Chapter 9

Plant Assets, Natural Resources, and Intangibles

Review Questions

1. What are plant assets? Provide some examples.

2. Plant assets are recorded at historical cost. What does the historical cost of a plant asset include?

3. How do land improvements differ from land?

Land improvements are depreciable improvements to land, such as fencing, sprinklers, paving, signs,

and lighting. Land is not depreciated.

4. What does the word capitalize mean?

5. What is a lump-sum purchase, and how is it accounted for?

A lump-sum purchase, also called a basket purchase, is the purchase of several assets as a group.

The total cost paid (100%) is divided among the assets according to their relative market values.

6. What is the difference between a capital expenditure and a revenue expenditure? Give an example of

each.

A capital expenditure is debited to an asset account because it increases the asset’s capacity or

7. What is depreciation? What are the methods described in the chapter that can be used to compute

depreciation?

Depreciation is the allocation of a plant asset’s cost to expense over its useful life. Depreciation

8. Which depreciation method ignores residual value until the last year of depreciation? Why?

9. How does a business decide which depreciation method is best to use?

A business should match an asset’s expense against the revenue that the asset produces when

10. What is the depreciation method that is used for tax accounting purposes? How is it different than

the methods that are used for financial accounting purposes?

Modified Accelerated Cost Recovery System (MACRS) is a method used for tax purposes. Under

11. If a business changes the estimated useful life or estimated residual value of a plant asset, what must

the business do in regard to depreciation expense?

When a company makes an accounting change in estimate, generally accepted accounting principles

12. What financial statement is plant assets reported on, and how?

Plant assets are reported at book value on the balance sheet. Companies may choose to report plant

and the related accumulated depreciation should be disclosed.

13. How is discarding of a plant asset different from selling a plant asset?

Discarding of plant assets involves disposing of the asset for no cash. Selling an asset involves

receiving cash in exchange for the asset.

14. How is gain or loss determined when disposing of plant assets? What situation constitutes a gain?

What situation constitutes a loss?

Gain or loss is determined by comparing the cash received and the market value of any other assets

15. What is a natural resource? What is the process by which businesses spread the allocation of a

natural resource’s cost over its usage?

16. What is an intangible asset? Provide some examples.

Intangible assets are assets that have no physical form. Instead, these assets convey special rights

from patents, copyrights, trademarks, and other creative works.

17. What is the process by which businesses spread the allocation of an intangible asset’s cost over its

useful life?

18. What is goodwill? Is goodwill amortized? What happens if the value of goodwill has decreased at

the end of the year?

Goodwill is the excess of the cost of an acquired company over the sum of the market values of its

19. What does the asset turnover ratio measure, and how is it calculated?

20A. What does it mean if an exchange of plant assets has commercial substance? Are gains and losses

recorded on the books because of the exchange?

An exchange has commercial substance if the future cash flows change as a result of the

Short Exercises

S9-1 Determining the cost of an asset

Learning Objective 1

Alton Clothing purchased land, paying $88,000 cash plus a $250,000 note payable. In addition, Alton

paid delinquent property tax of $1,900, title insurance costing $500, and $4,200 to level the land and

remove an unwanted building. Record the journal entry for purchase of the land.

SOLUTION

Purchase price of land

$ 338,000

Add related costs:

Title insurance

Removal of building

6,600

Total cost of land

$ 344,600

S9-2 Making a lump-sum asset purchase

Learning Objective 1

Foley Distribution Service paid $130,000 for a group purchase of land, building, and equipment. At the

time of the acquisition, the land had a market value of $70,000, the building $42,000, and the equipment

$28,000. Journalize the lump-sum purchase of the three assets for a total cost of $130,000, the amount

for which the business signed a note payable.

SOLUTION

Asset

Market

Value

Percentage of Total Value

× Total

Purchase

Price

= Assigned

Cost of

Each Asset

Land

$ 70,000

$70,000 / $140,000 = 50%

× $130,000

= $ 65,000

Building

$42,000 / $140,000 = 30%

× $130,000

= 39,000

Equipment

$28,000 / $140,000 = 20%

× $130,000

Total

$ 140,000

S9-3 Computing first-year depreciation and book value

Learning Objective 2

At the beginning of the year, Austin Airlines purchased a used airplane for $33,500,000. Austin Airlines

expects the plane to remain useful for five years (4,000,000 miles) and to have a residual value of

$5,500,000. The company expects the plane to be flown 1,100,000 miles during the first year.

Requirements

1. Compute Austin Airlines’s first-year depreciation expense on the plane using the following methods:

a. Straight-line

b. Units-of-production

c. Double-declining-balance

2. Show the airplane’s book value at the end of the first year for all three methods.

SOLUTION

Requirement 1

a.

Straight-line

=

(Cost − Residual value) / Useful life

=

b.

Depreciation per unit

=

(Cost – Residual value) / Useful life in units

=

$7 per mile

Units-of-production

=

Depreciation per unit × Current year usage

=

$7 per mile × 1,100,000 miles

=

c.

Double-declining-balance

=

(Cost – Accumulated depreciation) × 2 × (1 / Useful life)

=

Requirement 2

Straight-line

Units-of-production

Double-declining-

balance

Cost

$ 33,500,000

$ 33,500,000

$ 33,500,000

Less: Accumulated Depreciation

Book value

$ 27,900,000

$ 25,800,000

$ 20,100,000

S9-4 Computing second-year depreciation and accumulated depreciation

Learning Objective 2

Requirements

1. Compute second-year (2017) depreciation expense on the plane using the following methods:

a. Straight-line

b. Units-of-production

c. Double-declining-balance

2. Calculate the balance in Accumulated Depreciation at the end of the second year for all three

methods.

SOLUTION

Requirement 1

a.

Straight-line

=

(Cost − Residual value) / Useful life

=

b.

Depreciation per unit

=

(Cost – Residual value) / Useful life in units

=

$7 per mile

Units-of-production

=

Depreciation per unit × Current year usage

=

$7 per mile × 1,200,000 miles

=

$8,400,000 in year 1

=

Depreciation per unit × Current year usage

=

$7 per mile × 1,400,000 miles

=

c.

Double-declining-balance

=

(Cost – Accumulated depreciation) × 2 × (1 / Useful life)

=

$10,000,000 in year 1

=

(Cost – Accumulated depreciation) × 2 × (1 / Useful life)

=

Requirement 2

Straight-line

Units-of-

production

Double-declining-

balance

Depreciation Expense – year 1

$ 4,375,000

$ 8,400,000

$ 10,000,000

Depreciation Expense – year 2

4,375,000

Total Accumulated Depreciation

$ 8,750,000

$ 17,500,000

S9-5 Calculating partial-year depreciation

Learning Objective 2

On September 30, 2015, Meggie Services purchased a copy machine for $38,000. Meggie Services

expects the machine to last for four years and have a residual value of $2,000. Compute depreciation

expense on the machine for the year ended December 31, 2015, using the straight-line method.

SOLUTION

Straight-line

S9-6 Changing the estimated life of an asset

Learning Objective 2

Assume that ABC Catering Services paid $20,000 for equipment with a 10-year life and zero expected

residual value. After using the equipment for four years, the company determines that the asset will

remain useful for only three more years.

Requirements

1. Record depreciation expense on the equipment for year 5 by the straight-line method.

2. What is accumulated depreciation at the end of year 5?

SOLUTION

Requirement 1

Straight-line

=

(Cost − Residual value) / Useful life

=

Accumulated depreciation after 4 years

=

$2,000 per year × 4 years

=

$8,000

Book value after 4 years

=

(Cost – Accumulated Depreciation)

=

$12,000

Revised depreciation

=

(Book value − Revised residual value) / Revised useful life remaining

=

Requirement 2

Straight-line

Depreciation Expense – years 1– 4

$ 8,000

Depreciation Expense – year 5

Total Accumulated Depreciation

S9-7 Discarding of a fully depreciated asset

Learning Objective 3

On June 15, 2015, Perfect Furniture discarded equipment that had a cost of $12,000, a residual value of

$0, and was fully depreciated. Journalize the disposal of the equipment.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

S9-8 Discarding an asset

Learning Objective 3

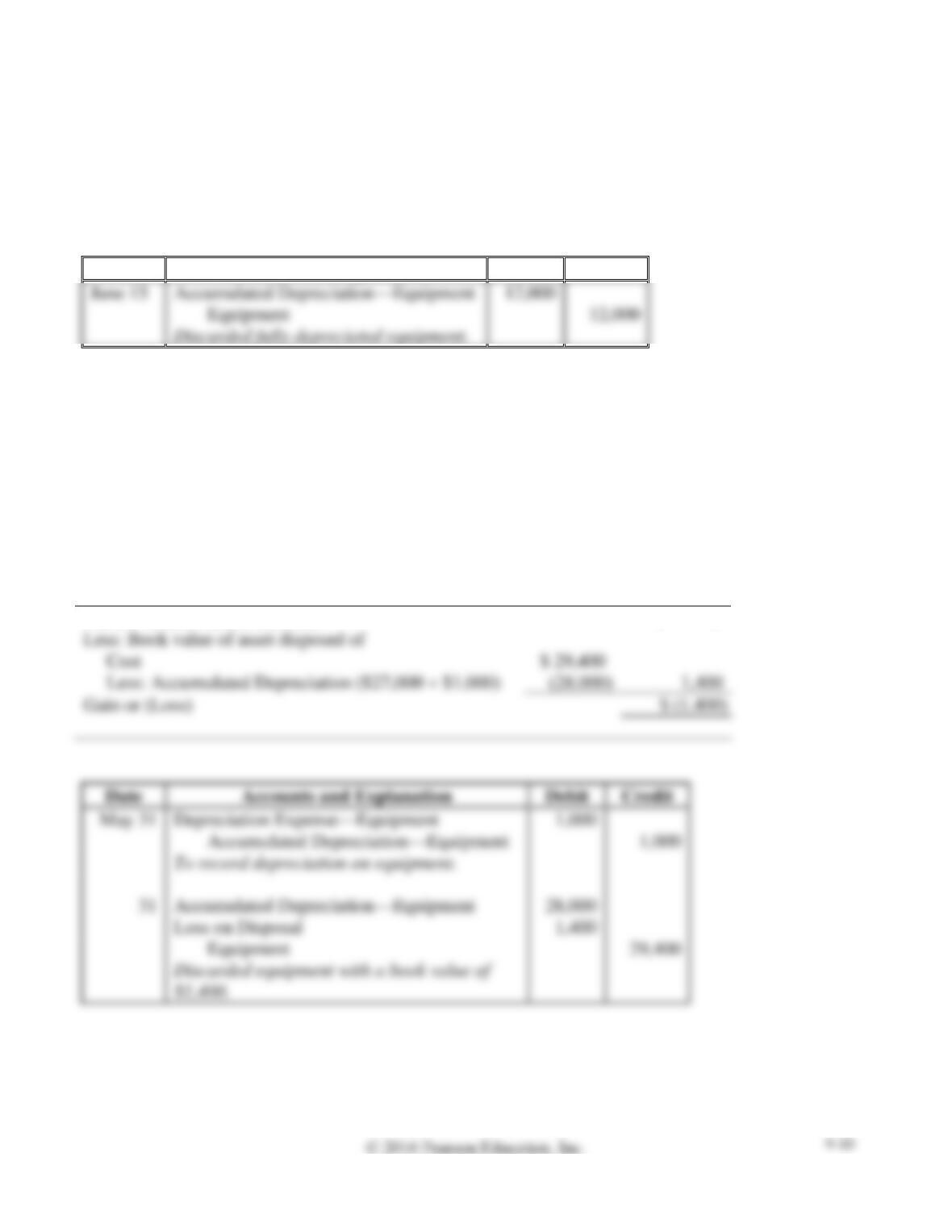

On May 31, 2016, Choice Landscapes discarded equipment that had a cost of $29,400. Accumulated

Depreciation as of December 31, 2015, was $27,000. Assume annual depreciation on the equipment is

$2,400. Journalize the partial-year depreciation expense and disposal of the equipment.

SOLUTION

Partial year depreciation = $2,400 × 5/12 = $1,000

Market value of assets received

$ 0

Less: Book value of asset disposed of

Cost

Less: Accumulated Depreciation ($27,000 + $1,000)

(28,000)

Gain or (Loss)

Date

Debit

Credit

S9-9 Selling an asset at gain or loss

Learning Objective 3

Mill Creek Golf Club purchased equipment on January 1, 2016, for $31,500. Suppose Mill Creek Golf

Club sold the equipment for $22,000 on December 31, 2018. Accumulated Depreciation as of December

31, 2018, was $21,000. Journalize the sale of the equipment, assuming straight-line depreciation was

used.

SOLUTION

Market value of assets received

$ 22,000

Less: Book value of asset disposed of

Cost

$ 31,500

Less: Accumulated Depreciation

Gain or (Loss)

S9-10 Selling an asset at gain or loss

Learning Objective 3

Pelman Company purchased equipment on January 1, 2016, for $32,000. Suppose Pelman sold the

equipment for $5,000 on December 31, 2017. Accumulated Depreciation as of December 31, 2017, was

$22,000. Journalize the sale of the equipment, assuming straight-line depreciation was used.

SOLUTION

Market value of assets received

$ 5,000

Less: Book value of asset disposed of

Cost

Less: Accumulated Depreciation

(22,000)

10,000

Gain or (Loss)

S9-11 Accounting for depletion of natural resources

Learning Objective 4

North Coast Petroleum holds huge reserves of oil assets. Assume that at the end of 2016, North Coast

Petroleum’s cost of oil reserves totaled $60,000,000,000, representing 5,000,000,000 barrels of oil.

Requirements

1. Which method does North Coast Petroleum use to compute depletion?

2. Suppose North Coast Petroleum removed and sold 900,000,000 barrels of oil during 2017.

Journalize depletion expense for 2017.

SOLUTION

Requirement 1

Units-of-production is the method used to compute depletion.

S9-12 Accounting for an intangible asset

Learning Objective 5

On March 1, 2016, Twist Company purchased a patent for $168,000 cash. Although the patent gives

legal protection for 20 years, the patent is expected to be used for only five years.

Requirements

1. Journalize the purchase of the patent.

2. Journalize the amortization expense for the year ended December 31, 2016. Assume straight-line

amortization.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Date

Accounts and Explanation

Debit

Credit

S9-13 Accounting for goodwill

Learning Objective 5

TXL Advertising paid $250,000 to acquire Seacoast Report, a weekly advertising paper. At the time of

the acquisition, Seacoast Report’s balance sheet reported total assets of $140,000 and liabilities of

$80,000. The fair market value of Seacoast Report’s assets was $110,000. The fair market value of

Seacoast Report’s liabilities was $80,000.

Requirements

1. How much goodwill did TXL Advertising purchase as part of the acquisition of Seacoast Report?

2. Journalize TXL Advertising’s acquisition of Seacoast Report.

SOLUTION

Requirement 1

Purchase price to acquire Seacoast Report

$ 250,000

Market value of Seacoast Report’s assets

Less: Seacoast Report’s liabilities

Market value of Seacoast Report’s net assets

S9-14 Computing the asset turnover ratio

Learning Objective 6

Balani, Inc. had net sales of $52,000,000 for the year ended May 31, 2016. Its beginning and ending

total assets were $53,200,000 and $98,400,000, respectively. Determine Balani’s asset turnover ratio for

year ended May 31, 2016.

SOLUTION

S9A-15 Exchanging plant assets

Learning Objective 7

Appendix 9A

Alpha Communications, Inc. purchased a computer for $2,600, debiting Computer Equipment. During

2014 and 2015, Alpha Communications, Inc. recorded total depreciation of $1,800 on the computer. On

January 1, 2016, Alpha Communications, Inc. traded in the computer for a new one, paying $2,400 cash.

The fair market value of the new computer is $4,300. Journalize Alpha Communications, Inc.’s

exchange of computers. Assume the exchange had commercial substance.

SOLUTION

Market value of assets received

$ 4,300

Less:

Book value of asset exchanged

Cash paid

Gain or (Loss)

$ 1,100

S9A-16 Exchanging plant assets

Learning Objective 7

Appendix 9A

Orange Corporation purchased equipment for $30,000. Orange recorded total depreciation of $24,000 on

the equipment. On January 1, 2016, Orange traded in the equipment for new equipment, paying $23,500

cash. The fair market value of the new equipment is $28,500. Journalize Orange Corporation’s exchange

of equipment. Assume the exchange had commercial substance.

SOLUTION

Market value of assets received

$ 28,500

Less:

Book value of asset exchanged

(24,000)

Cash paid

Gain or (Loss)

Exercises

E9-17 Determining the cost of assets

Learning Objective 1

1. Land $365,000

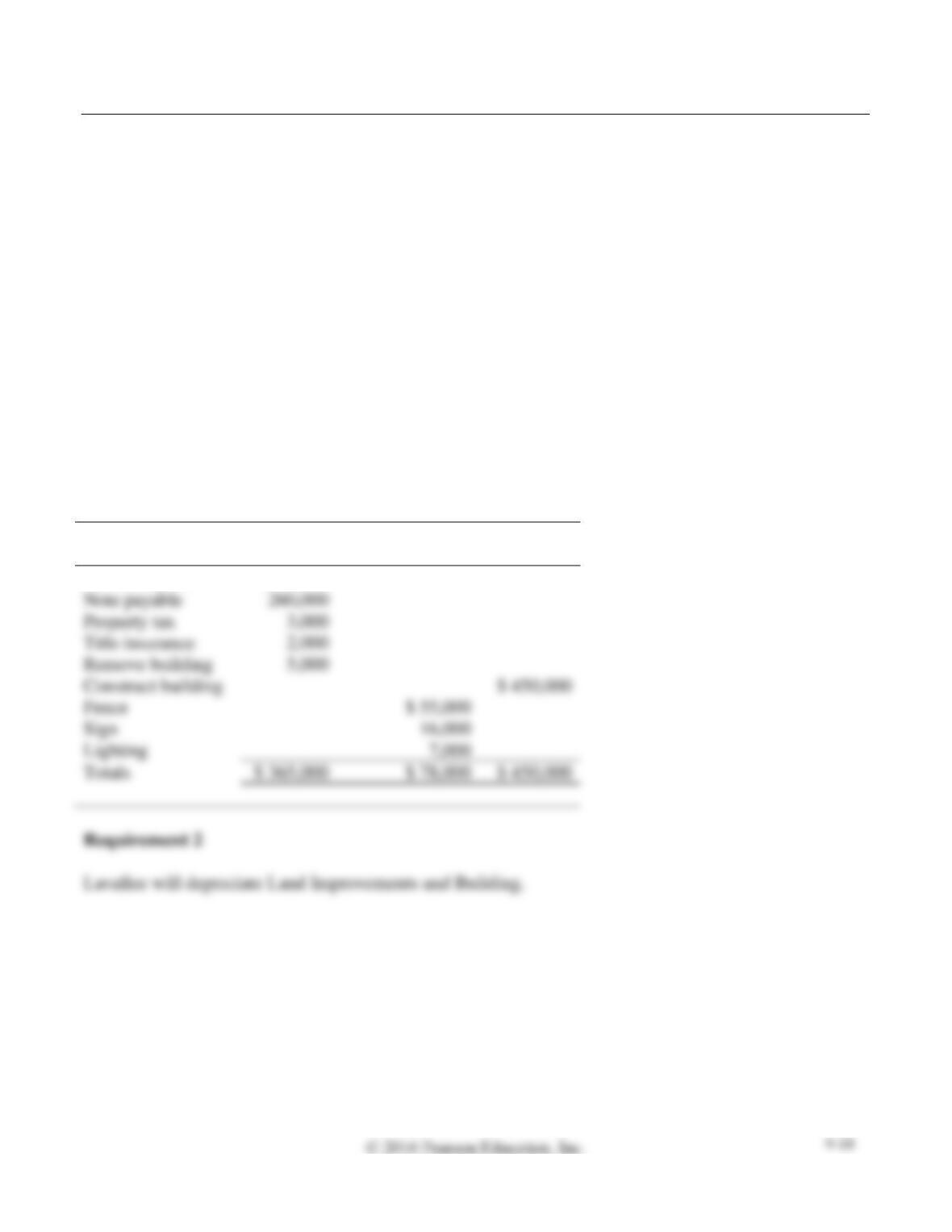

Lavallee Furniture purchased land, paying $95,000 cash plus a $260,000 note payable. In addition,

Lavallee paid delinquent property tax of $3,000, title insurance costing $2,000, and $5,000 to level the

land and remove an unwanted building. The company then constructed an office building at a cost of

$450,000. It also paid $55,000 for a fence around the property, $16,000 for a sign near the entrance, and

$7,000 for special lighting of the grounds.

Requirements

1. Determine the cost of the land, land improvements, and building.

2. Which of these assets will Lavallee depreciate?

SOLUTION

Requirement 1

Land

Land

Improvements

Building

Purchase price

$ 95,000

Note payable

Property tax

Remove building

Construct building

$ 450,000

Fence

Sign

Lighting

7,000

Totals

$ 450,000

E9-18 Making a lump-sum purchase of assets

Learning Objective 1

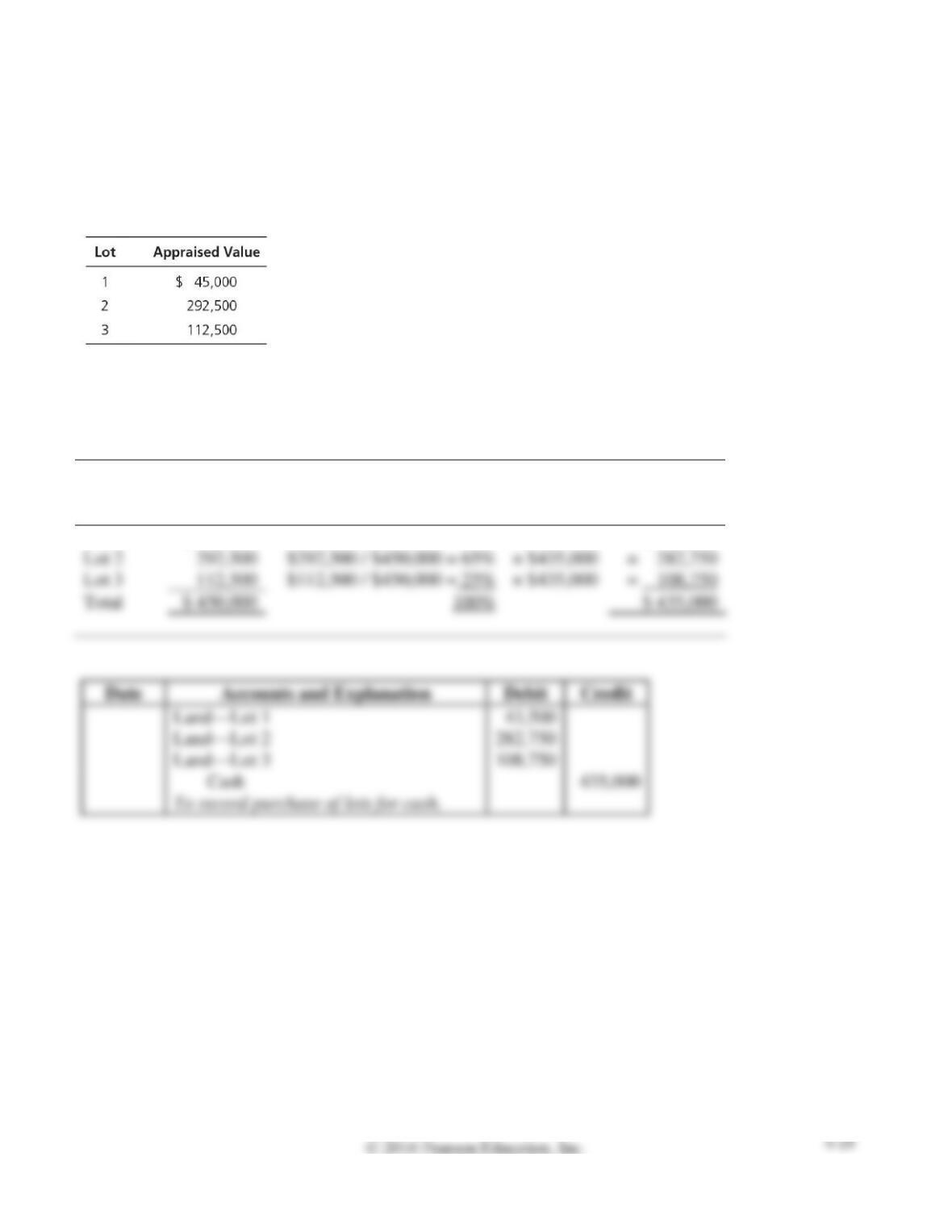

Lot 3 $108,750

Dearwood Properties bought three lots in a subdivision for a lump-sum price. An independent appraiser

valued the lots as follows:

Dearwood paid $435,000 in cash. Record the purchase in the journal, identifying each lot’s cost in a

separate Land account. Round decimals to two places, and use the computed percentages throughout.

SOLUTION

Asset

Market

Value

Percentage of Total Value

× Total

Purchase

Price

= Assigned

Cost of

Each Asset

Lot 1

$ 45,000

$45,000 / $450,000 = 10%

× $435,000

= $ 43,500

Lot 2

× $435,000

= 282,750

Lot 3

× $435,000

Total

$ 450,000

Debit

Credit

E9-19 Distinguishing capital expenditures from revenue expenditures

Learning Objective 1

Consider the following expenditures:

Classify each of the expenditures as a capital expenditure or a revenue expenditure related to machinery.

SOLUTION

a.

Capital expenditure

Revenue expenditure

c.

Capital expenditure

Revenue expenditure

e.

Capital expenditure

Capital expenditure

Capital expenditure

Capital expenditure

Capital expenditure