Accounting Information Systems, 10e 1

SOLUTIONS FOR CHAPTER 8

Each end-of-chapter question in the Solutions Manual is tagged to correspond with AACSB, AICPA

and CISA standards, allowing professors to more easily manage the task of reporting outcomes to these

professional and accrediting bodies. Please see the corresponding spreadsheet file for the tagging

information.

Discussion Questions

DQ 8-1 “The Enterprise Risk Management (ERM) framework introduced in Chapter 7

can be used by management to make decisions on which controls in this chapter

should be implemented.” Do you agree? Discuss fully.

ANS. Several issues might be included in an answer to this question. Here are some of

those issues:

DQ 8-2 “In small companies with few employees, it is virtually impossible to implement

the segregation of duties control plan.” Do you agree? Discuss fully.

ANS. Obviously, whether one agrees or disagrees with the statement depends on how

few “few” employees actually are. (Forty-seven percent of all U.S. employers

2 Solutions for Chapter 8

DQ 8-3 “No matter how sophisticated a system of internal control is, its success

ultimately requires that you place your trust in certain key personnel.” Do you

agree? Discuss fully.

ANS. Yes and no. We say no because we believe that a control system should monitor

the quantity, quality, and legitimacy of each employee’s work. Procedures should

DQ 8-4 “If personnel hiring is done correctly, the other personnel control plans are not

needed.” Do you agree? Discuss fully.

Accounting Information Systems, 10e 3

ANS. Emphatically no. While sound hiring practices are a crucial personnel policy,

employees can change over time. An employee’s need for ongoing training might

not be addressed (a personnel development control plan), or they may become

DQ 8-5 “Monitoring must be performed by an independent function such as a CPA.” Do

you agree? Discuss fully.

ANS. All internal controls need to be reviewed periodically to determine that they

continue to function effectively and efficiently. This review may be one of three

types.

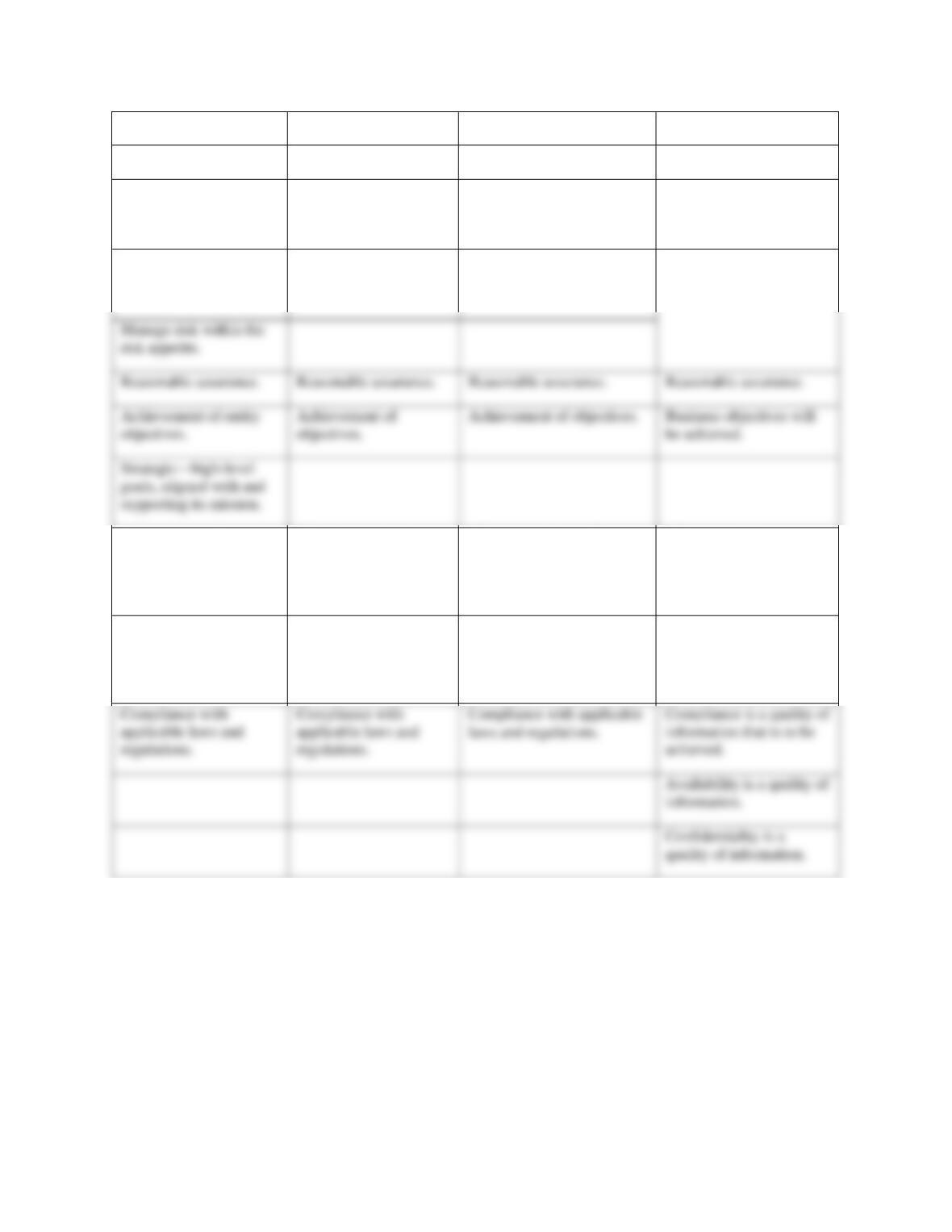

DQ 8-6 Compare and contrast the COBIT definition of control in this chapter with

definitions in Chapter 7 for ERM, the COSO definition of internal control, and

this textbook’s definition of internal control.

ANS. Some common elements, and some differences, are summarized in the following

table:

ERM

COSO

Textbook

COBIT

4 Solutions for Chapter 8

ERM

COSO

Textbook

COBIT

personnel.

personnel.

Applied in strategy

setting and across the

enterprise.

Identify potential events

that may affect the

entity.

Undesired events will be

prevented or detected and

corrected.

Operations—efficient

and effective use of

resources.

Effectiveness and

efficiency of operations.

Effectiveness and efficiency

of operations.

Effectiveness and

efficiency are qualities of

information that are to be

achieved.

Reliability of reporting.

Reliability of financial

reporting.

Reliability of reporting.

Reliability of information

and integrity are qualities

of information that are to

be achieved.

Compliance with

applicable laws and

regulations.

Compliance with

applicable laws and

regulations.

Compliance with applicable

laws and regulations.

Compliance is a quality of

information that is to be

achieved.

Availability is a quality of

information.

Confidentiality is a

quality of information.

DQ 8-7 According to ISACA, COBIT 5 is taking IT control in a “new direction.” Discuss aspects

of this new direction and state your opinion as to how radically new COBIT 5.

Manage risk within the

risk appetite.

Achievement of entity

objectives.

Achievement of

objectives.

Achievement of objectives.

Business objectives will

be achieved.

goals, aligned with and

supporting its mission.

Accounting Information Systems, 10e 5

ANS This can be answered in a couple of different ways. First, one might focus on the big

picture of COBIT 5. In this approach, the answer should include and discuss: (1) COBIT

DQ 8-8 A key control concern described in Table 8.2 regarding the systems development

manager is that “systems development can develop and implement systems

without management approval.” Discuss a control described in this chapter that

reduces the risk that unauthorized systems will be implemented.

ANS. Program change controls address this risk. As depicted in Figure 8.6, any new or

revised programs must go through three sets of hands. First, a programmer must

DQ 8-9 Debate the following point: “Business continuity planning is really an IT issue.”

ANS. Yes. IT needs to ensure the continued operation of IT, one of the organization’s

major resources.

DQ 8-10 “Contracting for a hot site is too cost-prohibitive except in the rarest of

circumstances. Therefore, the vast majority of companies should think in terms of

providing for a cold site at most.” Discuss fully.

ANS. The key discussion point in this question should be the trade-off between timely

recovery of critical business functions on the one hand and the cost of providing

6 Solutions for Chapter 8

DQ 8-11 “Preventing the unauthorized disclosure and loss of data has become almost

impossible. Employees and others can use iPods, flash drives, cameras, and

PDAs, such as BlackBerries and Treos, to download data and remove it from an

organization’s premises.” Do you agree? Describe some controls from this

chapter that might be applied to reduce the risk of data disclosure and loss for

these devices.

ANS. These devices can certainly be used to circumvent physical access controls and

logical access controls, such as physically restricting access to a computer facility,

capability to write to portable storage devices.

DQ 8-12 Your boss was heard to say, “If we implemented every control plan discussed in

this chapter, we’d never get any work done around here.” Do you agree? Discuss

fully.

ANS. Yes and no. In rebutting your boss’s statement, you could point out at least two

things:

1. The authors never intended that the plans be applied to all situations in all

companies. Some are appropriate for some environments, whereas others are

Accounting Information Systems, 10e 7

unnecessary, and cost-prohibitive.

Also, because over-control has the potential to encourage unwanted, negative

behavioral reactions, it often can be as injurious to an organization as can

under-control. Employees may rebel at controls that they perceive as unduly

constraining or distasteful. Their rebellion might well manifest itself in petty

acts of fraud, thievery, or other forms of covert and overt resistance.

3. Balancing effectiveness and efficiency: This topic was also mentioned in

Chapter 7, when the authors talked about controls being built in rather than

built on. Controls impose some overhead on a firm. Therefore, management

must attempt to integrate the control system as seamlessly as possible with the

work system so that normal operations are not unduly burdened or impeded.

DQ 8-13 For each of these control plans suggest a monitoring activity:

8 Solutions for Chapter 8

a. Credit approval

ANS. A list of new customers for the last month and the supporting documentation used

to approve credit reviewed by the CFO.

Short Problems

SP 8-1 ANS.

Control Situation

Control Plan

1.

A

2.

E

3.

4.

D

5.

SP 8-2 ANS.

Control Situation

Control Plan

1.

F

2.

B

4.

E

Accounting Information Systems, 10e 9

SP 8-3 ANS.

1. CAEMWLVGPE, A becomes C by adding 2, C becomes A by subtracting 2, C

SP 8-4 ANS. Students’ solutions will vary, of course. At a minimum, each answer should

SP 8-5 ANS. The following summarise the major changes in COBIT 5. Note that not all of

these are in the textbook summary. They can be found at various websites, e.g.,

ww.isaca.org/COBIT/Documents/COBIT5-Compare-With-4.1.ppt, accessed May 7, 2013.

o New GEIT Principles

o Increased Focus on Enablers

SP 8-6 ANS. This can be found on page 19 (Figures 5 and 6) of

C

O

B

I

T

5: A Business

Framework for the Governance and Management of Enterprise IT. COBIT 5

Problems

P 8-1 ANS.

Note: This problem and solution were adopted from Thomas Wailgum, “Security: 50-Cent

Holes,” CIO Magazine, October 15, 2005.

A.

The personal information can be used to perpetrate identify theft. Releasing the data

may violate privacy laws and regulations. To prevent this problem, train employees and

10 Solutions for Chapter 8

D.

The information on the laptop can be used to perpetrate identify theft. Releasing the

data may violate privacy laws and regulations. To prevent this problem, management

should perform risk assessment to determine what data must be protected and then

implement security policies based on that assessment. Security protection may include

password protection, encrypted data, and biometric access.

E.

of passwords that individuals must create and remember.

The information on the backup disks can be used to perpetrate identify theft and execute

fraudulent credit card charges. Releasing the data may violate privacy laws and

regulations and subject the company to financial loss as it indemnifies customers for

any losses. To prevent this problem, the credit card company should send the data

encrypted and electronically.

the policy by taking disciplinary action against those violating the policy. Management

might consider scanning messages for violation of the policy. For example, systems can

scan for messages with 16-digit numbers (i.e., credit card numbers).

A hacker, or any individual for that matter, could use the passwords to access computer

systems and cause many kinds of problems. To prevent this problem, establish an

organization-wide policy prohibiting the creation and storage of electronic files listing

passwords. Educate employees as to the importance of this policy, and enforce the

policy by taking disciplinary action against those violating the policy (assumes that

network files are scanned on a regular basis, looking for files that violate the policy).

Management might consider implementing single sign-on systems to reduce the number

H.

The account information can be used to steal funds from the individuals’ accounts and

to perpetrate identify theft. To prevent this problem, establish an organization-wide

policy specifying who can access what information, how they can access it, and how

often. Then implement the policy through library controls and access control software to

limit employee access to data. An employee education program about the importance of

this policy should be conducted.

her transmissions. The data accessed in this manner can be used for a variety of

fraudulent activities or to create a competitive advantage. To prevent this problem,

employees need to be trained on how to set up and secure (passwords, firewall,

antivirus, etc.) a wireless network. Perhaps the organization can provide assistance to

employees to ensure their proper installation.

the consumer-grade IM with an enterprise-grade system.

Accounting Information Systems, 10e 11

P 8-2 ANS.

P & D 1.

P & D 11.

P 2.

P & C 12.

P 3.

P & D 13.

C 4.

P 14.

C 5.

P & D 15.

C 6.

P 16.

P & C 7.

C 17.

P 8.

P 18.

P & D 9.

P & D 19.

P 10.

P & D 20.

Note: We have offered multiple possibilities for answers to some of the preceding

items:

• Item 1: Library controls will manage access to programs and data and thus

prevent unauthorized access. These controls also log all uses of programs and

data and thus can detect any unauthorized uses that may take place.

authorized users for authorized purposes.

handing in the cell phone.

12 Solutions for Chapter 8

P 8-3 ANS.

Control Situation

Control Plan

1.

H

2.

F

3.

B

4.

5.

C

6.

J

7.

I

8.

L

9.

K

10.

E

P 8-4 ANS.

Option

Manager

Matthew

Mark

1

No

No

No

2

No

Yes

No

3

No

No

5

No

No

6

Yes

7

Yes

Explanation:

Accounting Information Systems, 10e 13

Option 1, vendor data maintenance, should be performed by the purchasing office. By doing so,

we separate authorization to engage in business with a particular vendor from the approval to

create accounts payable records and to disburse payments.

P 8-5 ANS.

Employee

Function

Grant

1, 6, 7

Jordyn

2, 3, 10

James

4, 5, 8, 9

Comment: The preceding solution represents but one of many possible solutions.

Our primary goal in solving this problem should be to segregate the handling of

P 8-6 ANS.

14 Solutions for Chapter 8

Domain

Process

Plans

Plan and Organize Domain

Establish Strategic Vision for

Information Technology

An inventory of IT

capabilities

Statement of IT goals and

Develop and Acquire IT

Solutions

An assessment of how new

hardware might affect existing

hardware

Application documentation

Integrate IT Solutions into

A process for testing a new

Manage Changes to Existing

IT Systems

A process to select and

prioritize user requests for

system changes

Program change testing

Deliver and Support Domain

Deliver Required IT Services

Define service levels

Ensure Security and

Complete a disaster recovery

Biometric security devices

User training classes

Processes

Perform preventive

maintenance

strategies

Communicate, and Manage

Realization of the Strategic

Vision

the IT department

A quality assurance plan

Feasibility studies

Accounting Information Systems, 10e 15

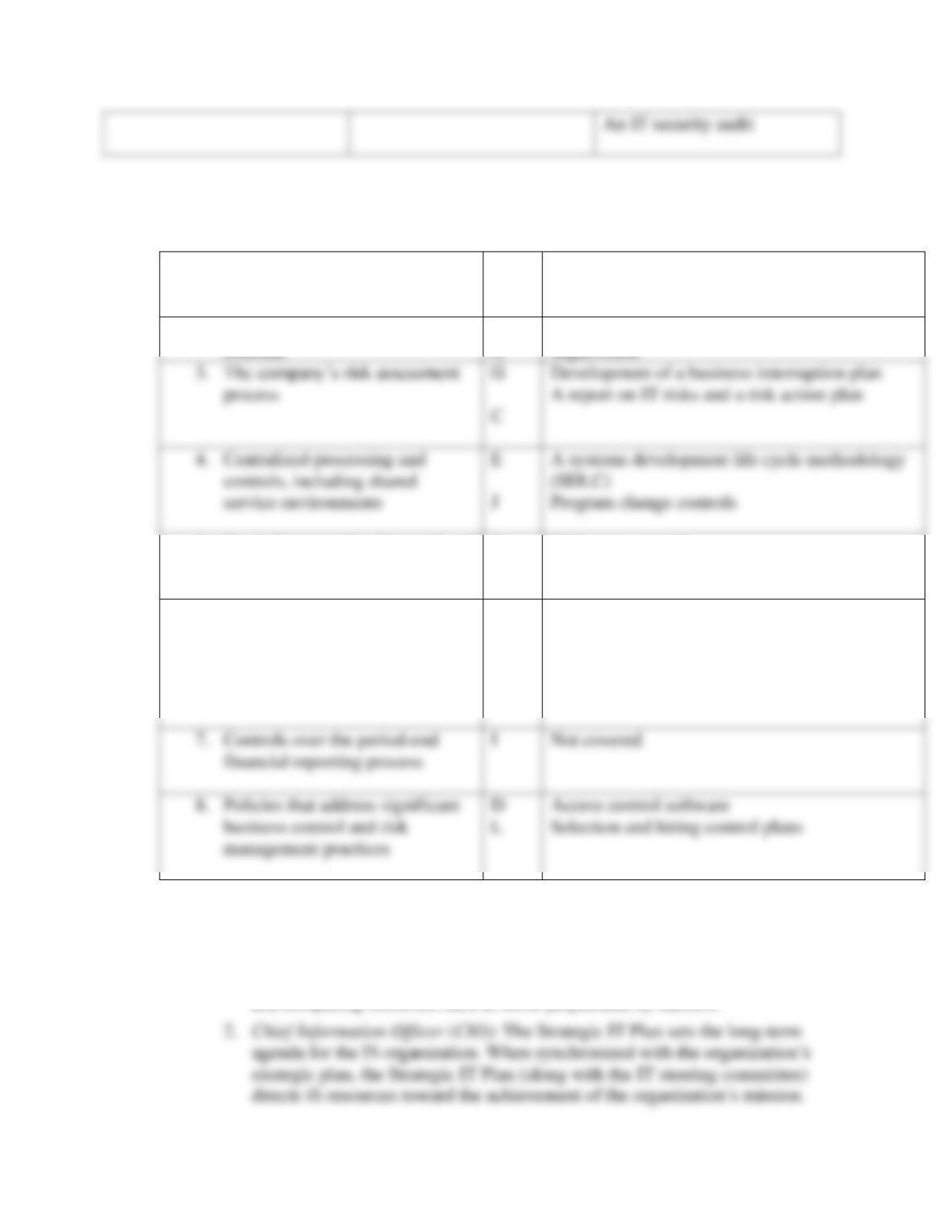

P 8-7 ANS.

1. Controls related to the control

environment

H

O

Establishment of a code of conduct

Use of control frameworks such as COBIT and

COSO

2. Controls over management

K

Segregation of duties

5. Controls to monitor the results of

operations

F

M

Budgetary controls

Service level agreements and reporting

processes

6. Controls to monitor other

controls, including activities of

the internal audit function, the

audit committee and self-

assessment programs

B

A

A report of all employees not taking required

vacation days

A file of signed code of conduct letters

7. Controls over the period-end

financial reporting process

I

Not covered

P 8-8 ANS.

1. Security officer: Business continuity planning can help an organization

recover quickly from natural disasters such as hurricanes and losses of data

and computing resources such as those perpetrated by hackers.

16 Solutions for Chapter 8

P 8-9 ANS. Student solutions will vary, of course. At a minimum, each answer should include

(1) a description of the incident(s), with background; (2) how long the site(s) were

not available; (3) how they came to be out of service; (4) which controls would

have prevented, detected, or corrected the outages; and (5) sources.

P 8-10 ANS. Student solutions will vary, of course. At a minimum, each answer should include

(1) a description of the incident(s), with background; (2) how long the site(s) were

P 8-11 ANS. As of this writing, the main Web page for Trust Services Principles and Criteria is

found at

Accounting Information Systems, 10e 17

• Privacy. Personal information is collected, used, retained, disclosed,

and destroyed in conformity with the commitments in the entity’s privacy

notice and with criteria set forth in generally accepted privacy principles

issued by the AICPA and CICA.

P 8-12 ANS. The 34 high level processes of COBIT 4.1 are:

In the “Plan and Organize” domain:

PO1 Define a Strategic IT Plan and direction

PO2 Define the Information Architecture

PO3 Determine Technological Direction

In the “Acquire and Implement” domain:

AI1 Identify Automated Solutions

AI2 Acquire and Maintain Application Software

AI3 Acquire and Maintain Technology Infrastructure

AI4 Enable Operation and Use

AI5 Procure IT Resources

AI6 Manage Changes

AI7 Install and Accredit Solutions and Changes

DS9 Manage the Configuration

DS10 Manage Problems

DS11 Manage Data

DS12 Manage the Physical Environment

DS13 Manage Operations

Here are the changes from 4.1 to 5:

Summary of changes between COBIT 4.1 and COBIT 5

Processes in COBIT 4.1 that are merged in COBIT 5

DS7 is merged with PO7 (Education and Human

Resources)

and Information Security)

Processes in COBIT 4.1 that are reassigned in COBIT 5

ME4 to EDM1, 2, 3, 4, 5 (Governance)

Processes in CobiT® 4.1 that are relocated in COBIT 5

PO1 to APO2 (Strategic Planning)

PO4 to APO1 (Organisation, Relationships and

Processes)