SOLUTION

Date

Accounts and Explanation

Debit

Credit

Jan. 1

Office Equipment

112,000

Cash

78,000

Note Payable

34,000

To record purchase of office equipment.

Land

307,500

Communication Equipment

102,500

Cash

410,000

To record purchase of land and comm. equipment.

Depreciation Expense—Building

Accumulated Depreciation—Building

To record depreciation on building.

Cash

360,000

Accumulated Depreciation—Building

248,000

Building

540,000

Gain on Disposal

68,000

To record sale of building.

Depreciation Expense—Communication Equipment

Accumulated Depreciation—Comm. Equipment

15,375

To record depreciation on communication equipment.

Depreciation Expense—Office Equipment

Accumulated Depreciation—Office Equipment

44,800

To record depreciation on office equipment.

Calculations:

Apr. 1 – Acquisition of land and communication equipment:

Asset

Market

Value

Percentage of Total Value

× Total

Purchase

Price

= Assigned

Cost of

Each Asset

P9-38B, cont.

Sep. 1 – Sale of building

Straight-line depreciation

=

(Cost − Residual value) / Useful life × (Number of Months / 12)

=

($540,000 ̶ $60,000) / 40 years × 8/12

=

$8,000 per partial year (2016)

Market value of assets received

Less: Book value of asset disposed of

Cost

$ 540,000

Less: Accumulated Depreciation ($240,000 + $8,000)

Gain or (Loss)

$ 68,000

Straight-line depreciation

=

(Cost − Residual value) / Useful life × (Number of Months / 12)

=

=

$15,375 per partial year (2016)

Double-declining-balance depreciation

(Cost – Accumulated depreciation) × 2 × (1 / Useful life)

$44,800 in 2016

P9-39B Accounting for natural resources

Learning Objective 4

Dep. Exp. $2,261,000

Gandy Oil Incorporated has an account titled Oil and Gas Properties. Gandy paid $6,100,000 for oil

reserves holding an estimated 300,000 barrels of oil. Assume the company paid $560,000 for additional

geological tests of the property and $480,000 to prepare for drilling. During the first year, Gandy

removed and sold 95,000 barrels of oil. Record all of Gandy’s transactions, including depletion for the

first year.

SOLUTION

Purchase price of oil reserves

$ 6,100,000

Add related costs:

Geological tests

Drilling preparation

Total cost of oil reserves

$ 7,140,000

Depletion per unit

(Cost – Residual value) / Estimated total units

$23.80 per barrel

Depletion expense

Depletion per unit × Number of units extracted

$23.80 per barrel × 95,000 barrels

$2,261,000

Date

Accounts and Explanation

Debit

Credit

Oil and Gas Properties

6,100,000

Cash

6,100,000

To record purchase of oil reserves.

Oil and Gas Properties

1,040,000

Cash

1,040,000

of oil reserves.

Depletion Expense—Oil and Gas Properties

2,261,000

Accumulated Depletion—Oil and Gas Properties

2,261,000

To record depletion.

P9-40B Accounting for intangibles

Learning Objective 5

1. Goodwill $460,000

Central States Telecom provides communication services in Iowa, Nebraska, the Dakotas, and Montana.

Central States purchased goodwill as part of the acquisition of Shurburn Wireless Company, which had

the following figures:

Requirements

1. Journalize the entry to record Central States’s purchase of Shurburn Wireless for $360,000 cash plus

a $540,000 note payable.

2. What special asset does Central States’s acquisition of Shurburn Wireless identify? How should

Central States Telecom account for this asset after acquiring Shurburn Wireless? Explain in detail.

SOLUTION

Requirement 1

Purchase price to acquire Shurburn Wireless ($360,000 + $540,000)

$ 900,000

Goodwill

Requirement 2

The acquisition identifies the asset goodwill.

P9A-41B Journalizing partial-year depreciation and asset disposals and exchanges

Learning Objectives 2, 3, 7

Appendix 9A

Jan. 1 Gain $8,000

During 2016, Dora Company completed the following transactions:

SOLUTION

Date

Accounts and Explanation

Debit

Credit

Jan. 1

Office Equipment (new)

163,000

Accumulated Depreciation—Office Equipment

69,000

Office Equipment (old)

124,000

Cash

100,000

Gain on Disposal

8,000

To record exchange of office equipment.

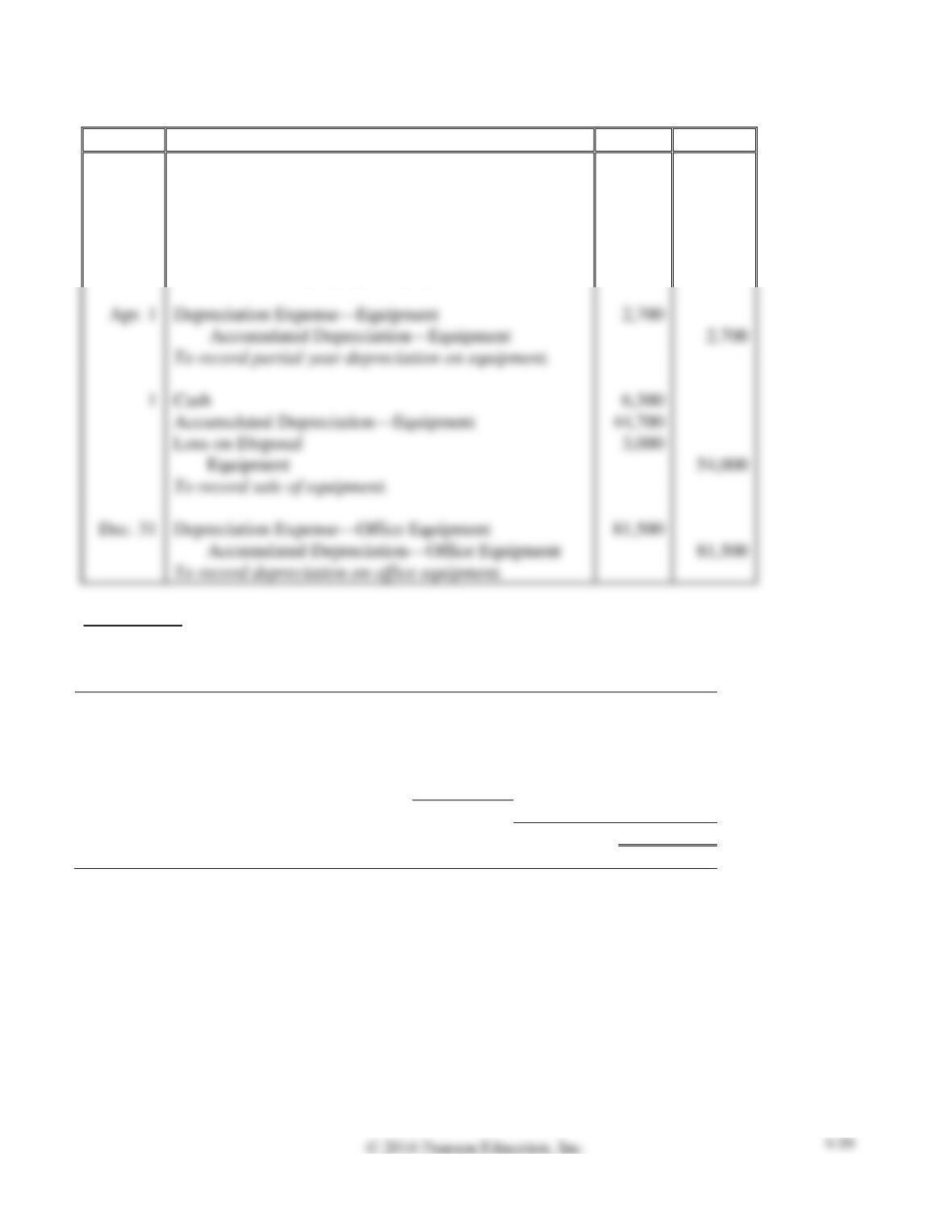

Depreciation Expense—Equipment

2,700

1

Cash

Accumulated Depreciation—Equipment

44,700

Loss on Disposal

Equipment

To record sale of equipment.

Dec. 31

Depreciation Expense—Office Equipment

81,500

Accumulated Depreciation—Office Equipment

To record depreciation on office equipment.

Calculations:

Jan. 1 – Exchange of office equipment

Market value of assets received

$ 163,000

Less:

Book value of asset exchanged

Cost

$ 124,000

Less: Accumulated depreciation

(69,000)

$ 55,000

Cash paid

100,000

155,000

Gain or (Loss)

$ 8,000

P9-41B, cont.

Apr. 1 – Sale of equipment

Straight-line depreciation

=

(Cost − Residual value) / Useful life × (Number of Months / 12)

=

($54,000 ̶ $0) / 5 years × 3/12

=

$2,700 per partial year (2016)

Market value of assets received

Less: Book value of asset disposed of

Cost

$ 54,000

Less: Accumulated Depreciation ($42,000 + $2,700)

Gain or (Loss)

Double-declining-balance depreciation

=

(Cost – Accumulated depreciation) × 2 × (1 / Useful life)

=

($163,000 – $0) × 2 × (1/4 years)

=

$81,500

Continuing Problem

P9-42 Calculating and journalizing partial-year depreciation

This problem continues the Daniels Consulting situation from Problem P8-41 of Chapter 8. Assume

Daniels Consulting had purchased a computer, $3,600, and office furniture, $3,000, on December 3 and

4, 2016, respectively, and that they were expected to last five years. Assume that both assets have a

residual value of $0.

Requirements

1. Calculate the amount of depreciation expense for each asset for the year ended December 31, 2016,

assuming the computer is depreciated using the straight-line method and the office furniture is

depreciated using the double-declining-balance method.

2. Record the entry for the one month’s depreciation.

SOLUTION

Requirement 1

Depreciation on computer

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Dec. 31

Depreciation Expense—Computer

60

Depreciation Expense—Office Furniture

Critical Thinking

Ethical Issue 9-1

Western Bank & Trust purchased land and a building for the lump sum of $3,000,000. To get the

maximum tax deduction, Western allocated 90% of the purchase price to the building and only 10% to

the land. A more realistic allocation would have been 70% to the building and 30% to the land.

Requirements

1. Explain the tax advantage of allocating too much to the building and too little to the land.

2. Was Western’s allocation ethical? If so, state why. If not, why not? Identify who was harmed.

SOLUTION

Requirement 1

The taxpayer wants to allocate as much of the purchase price as possible to the building because tax law

Requirement 2

Whether the taxpayer’s choice was ethical or unethical is a difficult call. If the taxpayer is deliberately

Fraud Case 9-1

Jim Reed manages a fleet of utility trucks for a rural county government. He’s been in his job for 30

years, and he knows where the angles are. He makes sure that when new trucks are purchased, the

residual value is set as low as possible. Then, when they become fully depreciated, they are sold off by

the county at residual value. Jim makes sure his buddies in the construction business are first in line for

the bargain sales, and they make sure he gets a little something back. Recently, a new county

commissioner was elected with vows to cut expenses for the taxpayers. Unlike other commissioners, this

man has a business degree, and he is coming to visit Jim tomorrow.

Requirements

1. When a business sells a fully depreciated asset for its residual value, is a gain or loss recognized?

2. How do businesses determine what residual values to use for their various assets? Are there “hard

and fast” rules for residual values?

3. How would an organization prevent the kind of fraud depicted here?

SOLUTION

Requirement 1

Requirement 2

Requirement 3

An organization could arrange for public auction of surplus vehicles, which would allow the public to

Financial Statement Case 9-1

Requirements

1. Which depreciation method does Starbucks Corporation use for reporting in the financial

statements? What type of depreciation method does the company probably use for income tax

purposes?

2. What was the amount of depreciation and amortization expense for the year ending September 29,

2013? (Hint: Review the Statement of Cash Flows.)

3. The statement of cash flows reports the cash purchases of property, plant, and equipment. How much

were Starbucks’s additions to property, plant, and equipment during the year ending 2013? Did

Starbucks record any proceeds from the sale of property, plant, and equipment?

4. What was the amount of accumulated depreciation at September 29, 2013? What was the net book

value of property, plant, and equipment for Starbucks as of September 29, 2013?

5. Compute Starbucks’s asset turnover ratio for year ending September 29, 2013. How does

Starbucks’s ratio compare with that of Green Mountain Coffee Roasters, Inc.?

SOLUTION

Requirement 1

Depreciation of property, plant, and equipment, which includes assets under capital leases, is provided

Requirement 2

Requirement 3

Starbucks’ statement of cash flows for the year ended September 29, 2013 reports a cash outflow of

Requirement 4

Requirement 5

(Amounts in millions)

Communication Activity 9-1

In 150 words or fewer, explain the different methods that can be used to calculate depreciation. Your

explanation should include how to calculate depreciation expense using each method.

SOLUTION

Student answers will vary, but should include the following points: