CHAPTER 9

Plant Assets, Natural Resources,

and Intangible Assets

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

1. Explain the accounting for

plant asset expenditures.

1, 2, 3, 9,

24

1, 2, 3

1

1, 2, 3

1A

2. Apply depreciation methods

to plant assets.

4, 5, 6,

7, 8, 21,

22, 23

4, 5,

6 ,7, 8

2a, 2b

4, 5, 6,

7, 8

2A, 3A,

4A, 5A

10, 11

9, 10

3

9, 10

5A, 6A

12, 13, 14,

15, 16,

17, 18, 19

4

7A, 8A

25, 26

15, 16

15, 16

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Determine acquisition costs of land and building.

Simple

20–30

2A

Compute depreciation under different methods.

Simple

30–40

Compute depreciation under different methods.

4A

Calculate revisions to depreciation expense.

20–30

purchase, sale, retirement, and depreciation.

6A

Record disposals.

Simple

30–40

assets section.

amortizing intangible assets.

9A

Calculate and comment on asset turnover.

WEYGANDT FINANCIAL ACCOUNTING MANAGERIAL 2E

CHAPTER 9

PLANT ASSETS, NATURAL RESOURCES,

AND INTANGIBLE ASSETS

Number

LO

BT

Difficulty

Time (min.)

BE1

1

AP

Simple

2–4

BE2

1

AP

Simple

1–2

BE9

3

AP

Simple

4–6

BE10

3

AP

Simple

4–6

BE11

4

AP

Simple

4–6

BE12

4

AP

Simple

2–4

BE13

5

AP

Simple

4–6

BE14

5

AP

Simple

2–4

*BE15

6

AP

Simple

4–6

*BE16

6

AP

Simple

4–6

DI1

1

C

Simple

4–6

DI2a

2

AP

Simple

2–4

DI2b

2

AP

Simple

DI3

3

AP

6–8

DI5

5

AP

Simple

2–4

EX1

1

C

Simple

6–8

EX2

1

AP

Simple

4–6

EX3

1

AP

Simple

4–6

EX4

2

C

Simple

4–6

EX5

2

AP

Simple

6–8

EX6

2

AP

Simple

8–10

EX8

2

AN

8–10

BE3

1

AP

Simple

2–4

BE4

2

AP

Simple

2–4

BE5

2

E

4–6

BE6

2

AP

Simple

4–6

BE7

2

AP

Simple

2–4

BE8

2

AN

4–6

PLANT ASSETS, NATURAL RESOURCES, AND INTANGIBLE

ASSETS (Continued)

Number

LO

BT

Difficulty

Time (min.)

EX9

3

AP

Moderate

8–10

EX10

3

AP

Moderate

10–12

EX11

4

AP

Simple

6–8

EX12

4

AP

Simple

4–6

EX13

4

AP

Simple

8–10

EX14

5

AP

Simple

2–4

EX15

6

AP

Moderate

8–10

EX16

6

AP

Moderate

8–10

BYP2

5

AN, E

Simple

10–15

BYP3

5

AN, E

Simple

10–15

BYP4

2

C

Simple

10–15

BYP5

2

AP, E

Moderate

20–25

BYP6

2

C

Simple

5–10

BYP7

2

E

Simple

10–15

BYP8

4

K

Simple

5–10

BYP9

AP

Simple

10–15

P1A

1

C

Simple

20–30

P2A

2

AP

Simple

30–40

P3A

2

AN

Moderate

30–40

P4A

2

AP

Moderate

20–30

P5A

AP

Moderate

40–50

P6A

3

AP

Simple

30–40

P7A

AP

Moderate

30–40

P8A

4

AP

Moderate

30–40

P9A

5

AN

Moderate

5–10

BYP1

AN

Simple

15–20

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Study Objectives and End–of–Chapter Exercises and Problems

Study Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

1. Explain the accounting for plant

asset expenditures.

Q9-1

Q9-2

Q9-3

Q9-9

Q9–24

DI9-1

E9-1

P9–1A

BE9-1

BE9-2

BE9-3

E9-2

E9-3

2. Apply depreciation methods to

plant assets.

Q9-5

Q9-4

Q9-6

Q9-7

Q9-8

Q9–21

Q9–22

Q9–23

E9-4

BE9-4

BE9-6

BE9-7

DI9-2a

DI9-2b

E9-5

E9-6

E9-7

P9–2A

P9–4A

P9–5A

BE9-8

E9-8

P9–3A

BE9-5

Communication

Comp. Analysis

Decision Making

ANSWERS TO QUESTIONS

1. For plant assets, the historical cost principle means that cost consists of all expenditures necessary to

5. (a) Salvage value, also called residual value, is the expected value of the asset at the end of its

9. Revenue expenditures are ordinary repairs made to maintain the operating efficiency and productive

Questions Chapter 9 (Continued)

12. Natural resources consist of underground deposits of oil, gas, and minerals, and standing timber.

17. Goodwill is the value of many favorable attributes that are intertwined in the business enterprise.

20. McDonald’s asset turnover ratio is computed as follows:

Questions Chapter 9 (Continued)

22. Yes, the tax regulations of the IRS allow a company to use a different depreciation method on the

tax return than is used in preparing financial statements. Gomez Corporation uses an accelerated

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 9-1

BRIEF EXERCISE 9-2

BRIEF EXERCISE 9-3

BRIEF EXERCISE 9-4

Depreciable cost of $32,000, or ($38,000 – $6,000). With a four-year useful life,

BRIEF EXERCISE 9-5

It is likely that management requested this accounting treatment to boost

BRIEF EXERCISE 9-6

BRIEF EXERCISE 9-7

The depreciation cost per unit is 26 cents per mile computed as follows:

BRIEF EXERCISE 9-8

Book value, 1/1/17 ……………………………………………………………….. $23,000

BRIEF EXERCISE 9-9

BRIEF EXERCISE 9-9 (Continued)

BRIEF EXERCISE 9-10

(a) Depreciation Expense ……………………………………….. 5,250

BRIEF EXERCISE 9-11

(a) Depletion cost per unit = $7,000,000 ÷ 35,000,000 = $.20 depletion cost

per ton

BRIEF EXERCISE 9-12

BRIEF EXERCISE 9-13

DENT COMPANY

Balance Sheet (partial)

December 31, 2017

BRIEF EXERCISE 9-14

*BRIEF EXERCISE 9-15

*BRIEF EXERCISE 9-15 (Continued)

Fair value of old delivery

*BRIEF EXERCISE 9-16

Equipment (new) ……………………………………………………… 38,000

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 9-1

The following four items are expenditures necessary to acquire the truck

and get it ready for use:

DO IT! 9-2A

DO IT! 9-2B

DO IT! 9-4

1. Intangible assets

DO IT! 9-5

SOLUTIONS TO EXERCISES

EXERCISE 9-1

(b) 1. Land

EXERCISE 9-2

EXERCISE 9-3

(a) Cost of land

EXERCISE 9-4

1. False. Depreciation is a process of cost allocation, not asset valuation.

EXERCISE 9-5

(b)

Computation

End of Year

EXERCISE 9-6

(a) Straight-line method:

EXERCISE 9-7

EXERCISE 9-8

(a)

Type of Asset

Building

Warehouse

EXERCISE 9-9

EXERCISE 9-10

(a) Cash ………………………………………………………………. 31,000

EXERCISE 9-10 (Continued)

(c) Cash ……………………………………………………….……….. 11,000

EXERCISE 9-11

(a) Dec. 31 Inventory …………………………………………… 80,000

EXERCISE 9-13

1/2/17 Patents …………………………………………………. 595,000

EXERCISE 9-14

*EXERCISE 9-15

(b) Equipment (new) ……………………………………………….. 14,000

*EXERCISE 9-16

(a) Equipment (new) ………………………………………………. 3,000

(b) Equipment (new) ………………………………………………. 3,000

SOLUTIONS TO PROBLEMS

PROBLEM 9-1A

PROBLEM 9-2A

(a)

Year

Computation

Accumulated

Depreciation

12/31

(b)

Year

Computation

Expense

PROBLEM 9-3A

(2) Recorded cost ………………………………………………………… $ 50,000

(2)

Book Value at

Beginning

of Year

DDB

Rate

Annual Depreciation

Expense

Accumulated

Depreciation

PROBLEM 9-3A (Continued)

(3) Depreciation cost per unit = ($180,000 – $10,000)/125,000 units =

$1.36 per unit.

Annual Depreciation Expense

(c) The declining–balance method reports the highest amount of depreciation

PROBLEM 9-4A

Year

Depreciation

Expense

Accumulated

Depreciation

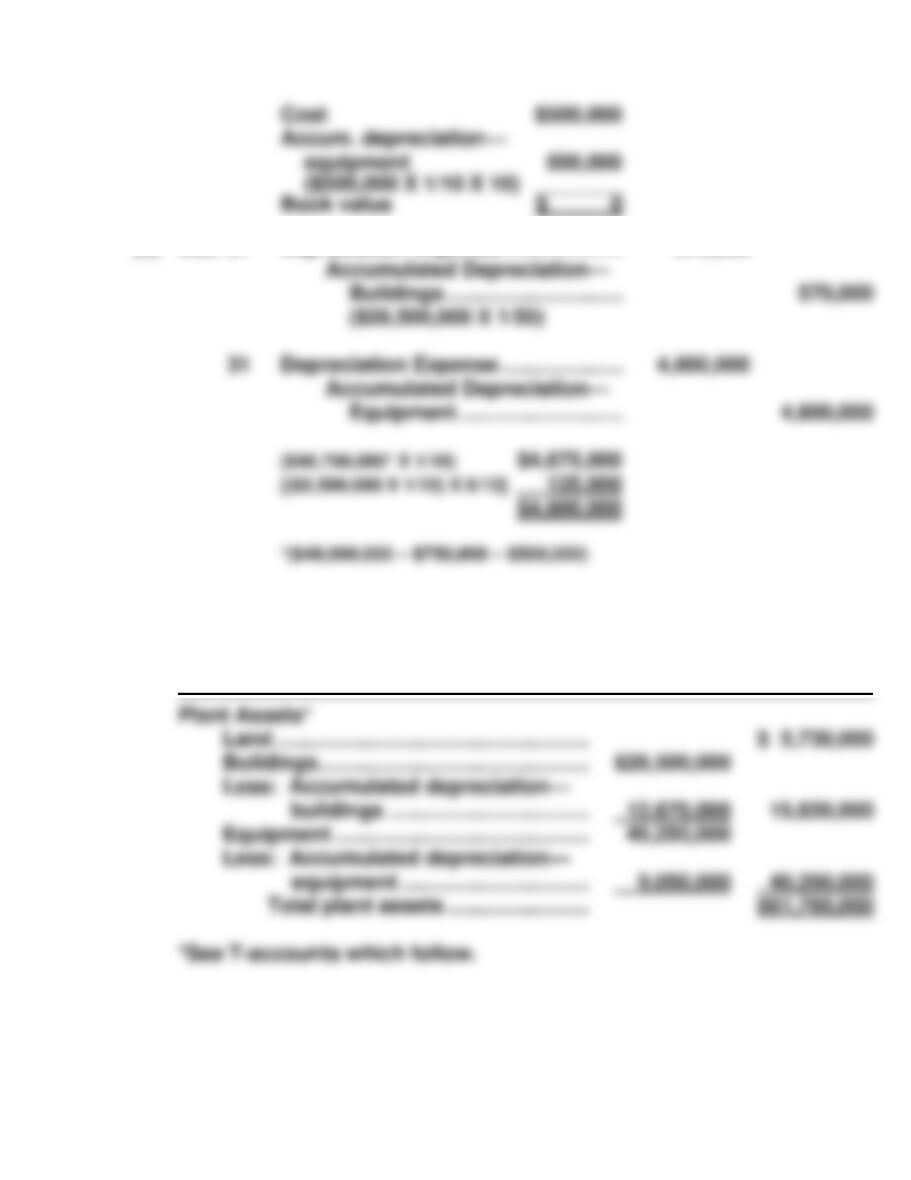

PROBLEM 9-5A

(a) Apr. 1 Land…………………………………………. 2,130,000

PROBLEM 9-5A (Continued)

(b) Dec. 31 Depreciation Expense ………………… 570,000

(c) GRAND COMPANY

Partial Balance Sheet

December 31, 2018

PROBLEM 9-5A (Continued)

Land

Equipment

PROBLEM 9-6A

(a) Accumulated Depreciation—Equipment ……………… 50,000

PROBLEM 9-7A

(a) Jan. 2 Patents …………………………………………….. 27,000

(c) Intangible Assets

PROBLEM 9-8A

1. Research and Development Expense ………………. 136,000

PROBLEM 9-9A

(a)

LaPorta

Lott

CP9COMPREHENSIVE PROBLEM SOLUTION

(a) 1. Equipment …………………………………………………… 22,800

COMPREHENSIVE PROBLEM (Continued)

COMPREHENSIVE PROBLEM (Continued)

(b) HASSELLHOUF COMPANY

Trial Balance

December 31, 2017

COMPREHENSIVE PROBLEM (Continued)

(c) HASSELLHOUF COMPANY

Income Statement

For the Year Ended December 31, 2017

HASSELLHOUF COMPANY

Retained Earnings Statement

For the Year Ended December 31, 2017

COMPREHENSIVE PROBLEM (Continued)

(d) HASSELLHOUF COMPANY

Balance Sheet

December 31, 2017

Liabilities and Stockholders’ Equity

BYP 9-1 FINANCIAL REPORTING PROBLEM

BYP 9-2 COMPARATIVE ANALYSIS PROBLEM

(a)

PepsiCo

Coca-Cola

BYP 9-3 COMPARATIVE ANALYSIS PROBLEM

(a)

Amazon

Wal-Mart

BYP 9-4 REAL-WORLD FOCUS

BYP 9-5 DECISION MAKING ACROSS THE ORGANIZATION

(a) Pinson Company—Straight-line method

Year

Asset

Computation

Annual

Depreciation

Accumulated

Depreciation

(b)

Year

Pinson

Company

Net Income

Estes

Company

Net Income

As Adjusted

Computations for Estes Company

BYP 9-5 (Continued)

BYP 9-6 COMMUNICATION ACTIVITY

Answers will depend on the position selected by the student. Some points

that should be considered include:

1. Some relatively small companies may spend less on R&D because they

BYP 9-7 ETHICS CASE

(a) The stakeholders in this situation are:

(c) Income before income taxes in the year of change is increased $160,000

by implementing the president’s proposed changes.

BYP 9-8 ALL ABOUT YOU

BYP 9-9 FASB CODIFICATION ACTIVITY

(a) Capitalize is used to indicate that the cost would be recorded as the

IFRS EXERCISES

IFRS9-1

Component depreciation is a method of allocating the cost of a plant asset

IFRS9-4 INTERNATIONAL FINANCIAL STATEMENT ANALYSIS