9-1

CHAPTER 9

Current Liabilities, Contingencies,

and the Time Value of Money

OVERVIEW OF EXERCISES, PROBLEMS, AND CASES

Estimated

Time in

Learning Objectives Exercises Minutes Level

Module 1

1. Identify the components of the Current Liability category of 1 10 Easy

the balance sheet. 2 10 Easy

3 10 Easy

Module 2

3. Explain how changes in current liabilities affect the 9 5 Easy

Module 3

Module 4

5. Explain the difference between simple and compound interest. 12 20 Mod

6. Calculate amounts using the future value and present value 13 6 Easy

concepts. 14 5 Mod

15 10 Mod

16 10 Mod

17 6 Mod

20* 10 Diff

9-2 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

Problems Estimated

and Time in

Learning Objectives Alternates Minutes Level

Module 1

1. Identify the components of the Current Liability category of 10* 10 Mod

the balance sheet.

Module 2

3. Explain how changes in current liabilities affect the 2 30 Mod

statement of cash flows. 3 20 Diff

Module 3

Module 4

5. Explain the difference between simple and compound interest. 6 40 Diff

9* 30 Mod

CHAPTER 9 • CURRENT LIABILITIES, CONTINGENCIES, AND THE TIME VALUE OF MONEY 9-3

Estimated

Time in

Learning Objectives Cases Minutes Level

Module 1

1. Identify the components of the Current Liability category of 1* 30 Mod

the balance sheet. 5* 25 Mod

Module 2

3. Explain how changes in current liabilities affect the 3* 25 Mod

statement of cash flows.

Module 3

Module 4

5. Explain the difference between simple and compound interest.

6. Calculate amounts using the future value and present value

concepts.

9-4 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISES

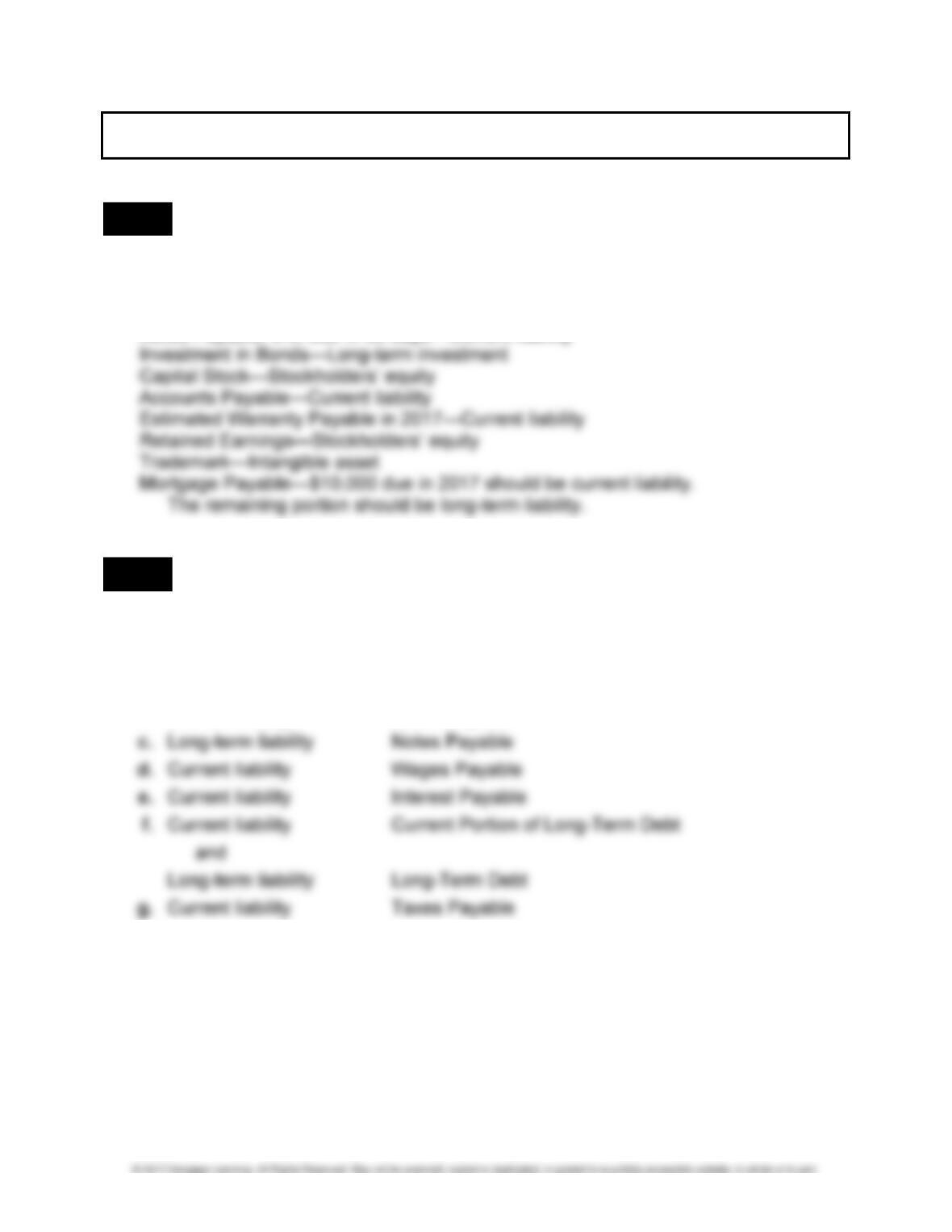

LO 1 EXERCISE 9-1 CURRENT LIABILITIES

The treatment of the items should be as follows:

Taxes Payable—Current liability

Accounts Receivable—Current asset

Notes Payable, 9%, due in 90 days—Current liability

LO 1 EXERCISE 9-2 CURRENT LIABILITIES

1. and 2.

Classification Account Title

a. Current liability Accounts Payable

b. Current liability Notes Payable

3. Investors are interested in this information because it enables them to better predict

the timing of future cash flows. Items that are classified as current liabilities require

the use of current assets to satisfy them, whereas long-term liabilities do not.

CHAPTER 9 • CURRENT LIABILITIES, CONTINGENCIES, AND THE TIME VALUE OF MONEY 9-5

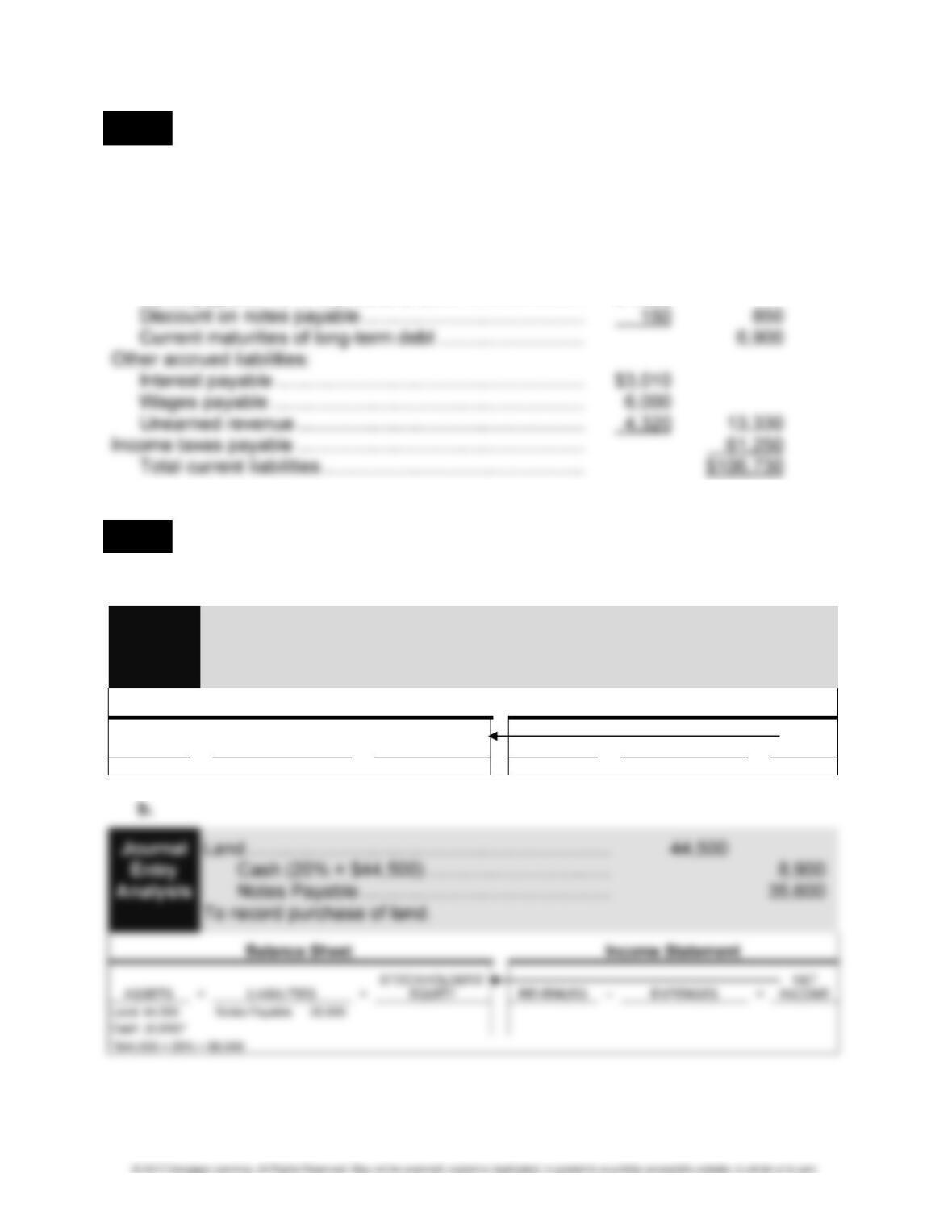

LO 1 EXERCISE 9-3 CURRENT LIABILITIES SECTION

JACKIE COMPANY

BALANCE SHEET

DECEMBER 31, 2016

Current liabilities:

Accounts payable ………………………………………………… $ 24,400

Notes payable, 10%, due June 2, 2017 ………………….. $1,000

LO 2 EXERCISE 9-4 TRANSACTION ANALYSIS

1. a.

Journal Purchases ………………………………………………….. 8,000

Entry Accounts Payable …………………………………. 8,000

Analysis To record purchase of inventory on account.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Accounts Payable 8,000 (8,000) Purchases 8,000 (8,000)

9-6 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISE 9-4 (Continued)

c.

Journal Accounts Payable …………………………………………. 450

Entry Purchase Returns and Allowances…………….. 450

Analysis To record purchase return.

Balance Sheet Income Statement

d.

Journal Accounts Payable ……………………………………….. 7,550

Entry Cash ……………………………………………………. 7,550

Analysis To record payment of account payable.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash(7,550)

Accounts

Payable(7,550)

e.

CHAPTER 9 • CURRENT LIABILITIES, CONTINGENCIES, AND THE TIME VALUE OF MONEY 9-7

EXERCISE 9-4 (Continued)

f.

g.

Journal Cash ($127,200 × 90%) …………………………………. 114,480

Entry Accounts Receivable …………………………………….. 12,720

Analysis Sales …………………………………………………….. 120,000

Sales Tax Payable ………………………………….. 7,200

To record sales and related sales tax.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash

114,480*

Accounts

Receiv-

able 12,720

Sales Tax Payable 7,200

120,000

Sales 120,000

120,000

*$127,200 × 90% = $114,480

2. b.

9-8 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISE 9-4 (Concluded)

e.

Journal Interest Expense …………………………………………… 700

Entry Discount on Notes Payable ($1,200 × 7/12) … 700

Analysis To record interest in advance as interest expense.

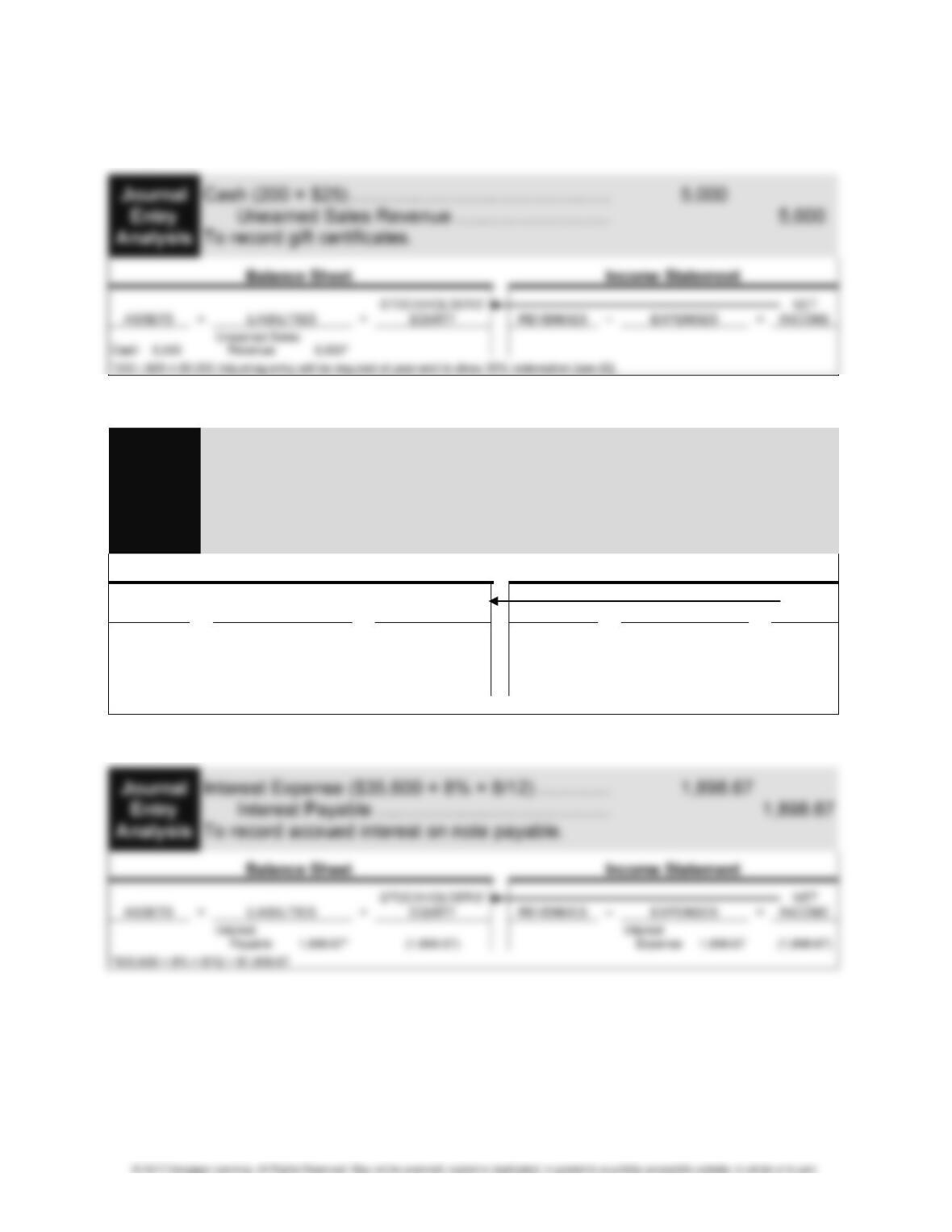

f.

Journal Unearned Sales Revenue ………………………………. 1,750

Entry Sales (35% × $5,000) ………………………………. 1,750

Analysis To record gift certificates redeemed.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Unearned Sales

Revenue (1,750)*

1,750 Sales 1,750 1,750

*$5,000 × 35% = $1,750

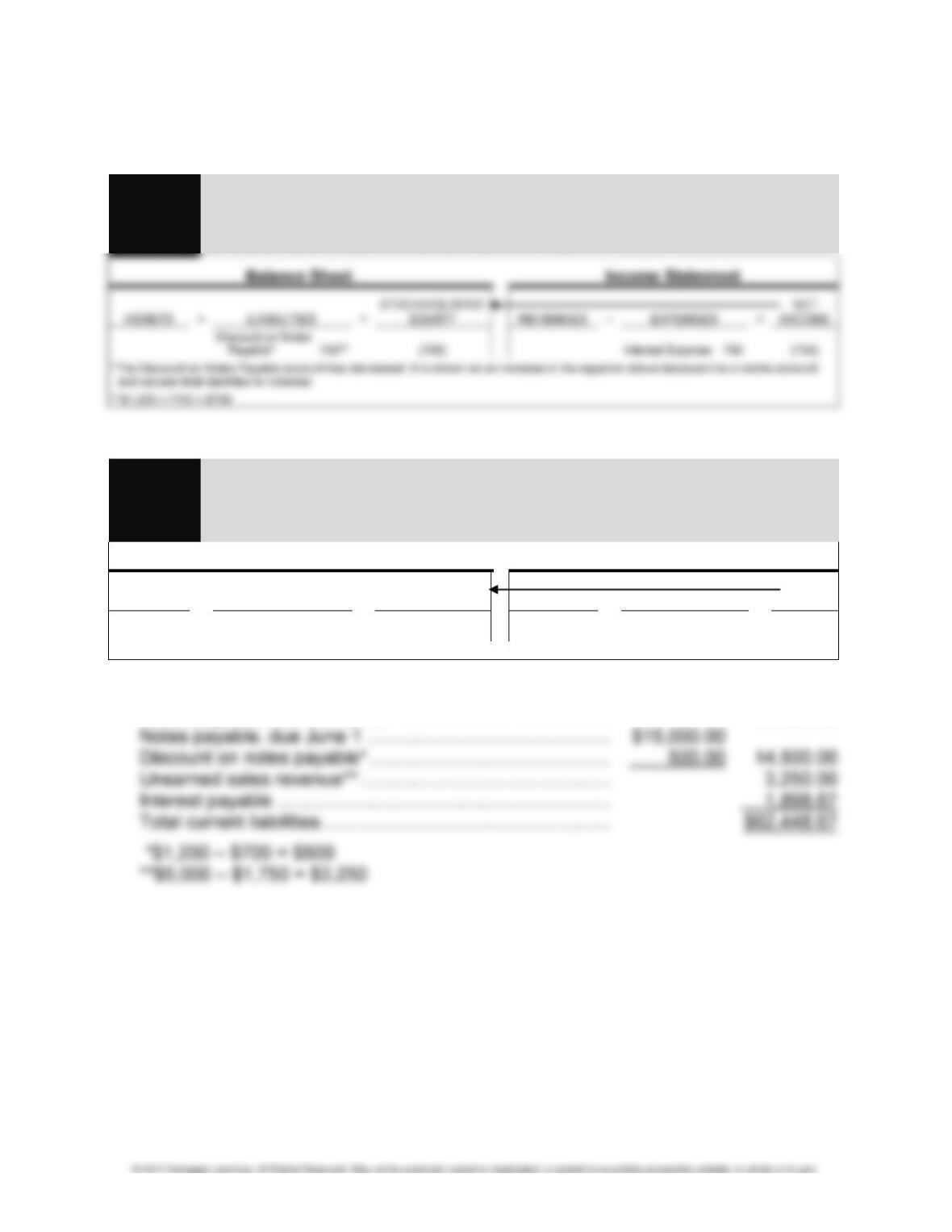

3. Sales tax payable …………………………………………………….. $ 7,200.00

Notes payable, due November 1 ……………………………….. 35,600.00

CHAPTER 9 • CURRENT LIABILITIES, CONTINGENCIES, AND THE TIME VALUE OF MONEY 9-9

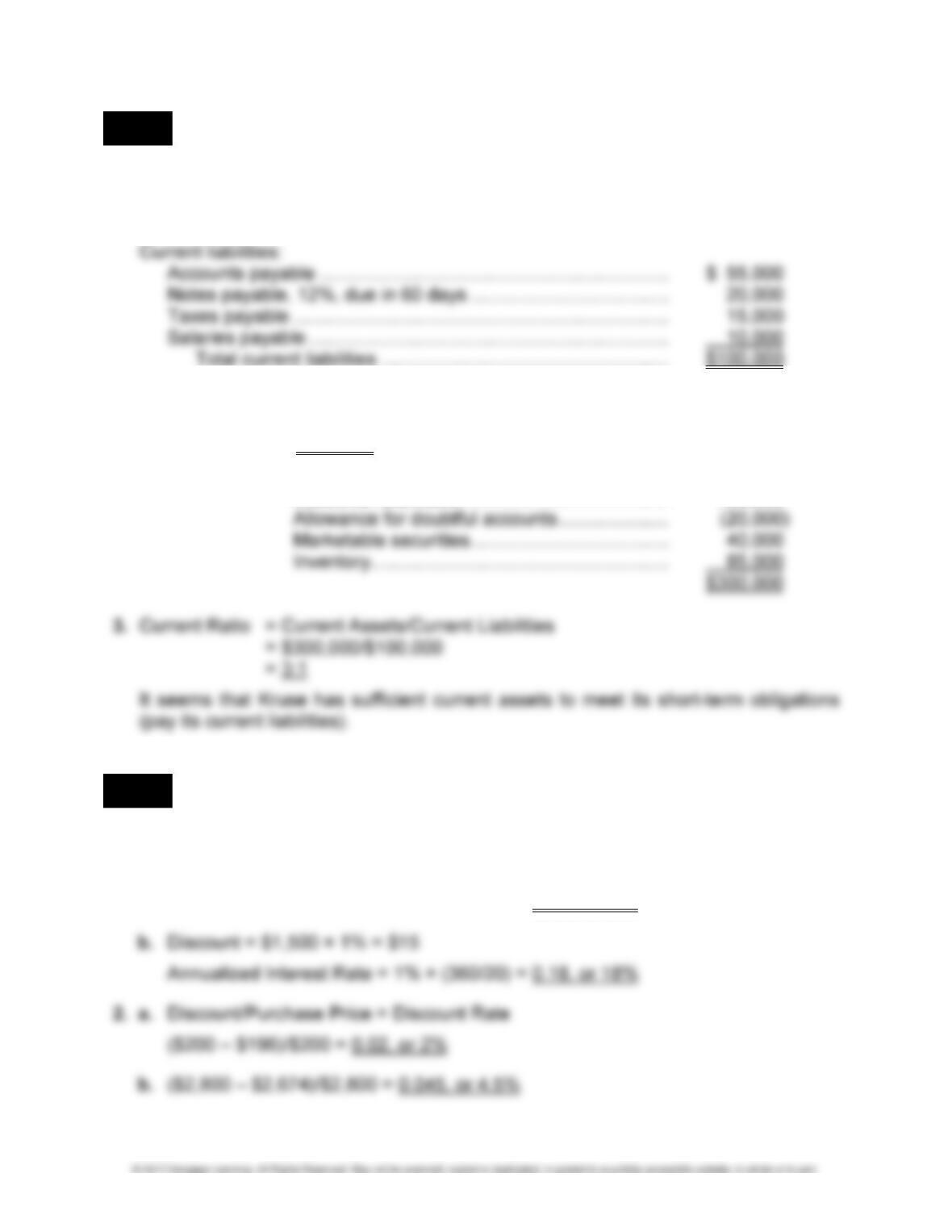

LO 2 EXERCISE 9-5 CURRENT LIABILITIES AND RATIOS

1. KRUSE

BALANCE SHEET

DECEMBER 31, 2016

2. Working Capital = Current Assets – Current Liabilities

= $300,000* – $100,000

= $200,000

*Current Assets = Cash ……………………………………………………… $ 15,000

Accounts receivable ………………………………… 180,000

LO 2 EXERCISE 9-6 DISCOUNTS

1. a. Purchase Price × Discount Rate = Discount

$450 × 2% = $9.00

Annualized Interest Rate = 2% × (360/30) = 0.24, or 24%

9-10 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 2 EXERCISE 9-7 NOTES PAYABLE AND INTEREST

1.

2.

Journal Dec. 31 Interest Expense ……………………………… 1,000

Entry Interest Payable ………………………….. 1,000

Analysis To record interest accrued on loan.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Interest Payable 1,000* (1,000)

Interest

Expense 1,000 (1,000)

*$25,000 × 8% × 6/12 = $1,000

3.

CHAPTER 9 • CURRENT LIABILITIES, CONTINGENCIES, AND THE TIME VALUE OF MONEY 9-11

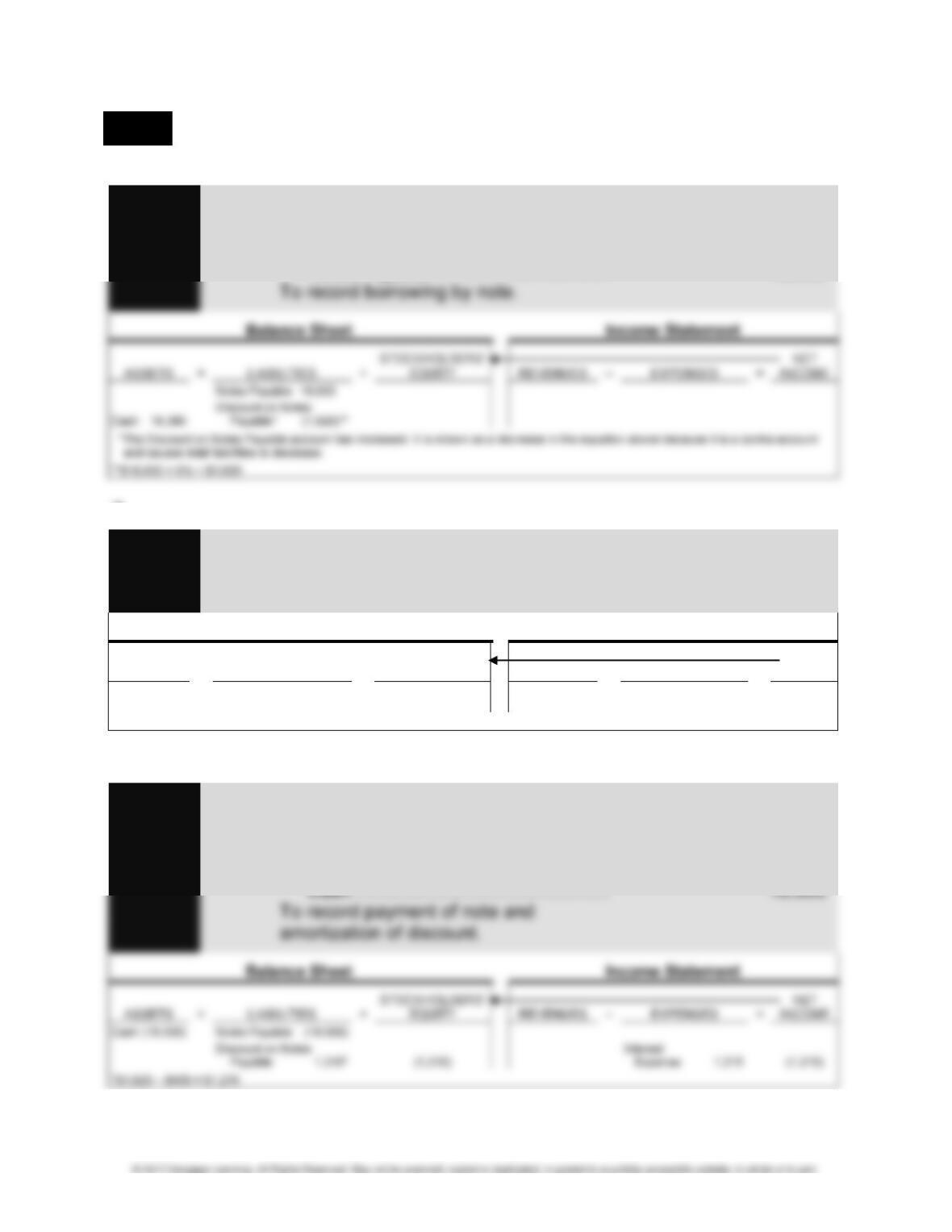

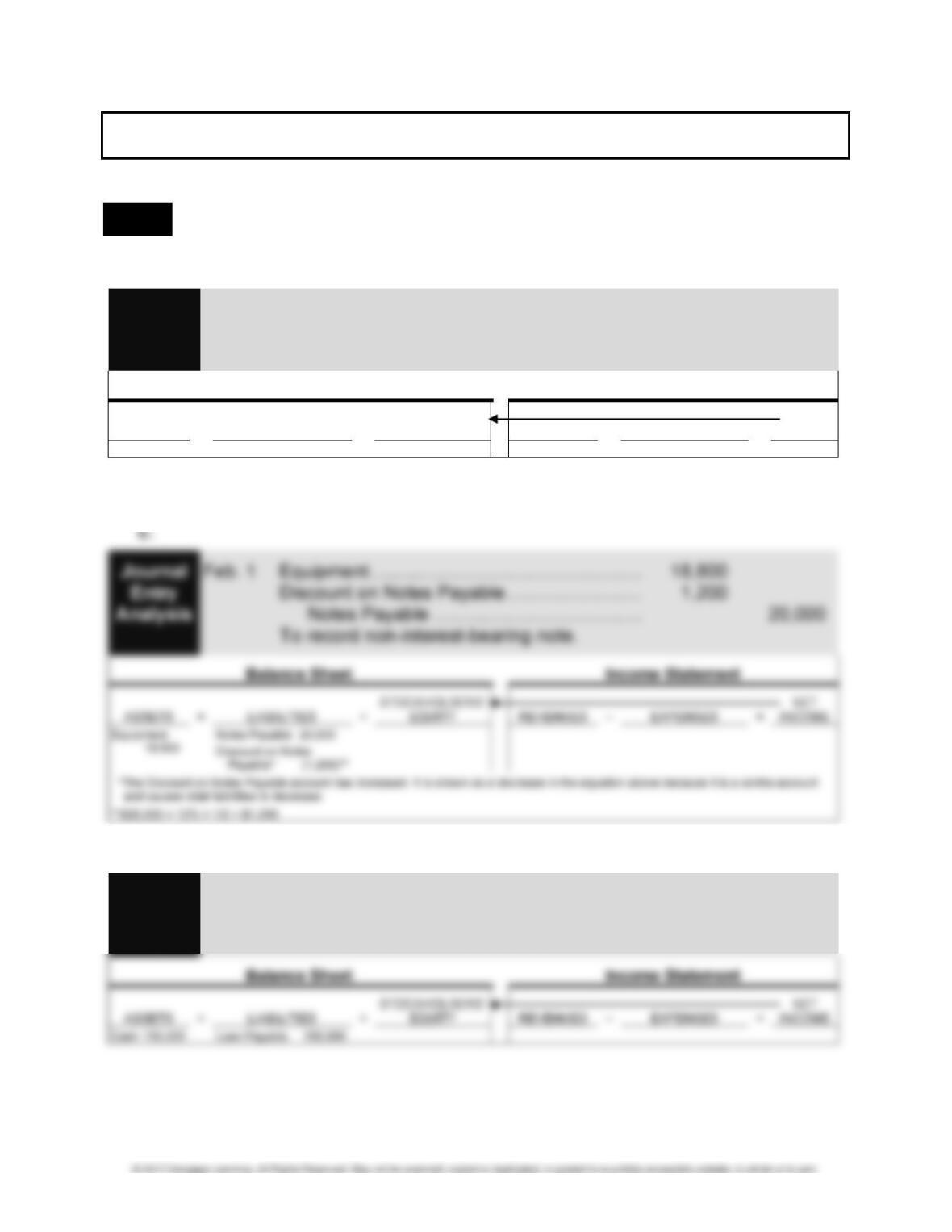

LO 2 EXERCISE 9-8 NON-INTEREST-BEARING NOTES PAYABLE

1.

Journal 2016

Entry Oct. 1 Cash ………………………………………………. 16,380

Analysis Discount on Notes Payable ……………….. 1,620

Notes Payable ……………………………. 18,000

2.

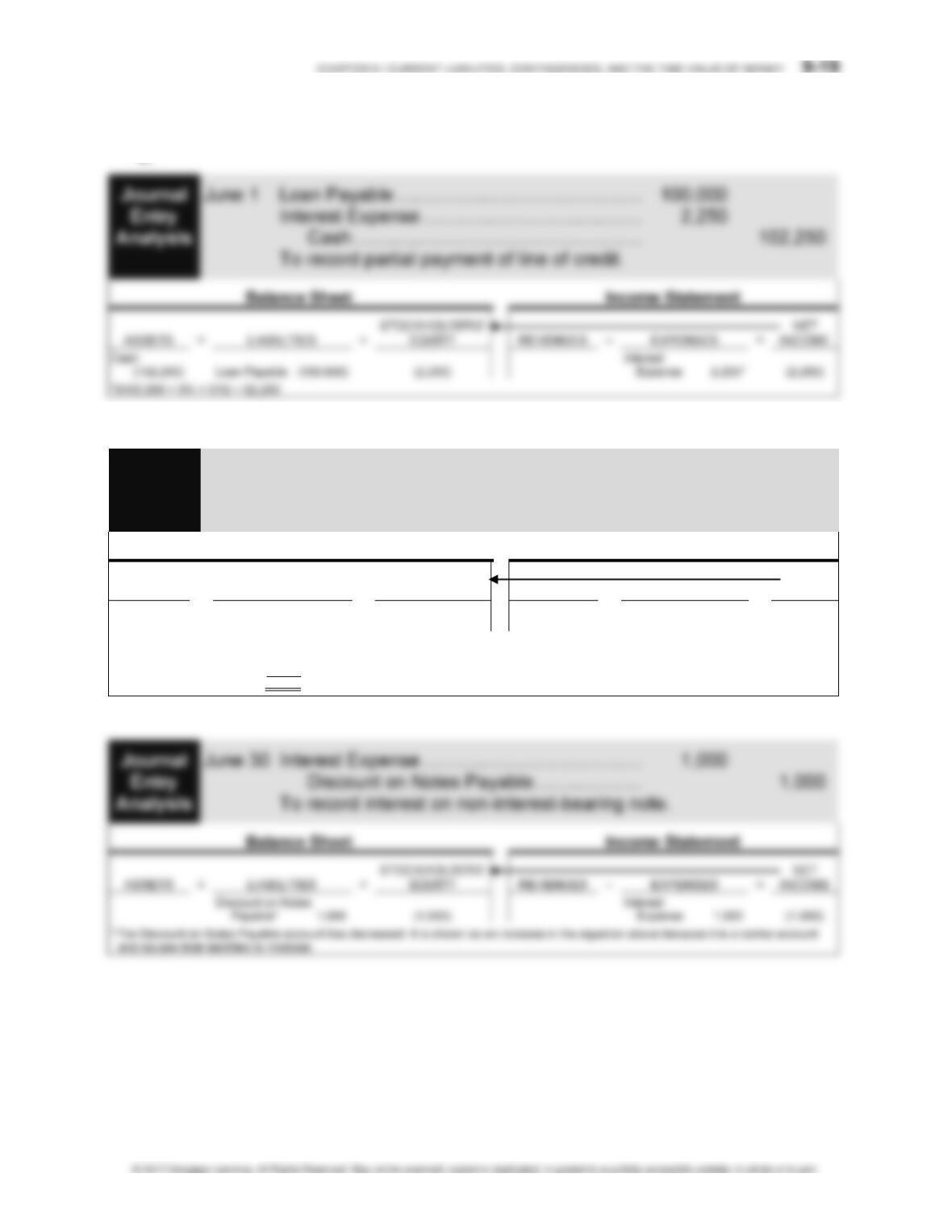

Journal Dec. 31 Interest Expense …………………………………… 405

Entry Discount on Notes Payable………………… 405

Analysis To record accrued interest on note.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Discount on Notes

Payable 405*

(405) Interest Expense 405 (405)

*$1,620 × 3/12 = $405

3.

Journal 2017

Entry Oct. 1 Interest Expense ……………………………… 1,215

Analysis Notes Payable …………………………………. 18,000

Discount on Notes Payable…………… 1,215

9-12 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISE 9-8 (Concluded)

4. Effective interest rate = $1,620/$16,380 = 9.89%

LO 3 EXERCISE 9-9 IMPACT OF TRANSACTIONS INVOLVING CURRENT LIABILITIES

ON STATEMENT OF CASH FLOWS

Accounts payable: O

Current maturities of long-term debt: F

LO 3 EXERCISE 9-10 IMPACT OF TRANSACTIONS INVOLVING CONTINGENT

LIABILITIES ON STATEMENT OF CASH FLOWS

Estimated liability for warranties: O

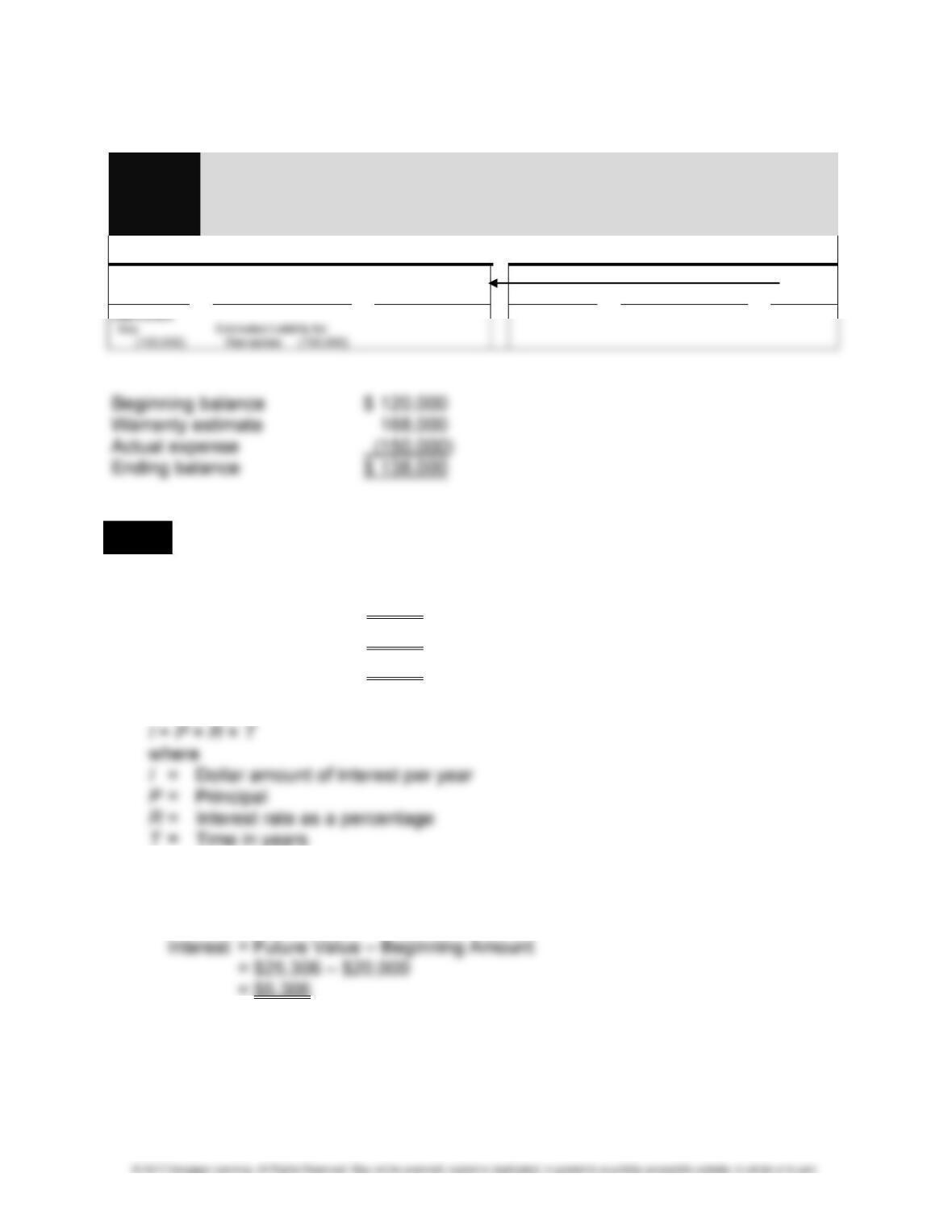

LO 4 EXERCISE 9-11 WARRANTIES

Journal Cash/Accounts Receivable ………………………… 32,500,000

Entry Sales ………………………………………………… 32,500,000

Analysis To record sales of dishwashers.

Balance Sheet Income Statement

Journal Warranty Expense ………………………………………… 168,000

Entry Estimated Liability for Warranties ………………. 168,000

Analysis To record current year’s estimated expense.

Balance Sheet Income Statement

CHAPTER 9 • CURRENT LIABILITIES, CONTINGENCIES, AND THE TIME VALUE OF MONEY 9-13

EXERCISE 9-11 (Concluded)

Journal Estimated Liability for Warranties ………………….. 150,000

Entry Cash/Inventory ……………………………………… 150,000

Analysis To record actual expenditures for warranty work.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

LO 5 EXERCISE 9-12 SIMPLE VERSUS COMPOUND INTEREST

Part 1.

1. *$20,000 × 4% × 6 years = $4,800

2. *$20,000 × 6% × 4 years = $4,800

3. *$20,000 × 8% × 3 years = $4,800

*Formula for Simple Interest Calculation:

Part 2.

1. Table 9-1 n = 6, i = 4%

Future Value = $20,000 × 1.26532 = $25,306

9-14 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISE 9-12 (Concluded)

2. Table 9-1 n = 4, i = 6%

Future Value = $20,000 × 1.26248 = $25,250

3. Table 9-1 n = 3, i = 8%

Part 3.

1. Table 9-1 n = 12, i = 2%

Future Value = $20,000 × 1.26824 = $25,365

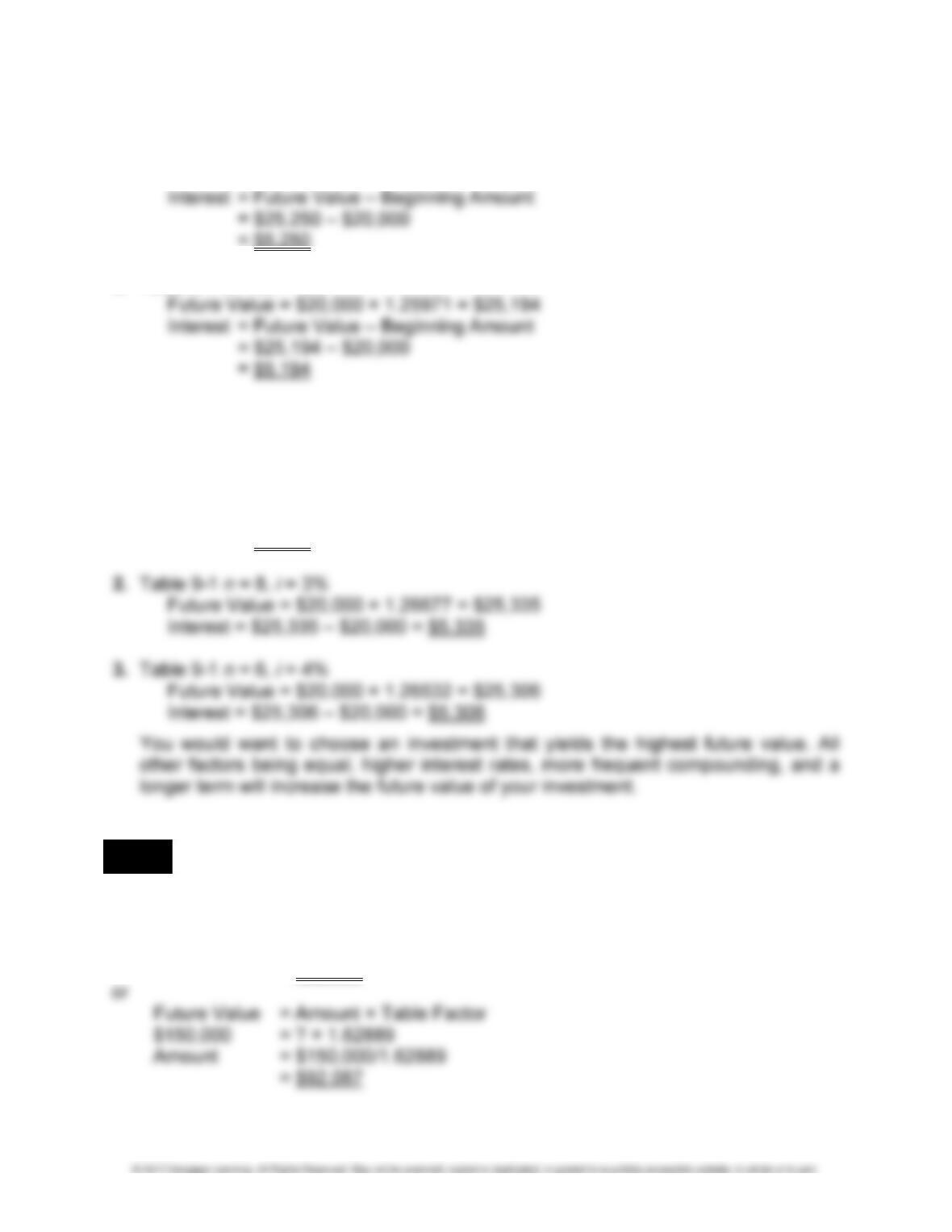

Interest = Future Value – Beginning Amount

= $25,365 – $20,000

= $5,365

LO 6 EXERCISE 9-13 PRESENT VALUE AND FUTURE VALUE

n = 10, i = 5%

Present Value = Amount × Table Factor

= $150,000 × 0.61391

= $92,087

CHAPTER 9 • CURRENT LIABILITIES, CONTINGENCIES, AND THE TIME VALUE OF MONEY 9-15

LO 6 EXERCISE 9-14 EFFECT OF COMPOUNDING PERIOD

1. $1,000 × 1.16640 = $1,166 n = 2, i = 8%

LO 6 EXERCISE 9-15 PRESENT VALUE AND FUTURE VALUE

1. a. $7,000 × 1.46933 = $10,285 n = 5, i = 8%

b. $7,000 × 1.48024 = $10,362 n = 10, i = 4%

c. $7,000 × 1.48595 = $10,402 n = 20, i = 2%

LO 6 EXERCISE 9-16 PRESENT VALUE AND FUTURE VALUE

1. a. $16,000 × 1.46933 = $23,509 n = 5, i = 8%

2. a. $20,000 × 0.68058 = $13,612 n = 5, i = 8%

LO 6 EXERCISE 9-17 ANNUITY

$2,000 × 20.02359 = $40,047 n = 15, i = 4%

9-16 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 7 EXERCISE 9-18 CALCULATION OF YEARS

LO 7 EXERCISE 9-19 VALUE OF PAYMENTS

1. Present Value = Payment × Table Factor

2. n = 8, i = 3%

Present Value = Payment × Table Factor

$2,501.27 = Payment × 7.01969

Payment = $2,501.27/7.01969 = $356.32

With annual payments:

CHAPTER 9 • CURRENT LIABILITIES, CONTINGENCIES, AND THE TIME VALUE OF MONEY 9-17

MULTI-CONCEPT EXERCISES

LO 6,7 EXERCISE 9-20 COMPARISON OF ALTERNATIVES

Present value of 1: $100,000 × 1.00000 = $100,000

Present value of 2: $108,000 × 0.92593 = $100,000

n = 1, i = 8%

LO 6,7 EXERCISE 9-21 TWO SITUATIONS

1. $53,300/$13,000 = 4.100 table factor for present value of an annuity for 5 years,

i = 7%

9-18 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEMS

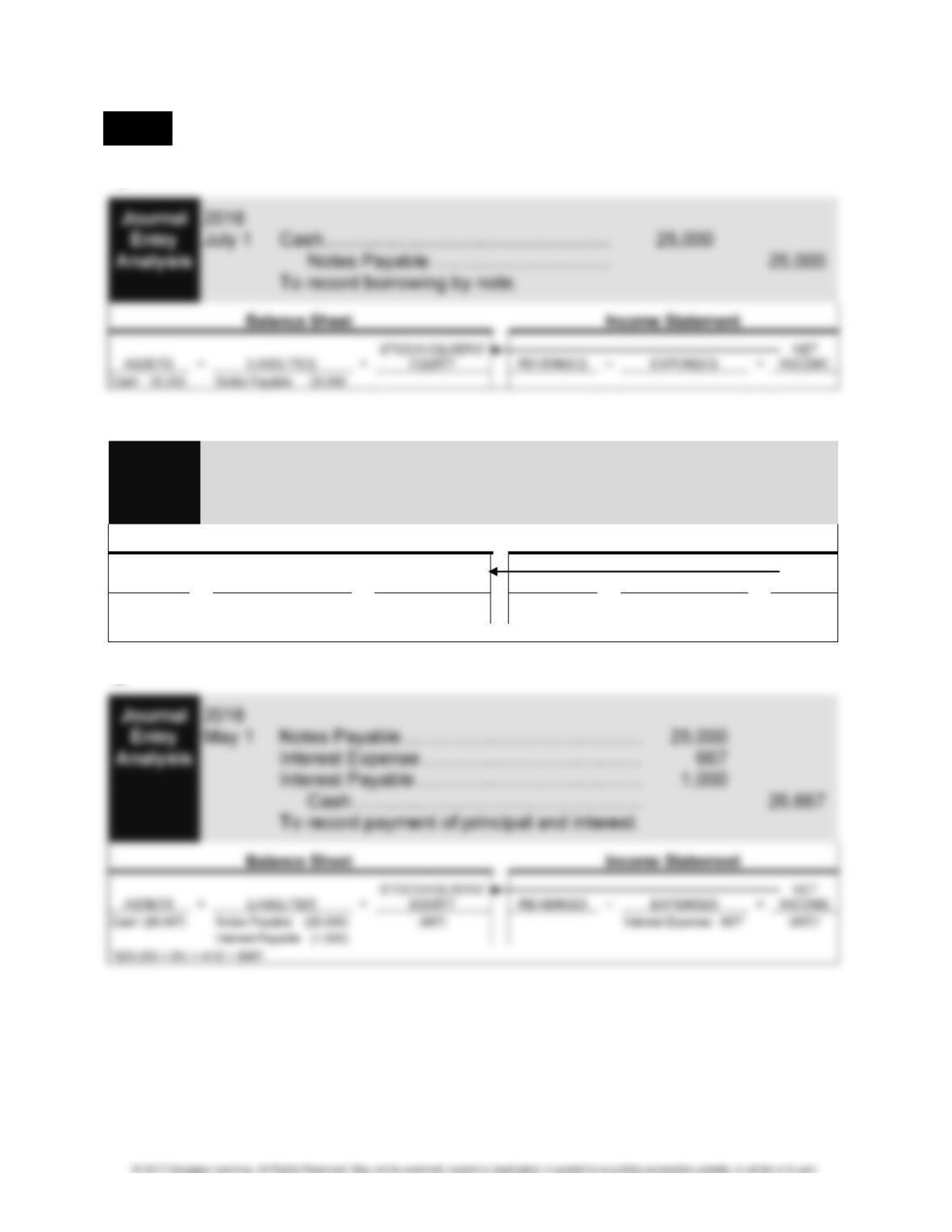

LO 2 PROBLEM 9-1 NOTES AND INTEREST

1. a.

Journal Jan. 1 Cash ……………………………………………………. 25,000

Entry Notes Payable …………………………………. 25,000

Analysis To record loan at 10% interest.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash 25,000 Notes Payable 25,000

b. On January 10, only a memorandum entry is made.

d.

Journal Mar. 1 Cash ……………………………………………………. 150,000

Entry Loan Payable …………………………………… 150,000

Analysis To record loan with line of credit.

PROBLEM 9-1 (Continued)

e.

f.

Journal June 30 Interest Expense …………………………………… 2,750

Entry Interest Payable ……………………………….. 2,750

Analysis To record interest on interest-bearing loan.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Interest Payable 2,750 (2,750)

Interest

Expense 2,750* (2,750)

*Interest-bearing:

$25,000 × 10% × 6/12 $1,250

$50,000 × 9% × 4/12 1,500

Subtotal $2,750

9-20 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 9-1 (Continued)

g.

h.

Journal Sept. 1 Cash ……………………………………………………. 200,000

Entry Notes Payable …………………………………. 200,000

Analysis To record loan from line of credit.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash 200,000 Notes Payable 200,000

i.

Journal Nov. 1 Accounts Payable …………………………………. 12,000

Entry Notes Payable …………………………………. 12,000

Analysis To record loan in repayment of account.