E9-20 Computing depreciation—three methods

Learning Objective 2

1. Double-declining-balance, 12/31/17, Exp. $5,250

(Requirement 1 only)

Crackling Fried Chicken bought equipment on January 2, 2016, for $21,000. The equipment was

expected to remain in service for four years and to perform 3,600 fry jobs. At the end of the equipment’s

useful life, Crackling’s estimates that its residual value will be $3,000. The equipment performed 360

jobs the first year, 1,080 the second year, 1,440 the third, and 720 the fourth year.

Requirements

1. Prepare a schedule of depreciation expense, accumulated depreciation, and book value per year for

the equipment under the three depreciation methods. Show your computations. Note: Three

depreciation schedules must be prepared.

2. Which method tracks the wear and tear on the equipment most closely?

SOLUTION

Requirement 1

Depreciable cost = Cost − Residual value = $21,000 − $3,000 = $18,000

Straight-Line Depreciation Schedule

Depreciation for the Year

Date

Asset

Cost

Depreciable

Cost

Depreciation

Rate

Depreciation

Expense

Accumulated

Depreciation

Book

Value

1/01/16

$ 21,000

$ 21,000

16,500

12,000

Depreciation per unit

=

(Cost – Residual value) / Useful life in units

=

$5 per fry job

Date

Asset

Cost

Depreciation

per Unit

of Units

Depreciation

Expense

Accumulated

Depreciation

Book

Value

1/01/16

$ 21,000

$ 21,000

19,200

13,800

E9-20, cont.

Requirement 1, cont.

Double-Declining-Balance Depreciation Schedule

Depreciation for the Year

Date

Asset

Cost

Book

Value

DDB

Rate

Depreciation

Expense

Accumulated

Depreciation

Book

Value

1/01/16

$ 21,000

$ 21,000

10,500

Requirement 2

E9-21 Changing an asset’s useful life and residual value

Learning Objective 2

Yr. 16 $42,400

Budget Hardware Consultants purchased a building for $452,000 and depreciated it on a straight-line

basis over a 35-year period. The estimated residual value is $102,000. After using the building for 15

years, Budget realized that wear and tear on the building would wear it out before 35 years and that the

estimated residual value should be $90,000. Starting with the 16th year, Budget began depreciating the

building over a revised total life of 20 years using the new residual value. Journalize depreciation

expense on the building for years 15 and 16.

SOLUTION

Straight-line depreciation

=

(Cost − Residual value) / Useful life

=

Accumulated depreciation after 15 years

=

$10,000 per year × 15 years

=

$150,000

Book value after 15 years

=

(Cost – Accumulated Depreciation)

=

$302,000

Revised depreciation

=

(Book value − Revised residual value) / Revised useful life remaining

=

($302,000 − $90,000) / (20 total years – 15 previous years)

=

E9-22 Recording partial-year depreciation and sale of an asset

Learning Objectives 2, 3

Depr. Exp. $2,400

On January 2, 2015, Ditto Clothing Consignments purchased showroom fixtures for $12,000 cash,

expecting the fixtures to remain in service for five years. Ditto has depreciated the fixtures on a double-

declining-balance basis, with zero residual value. On October 31, 2016, Ditto sold the fixtures for

$5,900 cash. Record both depreciation expense for 2016 and sale of the fixtures on October 31, 2016.

SOLUTION

Double-declining-balance

=

(Cost – Accumulated depreciation) × 2 × (1 / Useful life)

=

$4,800 in year 1

=

(Cost – Accumulated depreciation) × 2 × (1 / Useful life)

=

Market value of assets received

Less: Book value of asset disposed of

Cost

$ 12,000

Less: Accumulated Depreciation ($4,800 + $2,400)

Gain or (Loss)

Date

Accounts and Explanation

Debit

Credit

Oct. 31

Depreciation Expense—Fixtures

2,400

Accumulated Depreciation—Fixtures

2,400

To record depreciation on fixtures.

Cash

5,900

Accumulated Depreciation—Fixtures

7,200

Fixtures

Gain on Disposal

1,100

Sold fixtures for cash.

E9-23 Recording partial-year depreciation and sale of an asset

Learning Objectives 2, 3

Loss $(6,000)

On January 2, 2014, Pet Salon purchased fixtures for $48,200 cash, expecting the fixtures to remain in

service for nine years. Pet Salon has depreciated the fixtures on a straight-line basis, with $5,000

residual value. On May 31, 2016, Pet Salon sold the fixtures for $30,600 cash. Record both depreciation

expense for 2016 and sale of the fixtures on May 31, 2016.

SOLUTION

Straight-line depreciation

=

(Cost − Residual value) / Useful life

=

$4,800 per year (2014 and 2015)

=

(Cost − Residual value) / Useful life

=

Market value of assets received

Less: Book value of asset disposed of

Cost

$ 48,200

Less: Accumulated Depreciation ($4,800 + $4,800 + $2,000)

Gain or (Loss)

Date

Accounts and Explanation

Debit

Credit

May 31

Depreciation Expense—Fixtures

2,000

Accumulated Depreciation—Fixtures

2,000

To record depreciation on fixtures.

Cash

30,600

Accumulated Depreciation—Fixtures

11,600

Loss on Disposal

6,000

Fixtures

E9-24 Journalizing natural resource depletion

Learning Objective 4

$1.20 per ton

Colorado Mountain Mining paid $507,700 for the right to extract mineral assets from a 500,000-ton

deposit. In addition to the purchase price, Colorado also paid a $600 filing fee, a $1,700 license fee to

the state of Nevada, and $90,000 for a geological survey of the property. Because Colorado purchased

the rights to the minerals only, it expects the asset to have zero residual value. During the first year,

Colorado removed and sold 60,000 tons of the minerals. Make journal entries to record (a) purchase of

the minerals (debit Minerals), (b) payment of fees and other costs, and (c) depletion for the first year.

SOLUTION

Purchase price of minerals

$ 507,700

Add related costs:

Filing fee

License

Geological survey

92,300

Total cost of minerals

$ 600,000

Depletion per unit

(Cost – Residual value) / Estimated total units

$1.20 per ton

Depletion expense

Depletion per unit × Number of units extracted

$1.20 per ton × 60,000 tons

$72,000

Date

Accounts and Explanation

Debit

Credit

a.

Minerals

507,700

Cash

507,700

To record purchase of mineral rights.

b.

Minerals

Cash

purchase of minerals.

c.

Depletion Expense—Minerals

Accumulated Depletion—Minerals

To record depletion.

E9-25 Handling acquisition of patent, amortization, and change in useful life

Learning Objectives 2, 5

2. Amort. Exp. $225,000

Medway Printers (MP) manufactures printers. Assume that MP recently paid $900,000 for a patent on a

new laser printer. Although it gives legal protection for 20 years, the patent is expected to provide a

competitive advantage for only eight years.

Requirements

1. Assuming the straight-line method of amortization, make journal entries to record (a) the purchase of

the patent and (b) amortization for the first full year.

2. After using the patent for four years, MP learns at an industry trade show that another company is

designing a more efficient printer. On the basis of this new information, MP decides, starting with

year 5, to amortize the remaining cost of the patent over two remaining years, giving the patent a

total useful life of six years. Record amortization for year 5.

SOLUTION

Requirement 1

Amortization expense

=

(Cost – Residual value) / Useful life

=

$112,500

900,000

112,500

Requirement 2

Accumulated amortization after 4 years

=

$112,500 per year × 4 years

=

$450,000

Book value after 4 years

(Cost – Accumulated Amortization)

$450,000

Revised amortization

=

E9-26 Measuring and recording goodwill

Learning Objective 5

2. Goodwill $7,000,000

Princess has acquired several other companies. Assume that Princess purchased Kettle for $11,000,000

cash. The book value of Kettle’s assets is $12,000,000 (market value,

$16,000,000), and it has liabilities of $12,000,000 (market value, $12,000,000).

Requirements

1. Compute the cost of the goodwill purchased by Princess.

2. Record the purchase of Kettle by Princess.

SOLUTION

Requirement 1

Purchase price to acquire Kettle

$ 11,000,000

Market value of Kettle’s assets

$ 16,000,000

Less: Kettle’s liabilities

Market value of Kettle’s net assets

Goodwill

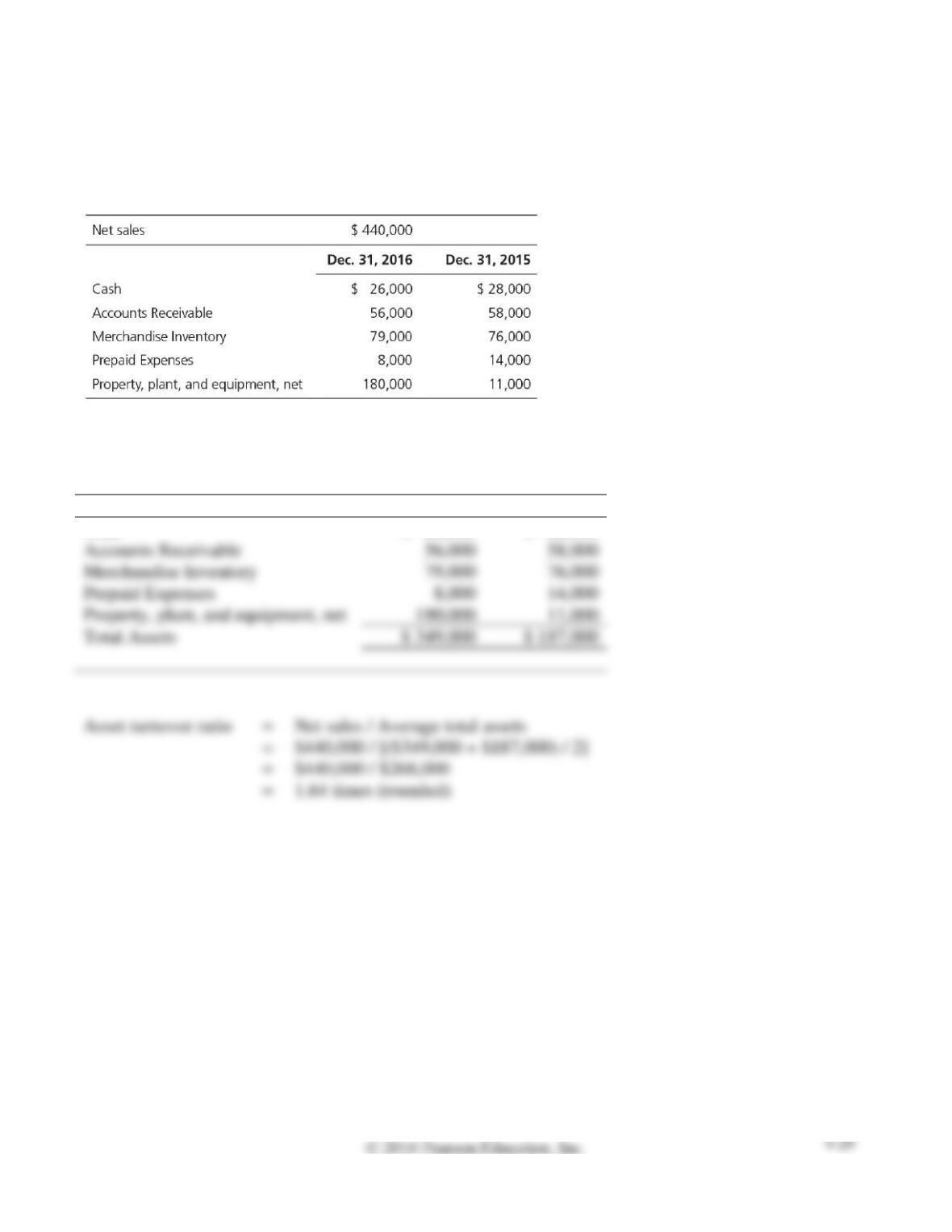

E9-27 Computing asset turnover ratio

Learning Objective 6

Snap Dragon Photo reported the following figures on its December 31, 2016, income statement and

balance sheet:

Compute the asset turnover ratio for 2016.

SOLUTION

Dec. 31, 2016

Dec. 31, 2015

Cash

$ 26,000

$ 28,000

Accounts Receivable

Merchandise Inventory

Prepaid Expenses

Property, plant, and equipment, net

Total Assets

$ 349,000

$ 187,000

Asset turnover ratio

Net sales / Average total assets

$440,000 / [($349,000 + $187,000) / 2]

$440,000 / $268,000

1.64 times (rounded)

E9A-28 Exchanging assets—two situations

Learning Objective 7

Appendix 9A

2. Loss $(7,000)

Commerce Bank recently traded in office fixtures. Here are the facts:

equirements

1. Record Commerce Bank’s trade-in of old fixtures for new ones. Assume the exchange had

commercial substance.

2. Now let’s change one fact. Commerce Bank feels compelled to do business with Shoreside

Furniture, a bank customer, even though the bank can get the fixtures elsewhere at a better price.

Commerce Bank is aware that the new fixtures’ market value is only $135,000. Record the trade-in.

Assume the exchange had commercial substance.

SOLUTION

Requirement 1

Market value of assets received

$ 142,000

Less:

Book value of asset exchanged

Cost

$ 99,000

Less: Accumulated depreciation

$ 34,000

Cash paid

Gain or (Loss)

108,000

Requirement 2

Market value of assets received

$ 135,000

Less:

Book value of asset exchanged

Cost

$ 99,000

Less: Accumulated depreciation

$ 34,000

Cash paid

(142,000)

Gain or (Loss)

$ (7,000)

108,000

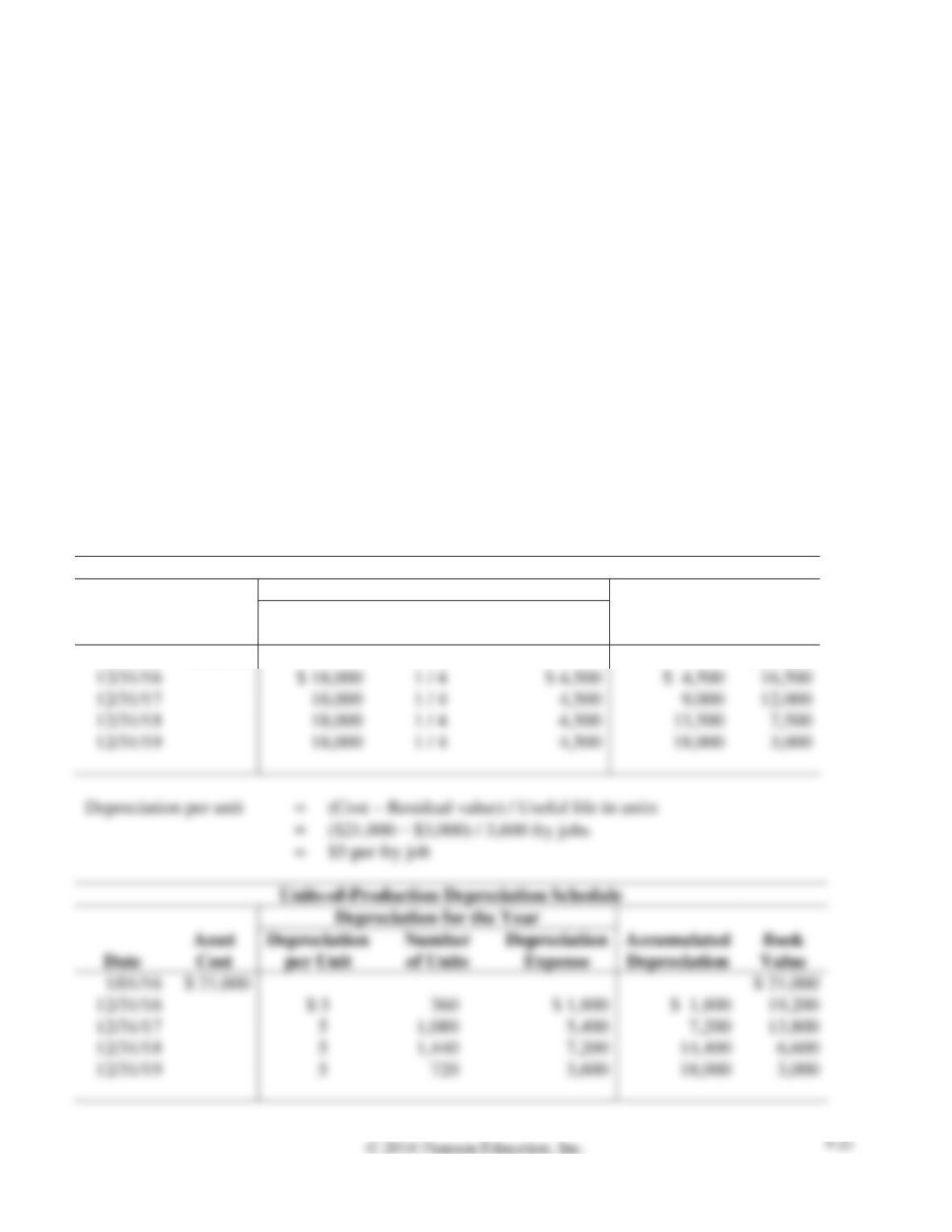

E9A-29 Measuring asset cost, units-of-production depreciation, and asset trade

Learning Objectives 1, 2, 7

Appendix 9A

1. $12,870

Pact Trucking Corporation uses the units-of-production depreciation method because units-of–

production best measures wear and tear on the trucks. Consider these facts about one Mack truck in the

company’s fleet.

When acquired in 2013, the rig cost $450,000 and was expected to remain in service for 10 years or

1,000,000 miles. Estimated residual value was $120,000. The truck was driven 82,000 miles in 2013,

122,000 miles in 2014, and 162,000 miles in 2015. After 39,000 miles, on March 15, 2016, the company

traded in the Mack truck for a less expensive Freightliner. Pact also paid cash of $27,000. Fair market

value of the Mack truck was equal to its net book value on the date of the trade.

Requirements

1. Record the journal entry for depreciation expense in 2016.

2. Determine Pact’s cost of the new truck.

3. Record the journal entry for the exchange of assets on March 15, 2016. Assume the exchange had

commercial substance.

SOLUTION

Requirement 1

Depreciation per unit

=

(Cost – Residual value) / Useful life in units

=

$0.33 per mile

Units-of-production

=

Depreciation per unit × Current year usage

=

$0.33 per mile × 82,000 miles

=

$27,060 in 2013

=

Depreciation per unit × Current year usage

=

$0.33 per mile × 122,000 miles

=

$40,260 in 2014

=

Depreciation per unit × Current year usage

=

$0.33 per mile × 162,000 miles

=

$53,460 in 2015

=

Depreciation per unit × Current year usage

=

$0.33 per mile × 39,000 miles

=

$12,870 in 2016

Total accumulated depreciation

=

$27,060 + $40,260 + $53,460 + $12,870

=

$133,650

Date

Accounts and Explanation

Debit

Credit

E9A-29, cont.

Requirement 2

Market value of assets received

$ 343,350

Less:

Book value of asset exchanged

Cost

$ 450,000

Less: Accumulated depreciation

(133,650)*

$ 316,350

Cash paid

27,000

343,350

Gain or (Loss)

$ 0

*from Requirement 1

If the fair market value of the old truck is equal to its net book value, then the “trade–in” value of the old

truck is equal to the book value and there is no gain or loss on the exchange. Therefore, the cost of the

new truck is $343,350—the book value of the old truck plus the cash paid.

Requirement 3

Date

Accounts and Explanation

Debit

Credit

Mar. 15

Truck (new)

343,350

Accumulated Depreciation—Truck

133,650

Truck (old)

450,000

Cash

27,000

Exchanged old truck and cash for new truck.

Problems (Group A)

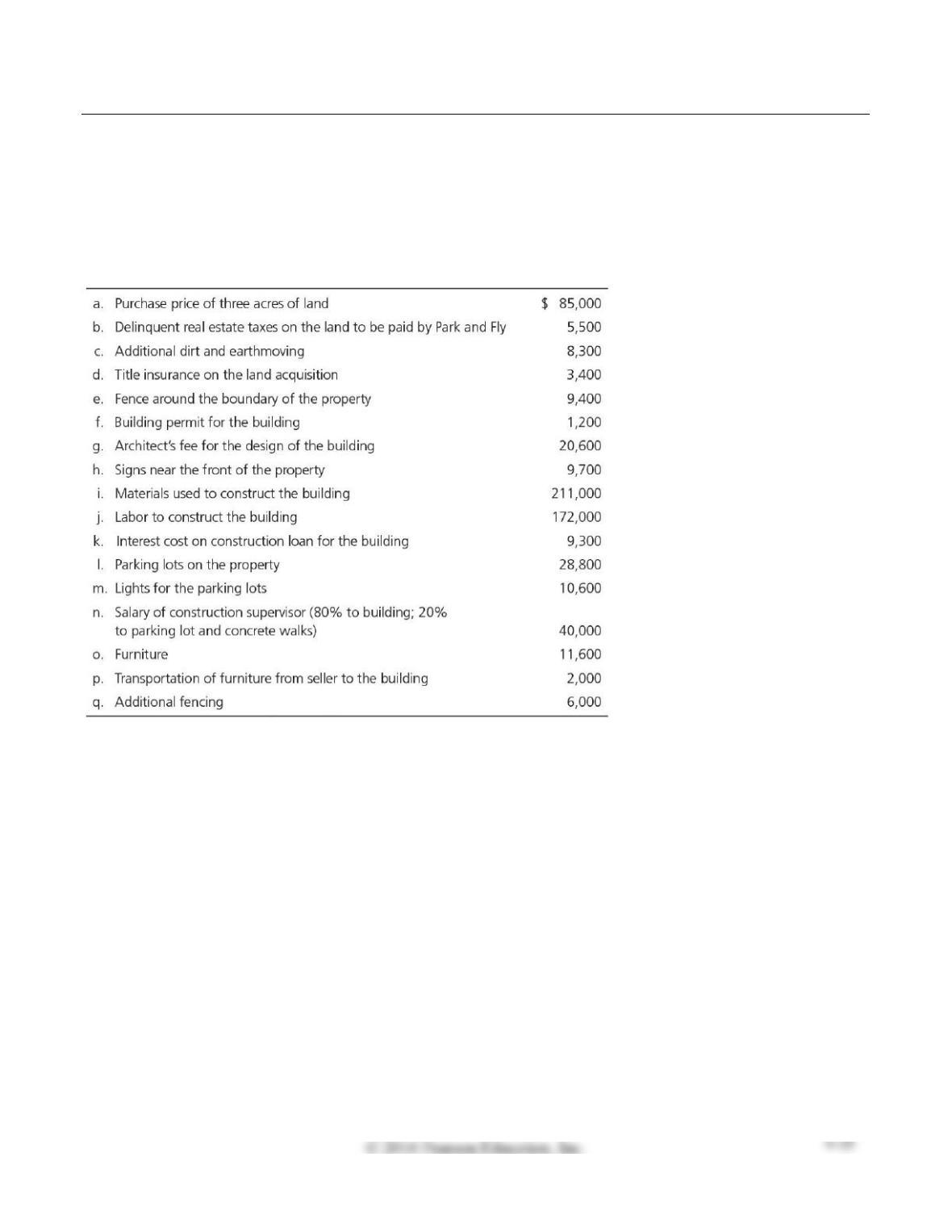

P9-30A Determining asset cost and recording partial-year depreciation

Learning Objectives 1, 2

1. Bldg. $446,100

Park and Fly, near an airport, incurred the following costs to acquire land, make land improvements, and

construct and furnish a small building:

Park and Fly depreciates land improvements over 20 years, buildings over 40 years, and furniture over

eight years, all on a straight-line basis with zero residual value.

Requirements

1. Set up columns for Land, Land Improvements, Building, and Furniture. Show how to account for

each cost by listing the cost under the correct account. Determine the total cost of each asset.

2. All construction was complete and the assets were placed in service on October 1. Record partial-

year depreciation expense for the year ended December 31.

SOLUTION

Requirement 1

Land

Land

Improvements

Building

Furniture

Purchase price

$ 85,000

Real estate taxes

5,500

Dirt and earthmoving

8,300

Title insurance

3,400

Fence

Building permit

Architect’s fee

Signs

Building materials

Building labor

Interest on construction loan

Parking lots

Lights for parking lots

Salary of construction supervisor

Furniture

Transportation of furniture

Additional fencing

Totals

$102,200

$ 446,100

Requirement 2

Straight-line

=

(Cost − Residual value) / Useful life × (Number of Months / 12)

Land Improvements

=

($72,500 ̶ $0) / 20 years × (3/12)

=

$906 (rounded)

=

$2,788 (rounded)

Furniture

=

=

$425

P9-30A, cont.

Requirement 2, cont.

Date

Accounts and Explanation

Debit

Credit

Dec. 31

Depreciation Expense—Land Improvements

906

Accumulated Depreciation—Land Improvements

906

To record depreciation on land improvements.

Depreciation Expense—Building

Accumulated Depreciation—Building

To record depreciation on building.

Depreciation Expense—Furniture

425

Accumulated Depreciation—Furniture

425

To record depreciation on furniture.

P9-31A Determining asset cost, recording first-year depreciation, and identifying depreciation

results that meet management objectives

Learning Objectives 1, 2

1. Units-of-production, 12/31/16, Dep. Exp. $14,000

On January 3, 2016, Fast Delivery Service purchased a truck at a cost of $62,000. Before placing the

truck in service, Fast spent $3,000 painting it, $1,500 replacing tires, and $3,500 overhauling the engine.

The truck should remain in service for five years and have a residual value of $5,000. The truck’s annual

mileage is expected to be 28,000 miles in each of the first four years and 18,000 miles in the fifth year—

130,000 miles in total. In deciding which depreciation method to use, Steven Kittridge, the general

manager, requests a depreciation schedule for each of the depreciation methods (straight-line, units-of-

production, and double- declining-balance).

Requirements

1. Prepare a depreciation schedule for each depreciation method, showing asset cost, depreciation

expense, accumulated depreciation, and asset book value.

2. Fast prepares financial statements using the depreciation method that reports the highest net income

in the early years of asset use. Consider the first year that Fast uses the truck. Identify the

depreciation method that meets the company’s objectives.

SOLUTION

Requirement 1

Purchase price of truck

$ 62,000

Add related costs:

Painting

$ 3,000

Tires

1,500

Engine overhaul

3,500

8,000

Total cost of truck

$ 70,000

Depreciable cost = Cost − Residual value = $70,000 − $5,000 = $65,000

Straight-Line Depreciation Schedule

Depreciation for the Year

Date

Asset

Cost

Depreciable

Cost

Depreciation

Rate

Depreciation

Expense

Accumulated

Depreciation

Book

Value

1/03/16

$ 70,000

$ 70,000

1 / 5

1 / 5

1 / 5

1 / 5

1 / 5

P9-31A, cont.

Requirement 1, cont.

Depreciation per unit

=

(Cost – Residual value) / Useful life in units

=

($70,000 ̶ $5,000) / 130,000 miles

=

$0.50 per mile

Units-of-Production Depreciation Schedule

Depreciation for the Year

Date

Asset

Cost

Depreciation

per Unit

Number

of Units

Depreciation

Expense

Accumulated

Depreciation

Book

Value

1/03/16

$ 70,000

$ 70,000

12/31/16

$ 14,000

12/31/17

12/31/18

12/31/19

12/31/20

Double-Declining-Balance Depreciation Schedule

Depreciation for the Year

Date

Asset

Cost

Book

Value

DDB

Rate

Depreciation

Expense

Accumulated

Depreciation

Book

Value

1/03/16

$ 70,000

$ 70,000

12/31/16

$ 70,000

2 × (1 / 5)

$ 28,000

$ 28,000

42,000

12/31/17

2 × (1 / 5)

25,200

12/31/18

2 × (1 / 5)

15,120

12/31/19

2 × (1 / 5)

12/31/20

Requirement 2

The depreciation method that reports the highest net income in the first year is the straight-line method.

It produces the lowest depreciation expense ($13,000) and therefore the highest net income.

P9-32A Recording lump-sum asset purchases, depreciation, and disposals

Learning Objectives 1, 2, 3

Sep. 1 Gain $88,000

Grace Carol Associates surveys American eating habits. The company’s accounts include Land,

Buildings, Office Equipment, and Communication Equipment, with a separate Accumulated

Depreciation account for each asset. During 2016, Grace Carol completed the following transactions:

Record the transactions in the journal of Grace Carol Associates.