CHAPTER 9 • CURRENT LIABILITIES, CONTINGENCIES, AND THE TIME VALUE OF MONEY 9-21

PROBLEM 9-1 (Concluded)

j.

Journal Dec. 31 Notes Payable ………………………………………. 25,000

Entry Interest Payable ……………………………………. 1,250

Analysis Interest Expense …………………………………… 1,250

2. Line of credit:

$50,000 × 9% × 10/12 …………………………………………………… $3,750

$200,000 × 9% × 4/12 …………………………………………………… 6,000

LO 3 PROBLEM 9-2 EFFECTS OF BURGER KING’S CURRENT LIABILITIES ON ITS

STATEMENT OF CASH FLOWS

1. Adjustments to reconcile net income to net cash provided by operating activities:

Net income ……………………………………………………………………….. $ xxx

Adjustments to reconcile net income to net

2. Burger King must have access to cash or other assets that can be converted to

cash, in amounts sufficient to pay its current liabilities. Burger King’s current ratio

would be useful in assessing its liquidity. However, Burger King would be expected

to have some amount of inventory on hand. Therefore, its quick ratio would be a

more conservative measure of its ability to pay its bills on time.

9-22 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 3 PROBLEM 9-3 EFFECTS OF BRINKER INTERNATIONAL’S CURRENT LIABILITIES

ON ITS STATEMENT OF CASH FLOWS

1. Operating Activities section of cash-flow statement:

Net income ………………………………………………………………….. $xxx,xxx

Adjustments to reconcile net income to net

2. Changes in the balance of current liability accounts should be reflected in the Oper-

ating Activities category of the statement of cash flows. An increase in a current lia-

bility account indicates that the company increased its cash position by incurring a

LO 4 PROBLEM 9-4 WARRANTIES

1. XX defective units × $150 per unit = $12,600

XX defective units = $12,600/$150 per unit

Defective units = 84

3. If the actual amount of warranty costs incurred during 2017 is significantly higher

than the estimated liability recorded for warranty costs at the end of 2016, Clearview

CHAPTER 9 • CURRENT LIABILITIES, CONTINGENCIES, AND THE TIME VALUE OF MONEY 9-23

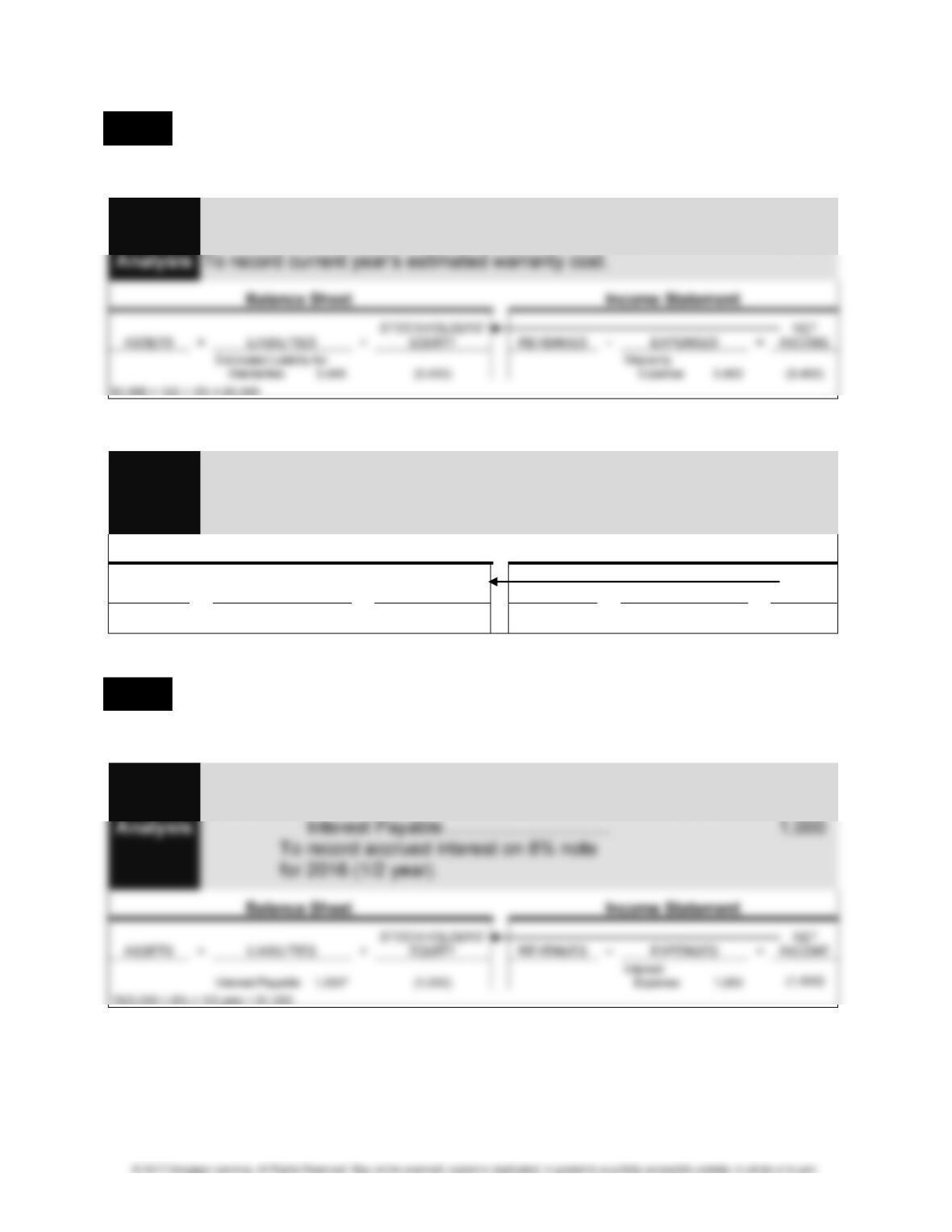

LO 4 PROBLEM 9-5 WARRANTIES

1.

Journal Warranty Expense ……………………………………………… 5,400

Entry Estimated Liability for Warranties ……………………. 5,400

2.

Journal Estimated Liability for Warranties …………………………. 4,950

Entry Inventory …………………………………………………….. 4,950

Analysis To record actual warranty repairs.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Inven-

tory (4,950)

Estimated Liability for

Warranties (4,950)

LO 5 PROBLEM 9-6 COMPARISON OF SIMPLE AND COMPOUND INTEREST

1.

Journal 2016

Entry Dec. 31 Interest Expense ……………………………… 1,000

9-24 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

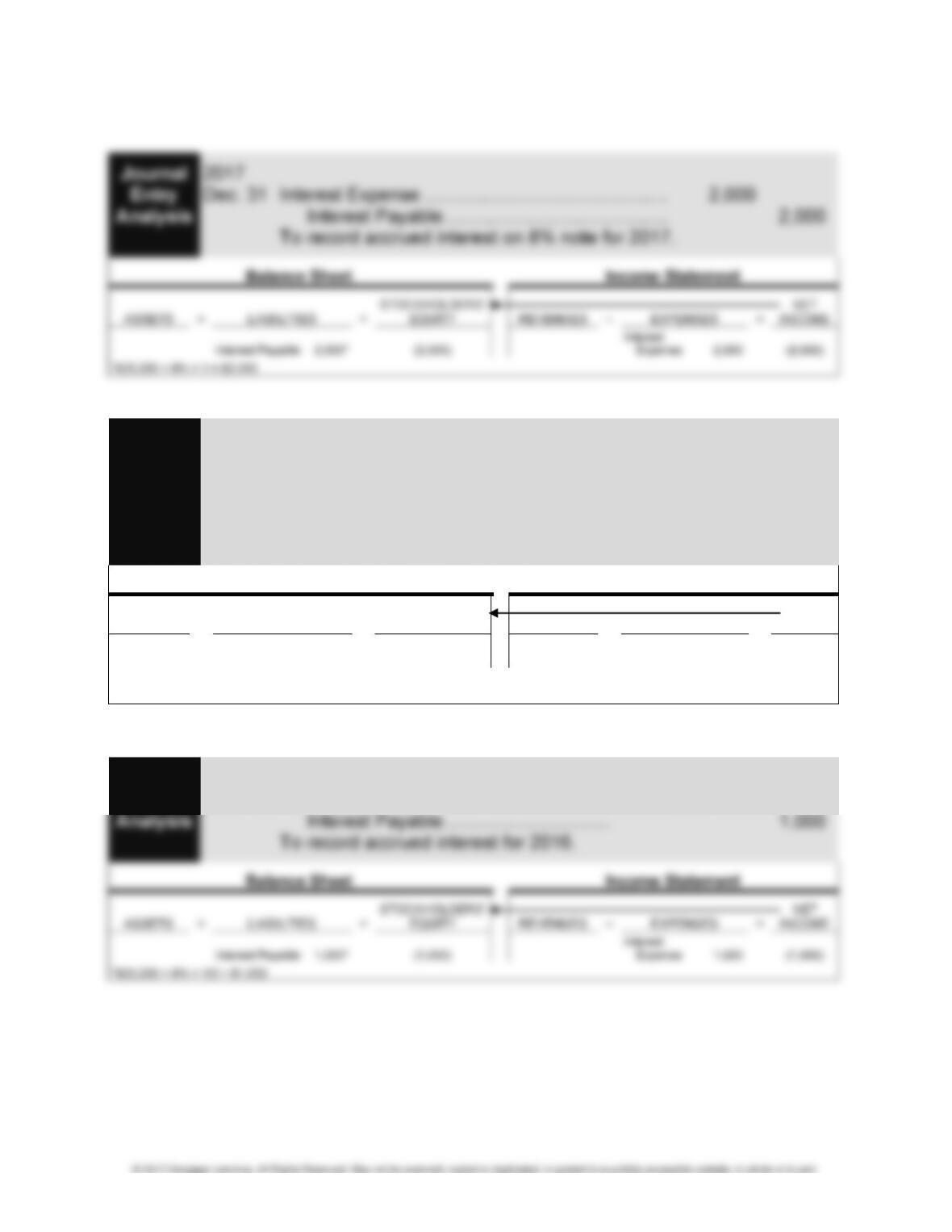

PROBLEM 9-6 (Continued)

Journal 2018

Entry June 30 Interest Expense ……………………………… 1,000

Analysis Interest Payable ………………………………. 3,000

Notes Payable …………………………………. 25,000

Cash …………………………………………. 29,000

To record repayment of note plus interest.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash (29,000)

Notes Payable (25,000)

Interest Payable (3,000)* (1,000)

Interest

Expense 1,000**

(1,000)

*$1,000 + $2,000 = $3,000

**$25,000 × 8% × 1/2 = $1,000

2.

Journal 2016

Entry Dec. 31 Interest Expense ……………………………… 1,000

CHAPTER 9 • CURRENT LIABILITIES, CONTINGENCIES, AND THE TIME VALUE OF MONEY 9-25

PROBLEM 9-6 (Concluded)

Journal 2017

Entry Dec. 31 Interest Expense ……………………………… 2,122

Analysis Interest Payable ………………………….. 2,122

To record accrued interest for 2017.

Balance Sheet Income Statement

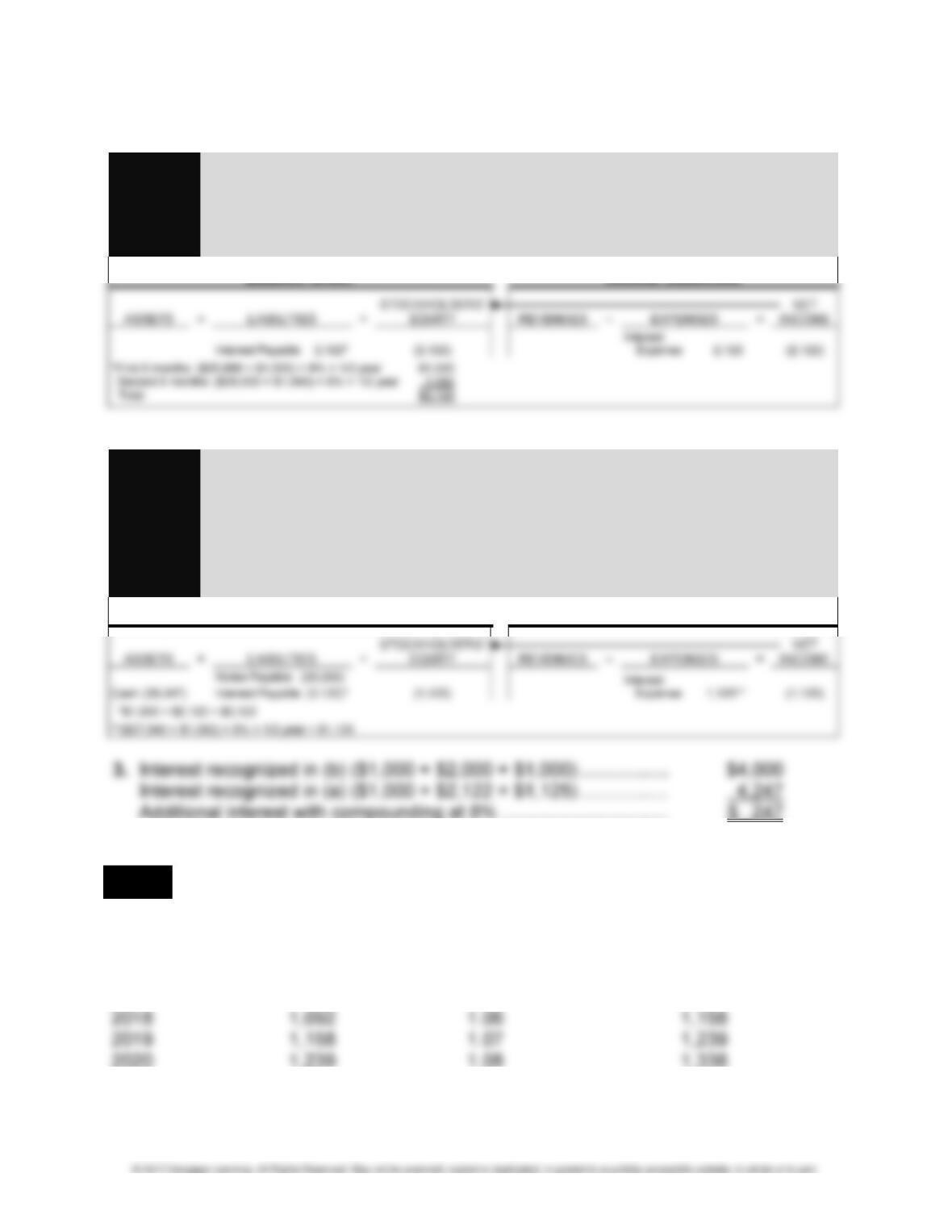

Journal 2018

Entry June 30 Interest Expense ……………………………… 1,125

Analysis Interest Payable ………………………………. 3,122

Notes Payable …………………………………. 25,000

Cash …………………………………………. 29,247

To record repayment of note plus interest.

Balance Sheet Income Statement

LO 6 PROBLEM 9-7 INVESTMENT WITH VARYING INTEREST RATE

Principal at Interest Accumulated

Year Beginning of Year Factor at End of Period

2016 $1,000 1.04 $1,040

2017 1,040 1.05 1,092

9-26 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

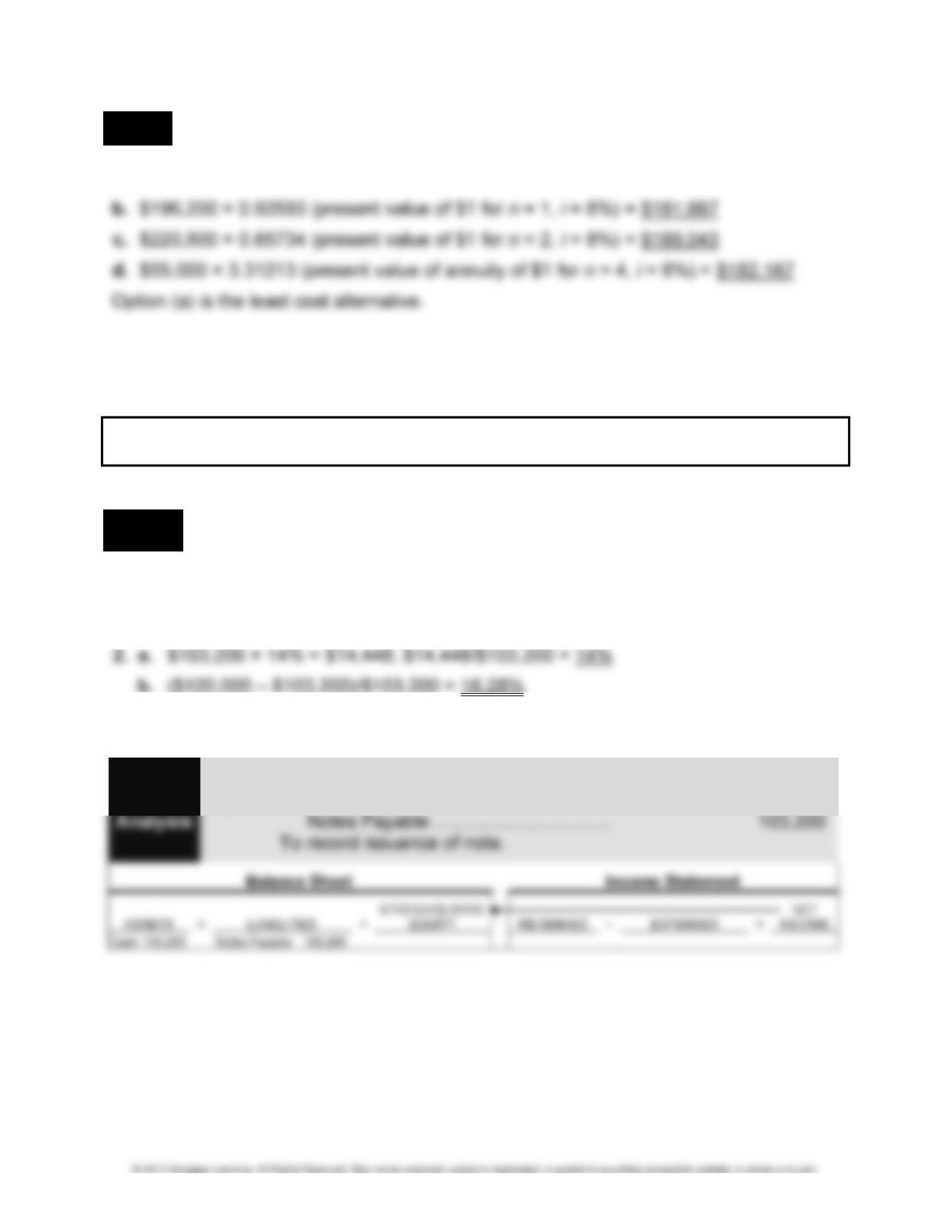

LO 6 PROBLEM 9-8 COMPARISON OF ALTERNATIVES

a. $180,000 × 1.0 = $180,000

MULTI-CONCEPT PROBLEMS

LO 2,5 PROBLEM 9-9 INTEREST IN ADVANCE VERSUS INTEREST PAID WHEN LOAN IS

DUE

1. a. $103,200

b. $103,200/(100% – 14%) = $120,000

3. a.

Journal 2016

Entry July 1 Cash ………………………………………………. 103,200

CHAPTER 9 • CURRENT LIABILITIES, CONTINGENCIES, AND THE TIME VALUE OF MONEY 9-27

PROBLEM 9-9 (Continued)

Journal Dec. 31 Interest Expense …………………………………… 7,224

Entry Interest Payable ……………………………….. 7,224

Analysis To record the accrual of interest.

Balance Sheet Income Statement

Journal 2017

Entry July 1 Notes Payable ………………………………………. 103,200

Analysis Interest Expense …………………………………… 7,224

Interest Payable ……………………………………. 7,224

Cash ………………………………………………. 117,648

To record payment of interest and principal.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash

(117,648)

Notes

Payable (103,200)

Interest Payable (7,224) (7,224)

Interest

Expense 7,224

(7,224)

b.

9-28 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 9-9 (Concluded)

Journal Dec. 31 Interest Expense …………………………………… 8,400

Entry Discount on Notes Payable………………… 8,400

Analysis To record interest for the year.

Journal 2017

Entry July 1 Interest Expense ……………………………… 8,400

Analysis Notes Payable …………………………………. 120,000

Discount on Notes Payable…………… 8,400

Cash …………………………………………. 120,000

To record payment of the note.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

$103,200

LO 1,4 PROBLEM 9-10 CONTINGENT LIABILITIES

1. Items (a), (d), (e): The liability is probable, and an estimate is available.

CHAPTER 9 • CURRENT LIABILITIES, CONTINGENCIES, AND THE TIME VALUE OF MONEY 9-29

LO 6,7 PROBLEM 9-11 TIME VALUE OF MONEY CONCEPT

1. $9,750 × 6.86604 (future value of $1 for n = 17, i = 12%) = $66,944

LO 6,7 PROBLEM 9-12 COMPARISON OF ALTERNATIVES

a. $15,000 × 1.36049 (future value of $1 for n = 4, i = 8%) = $20,407

9-30 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

ALTERNATE PROBLEMS

LO 2 PROBLEM 9-1A NOTES AND INTEREST

1. a.

Journal Jan. 1 Cash ……………………………………………………. 35,000

Entry Notes Payable …………………………………. 35,000

Analysis To record issuance of note.

Balance Sheet Income Statement

c.

Journal Feb. 1 Equipment ……………………………………………. 26,320

Entry Discount on Notes Payable …………………….. 1,680

Analysis Notes Payable …………………………………. 28,000

To record non-interest-bearing note.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Equip-

ment 26,320

Notes Payable 28,000

Discount on Notes

CHAPTER 9 • CURRENT LIABILITIES, CONTINGENCIES, AND THE TIME VALUE OF MONEY 9-31

PROBLEM 9-1A (Continued)

e.

Journal June 1 Loan Payable ……………………………………….. 140,000

Entry Interest Expense …………………………………… 3,150

Analysis Cash ………………………………………………. 143,150

To record partial payment of line of credit.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash

(143,150) Loan Payable (140,000) (3,150)

Interest

Expense 3,150* (3,150)

*$140,000 × 9% × 3/12 = $3,150

Journal June 30 Interest Expense …………………………………… 1,400

Entry Discount on Notes Payable………………… 1,400

Analysis To record accrued interest on

non-interest-bearing note.

Balance Sheet Income Statement

9-32 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 9-1A (Continued)

g.

Journal Aug. 1 Notes Payable ………………………………………. 28,000

Entry Interest Expense …………………………………… 280

Analysis Cash ………………………………………………. 28,000

Discount on Notes Payable………………… 280

Repaid non-interest-bearing note.

Balance Sheet Income Statement

h.

Journal Sept. 1 Cash ……………………………………………………. 280,000

Entry Notes Payable …………………………………. 280,000

Analysis Borrowed on line of credit.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash 280,000 Notes Payable 280,000

i.