10-19

10.25 Look at incremental cases.

ROROII = Incremental Yearly Savings / Incremental Investment

ROROIIBase +1 – Base = (0.77-0.75)/(5.1-5) = 0.20

See table for complete ROROII calculations.

Case FCI

($ million)

Cash Flow

($ million) ROROII

10.26 EAOC = -FCI(A/P,i,n) +YS

10.27 (a) Base Case

NPV = –FCI +CFi(P / A,i,n)

(b) INPV = –FCI +YS(P / A,i,n)

Alternative 2

(c) INPV = 0 = -3.26+4.08YS

YS = 0.80

10-21

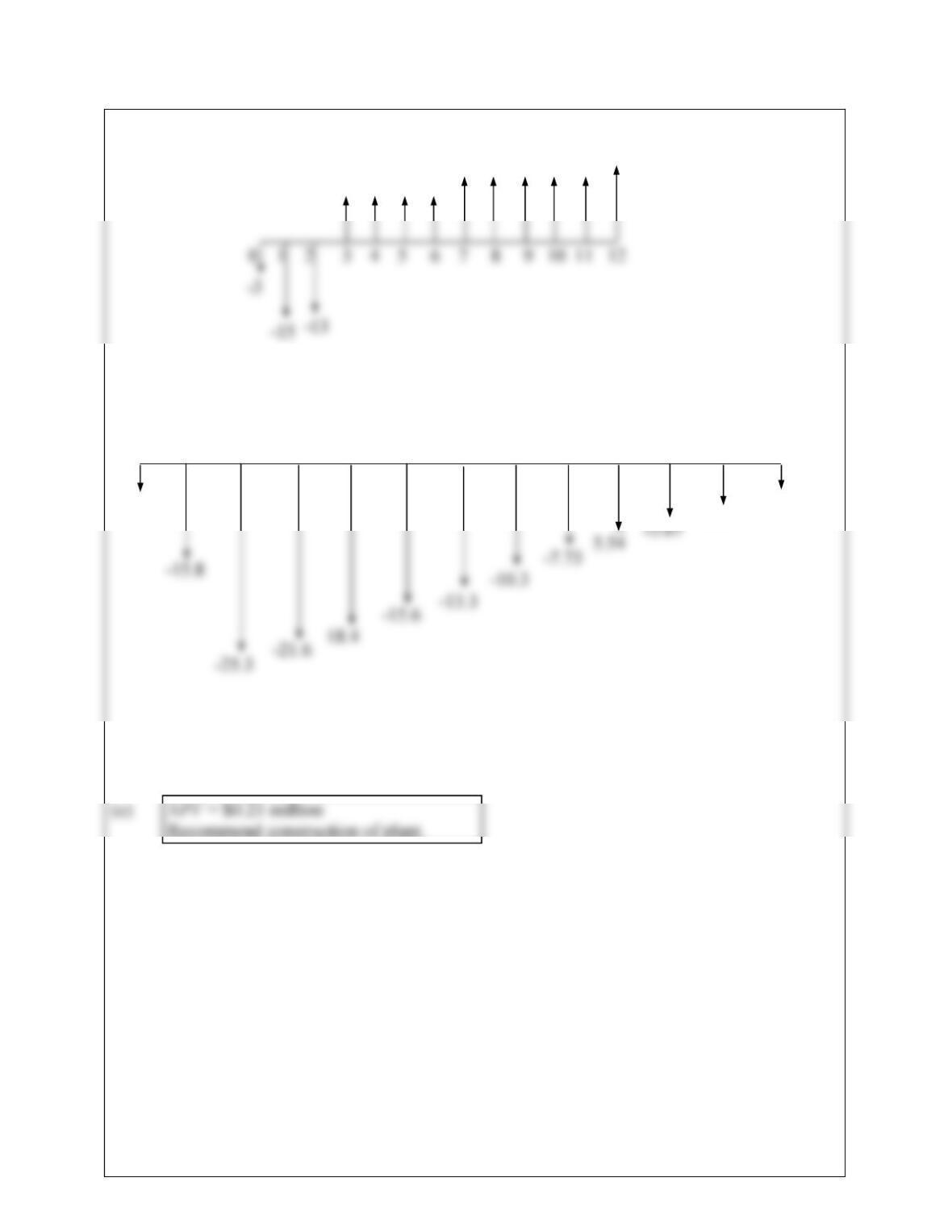

10.28 (a) All values are in $ millions.

(b) All values are in $ millions.

6 6 6 6

9 9 9 9 9 15

0 1 2 3 4 5 6 7 8 9 10 11 12

-3

10.29 INPV = –FCI +YS(P / A,i,n)

10.30 INPV = –FCI +YS(P / A,i,n)

10.31 INPV = –FCI +YS(P / A,i,n)

10-23

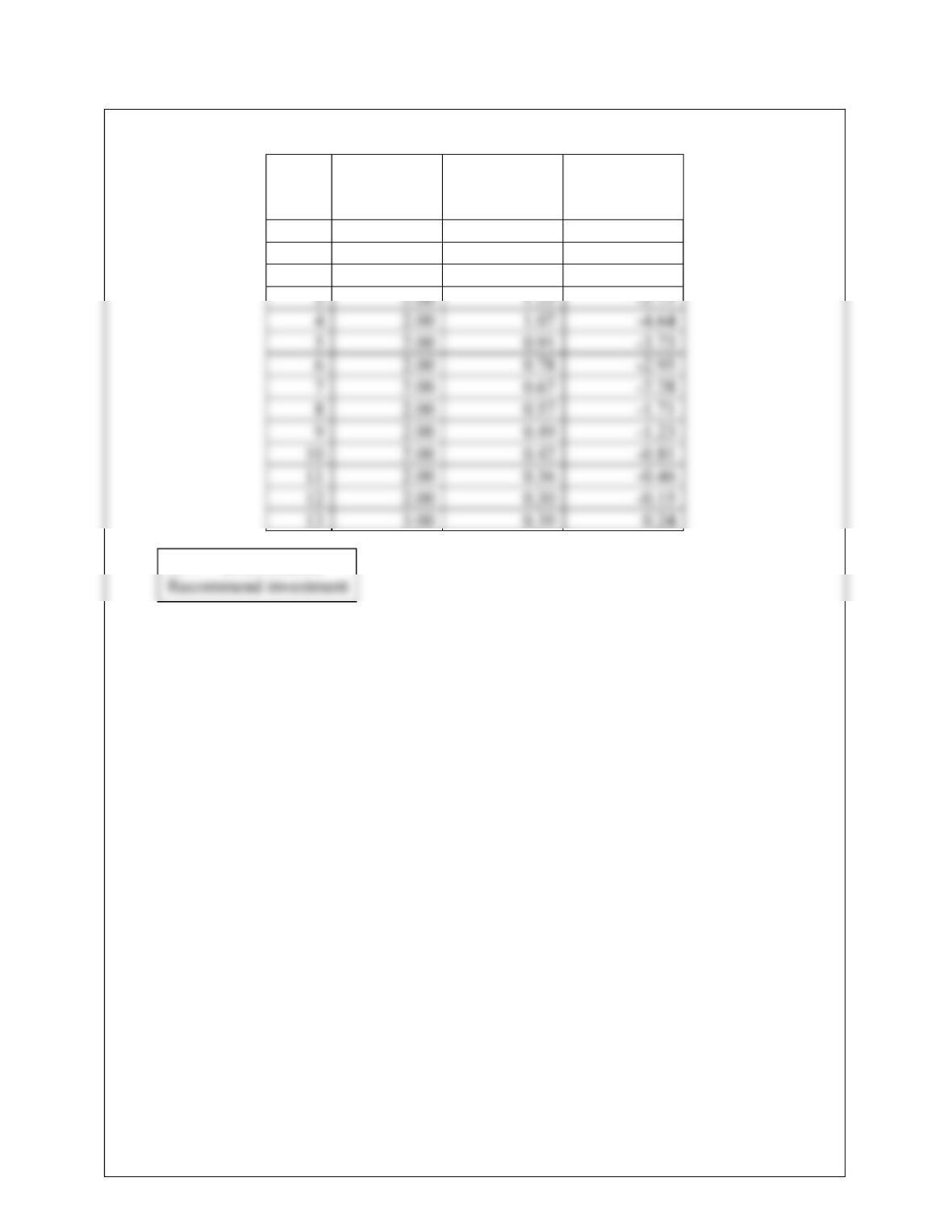

10.32

Year Cash Flow

($ million)

Discounted

Case Flow

($ million)

Cumulative

Cash Flow

($ million)

0 -5.00 -5.00 -5.00

1 -4.00 -3.42 -8.42

2 2.00 1.46 -6.96

NPV = $0.24 million

10-24

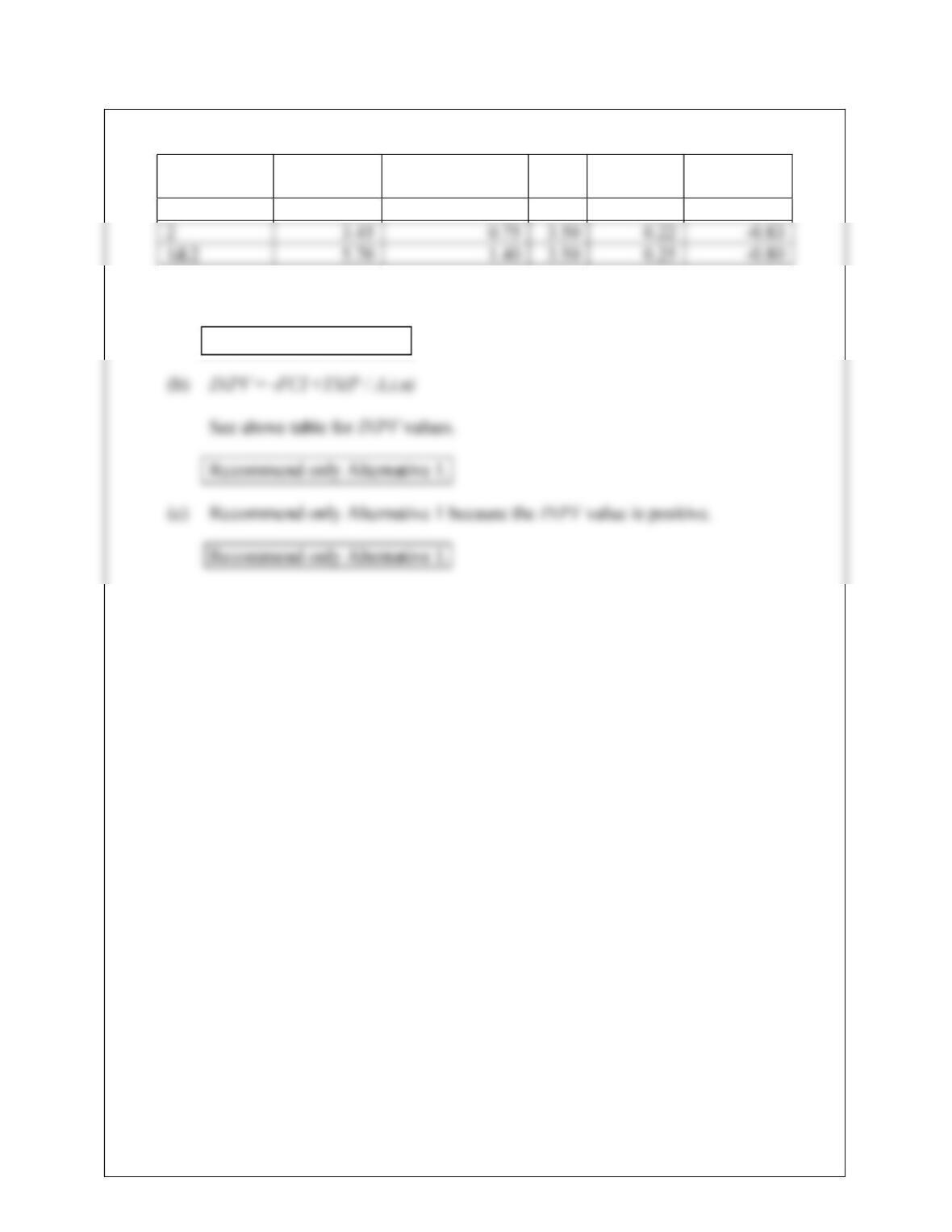

10.33 (a) ROROII = Incremental Yearly Savings / Incremental Investment

Alternative FCI

($ million)

Yearly Savings

($ million) P/A ROROII INPV

($ million)

1 2.25 0.65 3.50 0.29 0.02

All ROROII values are greater than 18%; therefore, all alternatives are good.

All alternatives will work.

10-25

10.34 (a) All values are in $ millions.

(b) All values are in $ millions.

(c)

Year Cash Flow

($ million)

Discounted

Cash Flow

($ million)

Cumulative Disc.

Cash Flow

($ million)

0 -10 -10.00 -10.00

1 -11 -9.82 -19.82

(d) For the NPV = $2 million, profit = $4.27 million

(e) INPV = –FCI +YS(P / A,i,n)

-10 -11

0 1 2 3 4 5 6 7 8 9 10 11

0.65

10.35 EAOC = FCI(A/P,i,n) + YOC

65.7$5.5

114.01

14.0114.0

53

3

A

EAOC thousand/yr

10.36 EAOC = FCI(A/P,i,n) – YS

39.53$332515

115.01

15.0115.0

88 8

8

A

EAOC thousand/yr

10-27

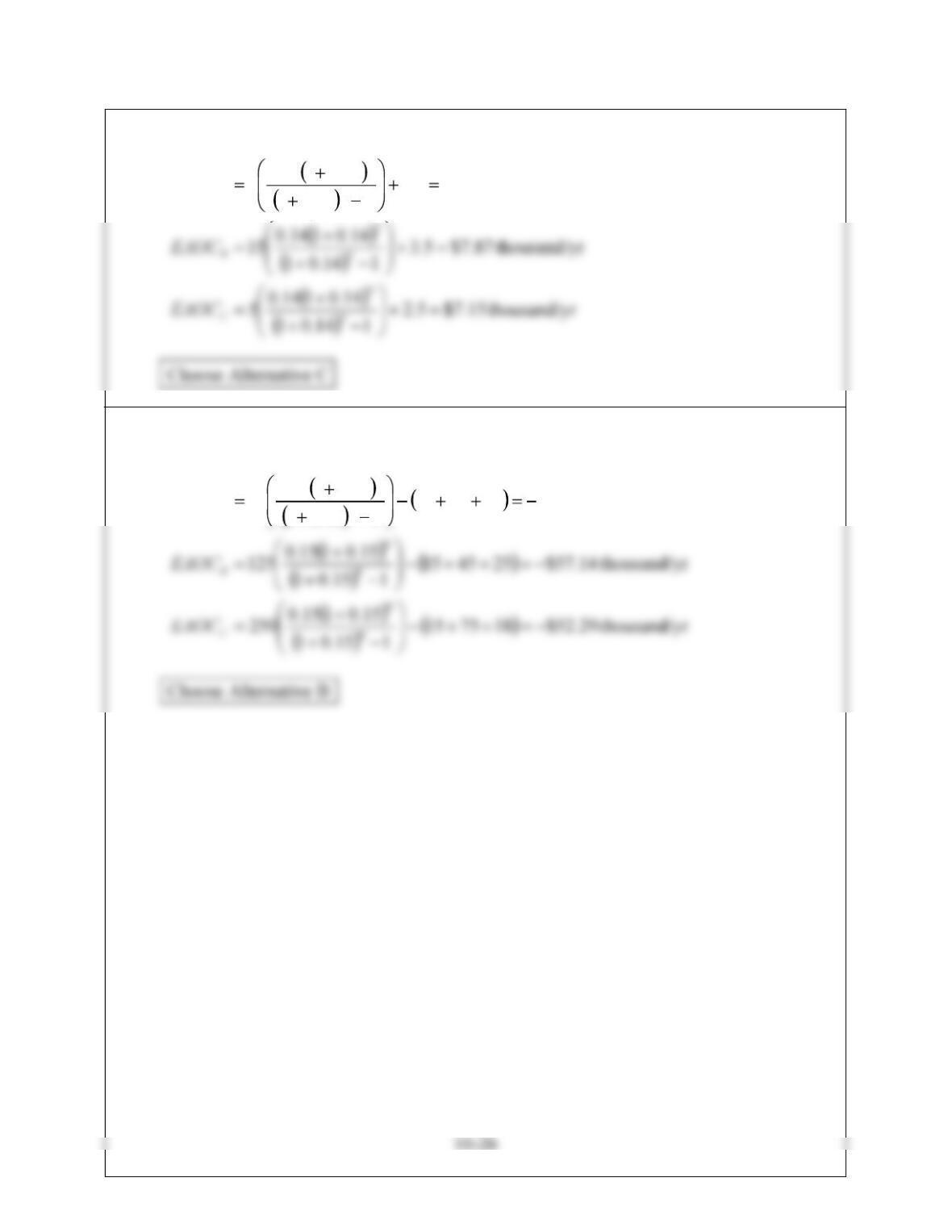

10.37 (a) ROROII = Incremental Yearly Savings / Incremental Investment

From above, choose Case B. However, can also do incremental comparison

between cases.

Use Case A as base case because it has the lowest FCI and evaluate ROROII going

from Case A to Case B.

Choose Case B

(b) EAOC = FCI(A/P,i,n) – YS

Choose Case B

10-28

(c) EAOC = FCI(A/P,i,n) – YS

Choose Case C

(d) EAOC = FCI(A/P,i,n) – YS

None of the cases provide an acceptable EAOC.

10-29

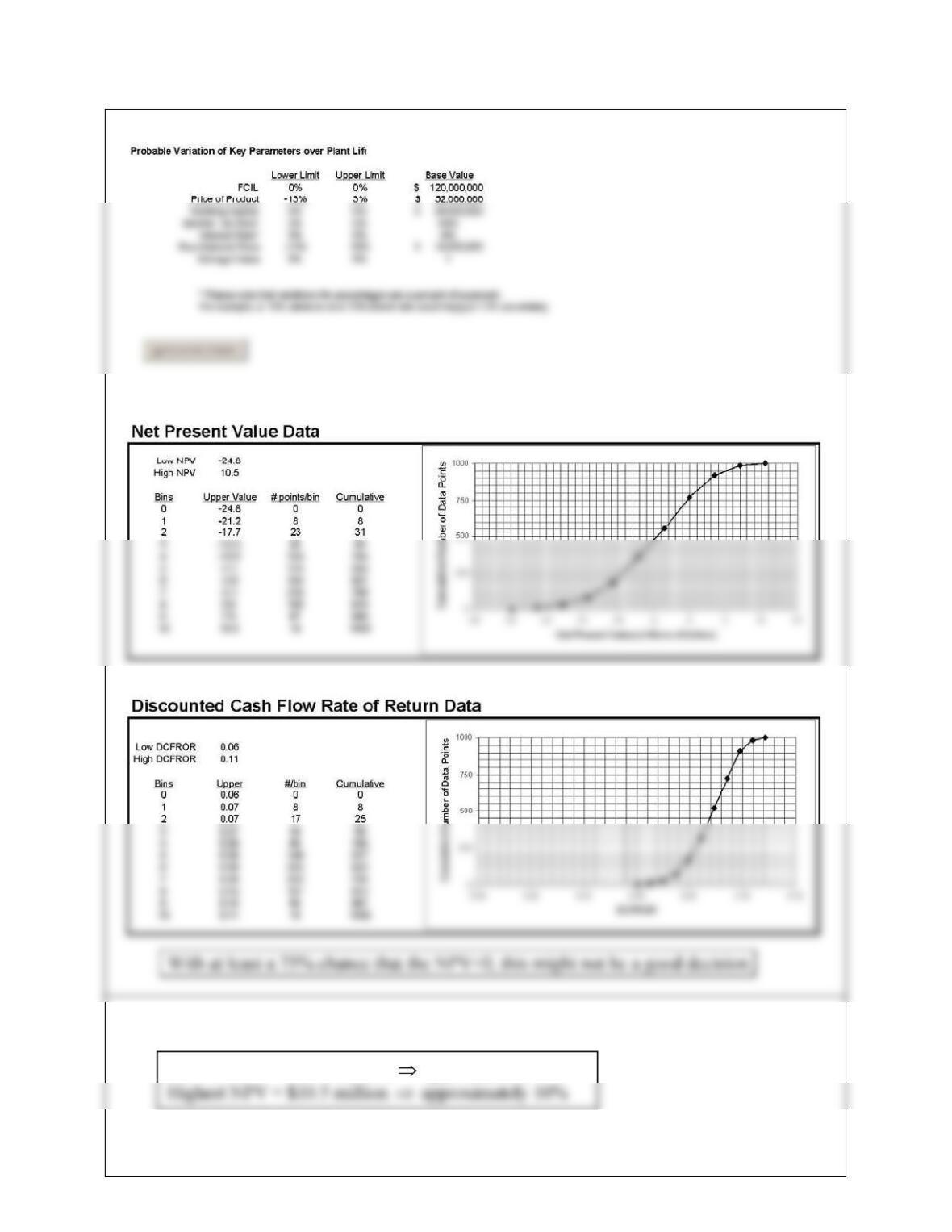

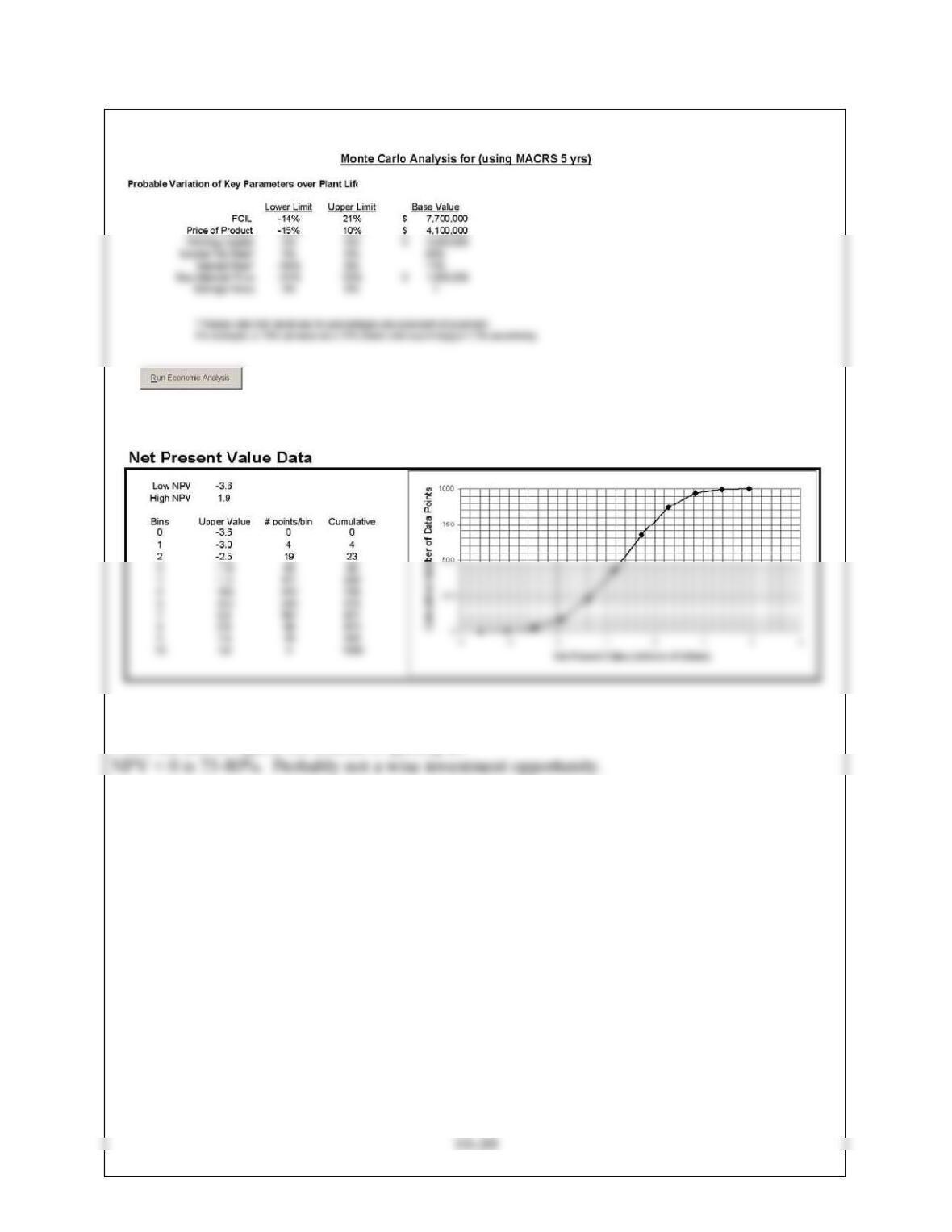

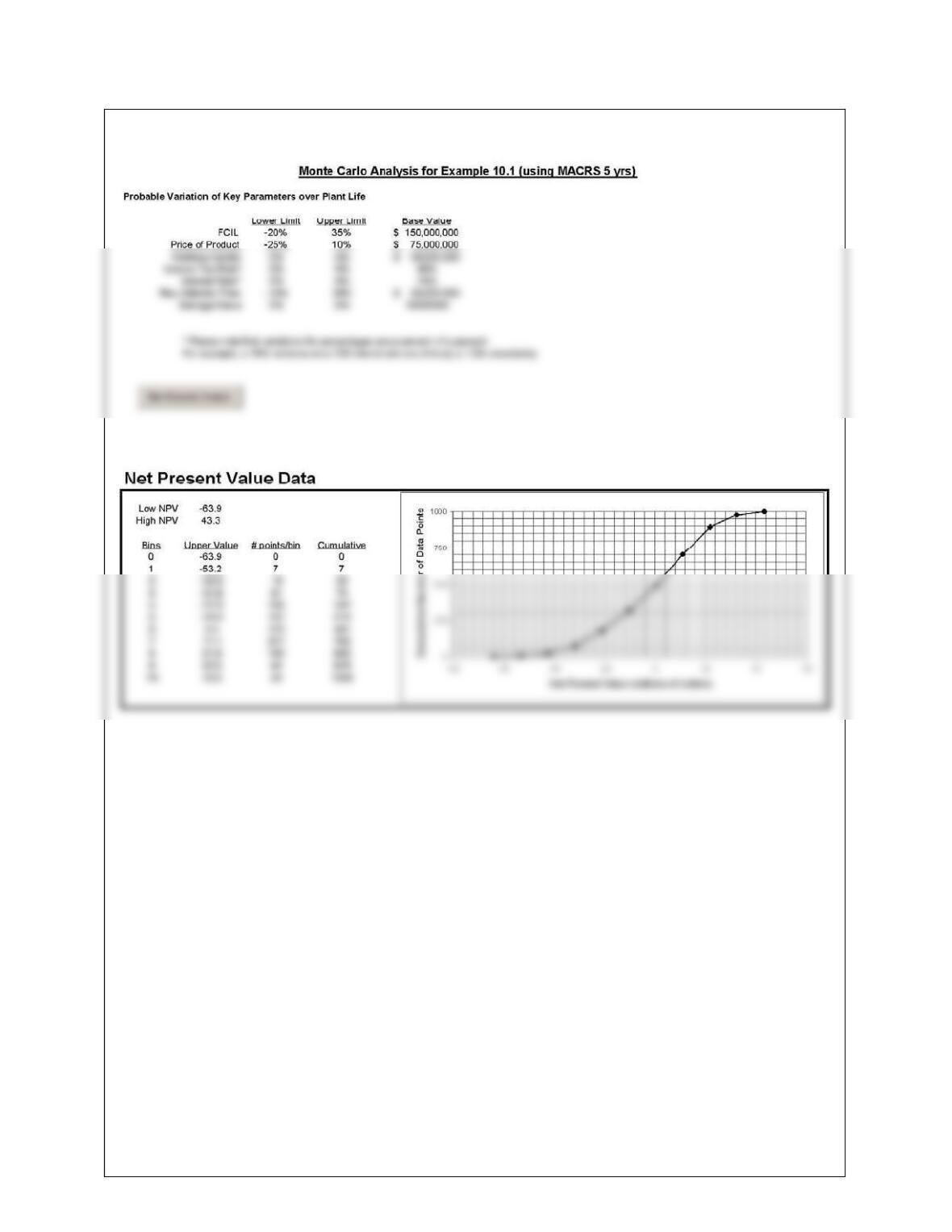

10.38 Individual solutions may differ slightly because of the Monte Carlo method being used.

10.39

Lowest NPV = -$24.8 million approximately 1%

10.40

From the above figure, the chance of getting an

10-31

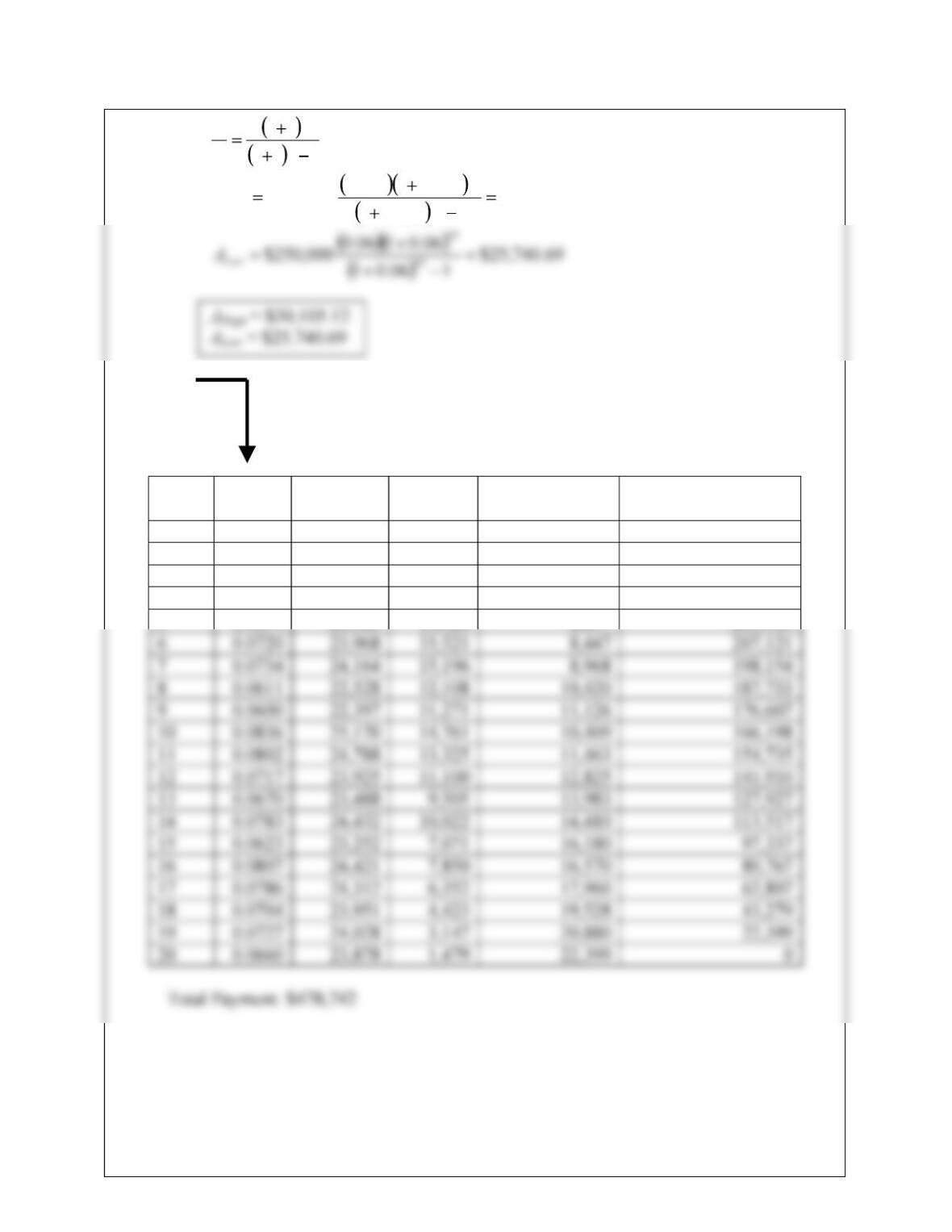

10.41 (a) 11

1

n

n

i

ii

P

A

12.105,30$

1085.01

085.01085.0

000,250$ 15

15

High

A

(b)

(c)

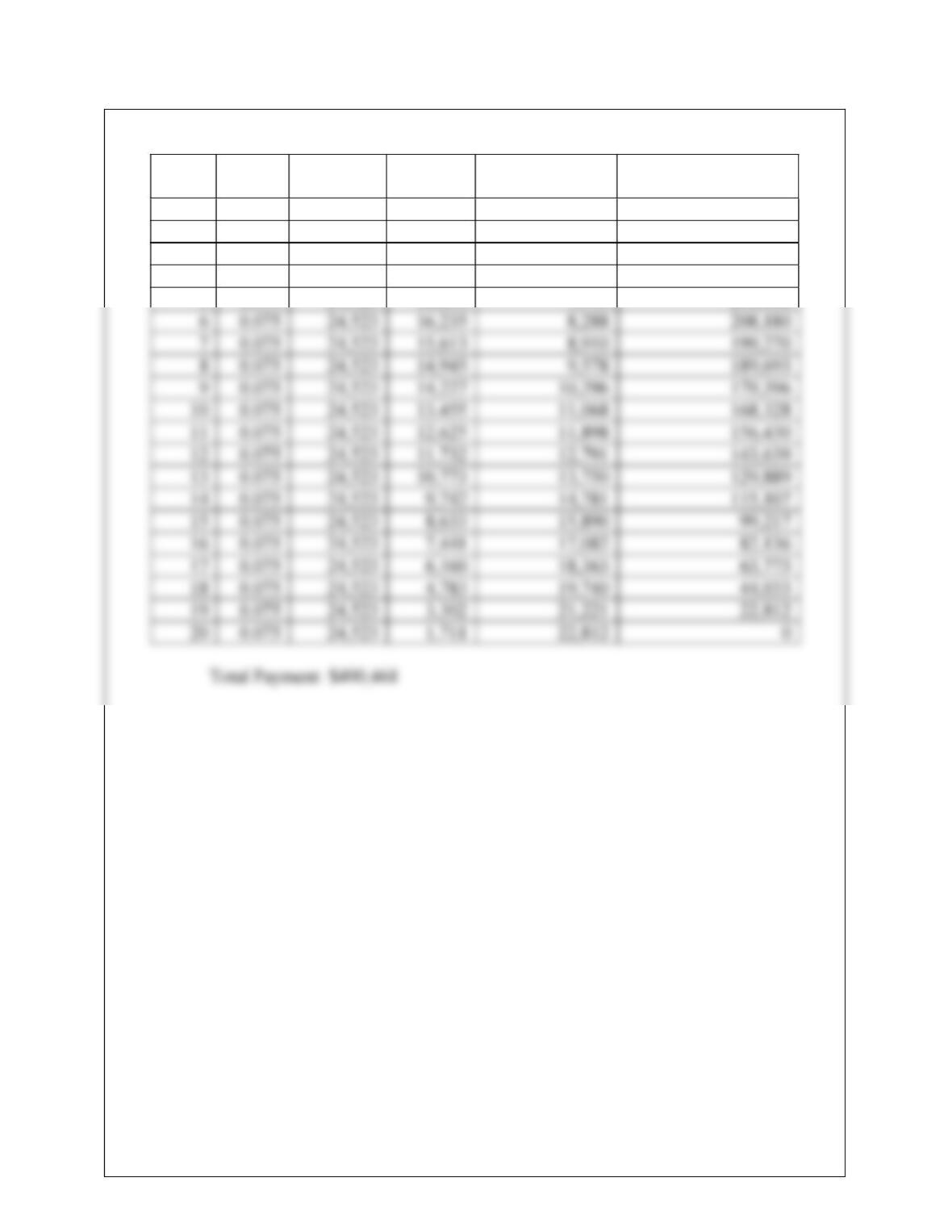

Variable Rate Simulation

Year iPayment

($/y)

Interest

($/y)

Principal Paid

($/y)

Remaining Balance

($/y)

1 0.0765 24,795 19,114 5,681 244,319

2 0.0664 23,010 16,230 6,779 237,539

3 0.0727 24,078 17,271 6,807 230,732

4 0.0757 24,577 17,471 7,106 223,626

5 0.0694 23,583 15,526 8,057 215,569

10-32

Fixed Rate Simulation

Year iPayment

($/y)

Interest

($/y)

Principal Paid

($/y)

Remaining Balance

($/y)

1 0.075 24,523 18,750 5,773 244,227

2 0.075 24,523 18,317 6,206 238,021

3 0.075 24,523 17,852 6,671 231,349

4 0.075 24,523 17,351 7,172 224,178

5 0.075 24,523 16,813 7,710 216,468

10-33

10.42

10-34

10.43 (a) UTRMWT CCCRni

P

FCINPV ,,

(c) When NPV = 0 and number of batches = 26/yr, i = 14.1%

i = 14.1%

10.44 (a) INPV = –FCI +YS(P / A,i,n) or EAOC = FCI(A/P,i,n) – YS

(b) 196,734$

17.0117.0

117.01

)000,950125,321,1(000,750 5

5

xINPV

x = 1.12

10-35

10.45 (a) INPV = –FCI +YS(P / A,i,n) or EAOC = FCI(A/P,i,n) – YS

Do not recommend this process.

(b) When INPV = 0 or EAOC = 0, FCI = $4.99 million