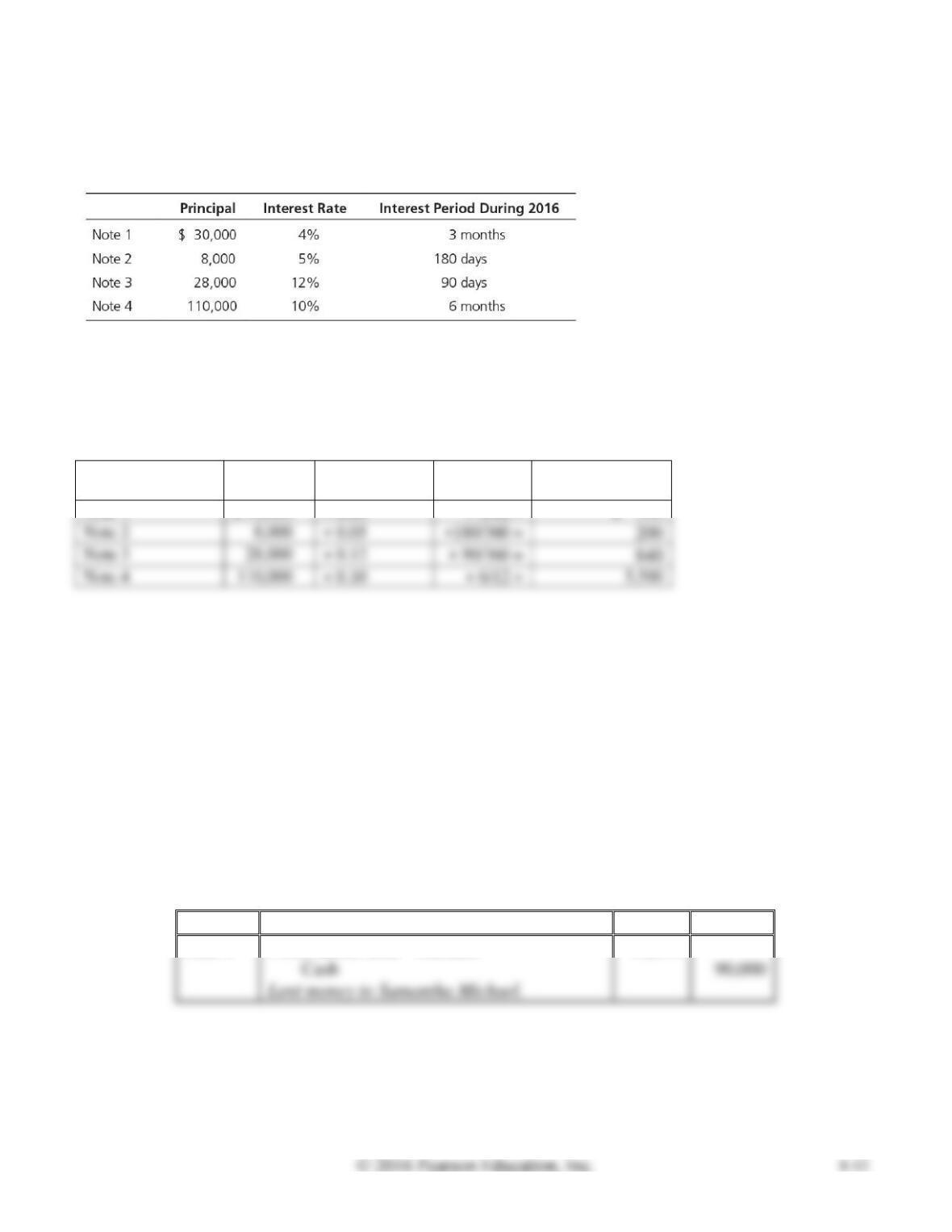

Chapter 8

Receivables

Review Questions

1. What is the difference between accounts receivable and notes receivable?

Accounts receivable represent the right to receive cash in the future from customers for goods sold

2. List some common examples of other receivables, besides accounts receivable and notes receivable.

3. What is a critical element of internal control in the handling of receivables by a business? Explain

how this element is accomplished.

A critical element of internal control is the separation of cash-handling and cash-accounting duties.

4. When dealing with receivables, give an example of a subsidiary account.

5. What type of account must the sum of all subsidiary accounts be equal to?

The balance in all the subsidiary accounts receivable accounts must equal the total balance of the

control account, Accounts Receivable.

6. What are some benefits to a business in accepting credit cards and debit cards?

7. What are two common methods used when accepting deposits for credit card and debit card

transactions?

Two common methods for deposits of proceeds from credit card sales are the net method and the

8. What occurs when a business factors its receivables?

When a business factors its receivables, it sells its receivables to a finance company or bank (often

9. What occurs when a business pledges its receivables?

In a pledging situation, a business uses its receivables as security for a loan. The business borrows

10. What is the expense account associated with the cost of uncollectible receivables called?

Bad Debts Expense is the account associated with the cost of the uncollectible receivables.

11. When is bad debts expense recorded when using the direct write-off method?

12. What are some limitations of using the direct write-off method?

13. When is bad debts expense recorded when using the allowance method?

Under the allowance method, bad debts expense is estimated and recorded in the same period as the

14. When using the allowance method, how are accounts receivable shown on the balance sheet?

Under the allowance method, accounts receivable are shown at the net realizable value. Net

15. When using the allowance method, what account is debited when writing off uncollectible accounts?

How does this differ from the direct write-off method?

16. When a receivable is written off under the allowance method, how does it affect the net realizable

value shown on the balance sheet?

17. How does the percent-of-sales method compute bad debts expense?

The percent-of-sales method computes bad debts expense as a percentage of net credit sales.

18. How do the percent-of-receivables and aging-of-receivables methods compute bad debts expense?

In both the percent-of-receivables method and aging-of-receivables method, the business determines

19. What is the difference between the percent-of-receivables and aging-of-receivables methods?

20. What is the formula to compute interest on a note receivable?

The formula for computing interest is as follows: Amount of interest = Principal × Interest rate ×

Time.

21. Why must companies record accrued interest revenue at the end of the accounting period?

The interest revenue earned on the note up to year-end is part of that year’s earnings. Interest

22. How is the acid-test ratio calculated, and what does it signify?

23. What does the accounts receivable turnover ratio measure, and how is it calculated?

24. What does the days’ sales in receivables indicate, and how is it calculated?

Days’ sales in receivables, also called the collection period, indicates how many days it takes to

Short Exercises

S8-1 Ensuring internal control over the collection of receivables

Learning Objective 1

Consider internal control over receivables collections. What job must be withheld from a company’s

credit department in order to safeguard its cash? If the credit department does perform this job, what can

a credit department employee do to hurt the company?

SOLUTION

The company’s credit department should not take customer payments or have any other cash-handling

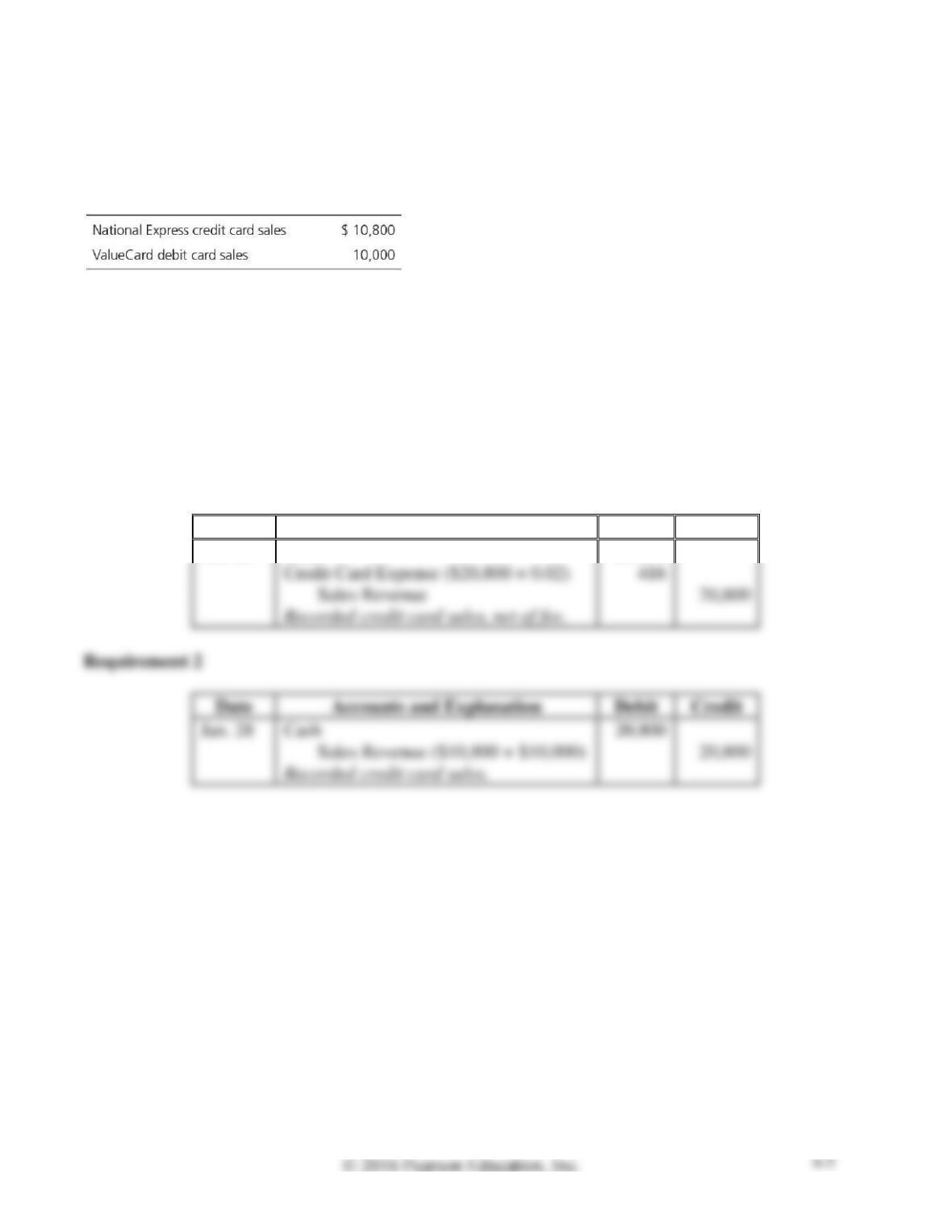

S8-2 Recording credit card and debit card sales

Learning Objective 1

Restaurants do a large volume of business by credit and debit cards. Suppose Summer, Sand, and

Castles Resort restaurant had these transactions on January 28, 2016:

Requirements

1. Suppose Summer, Sand, and Castles Resort’s processor charges a 2% fee and deposits sales net of

the fee. Journalize these sales transactions for the restaurant.

2. Suppose Summer, Sand, and Castles Resort’s processor charges a 2% fee and deposits sales using

the gross method. Journalize these sales transactions for the restaurant.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Jan. 28

Cash

20,384

Credit Card Expense ($20,800 × 0.02)

Date

Accounts and Explanation

Debit

Credit

Jan. 28

Cash

20,800

S8-3 Applying the direct write-off method to account for uncollectibles

Learning Objective 2

Susan Knoll is an attorney in Los Angeles. Knoll uses the direct write-off method to account for

uncollectible receivables.

At January 31, 2016, Knoll’s accounts receivable totaled $18,000. During February, she earned revenue

of $21,000 on account and collected $23,000 on account. She also wrote off uncollectible receivables of

$1,050 on February 29, 2016.

Requirements

1. Use the direct write-off method to journalize Knoll’s write-off of the uncollectible receivables.

2. What is Knoll’s balance of Accounts Receivable at February 29, 2016?

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Feb. 29

Bad Debts Expense

1,050

23,000 collected

S8-4 Collecting a receivable previously written off—direct write-off method

Learning Objective 2

Gate City Cycles had trouble collecting its account receivable from Shawna Brown. On June 19, 2016,

Gate City finally wrote off Brown’s $700 account receivable. On December 31, Brown sent a $700

check to Gate City.

Journalize the entries required for Gate City Cycles, assuming Gate City uses the direct write-off

method.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

2016

Jun. 19

Bad Debts Expense

700

Accounts Receivable—Brown

700

Wrote off receivable.

Accounts Receivable—Brown

700

Bad Debts Expense

700

Cash

700

Accounts Receivable—Brown

700

S8-5 Applying the allowance method to account for uncollectibles

Learning Objective 3

The Accounts Receivable balance and Allowance for Bad Debts for Turning Leaves Furniture

Restoration at December 31, 2015, was $10,800 and $2,000 (credit balance). During 2016, Turning

Leaves completed the following transactions:

Requirements

1. Journalize Turning Leaves’s transactions for 2016 assuming Turning Leaves uses the allowance

method.

2. Post the transactions to the Accounts Receivable, Allowance for Bad Debts, and Bad Debts Expense

T-accounts, and determine the ending balance of each account.

3. Show how accounts receivable would be reported on the balance sheet at December 31, 2016.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2016

a.

Accounts Receivable

265,800

Sales Revenue

265,800

Cash

220,000

220,000

c.

Allowance for Bad Debts

Bad Debts Expense

Requirement 2

2,000 12/31/15, Bal

wrote off 6,100

5,000 expense

900 12/31/16, Bal

expense 5,000

Requirement 3

TURNING LEAVES FURNITURE RESTORATION

Balance Sheet−Partial

December 31, 2016

Current Assets:

Accounts Receivable

$ 50,500

(900)

$ 49,600

Accounts Receivable

12/31/15, Bal 10,800

220,000 collected

revenue 265,800

6,100 wrote off

12/31/16, Bal 50,500

S8-6 Applying the allowance method (percent-of-sales) to account for uncollectibles

Learning Objective 3

During its first year of operations, Signature Lamp Company earned net credit sales of

$314,000. Industry experience suggests that bad debts will amount to 4% of net credit sales. At

December 31, 2016, accounts receivable total $45,000. The company uses the allowance method to

account for uncollectibles.

Requirements

1. Journalize Signature’s Bad Debts Expense using the percent-of-sales method.

2. Show how to report accounts receivable on the balance sheet at December 31, 2016.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

S8-7 Applying the allowance method (percent-of-receivables) to account for uncollectibles

Learning Objective 3

The Accounts Receivable balance for Field, Inc. at December 31, 2015, was $25,000. During 2016,

Field earned revenue of $457,000 on account and collected $326,000 on account. Field wrote off $5,900

receivables as uncollectible. Industry experience suggests that uncollectible accounts will amount to 4%

of accounts receivable.

Requirements

1. Assume Field had an unadjusted $2,300 credit balance in Allowance for Bad Debts at December 31,

2016. Journalize Field’s December 31, 2016, adjustment to record bad debts expense using the

percent-of-receivables method.

2. Assume Field had an unadjusted $1,900 debit balance in Allowance for Bad Debts at December 31,

2016. Journalize Field’s December 31, 2016, adjustment to record bad debts expense using the

percent-of-receivables method.

SOLUTION

Requirement 1

Dec. 31

Bad Debts Expense

($150,100 × 4% = $6,004; $6,004 – $2,300 = $3,704)

Dec. 31

Bad Debts Expense

($150,100 × 4% = $6,004; $6,004 + $1,900 = $7,904)

12/31/16, Bal 150,100

Accounts Receivable

12/31/15, Bal 25,000

326,000 collected

revenue 457,000

5,900 wrote off

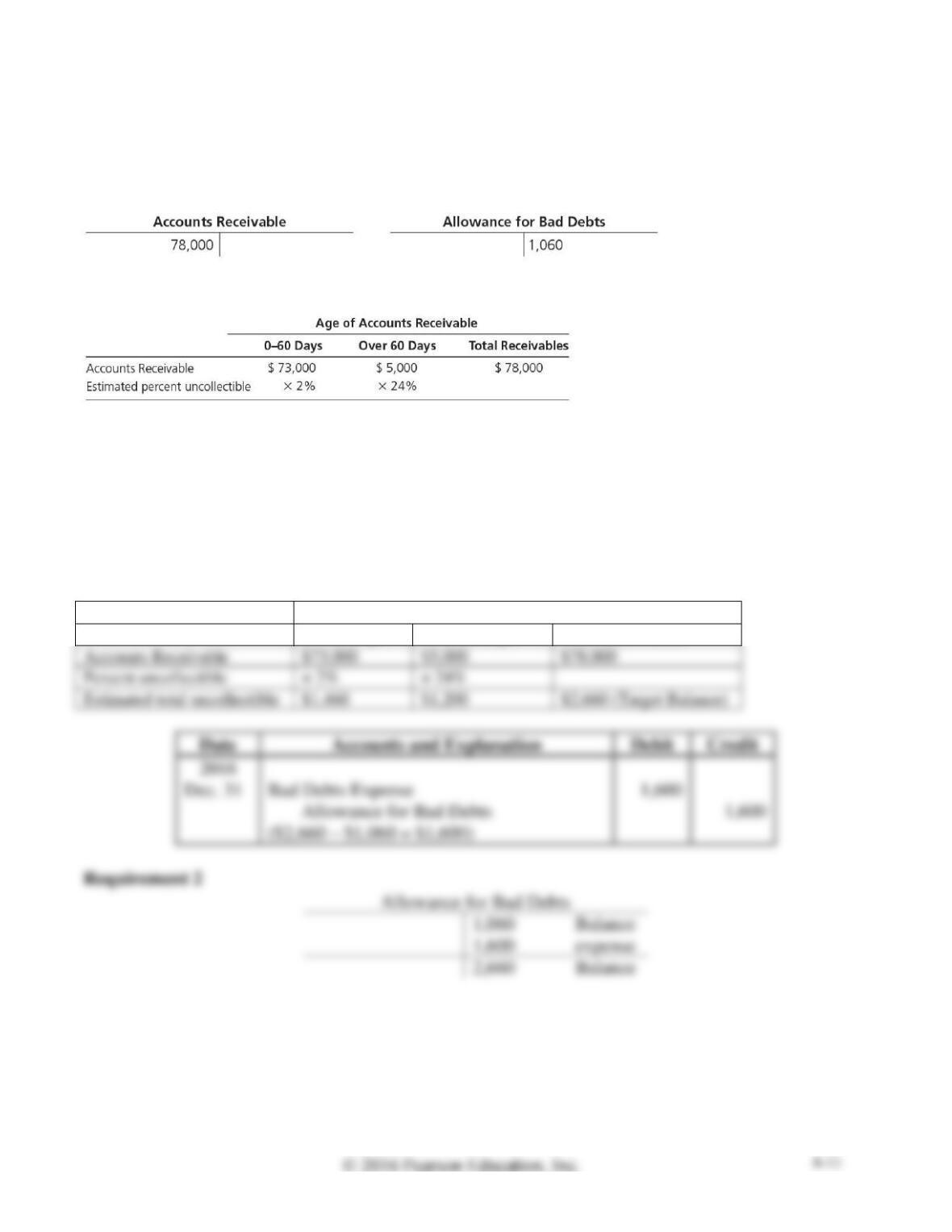

S8-8 Applying the allowance method (aging-of-receivables) to account for uncollectibles

Learning Objective 3

World Class Work Shoes had the following balances at December 31, 2016, before the year-end

adjustments:

The aging of accounts receivable yields the following data:

Requirements

1. Journalize World Class’s entry to record bad debts expense for 2016 using the aging-of-receivables

method.

2. Prepare a T-account to compute the ending balance of Allowance for Bad Debts.

SOLUTION

Requirement 1

Age of Accounts Receivable

0 – 60 Days

Over 60 Days

Total Receivables

Percent uncollectible

× 24%

Dec. 31

Bad Debts Expense

1,060 Balance

1,600 expense

2,660 Balance

S8-9 Computing interest amounts on notes receivable

Learning Objective 4

A table of notes receivable for 2016 follows:

For each of the notes receivable, compute the amount of interest revenue earned during 2016. Round to

the nearest dollar.

SOLUTION

Principal

Interest Rate

Interest

Period

Interest Revenue

Earned

Note 1

$ 30,000

× 0.04

× 3/12 =

$ 300

S8-10 Accounting for a note receivable

Learning Objective 4

On June 6, Southside Bank & Trust lent $90,000 to Samantha Michael on a 60-day, 6% note.

Requirements

1. Journalize for Southside the lending of the money on June 6.

2. Journalize the collection of the principal and interest at maturity. Specify the date.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

June 6

Notes Receivable—Michael

90,000

S8-10, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Aug. 5

Cash ($90,000 + $900)

90,900

S8-11 Accruing interest revenue and recording collection of a note

Learning Objective 4

On December 1, Kole Corporation accepted a 120-day, 6%, $17,000 note receivable from J. Peterman in

exchange for his account receivable.

Requirements

1. Journalize the transaction on December 1.

2. Journalize the adjusting entry needed on December 31 to accrue interest revenue.

3. Journalize the collection of the principal and interest at maturity. Specify the date.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Dec. 1

Notes Receivable—Peterman

17,000

Date

Debit

Credit

Dec. 31

Interest Receivable

Date

Debit

Credit

Mar. 31

Cash ($17,000 + $85 + $255)

17,340

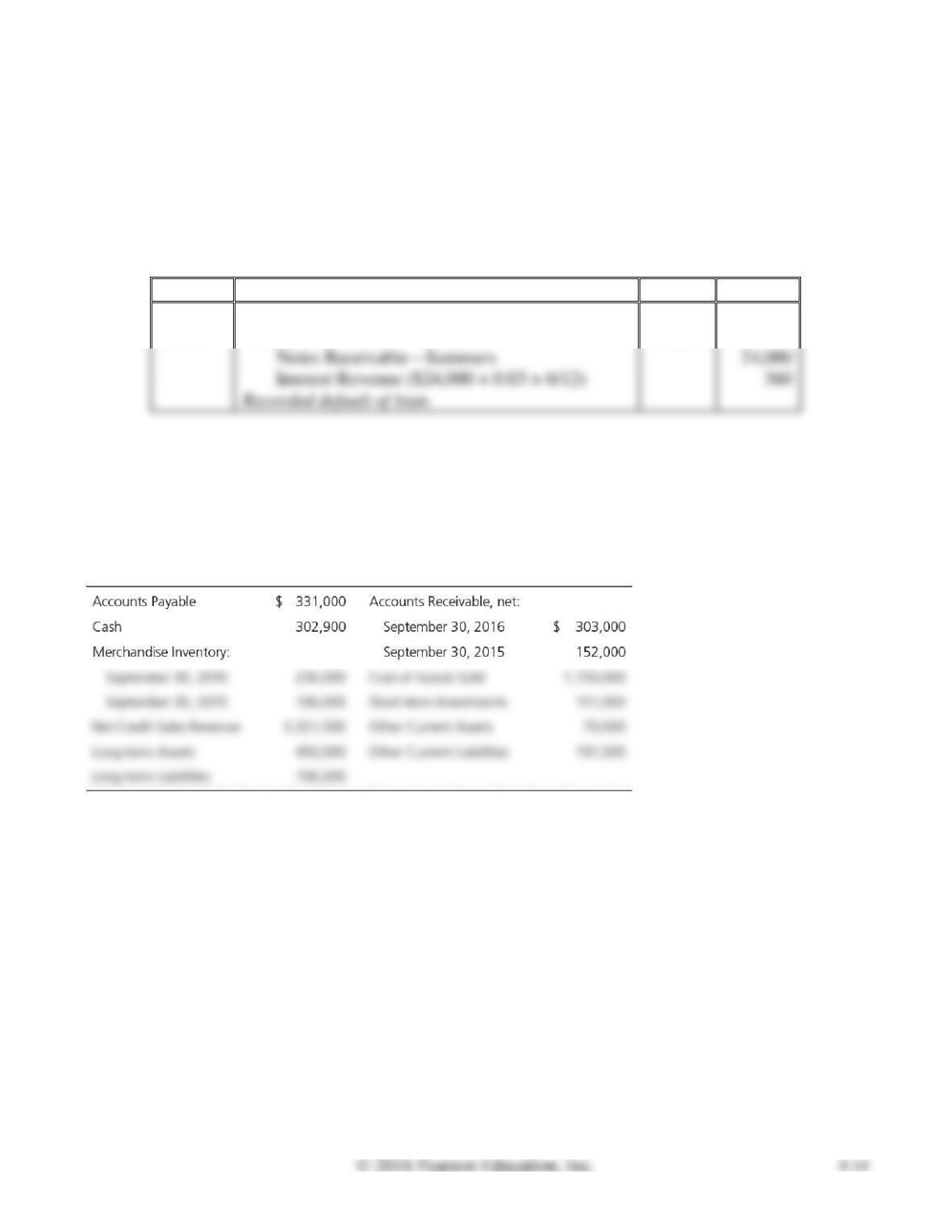

S8-12 Recording a dishonored note receivable

Learning Objective 4

Midway Corporation has a six-month, $24,000, 3% note receivable from L. Summers that was signed on

June 1, 2016. Summers defaults on the loan on December 1.

Journalize the entry for Midway to record the default of the loan.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

2016

Dec. 1

Accounts Receivable—Summers

24,360

S8-13 Using the acid-test ratio, accounts receivable turnover ratio, and days’ sales in receivables to

evaluate a company

Learning Objective 5

Gold Clothiers reported the following selected items at September 30, 2016 (last year’s—2015—

amounts also given as needed):

Compute Gold’s (a) acid–test ratio, (b) accounts receivable turnover ratio, and (c) days’ sales in

receivables for 2016. Evaluate each ratio value as strong or weak. Gold sells on terms of net 30. (Round

days’ sales in receivables to a whole number.)

SOLUTION

a) Acid-test ratio = (Cash including cash equivalents + Short-term investments + Net current

receivables) / Total current liabilities

= ($302,900 + $151,000 + $303,000) / ($331,000 + $191,000)

Exercises

E8-14 Defining common receivables terms

Learning Objective 1

Match the terms with their correct definition.

SOLUTION

1.

F

2.

E

4.

C

6.

B

E8-15 Identifying and correcting internal control weakness

Learning Objective 1

Suppose The Right Rig Dealership is opening a regional office in Omaha. Cary Regal, the office

manager, is designing the internal control system. Regal proposes the following procedures for credit

checks on new customers, sales on account, cash collections, and write-offs of uncollectible receivables:

• The credit department runs a credit check on all customers who apply for credit. When an account

proves uncollectible, the credit department authorizes the write-off of the accounts receivable.

• Cash receipts come into the credit department, which separates the cash received from the customer

remittance slips. The credit department lists all cash receipts by customer name and amount of cash

received.

• The cash goes to the treasurer for deposit in the bank. The remittance slips go to the accounting

department for posting to customer accounts.

• The controller compares the daily deposit slip to the total amount posted to customer accounts. Both

amounts must agree.

Recall the components of internal control. Identify the internal control weakness in this situation, and

propose a way to correct it.

SOLUTION

The internal control weakness is that the credit department receives incoming cash from customers.

E8-16 Journalizing transactions using the direct write-off method

Learning Objectives 1, 2

On June 1, High Performance Cell Phones sold $19,000 of merchandise to Andrew Trucking Company

on account. Andrew fell on hard times and on July 15 paid only $7,000 of the account receivable. After

repeated attempts to collect, High Performance finally wrote off its accounts receivable from Andrew on

September 5. Six months later, March 5, High Performance received Andrew’s check for $12,000 with a

note apologizing for the late payment.

Requirements

1. Journalize the transactions for High Performance Cell Phones using the direct write-off method.

Ignore Cost of Goods Sold.

2. What are some limitations that High Performance will encounter when using the direct write-off

method?

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

June 1

Accounts Receivable—Andrew Trucking Company

19,000

Sales Revenue

19,000

Record sales on account.

Cash

7,000

Accounts Receivable—Andrew Trucking Company

Record payment on account.

Bad Debts Expense

12,000

Accounts Receivable—Andrew Trucking Company

12,000

Wrote-off account balance.

Mar. 5

Accounts Receivable—Andrew Trucking Company

12,000

Bad Debts Expense

12,000

Reinstated previously written off account.

Cash

12,000

Accounts Receivable—Andrew Trucking Company

12,000

Collected cash on account.

Requirement 2

High Performance will encounter limitations with the direct write-off method because it violates the

matching principle. The matching principle requires that the expense of uncollectible accounts be

Use the following information to answer Exercises E8-17 and E8-18.

At January 1, 2016, Hilly Mountain Flagpoles had Accounts Receivable of $31,000, and Allowance for

Bad Debts had a credit balance of $3,000. During the year, Hilly Mountain Flagpoles recorded the

following:

a. Sales of $174,000 ($157,000 on account; $17,000 for cash). Ignore Cost of Goods Sold.

b. Collections on account, $131,000.

c. Write-offs of uncollectible receivables, $2,200.

E8-17 Accounting for uncollectible accounts using the allowance method (percent-of-sales) and

reporting receivables on the balance sheet

Learning Objectives 1, 3

2. AR, Dec. 31 $54,800

Requirements

1. Journalize Hilly’s transactions that occurred during 2016. The company uses the allowance method.

2. Post Hilly’s transactions to the Accounts Receivable and Allowance for Bad Debts T-accounts.

3. Journalize Hilly’s adjustment to record bad debts expense assuming Hilly estimates bad debts as 4%

of credit sales. Post the adjustment to the appropriate T-accounts.

4. Show how Hilly Mountain Flagpoles will report net accounts receivable on its December 31, 2016,

balance sheet.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2016

a.

Accounts Receivable

157,000

Cash

17,000

Sales Revenue

174,000

Cash

131,000

131,000

c.

Allowance for Bad Debts

Requirement 2

revenue 157,000

2,200 wrote off

Accounts Receivable

1/1 Bal 31,000

131,000 collected

E8-17, cont.

Requirement 3

Date

Accounts and Explanation

Debit

Credit

2016

Dec. 31

Bad Debts Expense

6,280

3,000 1/1 Bal

wrote off 2,200

800 Unadj. Bal

7,080 12/31Bal

1/1 Bal 0

12/31 exp. 6,280

12/31 Bal 6,280

Requirement 4

HILLY MOUNTAIN FLAGPOLES

Balance Sheet−Partial

December 31, 2016

Current Assets:

Accounts Receivable

$ 47,720

E8-18 Accounting for uncollectible accounts using the allowance method (percent-of-receivables)

and reporting receivables on the balance sheet

Learning Objectives 1, 3

3. Bad Debts Expense $844

Requirements

1. Journalize Hilly’s transactions that occurred during 2016. The company uses the allowance method.

2. Post Hilly’s transactions to the Accounts Receivable and Allowance for Bad Debts T-accounts.

3. Journalize Hilly’s adjustment to record bad debts expense assuming Hilly estimates bad debts as 3%

of accounts receivable. Post the adjustment to the appropriate T-accounts.

4. Show how Hilly Mountain Flagpoles will report net accounts receivable on its December 31, 2016,

balance sheet.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

2016

a.

Accounts Receivable

157,000

Cash

Cash

131,000

c.

Allowance for Bad Debts

Requirement 2

3,000 1/1 Bal

800 12/31 Unadj.Bal

Accounts Receivable

1/1 Bal 31,000

131,000 collected