9-1

Chapter 9

Chapter 9 (Short Answers)

9.1. Simple interest is calculated such that the interest is based on the original principal.

9.2 The nominal interest rate is a number based on interest payments once per year; however,

if interest is compounded multiple times per year, the interest rate for the period is the

9.3

9.4 An annuity is a uniform (constant) series of transactions at the same interval. Examples

include a loan payment, a fixed monthly deduction from a paycheck into savings, etc.

9.6 Interest is the return on an investment or the charge for borrowing money. Inflation is the

increase in cost over time of goods, commodities, and services, which is equivalent to the

9.7 This term is depreciation

S O N D J F M A May

Jn Jl A

9-2

9.8 Depreciation is an accounting procedure that allows a company to reduce their taxable

9.9 The time value of money suggests that “a dollar today is worth more than a dollar

9.10 A company can only use depreciation to offset revenue. Depreciation can never exceed

profit. Therefore, a small company, with only one project, may have to defer depreciation

9.11 After-tax profit is the net profit from the project taking into account all expenses including

9.12 P = $1,000

F = $1,000(1 + ieff)

(a) 260,1$) weeks52(5$000,1$F

9.13

(a)

mn

m

i

P

F1

000,1$P

(b) F = P(1 + ieff)

1000,1$21.109,1$

eff

i

9-4

9.14 n

iPF 1

2

P

F

9.15 11

mn

eff m

i

i

i ie

ff

0.04 0.0408

9.16 in

cont

mn

PeF

m

i

P

F;1

24.637,54$09.01000,15$

15

F

9.17

mn

m

i

P

F1

If P= $1

9.18

(a)

0 1 18

19 20 21 22

A

75 75 75 75

9-6

9.19

(a)

50

10

555

0 1 8 25

9.20

(a)

(b) i

i

A

F

i

P

Fn

n11

;1

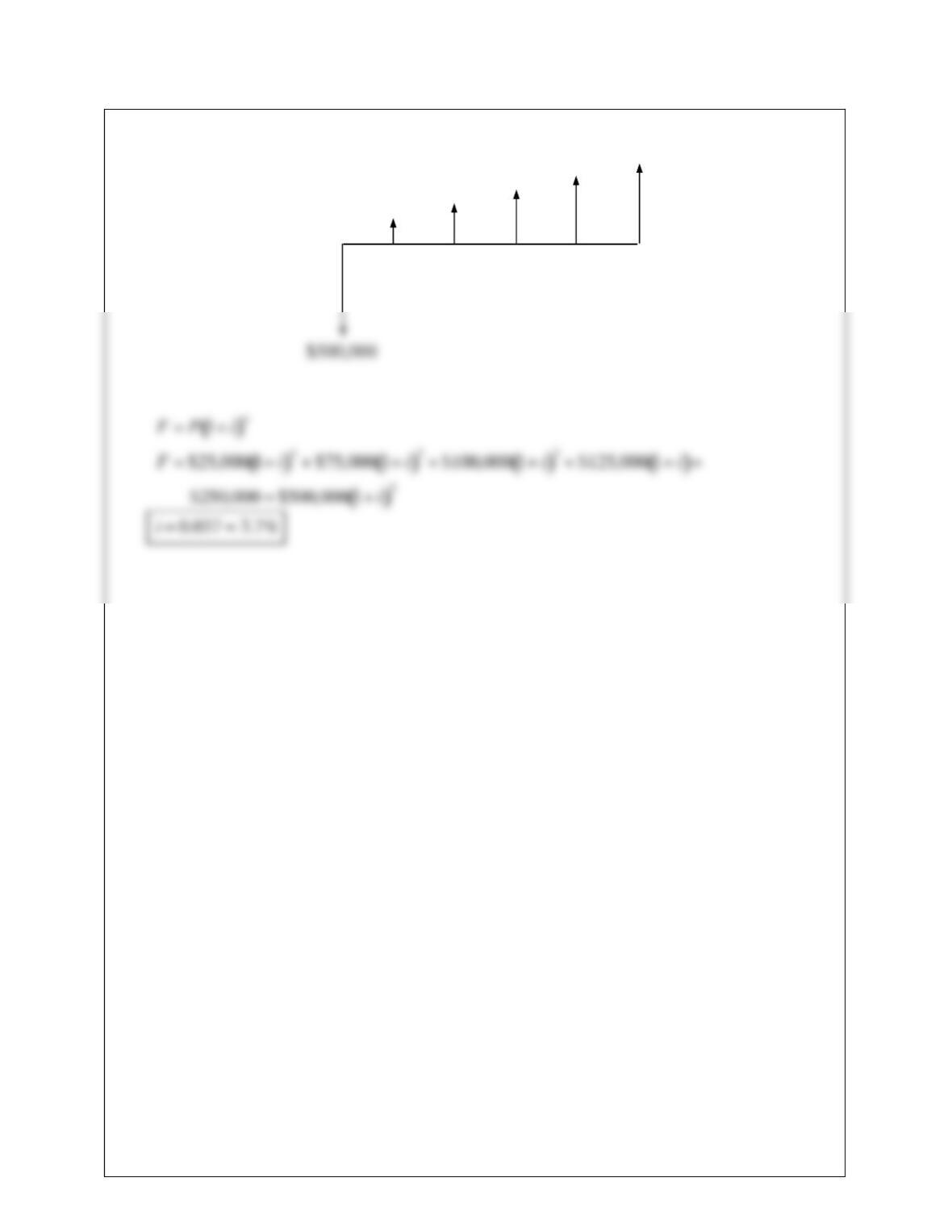

June Jul Aug Sept Oct Nov Dec Jan Feb March April May

AAA

1500 1500 1500

8000

1000 1000 1000 1000 1000 1000 1000

8000

9.21

(a)

nm

m

i

PF 1

9.22 i

i

A

Fn11

(a) i

i11

000,6$000,000,1$

40

%29.60629.0i

9-9

9.23

(a) 16,09.0,000,6$16,09.0,25,09.0,000,5$ A

F

P

F

A

F

F

9.24 11

1

n

n

i

ii

P

A

1

12

07.0

1

12

07.0

1

12

07.0

000,25$ 312

312

A

9.25 11

1

n

n

i

ii

P

A

9.26 11

1

n

n

i

ii

P

A

(a)

1

065.0

1

12

065.0

1

12

065.0

000,200$ 3012

3012

A

9-11

9.27 11

1

n

n

i

ii

P

A

1

1

12

1

12

000,225$600,1$ 2512

2512

i

ii

9.28 11

1

n

n

i

ii

P

A

9.29 11

1

n

n

i

ii

P

A

9-12

9.30

$25,000$75,000$100,000

$125,000$250,000

9-13

9.31

(a)

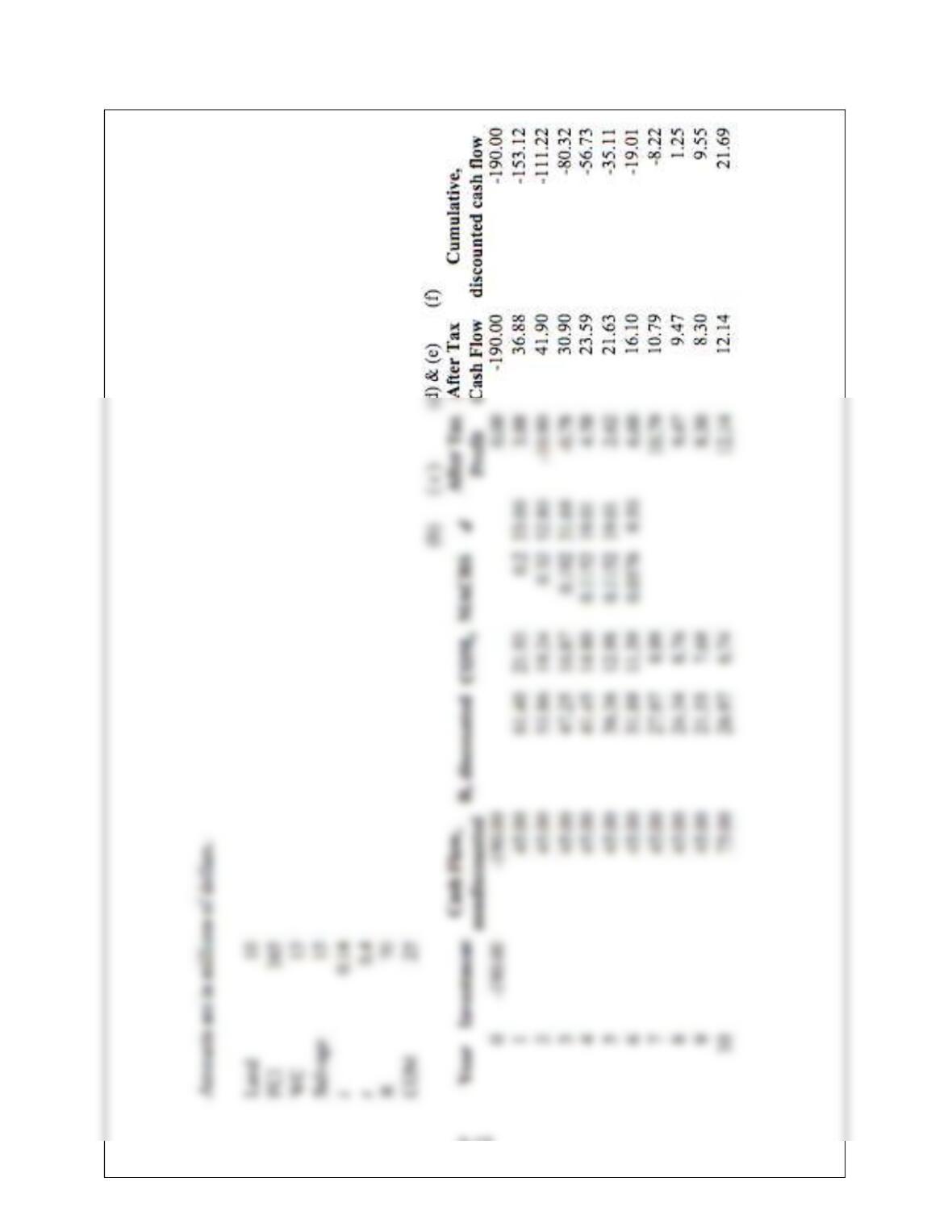

(b) Cumulative, discounted cash flow diagram

Year Cash Flow Discounted

Cash Flow

Cumulative, Discounted

Cash Flow

0 -$250,000.00 -$250,000.00

-$250,000.00

(c) F P 1in

F$44,332.07 1 0.09 8

$60,000 $60,000 $50,000…………………………………..$50,000

9-14

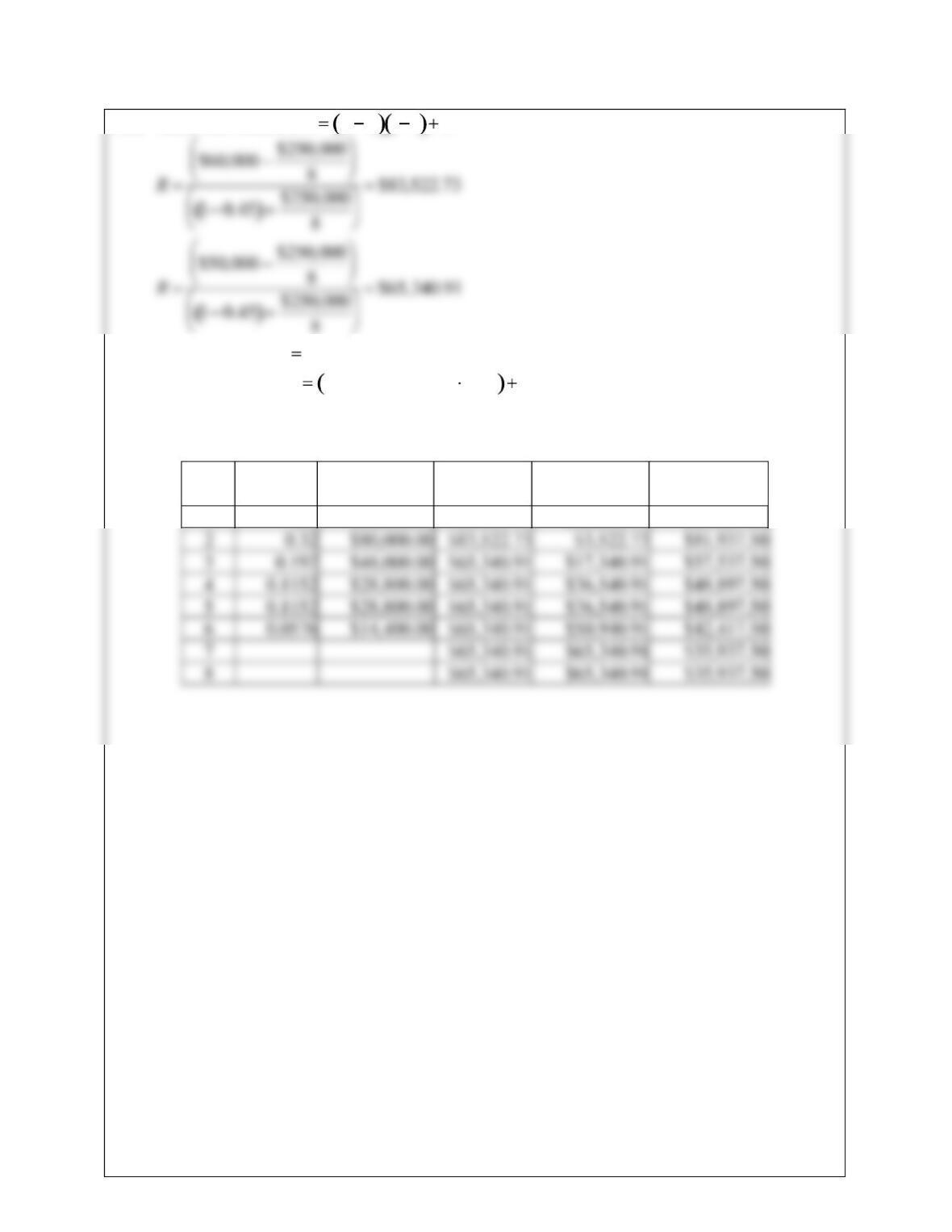

9.32 After Tax Cash Flow R d 1t d

Before Tax Profit Revenue – Depreciation

After Tax Revenue Before Tax Profit 0.55 Depreciation

Note: All values in millions of dollars.

Year MACRS Depreciation

Revenue

Before Tax

Profit

After Tax

Revenue

1 0.2 $50,000.00 $83,522.73 $33,522.73 $68,437.50

9-15

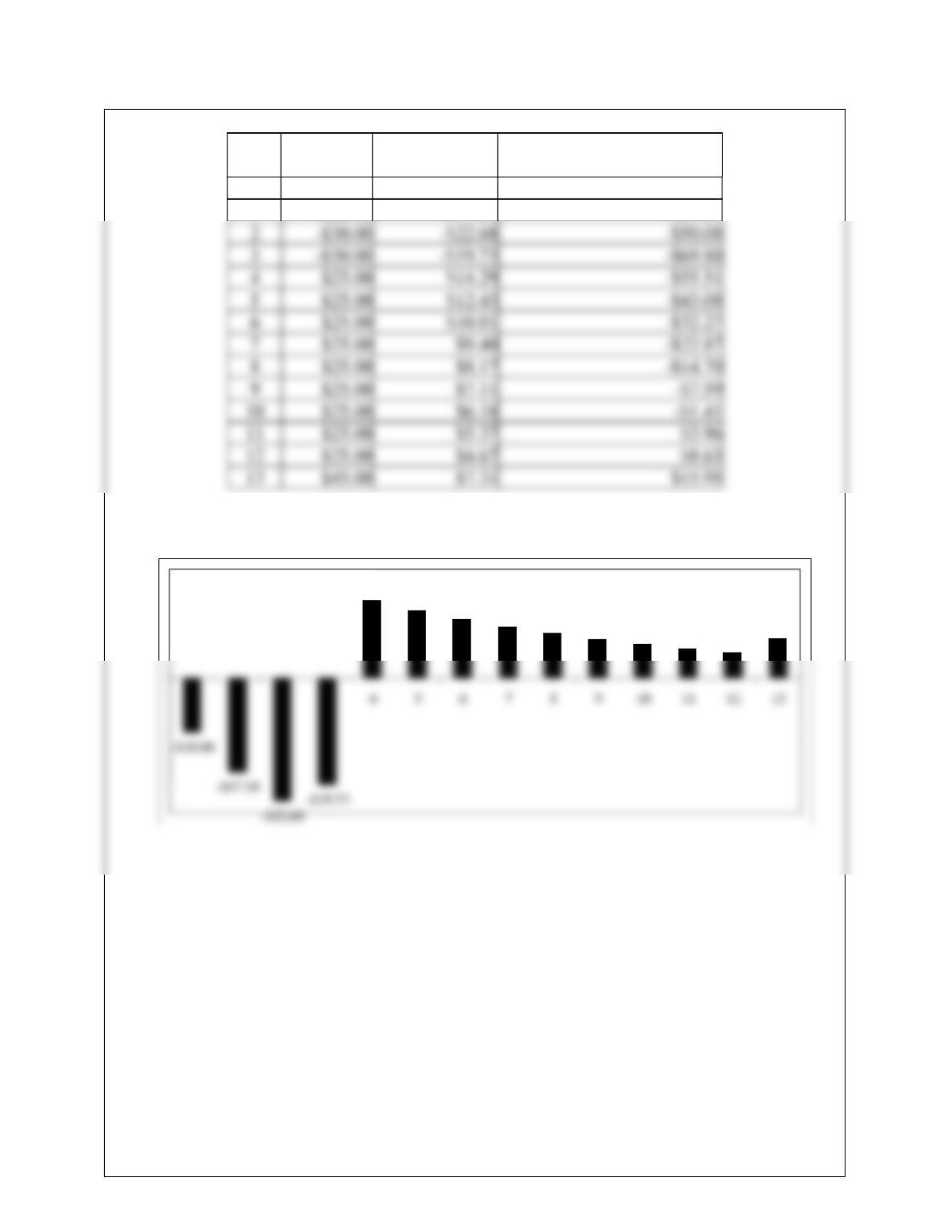

9.33

Year Cash Flow

Discounted

Cash Flow

Cumulative, Discounted

Cash Flow

0 -$10.00 -$10.00

-$10.00

1 -$20.00 -$17.39

-$27.39

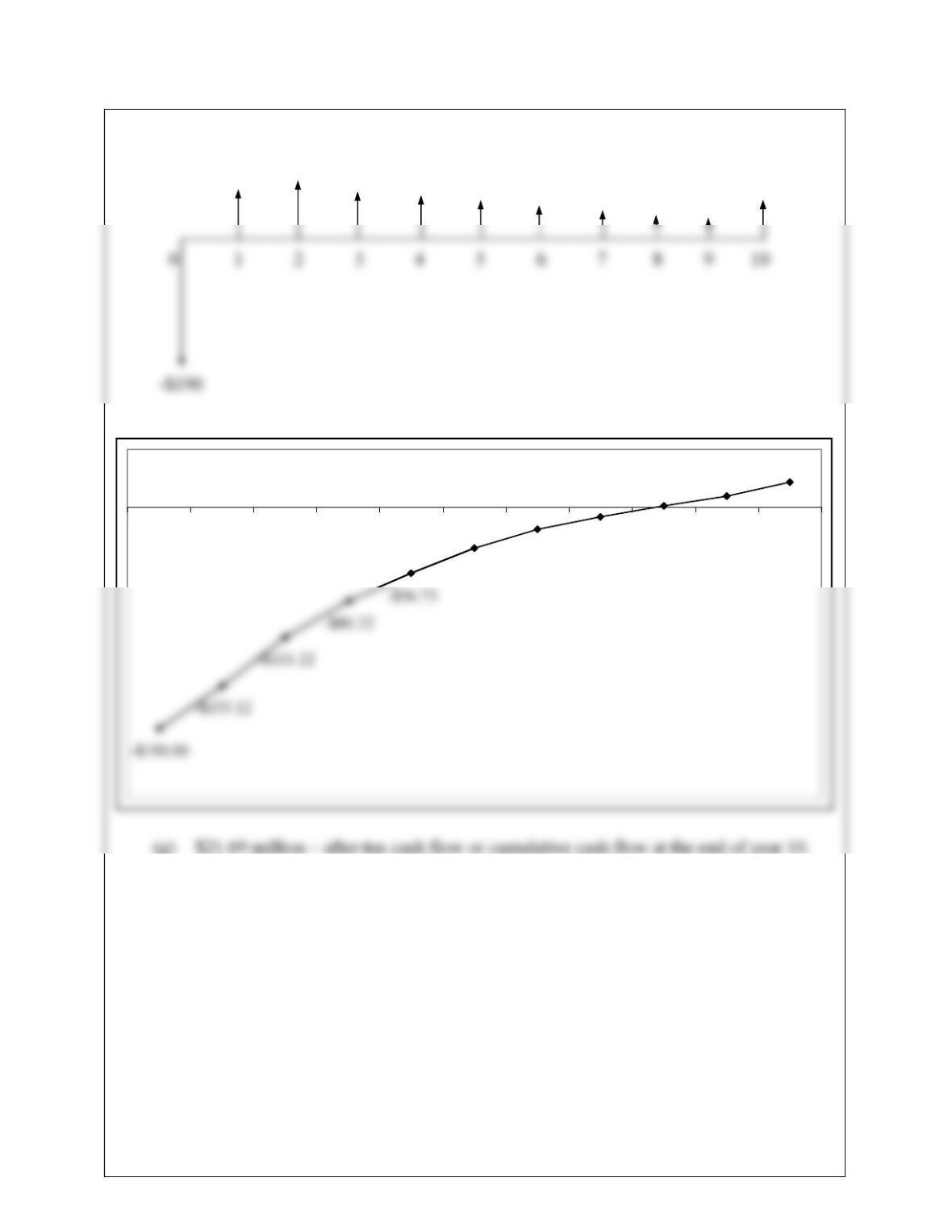

(a)

$14.29 $12.43 $10.81 $9.40 $8.17 $7.11 $6.18 $5.37 $4.67

$7.31

(b)

-$14.70

-$7.59

-$1.41

$3.96 $8.63

$15.95

0 1 2 3 4 5 6 7 8 9 10 11 12 13

(c) NPV $10 $20

1 0.15

$30

1 0.15 2

$30

1 0.15 3

$25 1 0.15 10 1

0.15 1 0.15 10 1 0.15 3

$20

10.15 13

NP

V

$15.9 million

9-17

Four Year

Year DDB SL MACRS

Six Year

Year DDB SL MACRS

1 16.67

16.67

2 27.78

15.15 27.78

Nine Year

Year DDB SL MACRS

1 11.11

11.11

2 19.75

10.46 19.75

9.35

(a)

$75

9-19

9-20

(e)

(f)

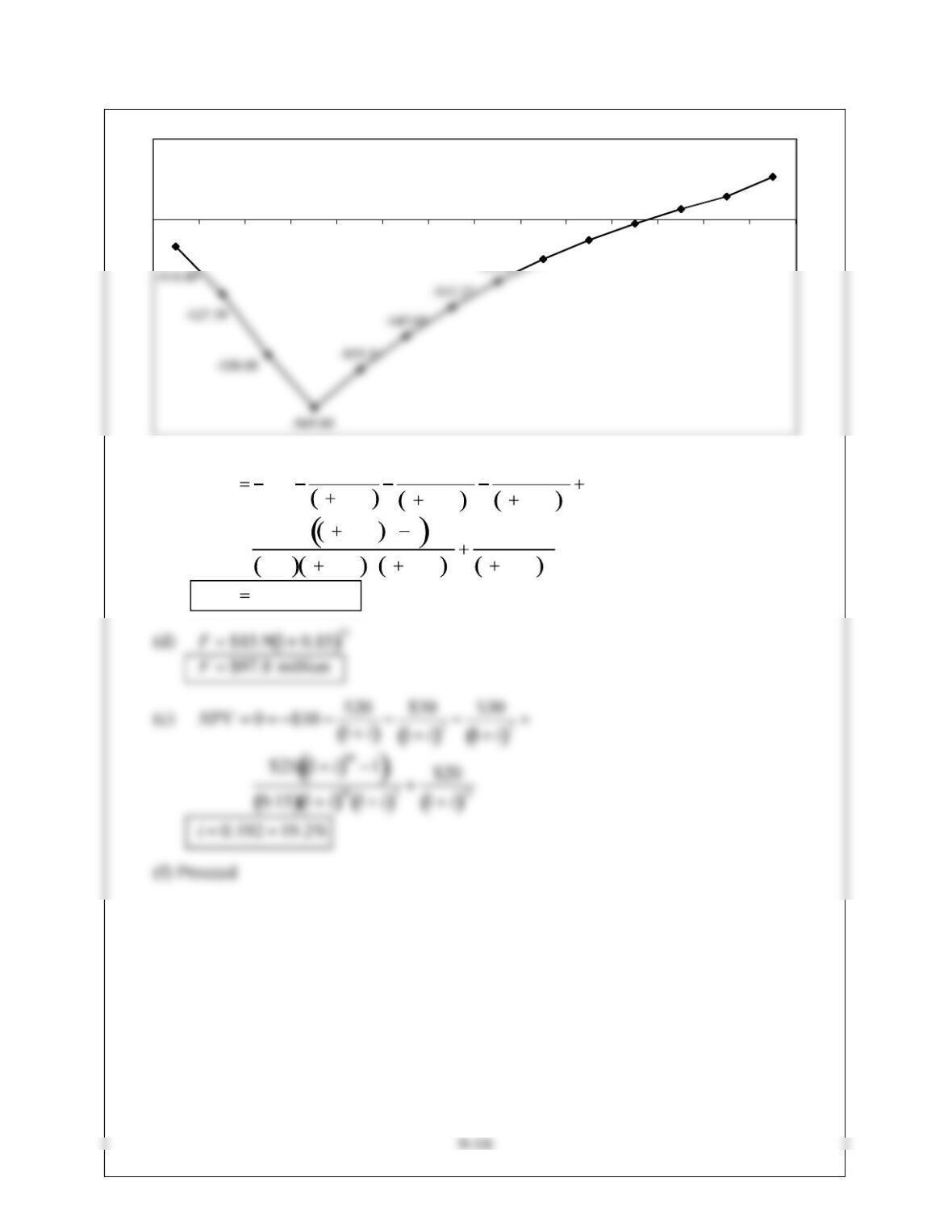

-$35.11

-$19.01 -$8.22

$1.25 $9.55 $21.69

0 1 2 3 4 5 6 7 8 9 10

$36.88 $41.90 $30.90 $23.59 $21.63 $16.10 $10.79 $9.47 $8.30

$12.14