CHAPTER 8

NET PRESENT VALUE AND OTHER

INVESTMENT CRITERIA

Answers to Concepts Review and Critical Thinking Questions

1. A payback period less than the project’s life means that the NPV is positive for a zero discount rate,

but nothing more definitive can be said. For discount rates greater than zero, the payback period will

still be less than the project’s life, but the NPV may be positive, zero, or negative, depending on

whether the discount rate is less than, equal to, or greater than the IRR.

3. a. Payback period is simply the break-even point of a series of cash flows. To actually compute the

payback period, it is assumed that any cash flow occurring during a given period is realized

continuously throughout the period, and not at a single point in time. The payback is then the

point in time for the series of cash flows when the initial cash outlays are fully recovered. Given

some predetermined cutoff for the payback period, the decision rule is to accept projects that

payback before this cutoff, and reject projects that take longer to payback.

4. a. The average accounting return is interpreted as an average measure of the accounting

performance of a project over time, computed as some average profit measure due to the project

divided by some average balance sheet value for the project. This text computes AAR as average

net income with respect to average (total) book value. Given some predetermined cutoff for AAR,

the decision rule is to accept projects with an AAR in excess of the target measure, and reject all

other projects.

b. AAR is not a measure of cash flows and market value, but a measure of financial statement

5. a. NPV is simply the sum of the present values of a project’s cash flows. NPV specifically measures,

after considering the time value of money, the net increase or decrease in firm wealth due to the

project. The decision rule is to accept projects that have a positive NPV, and reject projects with

a negative NPV.

6. a. The IRR is the discount rate that causes the NPV of a series of cash flows to be equal to zero.

IRR can thus be interpreted as a financial break-even rate of return; at the IRR discount rate, the

net value of the project is zero. The IRR decision rule is to accept projects with IRRs greater than

the discount rate, and to reject projects with IRRs less than the discount rate.

7. a. The profitability index is the present value of the future cash flows divided by the initial

investment. As such, it is a benefit/cost ratio, providing a measure of the relative profitability of

a project. The profitability index decision rule is to accept projects with a PI greater than one,

and to reject projects with a PI less than one.

8. For a project with future cash flows that are an annuity:

Payback = I / C

And the IRR is:

0 = – I + C / IRR

9. There are a number of reasons. Two of the most important have to do with transportation costs and

exchange rates. Manufacturing in the U.S. places the finished product much closer to the point of sale,

resulting in significant savings in transportation costs. It also reduces inventories because goods spend

less time in transit. Higher labor costs tend to offset these savings to some degree, at least compared

to other possible manufacturing locations. Of great importance is the fact that manufacturing in the

U.S. means that a much higher proportion of the costs are paid in dollars. Since sales are in dollars,

the net effect is to immunize profits to a large extent against fluctuations in exchange rates. This issue

is discussed in greater detail in the chapter on international finance.

11. Yes, they are. Such entities generally need to allocate available capital efficiently, just as for-profits

do. However, it is frequently the case that the “revenues” from not-for-profit ventures are not tangible.

For example, charitable giving has real opportunity costs, but the benefits are generally hard to

measure. To the extent that benefits are measurable, the question of an appropriate required return

remains. Payback rules are commonly used in such cases. Finally, realistic cost/benefit analysis along

the lines indicated should definitely be used by the U.S. government and would go a long way toward

balancing the budget!

13. The MIRR is calculated by finding the present value of all cash outflows, the future value of all cash

inflows to the end of the project, and then calculating the IRR of the two cash flows. As a result, the

14. The statement is incorrect. It is true that if you calculate the future value of all intermediate cash flows

to the end of the project at the required return, then calculate the NPV of this future value and the

initial investment, you will get the same NPV. However, NPV says nothing about reinvestment of

intermediate cash flows. The NPV is the present value of the project cash flows. What is actually done

15. The statement is incorrect. It is true that if you calculate the future value of all intermediate cash flows

to the end of the project at the IRR, then calculate the IRR of this future value and the initial

investment, you will get the same IRR. However, as in the previous question, what is done with the

cash flows once they are generated does not affect the IRR. Consider the following example:

Solutions to Questions and Problems

Basic

NOTE: All end-of-chapter problems were solved using a spreadsheet. Many problems require multiple

steps. Due to space and readability constraints, when these intermediate steps are included in this solutions

manual, rounding may appear to have occurred. However, the final answer for each problem is found

without rounding during any step in the problem.

1. To calculate the payback period, we need to find the time it takes to recover the initial investment.

After two years, the project has created:

$2,800 + 3,200 = $6,000

2. To calculate the payback period, we need to find the time it takes to recover the initial investment. The

cash flows in this problem are an annuity, so the calculation is simpler. If the initial cost is $3,100, the

payback period is:

Payback = 3 + $295 / $935

Payback = 3.32 years

If the initial cost is $7,900, the project never pays back. Notice that if you use the shortcut for annuity

cash flows, you get:

Payback = $7,900 / $935

Payback = 8.45 years

This answer does not make sense since the cash flows stop after eight years, so again, we must

conclude the payback period is never.

3. Project A has cash flows of:

Cash flows = $23,000 + 28,000

Cash flows = $51,000

during the first three years. The cash flows are still short by $29,000 of recapturing the initial

investment, so the payback for Project B is:

Payback = 3 + ($29,000 / $260,000)

Payback = 3.11 years

Using the payback criterion and a cutoff of 3 years, accept Project A and reject Project B.

4. Our definition of AAR is the average net income divided by the average book value. The average net

income for this project is:

5. The IRR is the interest rate that makes the NPV of the project equal to zero. So, the equation that defines

the IRR for this project is:

0 = –$168,500 + $86,000 / (1+IRR) + $91,000 / (1+IRR)2 + $53,000 / (1+IRR)3

6. The NPV of a project is the PV of the outflows minus by the PV of the inflows. The equation for the

NPV of this project at a 9 percent required return is:

NPV = –$168,500 + $86,000 / 1.09 + $91,000 / 1.092 + $53,000 / 1.093

NPV = $27,917.69

7. The NPV of a project is the PV of the outflows plus the PV of the inflows. Since the cash inflows are

an annuity, the equation for the NPV of this project at an 8 percent required return is:

NPV = –$8,450 + $2,145(PVIFA8%, 8)

NPV = $3,876.54

8. The IRR is the interest rate that makes the NPV of the project equal to zero. So, the equation that

defines the IRR for this project is:

0 = –$19,400 + $9,800 / (1+IRR) + $11,300 / (1+IRR)2 + $6,900 / (1+IRR)3

9. The NPV of a project is the PV of the outflows plus by the PV of the inflows. At a zero discount rate

(and only at a zero discount rate), the cash flows can be added together across time. So, the NPV of

the project at a zero percent required return is:

NPV = –$19,400 + 9,800 + 11,300 + 6,900

NPV = $8,600

The NPV at a 10 percent required return is:

10. a. The IRR is the interest rate that makes the NPV of the project equal to zero. The equation for the

IRR of Project A is:

0 = –$78,500 + $43,000 / (1 + IRR) + $29,000 / (1 + IRR)2 + $23,000 / (1 + IRR)3

+ $21,000 / (1 + IRR)4

b. The NPV of Project A is:

NPVA = –$78,500 + $43,000 / 1.11+ $29,000 / 1.112 + $23,000 / 1.113 + $21,000 / 1.114

NPVA = $14,426.54

And the NPV of Project B is:

c. To find the crossover rate, we subtract the cash flows from one project from the cash flows of the

other project. Here, we will subtract the cash flows for Project B from the cash flows of Project

A. Once we find these differential cash flows, we find the IRR. The equation for the crossover

rate is:

0 = $22,000 / (1 + R) + $1,000 / (1 + R)2 – $11,000 / (1 + R)3 – $20,000 / (1 + R)4

11. The IRR is the interest rate that makes the NPV of the project equal to zero. The equation to calculate

the IRR of Project X is:

0 = –$23,400 + $13,100 / (1 + IRR) + $9,480 / (1 + IRR)2 + $7,890 / (1 + IRR)3

Using a spreadsheet, financial calculator, or trial and error to find the root of the equation, we find that:

To find the crossover rate, we subtract the cash flows from one project from the cash flows of the other

project, and find the IRR of the differential cash flows. We will subtract the cash flows from Project

Y from the cash flows from Project X. It is irrelevant which cash flows we subtract from the other.

Subtracting the cash flows, the equation to calculate the IRR for these differential cash flows is:

Crossover rate: 0 = $3,900 / (1 + R) – $1,140 / (1 + R)2 – $3,290 / (1 + R)3

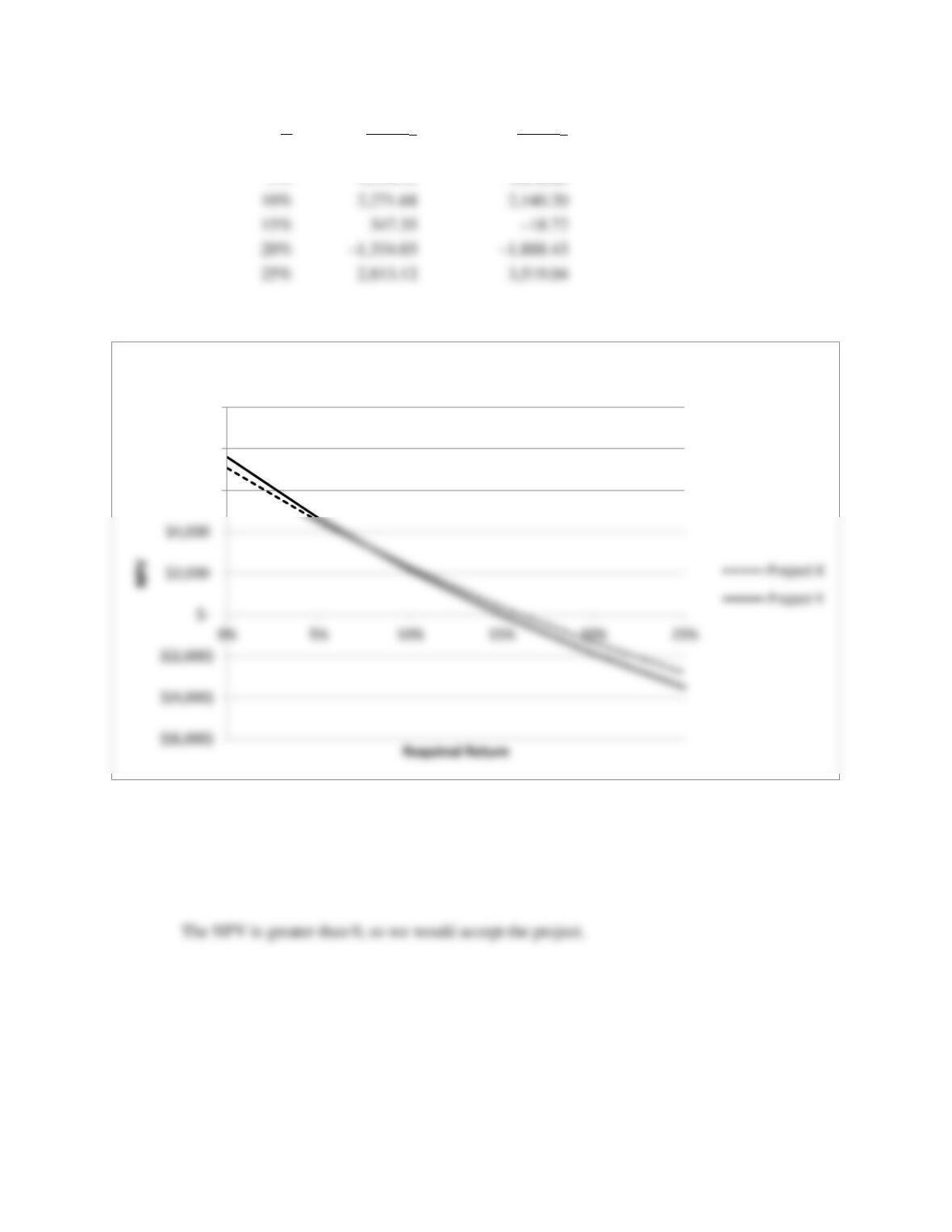

R

$NPVX

$NPVY

0%

$7,070.00

$7,600.00

5%

4,490.51

4,652.26

And the NPV profile is:

12. a. The equation for the NPV of the project is:

NPV = –$39,000,000 + $57,000,000 / 1.10 – $9,000,000 / 1.102

NPV = $5,380,165.29

$6,000

$8,000

$10,000

NPV Profile

b. The equation for the IRR of the project is:

0 = –$39,000,000 + $57,000,000 / (1 + IRR) – $9,000,000 / (1 + IRR)2

13. The profitability index is defined as the PV of the future cash flows divided by the initial investment.

The equation for the profitability index at a required return of 10 percent is:

PI = ($15,800 / 1.10 + $13,600 / 1.102 + $8,300 / 1.103) / $27,500

PI = 1.158

The equation for the profitability index at a required return of 15 percent is:

14. a. The profitability index is defined as the PV of the future cash flows divided by the initial

investment. The equation for the profitability index for each project is:

PII = ($28,300 / 1.11 + $34,800 / 1.112 + $43,700 / 1.113) / $78,000

PII = 1.099

b. The NPV of each project is:

NPVI = –$78,000 + $28,300 / 1.11 + $34,800 / 1.112 + $43,700 / 1.113

NPVI = $7,693.02

c. Using the profitability index to compare mutually exclusive projects can be ambiguous when the

15. a. The payback period for each project is:

A: 3 + ($110,000 / $325,000) = 3.34 years

B: 1 + ($18,300 / $19,900) = 1.92 years

The payback criterion implies accepting Project B, because it pays back sooner than Project A.

b. The NPV for each project is:

A: NPV = –$235,000 + $29,000 / 1.13 + $45,000 / 1.132 + $51,000 / 1.133 + $325,000 / 1.134

NPV = $60,579.46

c. The IRR for each project is:

A: $235,000 = $29,000 / (1 + IRR) + $45,000 / (1 + IRR)2 + $51,000 / (1 + IRR)3

+ $325,000 / (1 + IRR)4

Using a spreadsheet, financial calculator, or trial and error to find the root of the equation, we find

that:

IRR decision rule implies we accept Project B because IRR for B is greater than IRR for A.

d. The profitability index for each project is:

A: PI = ($29,000 / 1.13 + $45,000 / 1.132 + $51,000 / 1.133 + $325,000 / 1.134) / $235,000

PI = 1.258

16. a. The IRR for each project is:

M: $150,000 = $68,600 / (1 + IRR) + $76,800 / (1 + IRR)2 + $71,300 / (1 + IRR)3

+ $40,500 / (1 + IRR)4

Using a spreadsheet, financial calculator, or trial and error to find the root of the equation, we find

that:

b. The NPV for each project is:

M: NPV = –$150,000 + $68,600 / 1.15 + $76,800 / 1.152 + $71,300 / 1.153 + $40,500 / 1.154

NPV = $37,760.92

c. Accept Project N since the NPV is higher. IRR cannot be used to rank mutually exclusive

projects.

17. a. The profitability index for each project is:

Y: PI = ($19,800 / 1.12 + $17,500 / 1.122 + $20,700 / 1.123 + $14,600 / 1.124) / $43,400

PI = 1.282

b. The NPV for each project is:

Y: NPV = –$43,400 + $19,800 / 1.12 + $17,500 / 1.122 + $20,700 / 1.123 + $14,600 / 1.124

NPV = $12,241.88

c. Accept Project Z since the NPV is higher. The profitability index cannot be used to rank mutually

exclusive projects.

18. To find the crossover rate, we subtract the cash flows from one project from the cash flows of the other

project, and find the IRR of the differential cash flows. We will subtract the cash flows from Project J

from the cash flows from Project I. It is irrelevant which cash flows we subtract from the other.

Subtracting the cash flows, the equation to calculate the IRR for these differential cash flows is:

Crossover rate: 0 = $23,200 / (1 + R) + $5,600 / (1 + R)2 – $13,600 / (1 + R)3 – $26,200 / (1 + R)4

19. If the payback period is exactly equal to the project’s life then the IRR must be equal to zero since the

project pays back exactly the initial investment. If the project never pays back its initial investment,

then the IRR of the project must negative.

20. At a zero discount rate (and only at a zero discount rate), the cash flows can be added together across

time. So, the NPV of the project at a zero percent required return is:

NPV = –$745,382 + 265,381 + 304,172 + 225,153 + 208,614

NPV = $257,938

21. a. The payback period for each project is:

F: 2 + ($21,600 / $81,600) = 2.26 years

G: 3 + ($5,200 / $166,800) = 3.03 years

The payback criterion implies accepting Project F because it pays back sooner than Project G.

Project G does not meet the minimum payback of three years.

22. The MIRR for the project with all three approaches is:

Discounting approach:

In the discounting approach, we find the value of all cash outflows to Time 0, while any cash inflows

remain at the time at which they occur. So, discounting the cash outflows to Time 0, we find:

Using a spreadsheet, financial calculator, or trial and error to find the root of the equation, we find that:

MIRR = 19.21%

Reinvestment approach:

In the reinvestment approach, we find the future value of all cash except the initial cash flow at the

end of the project. So, reinvesting the cash flows to Time 5, we find:

Combination approach:

In the combination approach, we find the value of all cash outflows at Time 0, and the value of all

cash inflows at the end of the project. So, the value of the cash flows is:

Time 0 cash flow = –$27,500 – $4,050 / 1.105

Time 0 cash flow = –$30,014.73

Time 5 cash flow = $10,430(1.104) + $13,850(1.103) + $11,270(1.102) + $9,830(1.10)

Time 5 cash flow = $58,154.61

Intermediate

23. With different discounting and reinvestment rates, we need to make sure to use the appropriate interest

rate. The MIRR for the project with all three approaches is:

Discounting approach:

In the discounting approach, we find the value of all cash outflows to Time 0 at the discount rate, while

any cash inflows remain at the time at which they occur. So, discounting the cash outflows to Time 0,

we find:

Using a spreadsheet, financial calculator, or trial and error to find the root of the equation, we find that:

MIRR = 19.41%

Reinvestment approach:

In the reinvestment approach, we find the future value of all cash except the initial cash flow at the

end of the project using the reinvestment rate. So, reinvesting the cash flows to Time 5, we find:

Combination approach:

In the combination approach, we find the value of all cash outflows at Time 0 using the discount rate,

and the value of all cash inflows at the end of the project using the reinvestment rate. So, the value of

the cash flows is:

24. To find the crossover rate, we subtract the cash flows from one project from the cash flows of the other

project, and find the IRR of the differential cash flows. We will subtract the cash flows from Project

S from the cash flows from Project R. It is irrelevant which cash flows we subtract from the other.

Subtracting the cash flows, the equation to calculate the IRR for these differential cash flows is:

0 = $31,000 – $3,000 / (1 + R) – $1,000 / (1 + R)2 – $14,000 / (1 + R)3 – $21,000 / (1 + R)4

– $3,000 / (1 + R)5

Using a spreadsheet, financial calculator, or trial and error to find the root of the equation, we find that:

25. The IRR of the project is:

$91,000 = $55,000 / (1 + IRR) + $46,000 / (1 + IRR)2

Using a spreadsheet, financial calculator, or trial and error to find the root of the equation, we find that:

IRR = 7.47%

26. By definition, the profitability index is:

PI = Discounted Value of Future Cash Flows / Initial Cost

But note that the discounted value of future cash flows is just the NPV overstated by the neglected

initial costs, so:

27. a. To have a payback equal to the project’s life, given C is a constant cash flow for N years:

C = I/N

b. To have a positive NPV, I < C (PVIFAR%, N). Thus, C > I / (PVIFAR%, N).

Challenge

28. a. Here the cash inflows of the project go on forever, which is a perpetuity. Unlike ordinary

perpetuity cash flows, the cash flows here grow at a constant rate forever, which is a growing

perpetuity. If you remember back to the chapter on stock valuation, we presented a formula for

valuing a stock with constant growth in dividends. This formula is actually the formula for a

growing perpetuity, so we can use it here. The PV of the future cash flows from the project is:

b. Here we want to know the minimum growth rate in cash flows necessary to accept the project.

The minimum growth rate is the growth rate at which we would have a zero NPV. The equation

for a zero NPV, using the equation for the PV of a growing perpetuity, is:

0 = –$1,575,000 + $135,000 / (.12 – g)

29. The IRR is the interest rate that makes the NPV of the project equal to zero. So, the IRR of the project

is:

0 = $35,000 – $27,000 / (1 + IRR) + $29,000 / (1 + IRR)2

Even though it appears there are two IRRs, a spreadsheet, financial calculator, or trial and error will

not give an answer. The reason is that there is no real IRR for this set of cash flows. If you examine

30. First, we need to find the future value of the cash flows for the one year in which they are blocked by

the government. So, reinvesting each cash inflow for one year, we find:

Year 2 cash flow = $303,800(1.04) = $315,952

Year 3 cash flow = $219,700(1.04) = $228,488

Year 4 cash flow = $320,000(1.04) = $332,800

Year 5 cash flow = $288,700(1.04) = $300,248

So, the NPV of the project is:

Calculator Solutions

5.

CFo

–$168,500

C01

$86,000

F01

1

C02

$91,000

F02

1

C03

$53,000

1

IRR CPT

18.79%

6.

CFo

–$168,500

CFo

–$168,500

C01

$86,000

C01

$86,000

F01

1

F01

1

7.

CFo

–$8,450

CFo

–$8,450

CFo

–$8,450

C01

$2,145

C01

$2,145

C01

$2,145

F01

8

F01

8

F01

8

I = 8%

I = 24%

IRR CPT

NPV CPT

NPV CPT

19.13%

$3,876.54

–$1,111.48

8.

CFo

–$19,400

C01

$9,800

1

C02

$11,300

1

C03

$6,900

F03

1

IRR CPT

22.09%

9.

CFo

–$19,400

CFo

–$19,400

C01

$9,800

C01

$9,800

F01

1

F01

1

C02

$11,300

C02

$11,300

1

1

C03

$6,900

C03

$6,900

1

1

I = 0%

I = 10%

NPV CPT

NPV CPT

$8,600.00

$4,032.01

C02

$91,000

C02

$91,000

1

1

C03

$53,000

C03

$53,000

1

1

I = 9%

I = 21%

NPV CPT

NPV CPT

$27,917.69

–$5,354.28

CFo

–$19,400

CFo

–$19,400

C01

$9,800

C01

$9,800

F01

1

F01

1

10.

CF (A)

Cfo

–$78,500

CFo

–$78,500

C01

$43,000

C01

$43,000

F01

1

F01

1

C02

$29,000

C02

$29,000

F02

1

F02

1

C03

$23,000

C03

$23,000

F03

1

F03

1

C04

$21,000

C04

$21,000

F04

1

F04

1

CPT IRR

I = 11%

20.70%

NPV CPT

$14,426.54

CF (B)

CFo

–$78,500

CFo

–$78,500

C01

$21,000

C01

$21,000

F01

1

F01

1

C02

$28,000

C02

$28,000

F02

1

F02

1

C03

$34,000

C03

$34,000

F03

1

F03

1

C04

$41,000

C04

$41,000

F04

1

F04

1

CPT IRR

I = 11%

18.73%

NPV CPT

$15,012.82

C02

$11,300

C02

$11,300

F02

1

F02

1

C03

$6,900

C03

$6,900

F03

1

F03

1

I = 20%

I = 30%

NPV CPT

NPV CPT

$606.94

–$2,034.50

Crossover rate:

CFo

$0

C01

$22,000

F01

1

C02

$1,000

11.

CF (X)

CFo

–$23,400

CFo

–$23,400

C01

$13,100

C01

$13,100

F01

1

F01

1

C02

$9,480

C02

$9,480

F02

1

F02

1

C03

$7,890

C03

$7,890

F03

1

F03

1

I = 0%

I = 25%

NPV CPT

NPV CPT

$7,070

–$2,813.12

CF (Y)

CFo

–$23,400

CFo

–$23,400

C01

$9,200

C01

$9,200

F01

1

F01

1

C02

$10,620

C02

$10,620

F02

1

F02

1

C03

$11,180

C03

$11,180

F03

1

F03

1

I = 0%

I = 25%

NPV CPT

NPV CPT

$7,600

–$3,519.04

Crossover rate:

CFo

$0

C01

$3,900

F01

1

C02

–$1,140

F02

1

C03

–$3,290

F03

1

CPT IRR

7.62%

F02

1

C03

–$11,000

F03

1

C04

–$20,000

F04

1

CPT IRR

12.21%

12.

CFo

–$39,000,000

CFo

–$39,000,000

C01

$57,000,000

C01

$57,000,000

13.

CFo

$0

CFo

$0

CFo

$0

C01

$15,800

C01

$15,800

C01

$15,800

F01

1

F01

1

F01

1

C02

$13,600

C02

$13,600

C02

$13,600

F02

1

F02

1

F02

1

C03

$8,300

C03

$8,300

C03

$8,300

F03

1

F03

1

F03

1

I = 10%

I = 15%

I = 22%

NPV CPT

NPV CPT

NPV CPT

$31,839.22

$29,480.07

$26,659.02

@10%: PI = $31,839.22 / $27,500 = 1.158

@15%: PI = $29,480.07 / $27,500 = 1.072

@22%: PI = $26,659.02 / $27,500 = .969

14. a. The profitability indexes are:

CF (I)

CF (II)

CFo

$0

CFo

$0

C01

$28,300

C01

$9,600

F01

1

F01

1

C02

$34,800

C02

$17,400

F02

1

F02

1

C03

$43,700

C03

$15,600

F03

1

F03

1

I = 11%

I = 11%

NPV CPT

NPV CPT

$85,693.02

$34,177.46

F01

1

F01

1

C02

C02

F02

1

F02

1

I = 10

IRR CPT

NPV CPT

28.15%

$5,380,165.29

b. The NPV of each project is:

CF (I)

CF (II)

CFo

–$78,000

CFo

–$28,800

C01

$28,300

C01

$9,600

F01

1

F01

1

C02

$34,800

C02

$17,400

15.

CF (A)

CFo

–$235,000

CFo

–$235,000

CFo

$0

C01

$29,000

C01

$29,000

C01

$29,000

F01

1

F01

1

F01

1

C02

$45,000

C02

$45,000

C02

$45,000

1

1

1

C03

$51,000

C03

$51,000

C03

$51,000

1

1

1

C04

$325,000

C04

$325,000

C04

$325,000

F04

1

F04

1

F04

1

I = 13%

IRR CPT

I = 13%

NPV CPT

21.02%

NPV CPT

$60,579.46

$295,579.46

PI = $295,579.46 / $235,000 = 1.258

CF (B)

CFo

–$47,000

CFo

–$47,000

CFo

$0

C01

$28,700

C01

$28,700

C01

$28,700

F01

1

F01

1

F01

1

C02

$19,900

C02

$19,900

C02

$19,900

F02

1

F02

1

F02

1

C03

$17,300

C03

$17,300

C03

$17,300

F03

1

F03

1

F03

1

C04

$16,200

C04

$16,200

C04

$16,200

1

1

1

I = 13%

IRR CPT

I = 13%

NPV CPT

30.57%

NPV CPT

$15,908.38

$62,908.38

1

1

C03

$43,700

C03

$15,600

1

1

I = 11%

I = 11%

NPV CPT

NPV CPT

$7,693.02

$5,377.46

16.

Project M

CFo

–$150,000

CFo

–$150,000

C01

$68,600

C01

$68,600

F01

1

F01

1

C02

$76,800

C02

$76,800

F02

1

F02

1

Project N

CFo

–$372,000

CFo

–$372,000

C01

$159,300

C01

$159,300

F01

1

F01

1

C02

$193,200

C02

$193,200

F02

1

F02

1

C03

$154,800

C03

$154,800

F03

1

F03

1

C04

$110,400

C04

$110,400

F04

1

F04

1

CPT IRR

I = 15%

25.57%

NPV CPT

$77,513.77

17.

Project Y

CFo

$0

CFo

–$43,400

C01

$19,800

C01

$19,800

F01

1

F01

1

C02

$17,500

C02

$17,500

F02

1

F02

1

C03

$20,700

C03

$20,700

F03

1

F03

1

C04

$14,600

C04

$14,600

F04

1

F04

1

I = 12%

I = 12%

NPV CPT

NPV CPT

$55,641.88

$12,241.88

C03

$71,300

C03

$71,300

F03

1

F03

1

C04

$40,500

C04

$40,500

F04

1

F04

1

CPT IRR

I = 15%

27.82%

NPV CPT

$37,760.92

Project Z

CFo

$0

CFo

–$78,000

C01

$32,000

C01

$32,000

F01

1

F01

1

C02

$30,100

C02

$30,100

PI = $90,914.13 / $78,000 = 1.166

18.

CFo

$0

C01

$23,200

F01

1

C02

$5,600

F02

1

C03

F03

1

C04

F04

1

CPT IRR

14.06%

20.

CFo

–$745,382

CFo

–$745,382

C01

$265,381

C01

$265,381

F01

1

F01

1

C02

$304,172

C02

$304,172

F02

1

F02

1

C03

$225,153

C03

$225,153

F03

1

F03

1

C04

$208,614

C04

$208,614

F04

1

F04

1

I = 0

IRR CPT

NPV CPT

13.79%

$257,938

F02

1

F02

1

C03

$29,500

C03

$29,500

F03

1

F03

1

C04

$27,300

C04

$27,300

F04

1

F04

1

I = 12%

I = 12%

NPV CPT

NPV CPT

$90,914.13

$12,914.13

21. b.

Project F

Project G

CFo

–$180,000

CFo

–$280,000

C01

$93,600

C01

$64,800

F01

1

F01

1

C02

$64,800

C02

$86,400

F02

1

F02

1

24. Crossover rate:

CFo

$31,000

C01

–$3,000

F01

1

C02

–$1,000

F02

1

C03

–$14,000

F03

1

C04

–$21,000

F04

1

C05

–$3,000

F05

1

IRR CPT

9.24%

Project R

Project S

CFo

–$45,000

CFo

–$76,000

C01

$17,000

C01

$20,000

F01

1

F01

1

C02

$19,000

C02

$20,000

F02

1

F02

1

C03

$21,000

C03

$35,000

F03

1

F03

1

C04

$9,000

C04

$30,000

F04

1

F04

1

C05

$7,000

C05

$10,000

F05

1

F05

I = 9.24%

I = 9.24%

NPV CPT

NPV CPT

$13,414.39

$13,414.39

C03

$81,600

C03

$123,600

F03

1

F03

1

C04

$72,000

C04

$166,800

F04

1

F04

1

C05

$64,800

C05

$187,200

F05

1

F05

1

I = 10%

I = 10%

NPV CPT

NPV CPT

$109,364.59

$173,339.68

25.

CFo

$91,000

C01

–$55,000

F01

1

C02

–$46,000

F02

1

IRR CPT

7.47%

CFo

$91,000

CFo

$91,000

CFo

$91,000

C01

–$55,000

C01

–$55,000

C01

–$55,000

F01

1

F01

1

F01

1

C02

–$46,000

C02

–$46,000

C02

–$46,000

F02

1

F02

1

F02

1

I = 0%

I = 10%

I = 24%

NPV CPT

NPV CPT

NPV CPT

–$10,000

$2,983.47

$16,728.41