SOLUTION

Date

Accounts and Explanation

Debit

Credit

Jan. 1

Office Equipment

112,000

Cash

74,000

Note Payable

38,000

To record purchase of office equipment.

Land

255,000

Communication Equipment

Cash

340,000

To record purchase of land and comm. equipment.

Depreciation Expense—Building

Accumulated Depreciation—Building

To record depreciation on building.

Cash

380,000

Accumulated Depreciation—Building

248,000

Building

540,000

Gain on Disposal

88,000

To record sale of building.

Depreciation Expense—Communication Equipment

Accumulated Depreciation—Comm. Equipment

12,750

To record depreciation on communication equipment.

Depreciation Expense—Office Equipment

Accumulated Depreciation—Office Equipment

44,800

To record depreciation on office equipment.

Calculations:

Apr. 1 – Acquisition of land and communication equipment:

Asset

Market

Value

Percentage of Total Value

× Total

Purchase

Price

= Assigned

Cost of

Each Asset

$89,250 / $357,000 = 25%

P9-32A, cont.

Sep. 1 – Sale of building

Straight-line depreciation

=

(Cost − Residual value) / Useful life × (Number of Months / 12)

=

($540,000 ̶ $60,000) / 40 years × 8/12

=

$8,000 per partial year (2016)

Market value of assets received

Less: Book value of asset disposed of

Cost

$ 540,000

Less: Accumulated Depreciation ($240,000 + $8,000)

Gain or (Loss)

$ 88,000

Straight-line depreciation

=

(Cost − Residual value) / Useful life × (Number of Months / 12)

=

=

$12,750 per partial year (2016)

Double-declining-balance depreciation

=

(Cost – Accumulated depreciation) × 2 × (1 / Useful life)

=

($112,000 ̶ $0) × 2 × (1/5 years)

=

$44,800 in 2016

P9-33A Accounting for natural resources

Learning Objective 4

Dep. Exp. $1,186,250

Chapman Oil, Inc. has an account titled Oil and Gas Properties. Chapman paid $6,300,000 for oil

reserves holding an estimated 400,000 barrels of oil. Assume the company paid $560,000 for additional

geological tests of the property and $440,000 to prepare for drilling. During the first year, Chapman

removed and sold 65,000 barrels of oil. Record all of Chapman’s transactions, including depletion for

the first year.

SOLUTION

Purchase price of oil reserves

$ 6,300,000

Add related costs:

Geological tests

Drilling preparation

Total cost of oil reserves

$ 7,300,000

Depletion per unit

(Cost – Residual value) / Estimated total units

$18.25 per barrel

Depletion expense

Depletion per unit × Number of units extracted

$18.25 per barrel × 65,000 barrels

$1,186,250

Date

Accounts and Explanation

Debit

Credit

Oil and Gas Properties

6,300,000

Cash

6,300,000

To record purchase of oil reserves.

Oil and Gas Properties

1,000,000

Cash

1,000,000

of oil reserves.

Depletion Expense—Oil and Gas Properties

1,186,250

Accumulated Depletion—Oil and Gas Properties

1,186,250

To record depletion.

P9-34A Accounting for intangibles

Learning Objective 5

1. Goodwill $650,000

Middle Telecom provides communication services in Iowa, Nebraska, the Dakotas, and Montana.

Middle purchased goodwill as part of the acquisition of Shipley Wireless Enterprises, which had the

following figures:

Requirements

1. Journalize the entry to record Middle’s purchase of Shipley Wireless for $400,000 cash plus a

$600,000 note payable.

2. What special asset does Middle’s acquisition of Shipley Wireless identify? How should Middle

Telecom account for this asset after acquiring Shipley Wireless? Explain in detail.

SOLUTION

Requirement 1

Purchase price to acquire Shipley Wireless ($400,000 + $600,000)

$1,000,000

Goodwill

Date

Accounts and Explanation

Debit

Credit

Assets

900,000

Goodwill

650,000

Requirement 2

P9A-35A Journalizing partial-year depreciation and asset disposals and exchanges

Learning Objectives 2, 3, 7

Appendix 9A

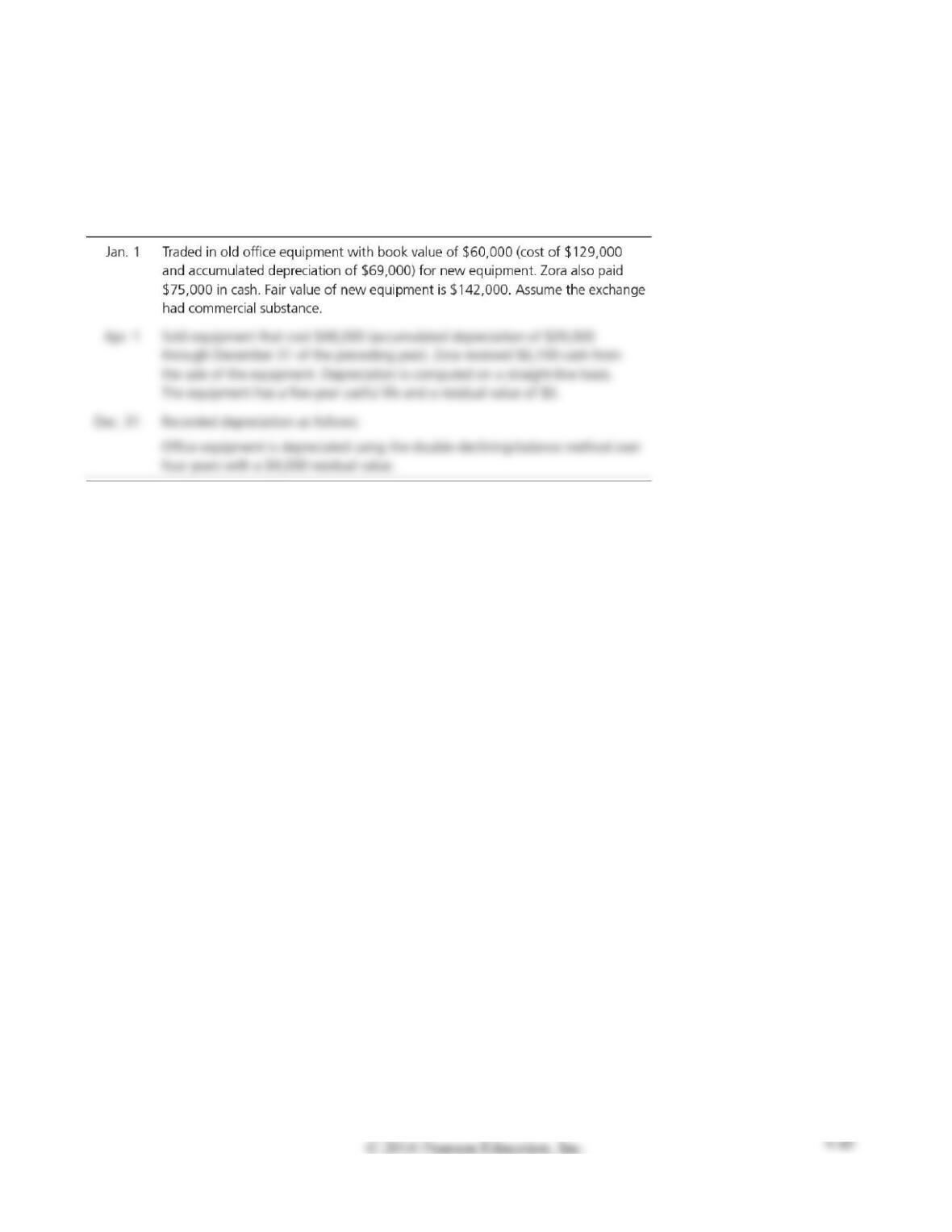

Jan. 1 Gain $7,000

During 2016, Zora Corporation completed the following transactions:

Record the transactions in the journal of Zora Corporation.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

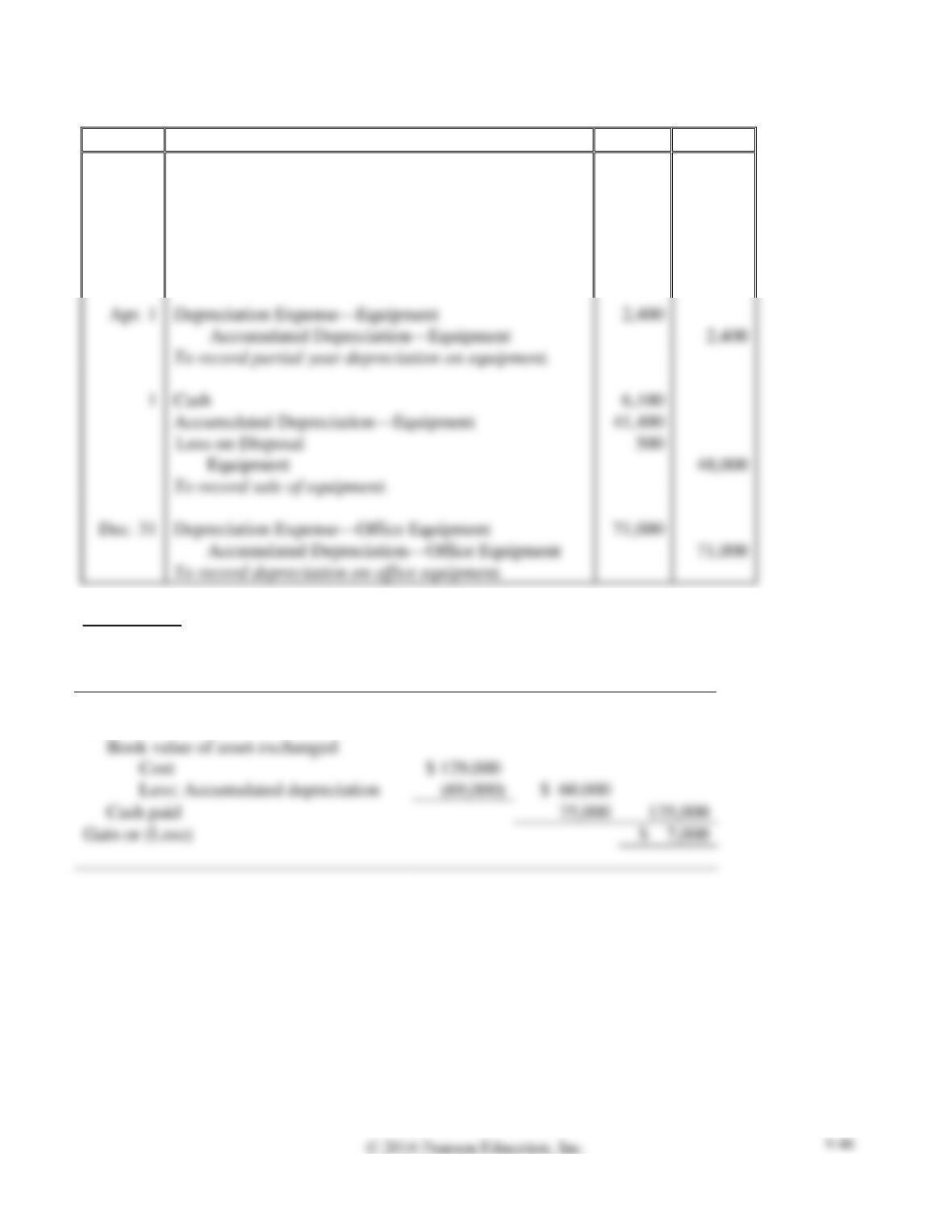

Jan. 1

Office Equipment (new)

142,000

Accumulated Depreciation—Office Equipment

69,000

Office Equipment (old)

129,000

Cash

75,000

Gain on Disposal

7,000

To record exchange of office equipment.

Depreciation Expense—Equipment

2,400

Cash

Accumulated Depreciation—Equipment

41,400

Equipment

48,000

To record sale of equipment.

Dec. 31

Depreciation Expense—Office Equipment

71,000

Accumulated Depreciation—Office Equipment

71,000

To record depreciation on office equipment.

Calculations:

Jan. 1 – Exchange of office equipment

Market value of assets received

$ 142,000

Less:

Book value of asset exchanged

Cash paid

Gain or (Loss)

P9-35A, cont.

Apr. 1 – Sale of equipment

Straight-line depreciation

=

(Cost − Residual value) / Useful life × (Number of Months / 12)

=

($48,000 ̶ $0) / 5 years × 3/12

=

$2,400 per partial year (2016)

Market value of assets received

Less: Book value of asset disposed of

Cost

$ 48,000

Less: Accumulated Depreciation ($39,000 + $2,400)

Gain or (Loss)

$ (500)

Double-declining-balance depreciation

=

(Cost – Accumulated depreciation) × 2 × (1 / Useful life)

=

($142,000 – $0) × 2 × (1/4 years)

=

$71,000

Problems (Group B)

P9-36B Determining asset cost and recording partial-year depreciation

Learning Objectives 1, 2

1. Bldg. $471,000

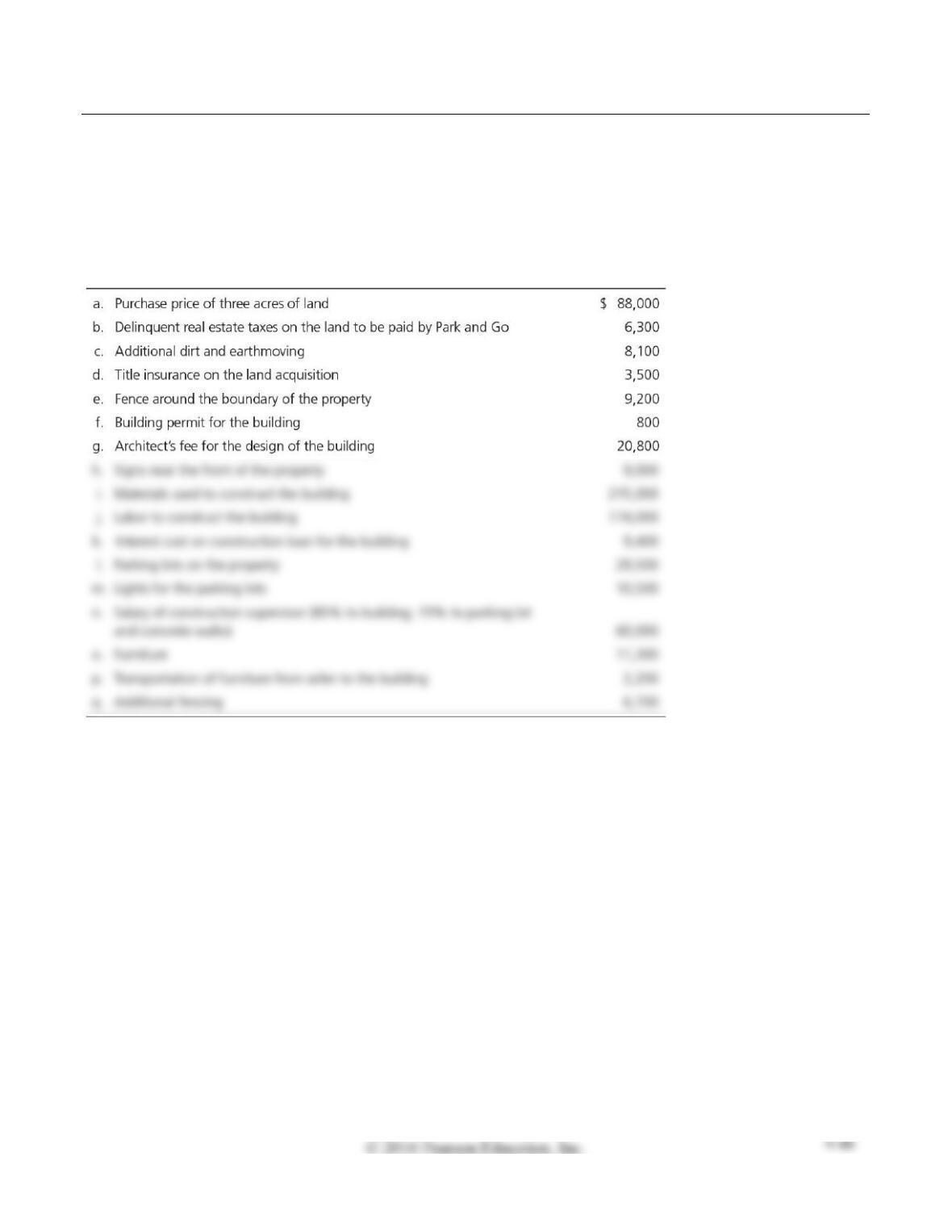

Park and Go, near an airport, incurred the following costs to acquire land, make land improvements, and

construct and furnish a small building:

Park and Go depreciates land improvements over 20 years, buildings over 50 years, and furniture over

eight years, all on a straight-line basis with zero residual value.

Requirements

1. Set up columns for Land, Land Improvements, Building, and Furniture. Show how to account for

each cost by listing the cost under the correct account. Determine the total cost of each asset.

2. All construction was complete and the assets were placed in service on July 1. Record partial-year

depreciation expense for the year ended December 31.

SOLUTION

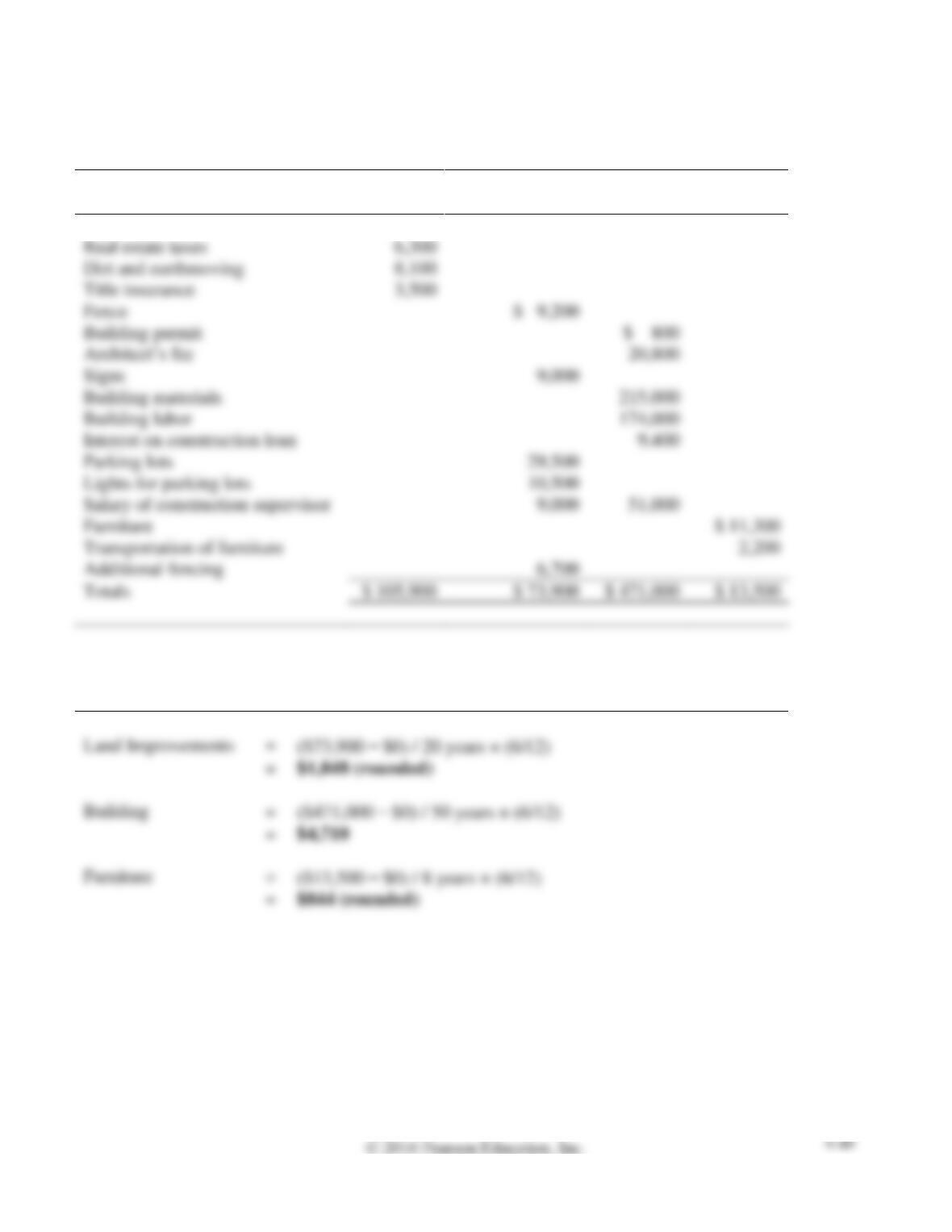

Requirement 1

Land

Land

Improvements

Building

Furniture

Purchase price

$ 88,000

Real estate taxes

Dirt and earthmoving

Title insurance

Fence

Building permit

Architect’s fee

Signs

9,000

Building materials

Building labor

Interest on construction loan

Parking lots

Lights for parking lots

Salary of construction supervisor

9,000

Furniture

Transportation of furniture

Additional fencing

6,700

Totals

$ 105,900

$ 471,000

Requirement 2

Straight-line

=

(Cost − Residual value) / Useful life × (Number of Months / 12)

=

=

=

P9-36B, cont.

Requirement 2, cont.

Date

Accounts and Explanation

Debit

Credit

Dec. 31

Depreciation Expense—Land Improvements

1,848

Accumulated Depreciation—Land Improvements

1,848

To record depreciation on land improvements.

Depreciation Expense—Building

4,710

Accumulated Depreciation—Building

4,710

To record depreciation on building.

Depreciation Expense—Furniture

Accumulated Depreciation—Furniture

To record depreciation on furniture.

P9-37B Determining asset cost, recording first-year depreciation, and identifying depreciation

results that meet management objectives

Learning Objectives 1, 2

1. Units-of-production, 12/31/16, Dep. Exp. $18,900

On January 3, 2016, Quick Delivery Service purchased a truck at a cost of $90,000. Before placing the

truck in service, Quick spent $2,500 painting it, $1,800 replacing tires, and $4,700 overhauling the

engine. The truck should remain in service for five years and have a residual value of $9,000. The

truck’s annual mileage is expected to be 21,000 miles in each of the first four years and 16,000 miles in

the fifth year—100,000 miles in total. In deciding which depreciation method to use, Harvey Warner,

the general manager, requests a depreciation schedule for each of the depreciation methods (straight–

line, units-of-production, and double-declining-balance).

Requirements

1. Prepare a depreciation schedule for each depreciation method, showing asset cost, depreciation

expense, accumulated depreciation, and asset book value.

2. Quick prepares financial statements using the depreciation method that reports the highest net

income in the early years of asset use. Consider the first year that Quick uses the truck. Identify the

depreciation method that meets the company’s objectives.

SOLUTION

Requirement 1

Purchase price of truck

$ 90,000

Add related costs:

Painting

Tires

Engine overhaul

Total cost of truck

$ 99,000

Depreciable cost = Cost − Residual value = $99,000 − $9,000 = $90,000

Straight-Line Depreciation Schedule

Depreciation for the Year

Date

Asset

Cost

Depreciable

Cost

Depreciation

Rate

Depreciation

Expense

Accumulated

Depreciation

Book

Value

1/03/16

$ 99,000

$ 99,000

81,000

63,000

45,000

27,000

P9-37B, cont.

Requirement 1, cont.

Depreciation per unit

=

(Cost – Residual value) / Useful life in units

=

($99,000 ̶ $9,000) / 100,000 miles

=

$0.90 per mile

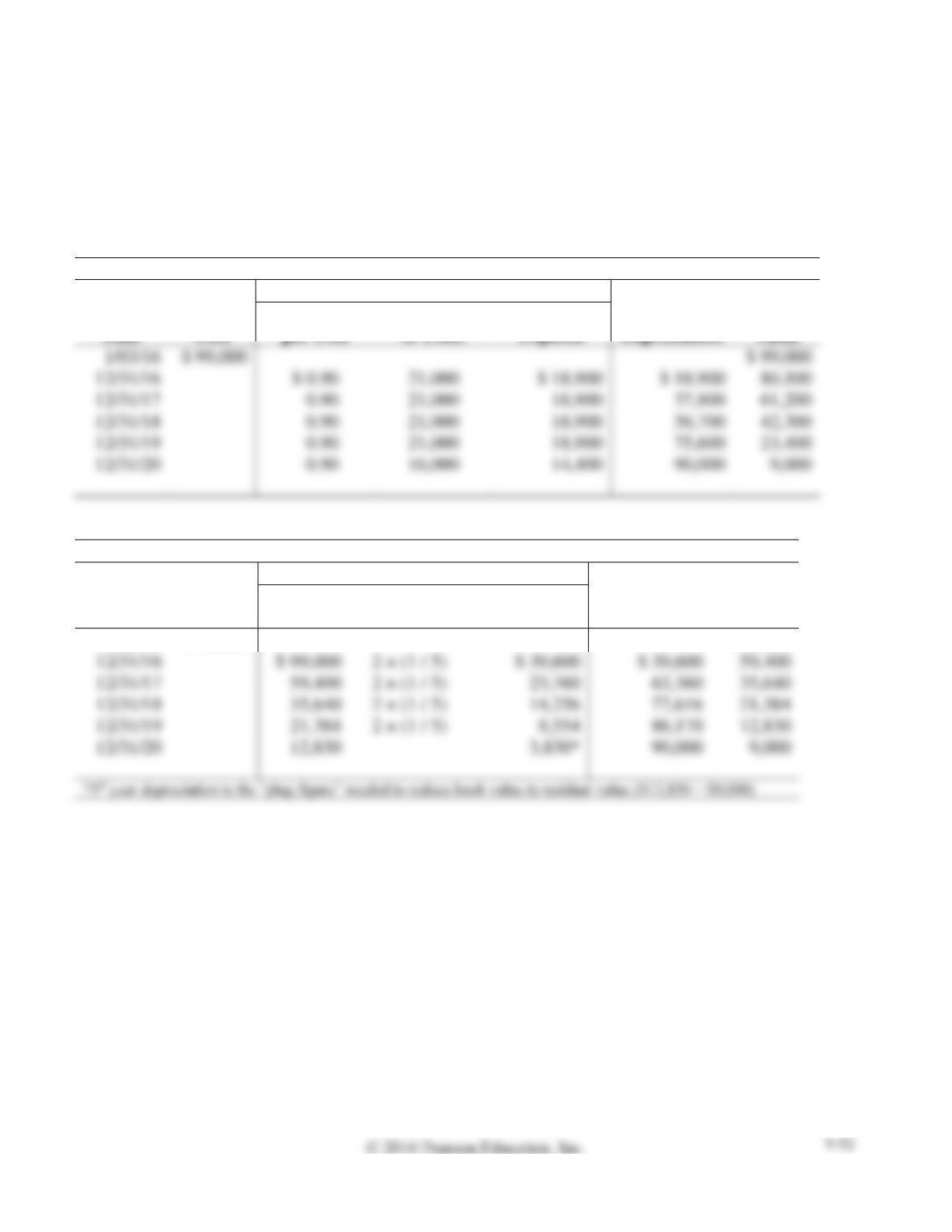

Units-of-Production Depreciation Schedule

Depreciation for the Year

Date

per Unit

Expense

Depreciation

Value

1/03/16

12/31/16

12/31/17

12/31/18

12/31/19

12/31/20

Asset

Depreciation

Number

Depreciation

Accumulated

Book

Double-Declining-Balance Depreciation Schedule

Depreciation for the Year

Date

Asset

Cost

Book

Value

DDB

Rate

Depreciation

Expense

Accumulated

Depreciation

Book

Value

1/03/16

$ 99,000

$ 99,000

Requirement 2

The depreciation method that reports the highest net income in the first year is the straight-line method.

It produces the lowest depreciation expense ($18,000) and therefore the highest net income.

P9-38B Recording lump-sum asset purchases, depreciation, and disposals

Learning Objectives 1, 2, 3

Sep. 1 Gain $68,000

Granny Carney Associates surveys American eating habits. The company’s accounts include Land,

Buildings, Office Equipment, and Communication Equipment, with a separate Accumulated

Depreciation account for each asset. During 2016, Granny Carney completed the following transactions:

Record the transactions in the journal of Granny Carney Associates.