Accounting Information Systems, 10e 1

SOLUTIONS FOR CHAPTER 9

Each end-of-chapter question in the Solutions Manual is tagged to correspond with AACSB, AICPA

and CISA standards, allowing professors to more easily manage the task of reporting outcomes to these

professional and accrediting bodies. Please see the corresponding spreadsheet file for the tagging

information.

Discussion Questions

DQ 9-1 Discuss why the control matrix is custom-tailored for each business process.

ANS. The control matrix is customized for each business process because the following

DQ 9-2 Explain why input controls are so important. Discuss fully.

ANS. Perhaps the most error-prone and inefficient steps in an operations or information

process are the steps during which data is entered into a system. Although much

has been done to improve the accuracy and efficiency of the data entry process,

problems still remain, especially when humans enter data into a system.

2 Solutions for Chapter 9

is based on invalid or inaccurate data).

DQ 9-3 In evaluating business process controls and application controls, some auditors

differentiate between the point in the system at which the control is “established”

and the later point at which that control is “exercised.” Speculate about the

meaning of the terms “establish a control” and “exercise a control” by discussing

those terms in the context of the following:

a. Batch total procedures

ANS. We establish the control when we calculate the original batch total. We exercise

ANS. We establish the control when we prepare a turnaround document, typically by

having a document printed by a computer, as, for example, the stub of a customer

invoice. We exercise the control when we use that document for input to a

DQ 9-4 “The mere fact that event data appear on a prenumbered document is no proof of

the validity of the event. Someone intent on defrauding a system by introducing a

fictitious event probably would be clever enough to get access to the prenumbered

documents or would replicate those documents to make the event appear

genuine.”

a. Do you agree with this comment? Why or why not?

ANS. To some extent, we agree. An individual inside the organization or normally

Accounting Information Systems, 10e 3

DQ 9-5 Describe situations in your daily activities, working or not, where you have

experienced or employed controls in this chapter.

ANS. Many students will have worked in retail as cashiers, wait staff, and so on. They

will also likely have engaged in retail as consumers. Therefore, situations that

might be mentioned include the following. Most retail sites on the Internet use

DQ 9-6 Referring to Appendix 9A, discuss fully the following statement: “Protecting the

private key is a critical element in public key cryptography.”

ANS. If we receive a transmission and open it with a public key (say Bob’s public key),

unauthorized use of that key is critical to the integrity of public key cryptography.

DQ 9-7 On October 2, 2002, a clerk at Bear Stearns had erroneously entered an order to

sell nearly $4 billion worth of securities. The trader had sent an order to sell $4

million worth. Only $622 million of the order was executed, and the remainder of

the order was canceled prior to execution. Reports stated that it was a human

error, not a computer error and that it was the fault of the clerk, not the trader.

What is your opinion of these reports? What controls could have prevented this

error?

4 Solutions for Chapter 9

ANS. If the clerk misread the order and input the order for $4 billion, rather than $4

million, there is a human error. But it is not clear whose error this is. Was the

DQ 9-8 “Technology Summary 9.1 seems to indicate that the business process and

application control plans in this chapter cannot be relied on.” Do you agree?

Discuss fully.

ANS. No, we do not agree. As indicated in Figure 7.6, the hierarchy of controls has

business process and application control plans at the bottom. Does that mean that

they cannot be relied on? No, but it does mean that we need to be aware of the

DQ 9-9 “If a business process is implemented with OLRT processing, we do not need to

worry about update completeness and update accuracy.” Do you agree? Discuss

fully.

Accounting Information Systems, 10e 5

ANS. No, we do not agree. Our control framework looks separately at update

completeness (UC) and update accuracy (UA) only when there is a delay between

Short Problems

SP 9-1 ANS.

1. D

SP 9-2 ANS.

1. No. Only someone with Sally’s private key (D) can open the message. (This assumes that

only Sally has her private key.)

2. No. Anyone with Sally’s public key (C) can send this message.

SP 9-3 ANS.

Control Plan

Input Validity

Input Completeness

Input Accuracy

Document design

1

Written approvals

2

6 Solutions for Chapter 9

FIGURE SM-9.1 Short Problem 3 Completed Table

Description of table entries (number 1 and 2 were given):

1. A well-designed document can be filled in completely and legibly and be input to the computer with fewer

errors.

2. Approvals indicate authorization for a document or business event, thus reducing the possibility of

processing invalid events.

7. By matching the hash total in the signature message with the hash total of the encrypted message, we can

ensure that the message was not altered in transmission.

8. If we reconcile the count documents before entry with the total number of documents accepted by the

computer, we have some evidence (but not strong evidence) that no invalid documents were entered.

9. If we reconcile the count documents before entry with the total number of documents accepted by the

computer, we have some evidence (but not strong evidence) that all documents were entered once and only

once.

Accounting Information Systems, 10e 7

Problems

P 9-1

a. ANS. The control matrix is shown in Figure SM-9.2, and the explanations of the cell

b. ANS. See Figure SM-9.2.

8 Solutions for Chapter 9

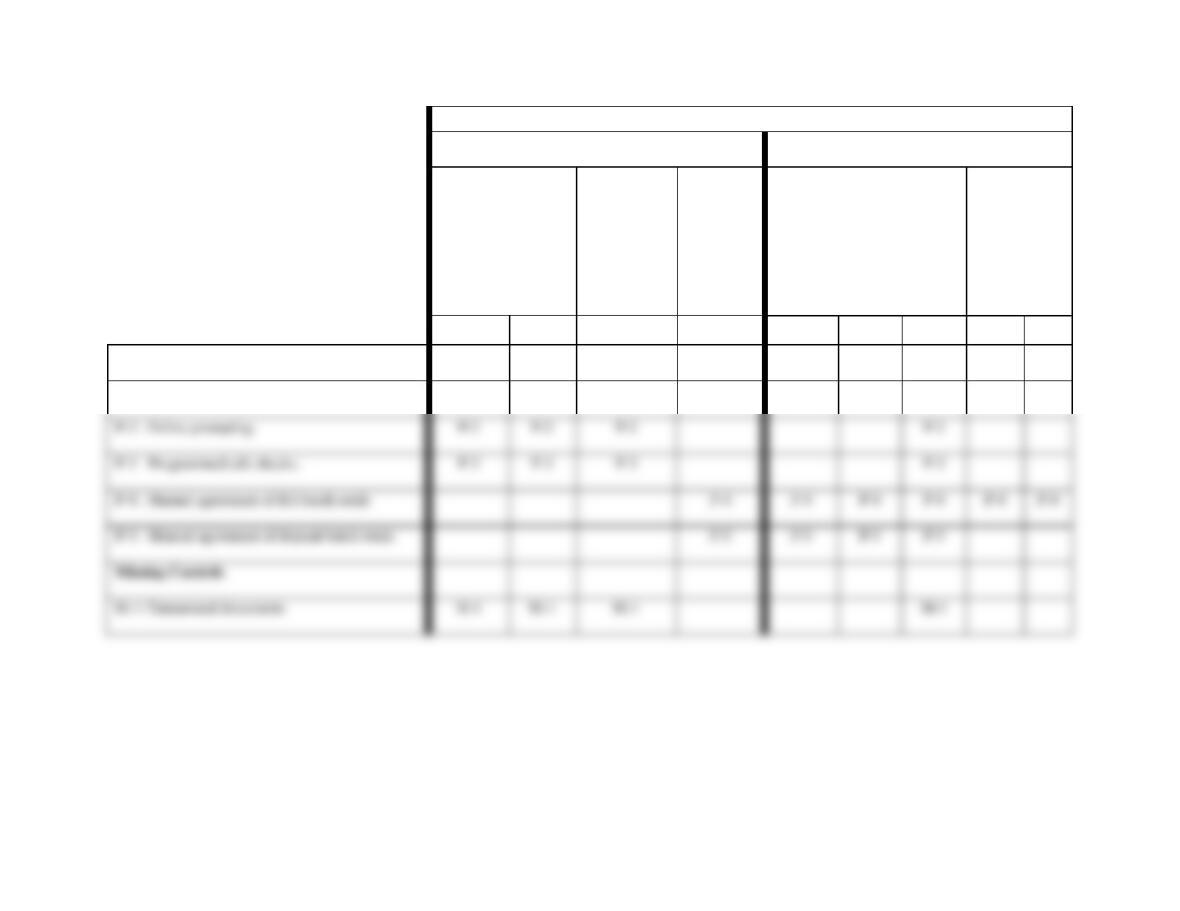

Control Goals of the BridgeportCash Receipts Process

Control Goals of the Operations Process

Control Goals of the Information Process

Ensure effectiveness

of operations:

Ensure

efficient

employment

of resources

(people,

computers)

Ensure

security of

resources

(cash,

accounts

receivable

master

data)

For the remittance advice

inputs (i.e., cash receipts),

ensure:

For the

accounts

receivable

master data,

ensure:

Recommended control plans

A

B

IV

IC

IA

UC

UA

Present Controls

P-1: Preformatted screens

P-1

P-1

P-1

P-1

P-2: Online prompting

P-2

P-2

P-2

P-2

P-5: Manual agreement of deposit batch totals

P-5

P-5

P-5

P-5

M-1: Turnaround documents

Accounting Information Systems, 10e 9

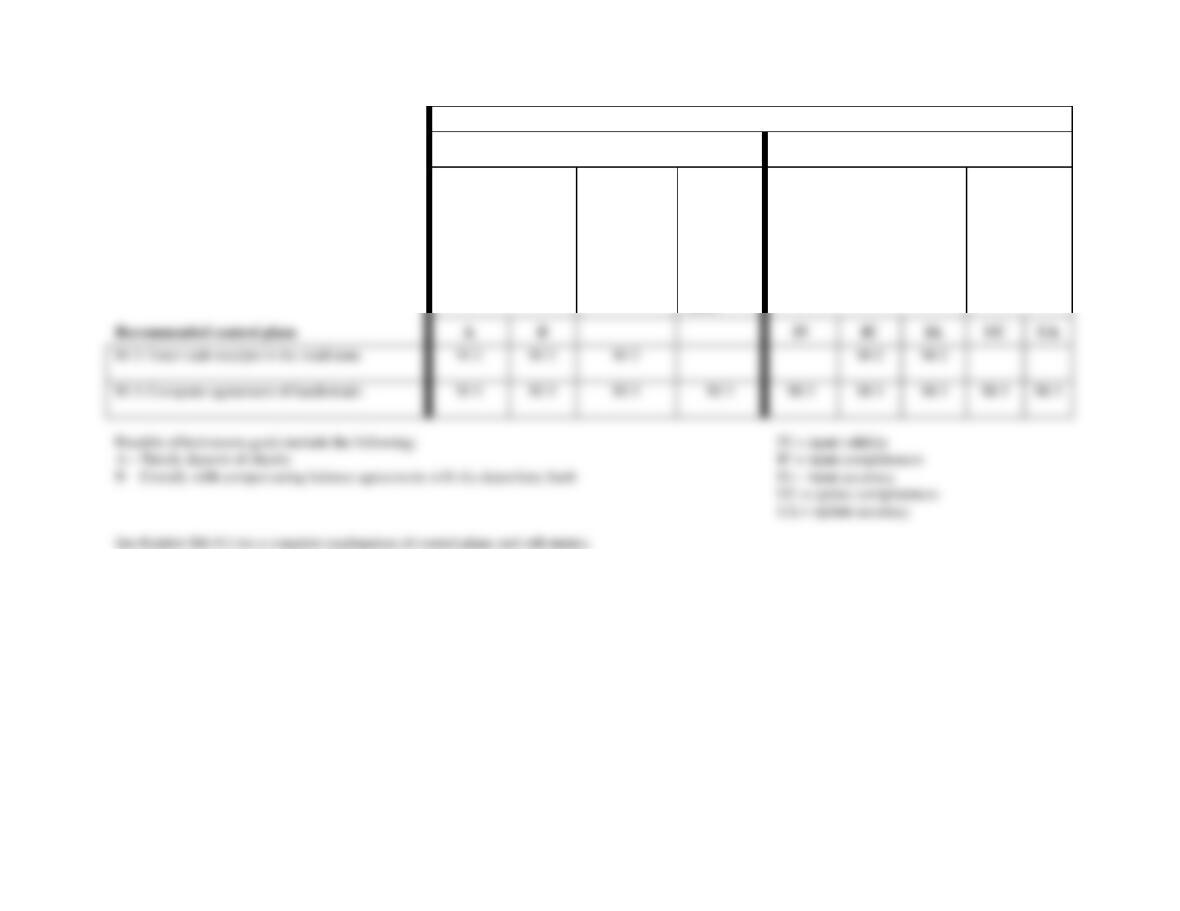

Control Goals of the BridgeportCash Receipts Process

Control Goals of the Operations Process

Control Goals of the Information Process

Ensure effectiveness

of operations:

Ensure

efficient

employment

of resources

(people,

computers)

Ensure

security of

resources

(cash,

accounts

receivable

master

data)

For the remittance advice

inputs (i.e., cash receipts),

ensure:

For the

accounts

receivable

master data,

ensure:

FIGURE SM-9.2 Problem 1 Part a Solution (Partial)—Control Matrix for Bridgeport LLC

10 Solutions for Chapter 9

Exhibit SM-9.1 Problem 9-1 Part a Solution (Partial)—Explanation of Cell Entries

Discussion and Explanation of Recommended Control Plans

P-1: Preformatted screens.

System goals A and B, efficient employment of resources: By structuring the data

entry process and by preventing input errors, data entry is simplified, time saved,

P-2: Online prompting.

System goals A and B, efficient employment of resources: Asking the user for

input or asking questions that the user must answer can ensure a quicker and more

P-3: Programmed edit checks.

Effectiveness goals A and B, efficient employment of resources: Event data can be

processed on a timelier basis when errors are identified and the input clerk can

take corrective action immediately. Event data can be processed on a timelier

Input accuracy: The edits identify erroneous or suspect data and can reduce input

errors.

P-4: Manual agreement of RA batch totals. (Solution Note: The following discussion

assumes that the batch totals are hash totals. If the batch totals consisted of

Accounting Information Systems, 10e 11

P-5: Manual agreement of deposit batch totals.

Note: We assume that the cashier is reconciling batch totals. Perhaps this control

is a one-for-one comparison of the checks on the deposit slip to those in the

temporary file.

M-1: Turnaround documents.

Effectiveness goals A and B, efficient employment of resources, input accuracy: A

document, printed by the computer, is used to capture and input a subsequent

M-2: Enter cash receipts in the mailroom.

Effectiveness goals A and B, efficient employment of resources: If the cash

receipts were to be entered immediately upon receipt at the organization, the cash

12 Solutions for Chapter 9

M-3: Computer agreement of batch totals. (Solution Note: The following discussion

assumes that the batch totals are hash totals. If the batch totals consisted of

document/record counts and/or item/line counts only, those types of batch totals

would address only the goals of input validity, input completeness, and update

completeness.)

Accounting Information Systems, 10e 13

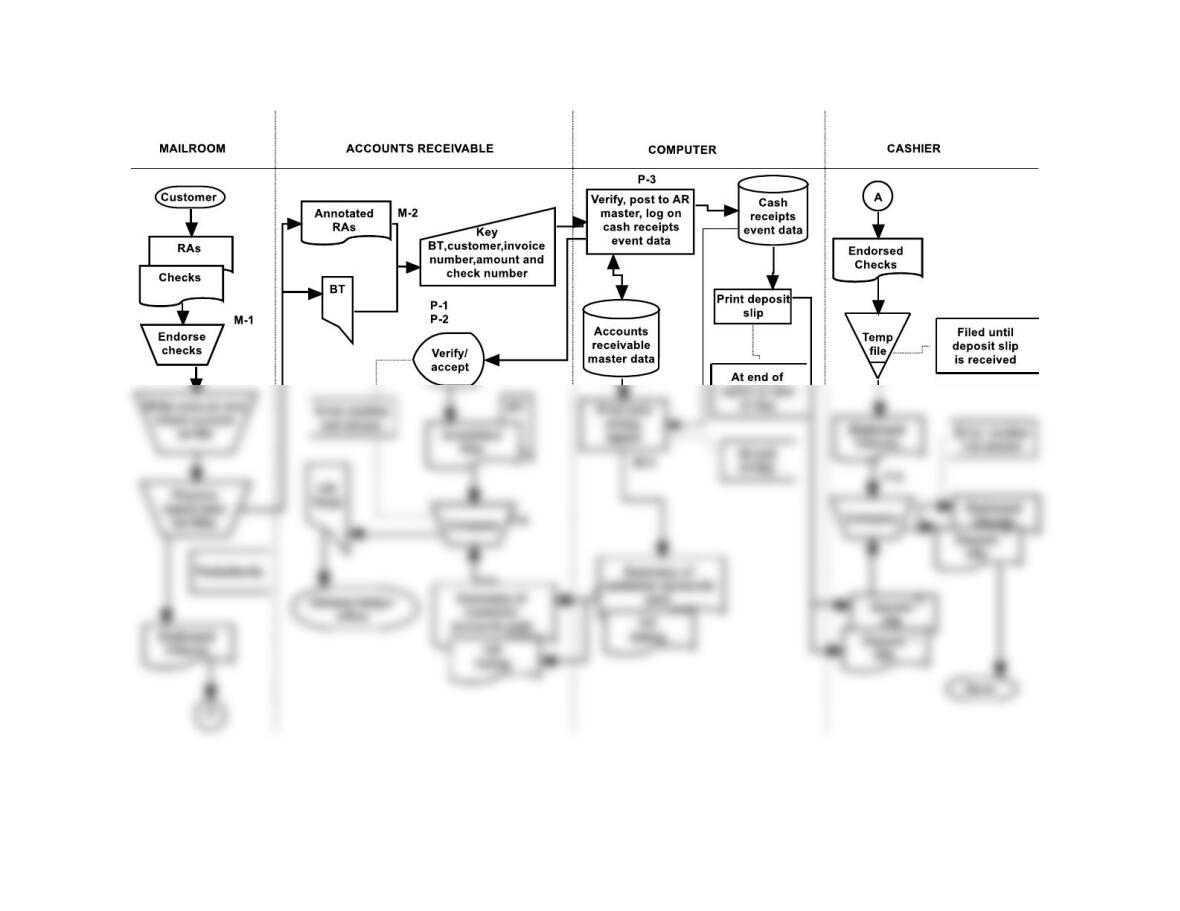

Figure SM-9.3 Problem 1 Part b Solution—Annotated Systems Flowchart for Causeway

14 Solutions for Chapter 9

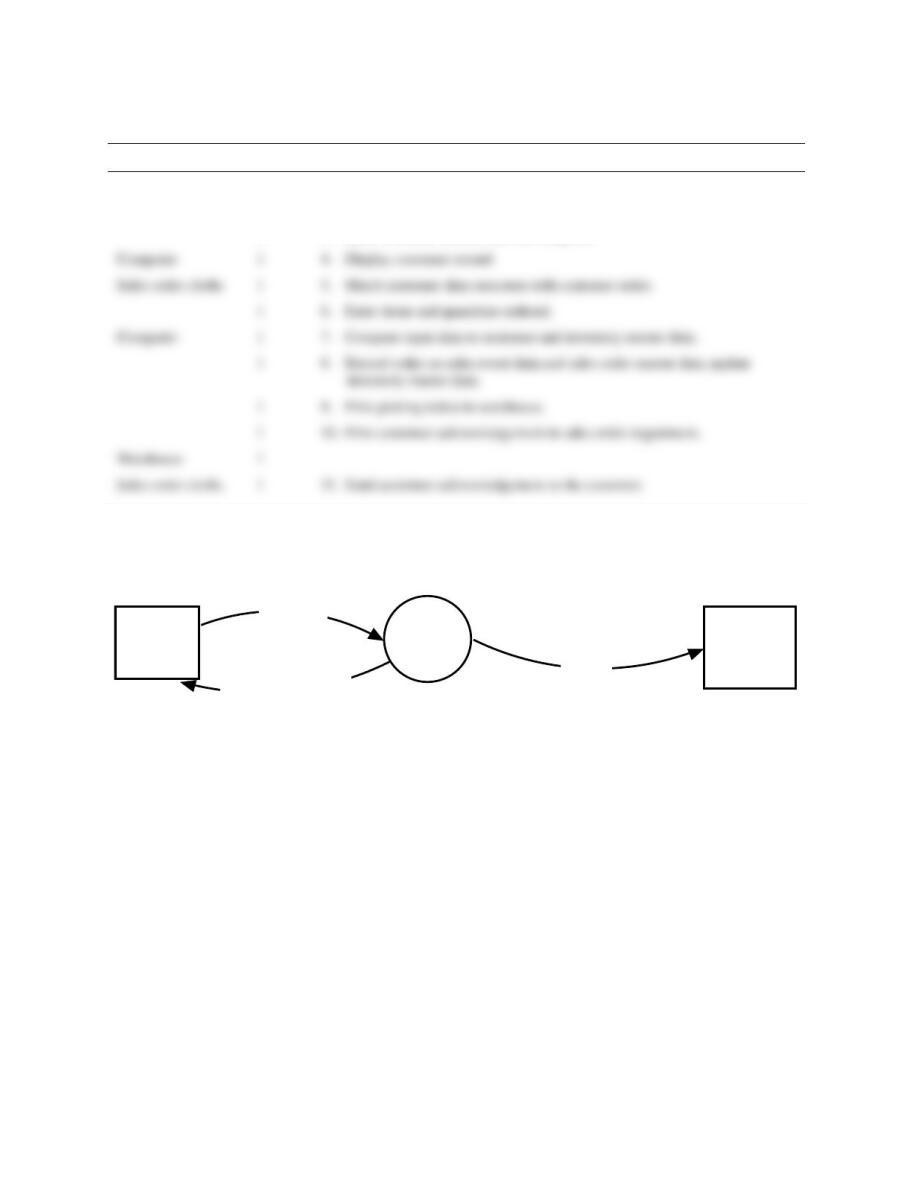

P 9-2 a. ANS. Table of Entities and Activities for Eye-Dee-A-Pet, Inc.,

Entities

Para

Activities

Customer

1

1. Send orders by mail.

Sales order clerks

1

2. Open and review orders for accuracy.

1

3. Enter customer number into the computer.

Customer

Sales

order

entry

system

Warehouse

Customer

order

Customer

acknowledgement

Picking

ticket

FIGURE SM-9.4 Problem 2 Part b Solution—Context Diagram for Eye-Dee-A-Pet, Inc.,

(Would look like this in Microsoft Visio or other diagraming software.)

Computer

1

4. Display customer record.

1

5. Match customer data onscreen with customer order.

1

7. Compare input data to customer and inventory master data.

1

9. Print picking ticket in warehouse.

1

10. Print customer acknowledgement in sales order department.

Sales order clerks

1

11. Send customer acknowledgement to the customer.