8-1

CHAPTER 8

Operating Assets: Property, Plant,

and Equipment, and Intangibles

OVERVIEW OF EXERCISES, PROBLEMS, AND CASES

Estimated

Time in

Learning Objectives Exercises Minutes Level

Module 1

1. Understand balance sheet disclosures for 11* 30 Mod

operating assets.

2. Determine the acquisition cost of an operating asset. 1 10 Easy

Module 2

5. Compare depreciation methods and understand the factors 3 20 Mod

affecting the choice of method. 4 15 Mod

12* 5 Easy

8. Analyze the effect of the disposal of an asset at a gain or loss. 6 15 Mod

7 15 Mod

Module 3

9. Understand the balance sheet presentation of intangible assets. 13* 10 Mod

13* 10 Mod

Module 4

11. Explain the impact that long-term assets have on the statement 9 5 Mod

of cash flows. 10 5 Mod

8-2 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

Problems Estimated

and Time in

Learning Objectives Alternates Minutes Level

Module 1

1. Understand balance sheet disclosures for

operating assets. 6* 30 Mod

2. Determine the acquisition cost of an operating asset. 7* 15 Diff

Module 2

5. Compare depreciation methods and understand the factors 2 10 Easy

affecting the choice of method. 3 15 Mod

6* 30 Mod

7* 15 Diff

8# 20 Mod

Module 3

9. Understand the balance sheet presentation of intangible assets. 6** 30 Mod

11* 20 Diff

Module 4

11. Explain the impact that long-term assets have on the statement 4 15 Mod

of cash flows. 5 40 Diff

10* 35 Mod

11* 20 Diff

CHAPTER 8 • OPERATING ASSETS: PROPERTY, PLANT, AND EQUIPMENT, AND INTANGIBLES 8-3

Estimated

Time in

Learning Objectives Cases Minutes Level

Module 1

1. Understand balance sheet disclosures for 1* 20 Mod

operating assets. 2* 20 Mod

3* 20 M

Module 2

5. Compare depreciation methods and understand the factors 3* 20 Mod

affecting the choice of method. 4 25 Mod

6 15 Mod

Module 3

9. Understand the balance sheet presentation of intangible assets. 1* 20 Mod

2* 20 Mod

Module 4

11. Explain the impact that long-term assets have on the statement

of cash flows.

8-4 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISES

LO 2 EXERCISE 8-1 ACQUISITION COST

The acquisition cost of the asset should be computed as follows:

List price ………………………………………………………………………….. $60,000

Discount of 2% ………………………………………………………………….. (1,200)

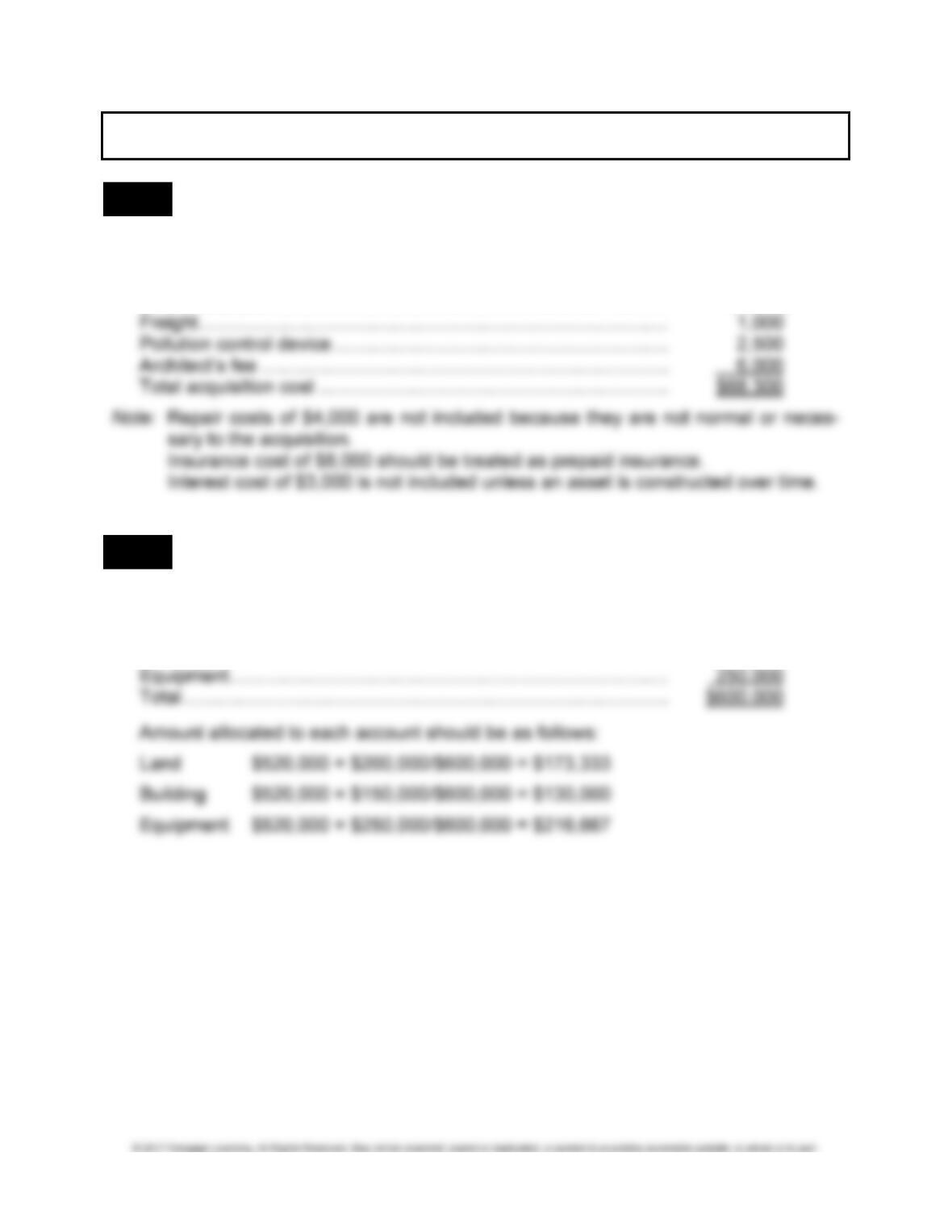

LO 3 EXERCISE 8-2 LUMP-SUM PURCHASE

1. The total market value is calculated as follows:

Land ………………………………………………………………………………… $200,000

Building ……………………………………………………………………………. 150,000

CHAPTER 8 • OPERATING ASSETS: PROPERTY, PLANT, AND EQUIPMENT, AND INTANGIBLES 8-5

EXERCISE 8-2 (Concluded)

The journal entry would be as follows:

Journal Jan. 1 Land ……………………………………………………. 173,333

Entry Building ……………………………………………….. 130,000

Analysis Equipment ……………………………………………. 216,667

Build-

ing 130,000

Equip-

ment

216,667

Cash

(520,000)

2. The amount of depreciation expense that should be recorded for 2016 is as follows:

Land = $0

3. The assets would appear on the balance sheet as follows:

Long-term assets:

8-6 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

LO 5 EXERCISE 8-3 STRAIGHT-LINE AND UNITS-OF-PRODUCTION METHODS

Depreciation, accumulated depreciation, and book value for the straight-line method

should be as follows:

Annual Accumulated Book

Year Depreciation Depreciation Value

2016 $10,800* $10,800 $49,200

*($60,000 – $6,000)/5 years = $10,800 per year

The estimated total number of units to be produced is

10,000 + 20,000 + 30,000 + 40,000 + 50,000 = 150,000 units.

Annual Accumulated Book

Year Depreciation Depreciation Value

2016 10,000 × $0.36 = $ 3,600 $ 3,600 $56,400

2017 20,000 × $0.36 = 7,200 10,800 49,200

CHAPTER 8 • OPERATING ASSETS: PROPERTY, PLANT, AND EQUIPMENT, AND INTANGIBLES 8-7

LO 5 EXERCISE 8-4 ACCELERATED DEPRECIATION

1. Accumulated Book Value

Year Annual Depreciation Depreciation at end of Yr. 1 becomes

beginning Yr. 2 and so on

2016 40%* × $6,000 = $2,400 $2,400 $3,600

2.

Journal Dec. 31 Depreciation Expense ……………………………. 2,400

Entry Accumulated Depreciation …………………. 2,400

3. Koffman may believe that the double-declining-balance method best matches the

decline in usefulness of the asset with the revenues produced by the asset. Koffman

may also choose this method because it allows more depreciation to be taken in the

early years of the asset life and thus delays taxes until the later years.

8-8 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 6 EXERCISE 8-5 CHANGE IN ESTIMATE

1. Depreciation, accumulated depreciation, and book value for the straight-line method

should be as follows:

Accumulated

Year Depreciation Depreciation Book Value

2016 $ 8,000* $ 8,000 $72,000

2017 8,000 16,000 64,000

*($80,000 – $8,000)/9 years = $8,000

**$64,000 – $2,000 = $62,000

$62,000/4 years = $15,500

Depreciation = Remaining Depreciable Amount/Remaining Life

Depreciation = $62,000/4 years

= $15,500

2. Depreciation for 2016 and 2017 was not wrong. The company used the best infor-

mation available at that time to develop its estimate of depreciation. The information

CHAPTER 8 • OPERATING ASSETS: PROPERTY, PLANT, AND EQUIPMENT, AND INTANGIBLES 8-9

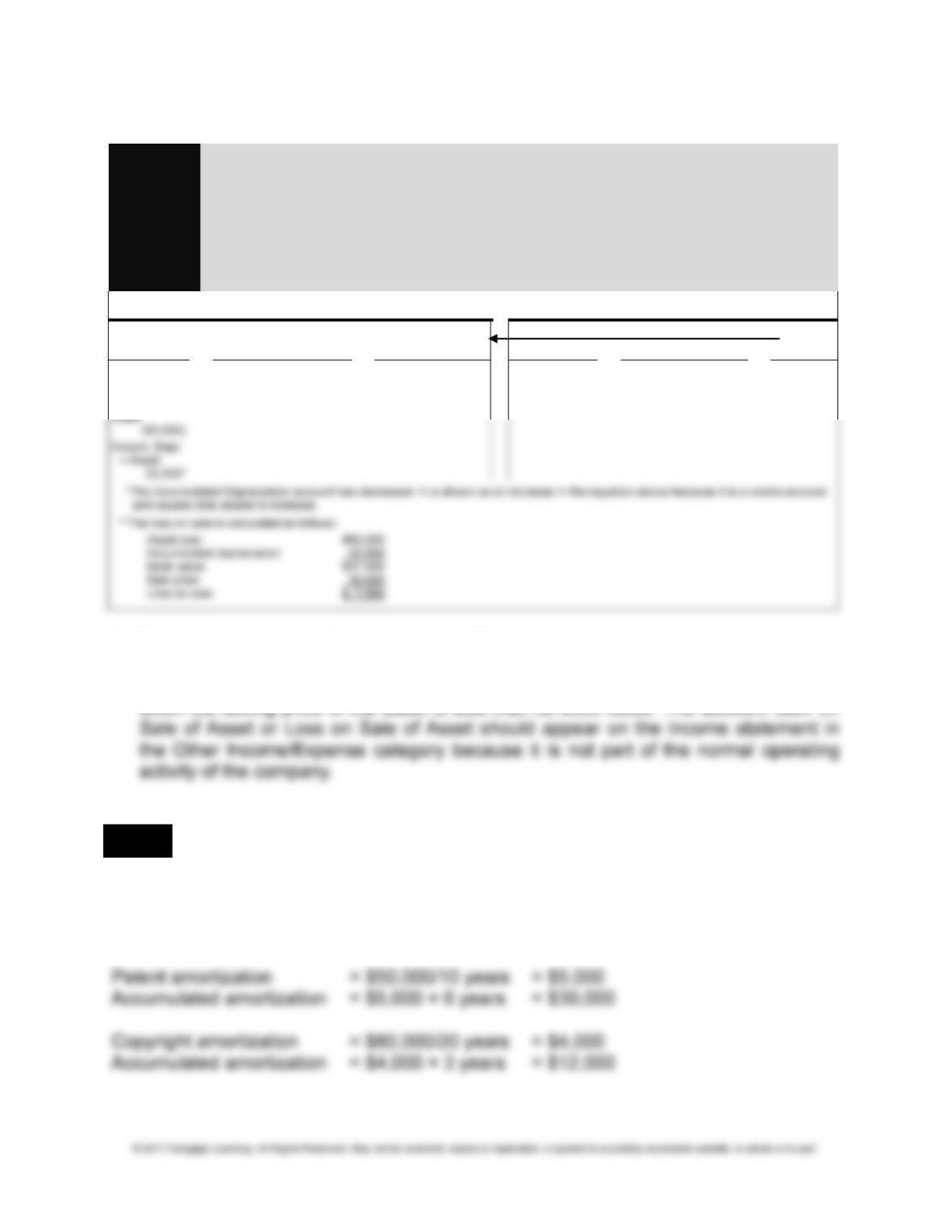

LO 8 EXERCISE 8-6 ASSET DISPOSAL

1.

Journal July 1 Depreciation Expense ……………………………. 4,500

Entry Accumulated Depreciation—Asset ……… 4,500

Analysis To record depreciation of asset to July 1 for ½ year 2016.

($60,000 – $6,000)/6 years = $9,000 per year.

causes total assets to decrease.

Journal July 1 Cash ……………………………………………………. 40,000

Entry Accumulated Depreciation—Asset …………… 22,500*

Analysis Asset ………………………………………………. 60,000

Gain on Sale of Asset ……………………….. 2,500**

8-10 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISE 8-6 (Concluded)

The depreciation for 2016 is calculated as follows:

($60,000 – $6,000)/6 years = $9,000 per year

$9,000 × 6/12 = $4,500 for 2016

2. The gain or loss should appear in the Other Income category of the income state-

ment to indicate that it is not part of the normal operating activity of the company. A

gain occurs when the selling price of the asset exceeds its book value. A loss occurs

activity of the company.

LO 8 EXERCISE 8-7 ASSET DISPOSAL

1.

Journal July 1 Depreciation Expense ……………………………. 4,500

Entry Accumulated Depreciation—Asset ……… 4,500

Analysis To record depreciation to July 1 for ½ year 2016.

($60,000 – $6,000)/6 years = $9,000 per year.

$9,000 × 6/12 = $4,500.

Balance Sheet Income Statement

CHAPTER 8 • OPERATING ASSETS: PROPERTY, PLANT, AND EQUIPMENT, AND INTANGIBLES 8-11

EXERCISE 8-7 (Concluded)

Journal July 1 Cash ……………………………………………………. 15,000

Entry Note Receivable ……………………………………. 15,000

Analysis Accumulated Depreciation—Asset …………… 22,500

Loss on Sale of Asset ……………………………. 7,500

Asset ………………………………………………. 60,000

To record sale of the asset.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash 15,000

Note Receiv-

able 15,000

(7,500)

Loss on Sale

of Asset 7,500**

(7,500)

2. The gain or loss should appear in the Other Income category of the income state-

ment to indicate that it is not part of the normal operating activity of the company. A

gain occurs when the selling price of the asset exceeds its book value. A loss occurs

LO 10 EXERCISE 8-8 AMORTIZATION OF INTANGIBLES

Trademark is not amortized because it has an indefinite life.

Amortization expense = $0

Accumulated amortization = $0

8-12 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

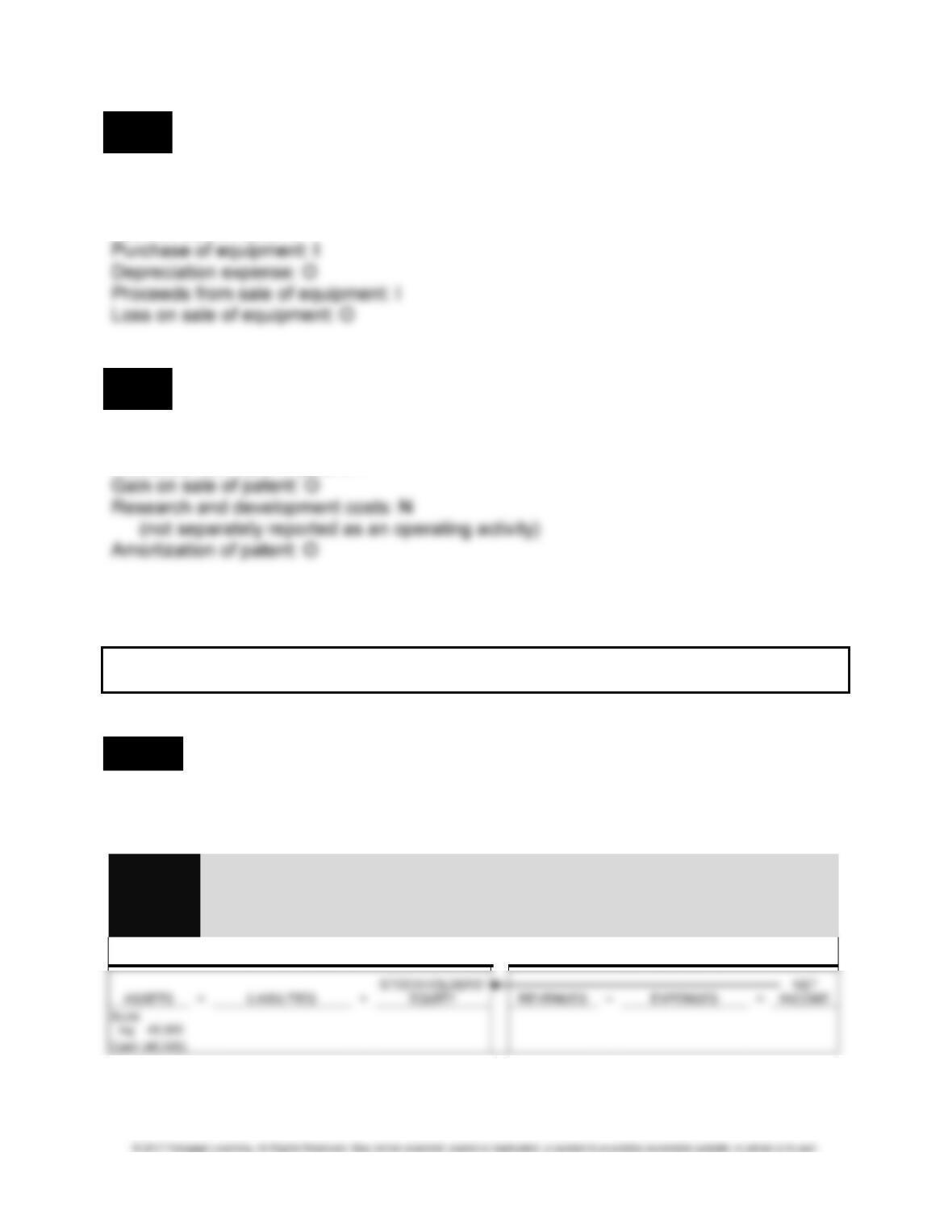

LO 11 EXERCISE 8-9 IMPACT OF TRANSACTIONS INVOLVING OPERATING ASSETS ON

STATEMENT OF CASH FLOWS

Purchase of land: I

Proceeds from sale of land: I

Gain on sale of land: O

LO 11 EXERCISE 8-10 IMPACT OF TRANSACTIONS INVOLVING INTANGIBLE ASSETS

ON STATEMENT OF CASH FLOWS

Cost incurred to acquire copyright: I

Proceeds from sale of patent: I

MULTI-CONCEPT EXERCISES

LO 1,7 EXERCISE 8-11 CAPITAL VERSUS REVENUE EXPENDITURES

1. The following entries should be made to capitalize costs:

Jan. 1

Journal Building ……………………………………………………….. 40,000

Entry Cash ……………………………………………………… 40,000

Analysis To record cost of new conveyor system.

Balance Sheet Income Statement

CHAPTER 8 • OPERATING ASSETS: PROPERTY, PLANT, AND EQUIPMENT, AND INTANGIBLES 8-13

EXERCISE 8-11 (Continued)

Journal Delivery Truck ………………………………………………. 5,000

Entry Cash ……………………………………………………… 5,000

Analysis To record cost of hydraulic lift installed on truck.

2. The entry to record depreciation should be as follows:

Journal Dec. 31 Depreciation Expense ……………………………. 14,322

Entry Accumulated Depreciation—Building …… 9,739

Analysis Accumulated Depreciation—Truck ……… 4,583

To record 2016 depreciation.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Accum. Depr.

—Building

(9,739)*

(14,322)

Depreciation

Expense 14,322

(14,322)

The depreciation for 2016 should be calculated as follows:

Building Truck

Original cost …………………………………………………… $200,000 $20,000

Depreciation for 2014 and 2015 ………………………… (16,000)* (6,667)**

Book value …………………………………………………….. $184,000 $13,333

Capitalized costs …………………………………………….. 40,000 5,000

8-14 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISE 8-11 (Concluded)

3. The assets should appear on the 2016 balance sheet as follows:

Building …………………………………………………………. $240,000

Accumulated depreciation ………………………………… 25,739* $214,261

LO 4,5 EXERCISE 8-12 CAPITALIZATION OF INTEREST AND DEPRECIATION

1. $200,000 + $8,000 = $208,000

LO 9,10 EXERCISE 8-13 RESEARCH AND DEVELOPMENT AND PATENTS

a. All research and development costs should be treated as an expense. The 2016 in-

come statement should reflect an expense of $20,000.

b. Patent costs should be treated as an asset. The 2016 balance sheet should reflect a

Patent account of $10,000 – ($10,000/5 years) = $8,000.

CHAPTER 8 • OPERATING ASSETS: PROPERTY, PLANT, AND EQUIPMENT, AND INTANGIBLES 8-15

PROBLEMS

LO 3 PROBLEM 8-1 LUMP-SUM PURCHASE OF ASSETS AND SUBSEQUENT EVENTS

1. Relative fair values:

Section 1 ……………………………………………………….. $ 630,000 50%

Section 2 ……………………………………………………….. 378,000 30

2. The purchase of the land has no effect on total assets. Current assets (cash) de-

clines and long-term assets (land) increases and, therefore, only the composition of

assets on the balance sheet is changed.

3. Carter would be concerned with the value assigned to each section if it intended to

LO 5 PROBLEM 8-2 DEPRECIATION AS A TAX SHIELD

If the asset is not purchased, the company must pay income tax of $50,000 × 35% =

$17,500.

If the asset is purchased, the company should record depreciation of $20,000 per

8-16 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 5 PROBLEM 8-3 BOOK VERSUS TAX DEPRECIATION

1. Year Straight-Line – MACRS = Difference

1 $ 5,600* $ 6,720 $(1,120)

2 5,600 10,750 (5,150)

2. The president is correct that a total of $33,600 will be deducted as depreciation un-

der either method over the six-year life. However, the memo should stress that all

other things being equal, Griffith should prefer MACRS for taxes, since it results in

the payment of less income tax during the early years in the life of the truck. Money

LO 11 PROBLEM 8-4 DEPRECIATION AND CASH FLOW

1. O’HARE COMPANY

INCOME STATEMENT

2. The amount of the net cash inflow for 2016 is $100,000.

3. The amount of the net income ($85,000) does not equal the amount of the net cash

inflow ($100,000) because of depreciation expense. Depreciation is an expense on

CHAPTER 8 • OPERATING ASSETS: PROPERTY, PLANT, AND EQUIPMENT, AND INTANGIBLES 8-17

PROBLEM 8-4 (Concluded)

4. If O’hare develops a cash flow statement using the indirect method, the Operating

category should appear as follows:

LO 11 PROBLEM 8-5 RECONSTRUCT NET BOOK VALUES USING STATEMENT OF CASH

FLOWS

1. Book value of equipment at time of sale:

Book value …………………………………………………………. $ X

Book value of copyright at time of sale:

Book value …………………………………………………………. $ X

2. Net book value of property, plant, and equipment at December 31, 2015:

Net book value at 12/31/15 …………………………………… $ X

3. Net book value of intangibles at December 31, 2015:

Net book value at 12/31/15 …………………………………… $ X

Payment of legal fees during 2016 ………………………… 15,000

Book value of copyright sold during 2016 ……………….. (20,000)**

2016 amortization ……………………………………………….. (33,000)

8-18 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

MULTI-CONCEPT PROBLEMS

LO 1,3,5,7,8 PROBLEM 8-6 COST OF ASSETS, SUBSEQUENT BOOK VALUES, AND

BALANCE SHEET PRESENTATION

1. Values assigned to each asset:

a. Value at time of purchase: $14,000 + $4,800 = $18,800

b. Allocation of purchase price:

2. Depreciation or other expense recorded for each asset during 2016:

a. ($18,800 – $800)/4 years = $4,500

b. Supplies expense $150

Depreciation of office furniture $450/9 years = 50

Depreciation of equipment $1,800/4 years = 450

3. Balance Sheet Presentation:

Current assets:

Prepaid license expense ($1,500 – $458) ………….. $ 1,042

Property, plant, and equipment:

CHAPTER 8 • OPERATING ASSETS: PROPERTY, PLANT, AND EQUIPMENT, AND INTANGIBLES 8-19

LO 2,5 PROBLEM 8-7 COST OF ASSETS AND THE EFFECT ON DEPRECIATION

2. Reported income in Year 1 is $51,500 ($100,000 – $16,500 – $25,000 – $4,000 –

$3,000). Reported income should be $80,300 ($100,000 – $19,700).

LO 5,7,8 PROBLEM 8-8 CAPITAL EXPENDITURES, DEPRECIATION, AND DISPOSAL

1. The entry to record depreciation for 2015 is as follows:

Journal Dec. 31 Depreciation Expense ……………………………. 14,000

Entry Accumulated Depreciation—Building …… 14,000

Analysis To record depreciation for 2015.

($364,000 – $14,000)/25 = $14,000.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Accum. Depr.

—Building*

(14,000) (14,000)

Depreciation

Expense 14,000

(14,000)

*The Accumulated Depreciation account has increased. It is shown as a decrease in the equation above because it is a contra account and

causes total assets to decrease.

8-20 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 8-8 (Continued)

Journal Jan. 1 Building ……………………………………………….. 42,000

Entry Cash ………………………………………………. 42,000

Analysis To record pollution control equipment.

Balance Sheet Income Statement

The depreciation for 2015 should be calculated as follows:

($364,000 – $14,000)/25 years = $14,000 for 2015.

The depreciation for 2016 should be calculated as follows:

Original cost ………………………………………………….. $ 364,000

2015 depreciation …………………………………………… (14,000)

Journal Dec. 31 Depreciation Expense ……………………………. 12,600

Entry Accumulated Depreciation—Building …… 12,600

Analysis To record depreciation for 2016.

Balance Sheet Income Statement

2. The pollution control equipment extended the life of the asset and should be capital-

ized rather than expensed. It is difficult to determine whether Merton would rather