)

(A/P, i, n)

(F/A, i, n)

(A/F, i, n)

38

22.19882824

0.04504742

11.23473620

0.08900966

249.39797935

0.00400966

39

40

26.13301558

0.03826577

11.31452034

0.08838201

295.68253624

0.00338201

41

42

30.76443927

0.03250506

11.38229339

0.08785576

350.16987372

0.00285576

43

44

36.21666702

0.02761160

11.43986357

0.08741363

414.31372959

0.00241363

45

46

42.63516583

0.02345482

11.48876686

0.08704154

489.82548032

0.00204154

47

48

50.19118309

0.01992382

11.53030802

0.08672795

578.71980107

0.00172795

49

50

59.08631551

0.01692439

11.56559538

0.08646334

683.36841782

0.00146334

The Interest

–

Time Factors for i = 9.5%

n (F/P, i, n)

(P/F, i, n)

(P/A, i, n)

(A/P, i, n)

(F/A, i, n)

(A/F, i, n)

1

1.09500000

0.91324201

0.91324201

1.09500000

1.00000000

1.00000000

2

3

1.31293238

0.76165385

2.50890683

0.39857997

3.29402500

0.30357997

4

5

1.57423874

0.63522767

3.83970879

0.26043642

6.04461833

0.16543642

6

7

1.88755161

0.52978684

4.94961222

0.20203603

9.34264849

0.10703603

8

9

2.26322156

0.44184803

5.87528385

0.17020454

13.29706910

0.07520454

10

11

2.71365924

0.36850611

6.64730414

0.15043693

18.03851828

0.05543693

12

13

3.25374527

0.30733813

7.29117753

0.13715206

23.72363438

0.04215206

14

15

3.90132192

0.25632337

7.82817500

0.12774370

30.54023072

0.03274370

16

17

4.67778251

0.21377651

8.27603678

0.12083078

38.71350013

0.02583078

18

19

5.60877818

0.17829195

8.64955842

0.11561284

48.51345450

0.02061284

20

21

6.72506525

0.14869744

8.96107956

0.11159370

60.26384478

0.01659370

22

23

8.06352137

0.12401530

9.22089161

0.10844938

74.35285649

0.01344938

24

25

9.66836371

0.10343012

9.43757770

0.10595939

91.24593375

0.01095939

26

10.58685826

0.09445673

9.53203443

0.10490940

100.91429745

0.00990940

377

The Interest-Time Factors for i = 9.5%

(continued)

n (F/P, i, n)

(P/F, i, n)

(P/A, i, n)

(A/P, i, n)

(F/A, i, n)

(A/F, i, n)

27

28

12.69390772

0.07877795

9.69707423

0.10312389

123.09376551

0.00812389

29

30

15.22031271

0.06570167

9.83471924

0.10168058

149.68750218

0.00668058

31

32

18.24953544

0.05479592

9.94951668

0.10050739

181.57405731

0.00550739

33

34

21.88164924

0.04570039

10.04525901

0.09954945

219.80683406

0.00454945

35

36

26.23664448

0.03811463

10.12510916

0.09876437

265.64888921

0.00376437

37

38

31.45839264

0.03178802

10.19170506

0.09811901

320.61465939

0.00311901

39

40

37.71939924

0.02651156

10.24724677

0.09758719

386.51999197

0.00258719

41

42

45.22650267

0.02211093

10.29356917

0.09714803

465.54213337

0.00214803

43

44

54.22770736

0.01844076

10.33220255

0.09678478

560.29165647

0.00178478

45

46

65.02037682

0.01537979

10.36442322

0.09648390

673.89870340

0.00148390

47

48

77.96105732

0.01282692

10.39129561

0.09623439

810.11639284

0.00123439

49

50

93.47725675

0.01069779

10.41370748

0.09602728

973.44480793

0.00102728

20.9 Using Excel or a spreadsheet of your choice, create interest-time factor tables,

similar to Table 20.9, that can be used for i = 8.5% compounding monthly.

SOLUTION

The monthly interest rate: i = 8.5/12 =0.708333%

The Interest-Time Factors for i

=0.7083333333%

n (F/P, i, n)

(P/F, i, n)

(P/A, i, n)

(A/P, i, n)

(F/A, i, n)

(A/F, i, n)

1

1.00708333

0.99296649

0.99296649

1.00708333

1.00000000

1.00000000

2

3

1.02140088

0.97904753

2.95799646

0.33806667

3.02130017

0.33098333

4

5

1.03592197

0.96532367

4.89548151

0.20427000

5.07133685

0.19718666

6

7

1.05064951

0.95179220

6.80580776

0.14693333

7.15051857

0.13985000

8

9

1.06558642

0.93845040

8.68935591

0.11508333

9.25925968

0.10800000

10

11

1.08073569

0.92529562

10.54650132

0.09481817

11.39798043

0.08773484

12

13

1.09610034

0.91232523

12.37761409

0.08079101

13.56710703

0.07370768

14

15

1.11168342

0.89953666

14.18305914

0.07050665

15.76707176

0.06342332

16

17

1.12748805

0.88692736

15.96319626

0.06264410

17.99831303

0.05556076

18

19

1.14351737

0.87449481

17.71838021

0.05643857

20.26127551

0.04935523

20

21

1.15977457

0.86223653

19.44896078

0.05141663

22.55641016

0.04433330

22

23

1.17626290

0.85015008

21.15528283

0.04726952

24.88417437

0.04018618

24

25

1.19298564

0.83823305

22.83768643

0.04378727

27.24503204

0.03670394

26

27

1.20994613

0.82648308

24.49650683

0.04082215

29.63945364

0.03373881

28

29

1.22714774

0.81489780

26.13207464

0.03826715

32.06791635

0.03118382

30

31

1.24459390

0.80347493

27.74471578

0.03604290

34.53090413

0.02895957

32

33

1.26228810

0.79221218

29.33475163

0.03408926

37.02890781

0.02700593

34

35

36

The Interest-Time Factors for i

=0.7083333333% (continued)

n (F/P, i, n)

(P/F, i, n)

(P/A, i, n)

(A/P, i, n)

(F/A, i, n)

(A/F, i, n)

37

1.29843473

0.77015808

32.44827053

0.03081828

42.13196123

0.02373495

38

39

1.31689436

0.75936235

33.97237404

0.02943568

44.73802792

0.02235235

4

0

1.32622237

0.75402137

34.72639541

0.02879654

46.05492229

0.02171321

41

42

1.34507706

0.74345183

36.21856519

0.02761015

48.71676110

0.02052682

43

44

1.36419980

0.73303045

37.68981839

0.02653236

51.41644284

0.01944903

45

46

1.38359441

0.72275516

39.14044822

0.02554902

54.15450553

0.01846568

47

48

1.40326475

0.71262390

40.57074377

0.02464830

56.93149482

0.01756497

49

50

1.42321475

0.70263465

41.98099008

0.02382031

59.74796412

0.01673697

20.10 Most of you have credit cards, so you already know that if you do not pay the

balance on time, the credit card issuer will charge you a certain interest rate each

month. Assuming that you are charged 1.25% interest each month on your unpaid

balance, what are the nominal and effective interest rates? Also, determine the

effective interest rate that your own credit card issuer charges you.

SOLUTION

20.11 You have accepted a loan in the amount of $15,000 for your new car. You have

agreed to pay the loan back in four years. What is your monthly payment if you

agree to pay an interest rate of 9% compounding monthly? Solve this problem for

i = 5%, i = 6%, i = 7%, and i = 8%, each compounding monthly.

380

© 2020 Cengage Learning®. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website,

in whole or in part.

𝐴=𝑃(𝑖

𝑚)(1+ 𝑖

𝑚)

(1+ 𝑖

𝑚)−1=15000(0.09

12)(1+0.09

12)

(1+0.09

12)−1 =$373.27

For i = 5%

𝐴=𝑃(𝑖

𝑚)(1+ 𝑖

𝑚)

(1+ 𝑖

𝑚)−1=15000(0.05

12)(1+0.05

12)

(1+0.06

12)−1 =$345.44

For i = 6%

𝐴=𝑃(𝑖

𝑚)(1+ 𝑖

𝑚)

(1+ 𝑖

𝑚)−1=15000(0.06

12)(1+0.06

12)

(1+0.06

12)−1 =$352.27

For i = 7%

𝐴=𝑃(𝑖

𝑚)(1+ 𝑖

𝑚)

(1+ 𝑖

𝑚)−1=15000(0.07

12)(1+0.07

12)

(1+0.07

12)−1 =$359.19

For i = 8%

𝐴=𝑃(𝑖

𝑚)(1+ 𝑖

𝑚)

(1+ 𝑖

𝑚)−1=15000(0.08

12)(1+0.08

12)

(1+0.08

12)−1 =$366.19

20.12 How much money will you have available to you after 5 years if you put aside

$100 a month in an account that gives you 6.75% interest compounding monthly?

381

© 2020 Cengage Learning®. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website,

in whole or in part.

15.7113$

12

0675.0

1)

12

0675.0

1(

100

1)1( )5)(12(

))((

m

i

m

i

AF

nm

20.13 How long does it take to double a deposit of $1000

(a) at a compound annual interest rate of 6%

(b) at a compound annual interest rate of 7%

(c) at a compound annual interest rate of 8%

(d) If instead of $1000 you deposit $5000, would the time to double your money

be different in parts (a)-(c)? In other words, is the initial sum of money a factor in

determining how long it takes to double your money?

Now use your answers to verify a rule of thumb that is commonly used by

bankers to determine how long it takes to double a sum of money. The rule of

thumb commonly used by bankers is given by:

rate

interest

72

money of sum a double toperiod Time

SOLUTION

382

6

11.89

71.3

7

10.24

71.7

8

9

72

20.14 Imagine that as an engineering intern you have been assigned the task of selecting

a motor for a pump. After reviewing motor catalogs you narrow your choice to

two motors that are rated at 1.5 kW. Additional information collected is shown in

an accompanying table. The pump is expected to run 4200 hours every year. After

checking with your electric utility company, you determine the average cost of

electricity is about 11 cents per kWh. Based on the information given here, which

one of the motors will you recommend to be purchased?

Criteria Motor X Motor Y

Expected useful life

5 years

5 years

Initial cost

$300

$400

Efficiency at the

operating point

0.75 0.85

Estimated maintenance

cost

$12 per year $10 per year

SOLUTION

383

© 2020 Cengage Learning®. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website,

in whole or in part.

PW = -3695

Based on the given information, Motor-Y should be recommended.

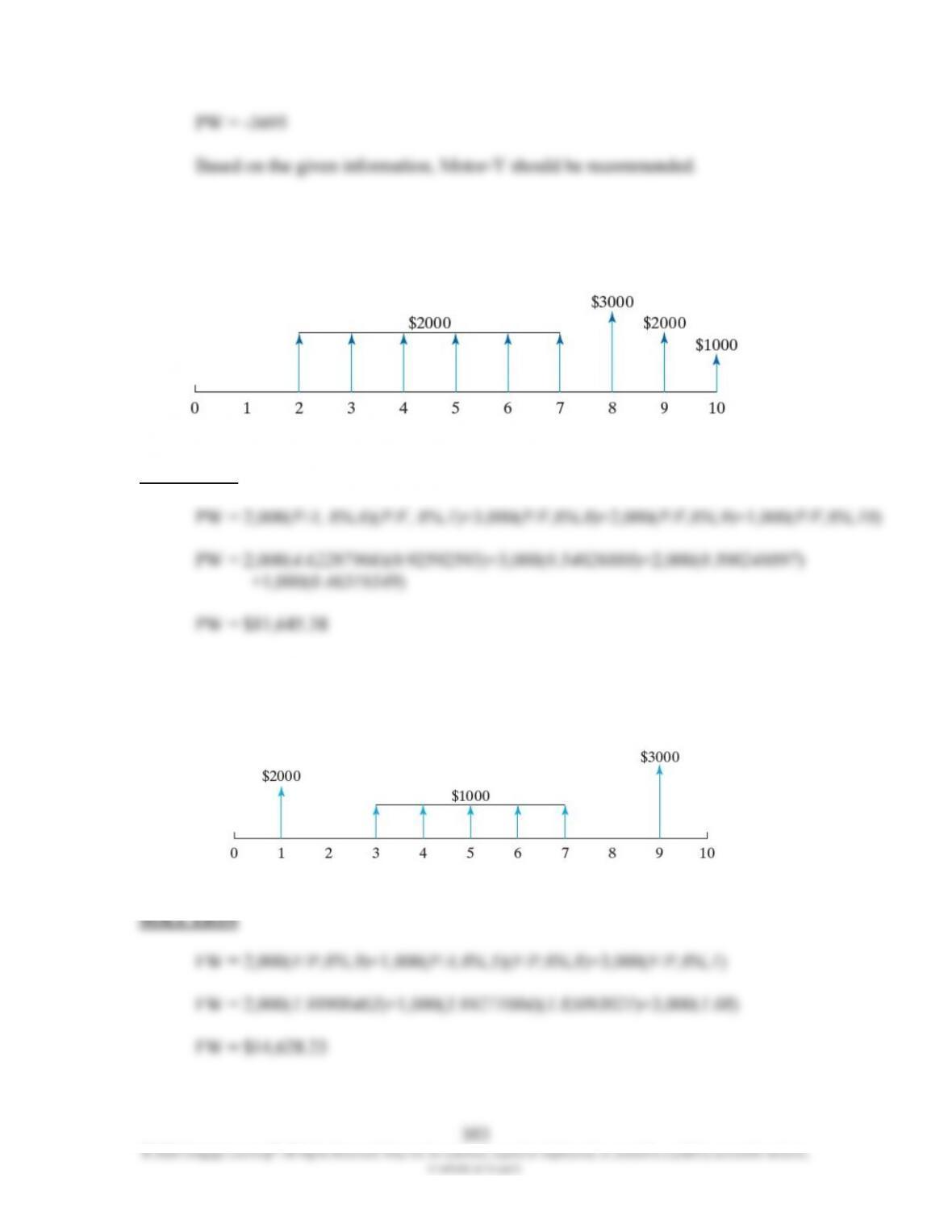

20.15 What is the equivalent present worth of the cash flow given in the accompanying

figure? Assume i = 8%.

SOLUTION

20.16 What is the equivalent future worth of the cash flow given in the accompanying

figure? Assume i = 8%.