CHAPTER 8

Accounting for Receivables

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

1. Explain how companies

recognize accounts

receivable.

1, 2, 3

1, 2

1

1, 2

1A, 6A, 7A

disposition.

9, 10, 11

8

9

4A, 5A, 6A,

3. Explain how companies

recognize notes

receivable.

12, 13, 14,

9, 10, 11

3

10, 11, 12, 13

6A, 7A

and present and analyze

receivables.

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Prepare journal entries related to bad debt expense.

Simple

15–20

2A

Compute bad debt amounts.

Moderate

20–25

Journalize transactions related to bad debts.

5A

Journalize entries to record transactions related to bad debts.

Moderate

20–30

6A

Moderate

40–50

Prepare entries for various receivable transactions.

WEYGANDT FINANCIAL AND MANAGERIAL ACCOUNTING 2E

CHAPTER 8

ACCOUNTING FOR RECEIVABLES

Number

LO

BT

Difficulty

Time (min.)

BE1

1

C

Simple

1–2

BE2

1

AP

Simple

5–7

BE3

AN

Simple

4–6

BE4

2

AP

Simple

4–6

BE5

2

AP

Simple

4–6

BE6

2

AP

Simple

2–4

BE7

2

AN

Simple

4–6

BE8

2

AP

Simple

6–8

BE9

3

AP

Simple

8–10

BE10

3

AP

8–10

BE11

3

AP

Simple

2–4

BE12

4

AP

Simple

4–6

DI1

1

AP

Simple

2–4

DI2

2

AP

Simple

4–6

DI3

3

AP

Simple

6–8

DI4

4

AN

Simple

4–6

EX1

1

AP

Simple

8–10

EX2

1

AP

Simple

8–10

EX3

2

AN

Simple

8–10

EX4

2

AN

Simple

6–8

EX5

2

AP

Simple

6–8

EX6

2

AP

Simple

6–8

EX7

2

AP

Simple

4–6

EX8

2

AP

Simple

6–8

EX9

2

AP

Simple

6–8

EX10

3

AN

Simple

8–10

EX11

AN

Simple

6–8

EX12

AP

EX13

AP

Simple

8–10

EX14

4

AP

Simple

8–10

ACCOUNTING FOR RECEIVABLES (Continued)

Number

LO

BT

Difficulty

Time (min.)

P1A

1, 2, 4

AN

Simple

15–20

P2A

2

AN

Moderate

20–25

2

AP

10–15

P3A

2

AN

Moderate

20–30

P4A

AN

20–30

P5A

2

AN

Moderate

20–30

P6A

AN

Moderate

40–50

P7A

AP

50–60

2

Moderate

20–25

4

10–15

Simple

10–15

2

AN

Moderate

20–30

2

10–15

Simple

10–15

2

15–20

AP

Moderate

10–15

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

1. Explain how companies recognize

accounts receivable.

Q9-2

Q9-1 BE9-1

Q9-3

BE9-2

DI9-1

E9-1

E9-2

P9–7A

P9–7B

P9–1A

P9–3A

P9–4A

P9–6A

ANSWERS TO QUESTIONS

1. Accounts receivable are amounts owed by customers on account. They result from the sale of goods

and services. Notes receivable represent claims that are evidenced by formal instruments of credit.

4. The essential features of the allowance method of accounting for bad debts are:

(1) Uncollectible accounts receivable are estimated and matched against revenue in the same

accounting period in which the revenue occurred.

(2) Estimated uncollectibles are debited to Bad Debts Expense and credited to Allowance for Doubtful

Accounts through an adjusting entry at the end of each period.

(3) Actual uncollectibles are debited to Allowance for Doubtful Accounts and credited to Accounts

Receivable at the time the specific account is written off.

7. The adjusting entry under the percentage-of-sales basis is:

Bad Debt Expense ……………………………………………………………………. 4,100

Allowance for Doubtful Accounts ………………………………………….. 4,100

The adjusting entry under the percentage-of-receivables basis is:

Bad Debt Expense ……………………………………………………………………. 2,800

Allowance for Doubtful Accounts ($5,800 – $3,000) ………………… 2,800

Questions Chapter 8 (Continued)

(3) The issuer undertakes the collection process and absorbs any losses from uncollectible accounts.

(4) The retailer receives cash more quickly from the credit card issuer than it would from individual

12. A promissory note gives the holder a stronger legal claim than one on an accounts receivable. As a

result, it is easier to sell to another party. Promissory notes are negotiable instruments, which

means they can be transferred to another party by endorsement. The holder of a promissory note also

can earn interest.

13. The maturity date of a promissory note may be stated in one of three ways: (1) on demand, (2) on

a stated date, and (3) at the end of a stated period of time.

17. When Jana Company has dishonored a note, the ledger can set up a receivable equal to the

face amount of the note plus the interest due. It will then try to collect the balance due, or as

much as possible. If there is no hope of collection it will write-off the receivable.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 8-1

BRIEF EXERCISE 8-2

BRIEF EXERCISE 8-3

(a) Bad Debt Expense ……………………………………….. 31,000

BRIEF EXERCISE 8-4

BRIEF EXERCISE 8-5

BRIEF EXERCISE 8-6

BRIEF EXERCISE 8-7

BRIEF EXERCISE 8-8

BRIEF EXERCISE 8-9

Interest

Maturity Date

BRIEF EXERCISE 8-10

Maturity Date

Annual Interest Rate

Total Interest

(c)

September 7

BRIEF EXERCISE 8-11

BRIEF EXERCISE 8-12

Accounts Receivable Turnover:

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 8-1

DO IT! 8-2

DO IT! 8-3

DO IT! 8-4

SOLUTIONS TO EXERCISES

EXERCISE 8-1

EXERCISE 8-2

EXERCISE 8-3

EXERCISE 8-4

(a)

Accounts Receivable

Amount

%

Estimated Uncollectible

EXERCISE 8-5

EXERCISE 8-6

EXERCISE 8-7

EXERCISE 8-8

EXERCISE 8-9

EXERCISE 8-10

(a) 2017

EXERCISE 8-11

EXERCISE 8-11 (Continued)

EXERCISE 8-12

4/1/17 Notes Receivable …………………………………….. 30,000

Accounts Receivable—Goodwin ………… 30,000

EXERCISE 8-13

(a) May 2 Notes Receivable ………………………………… 9,000

EXERCISE 8-14

(a) Beginning accounts receivable …………………………..……. $ 100,000

SOLUTIONS TO PROBLEMS

PROBLEM 8-1A

(a) 1. Accounts Receivable ………………………….. 3,700,000

(b)

Accounts Receivable

Allowance for Doubtful Accounts

(5) 29,000

PROBLEM 8-1A (Continued)

PROBLEM 8-2A

PROBLEM 8-3A

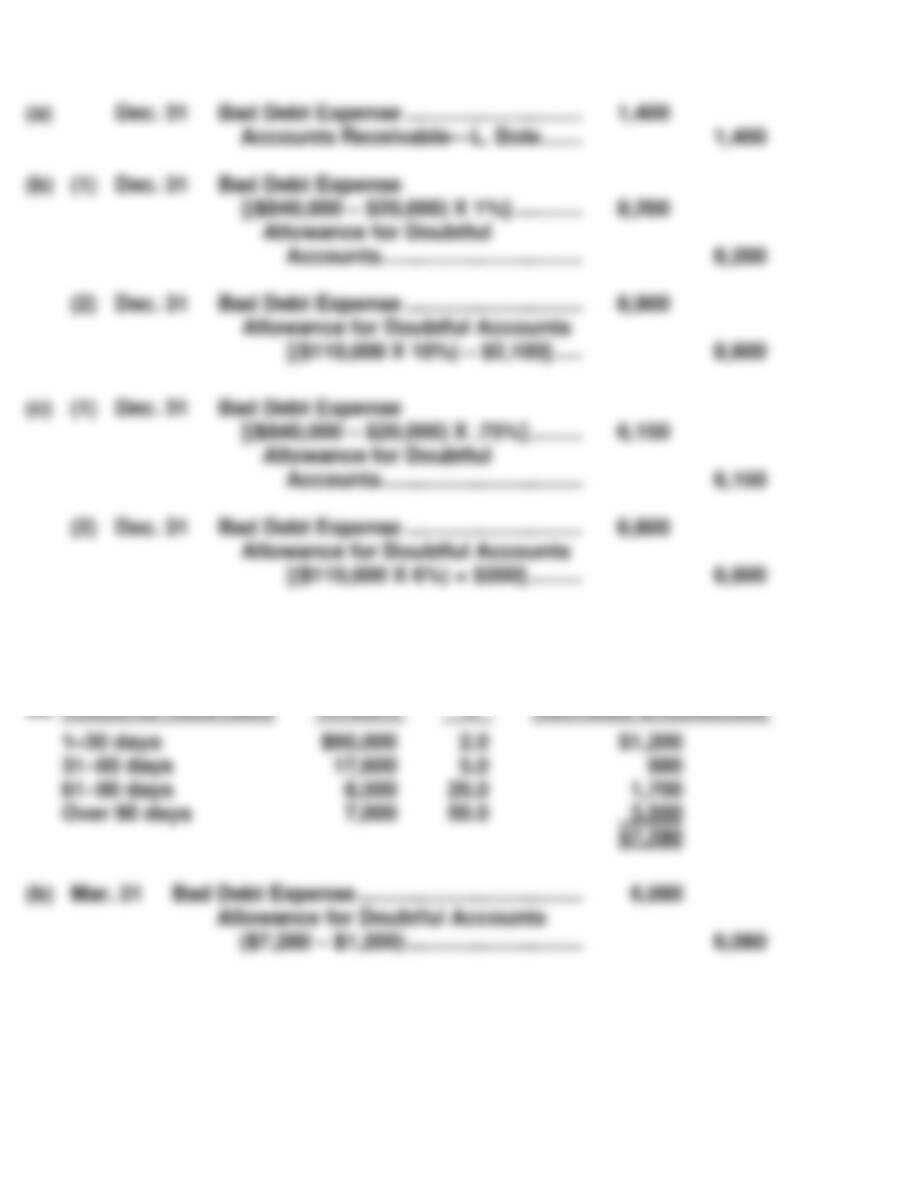

(a) Dec. 31 Bad Debt Expense ……………………………… 26,610

Allowance for Doubtful Accounts

Date

Explanation

Ref.

Debit

Credit

Balance

(b) 2018

(1)

PROBLEM 8-4A

(a) Total estimated bad debts

Number of Days Outstanding

Total

0–30

31–60

61–90

91–120

Over 120

(b) Bad Debt Expense …………………………..……………….. 17,400

Allowance for Doubtful Accounts

[$9,400 + $8,000] ……………………………………….. 17,400

(e) If Rigney Inc. used 4% of total accounts receivable rather than aging the

% uncollectible

PROBLEM 8-5A

(d) Allowance for Doubtful Accounts ………………………. 3,000

Accounts Receivable ………………………………….. 3,000

PROBLEM 8-6A

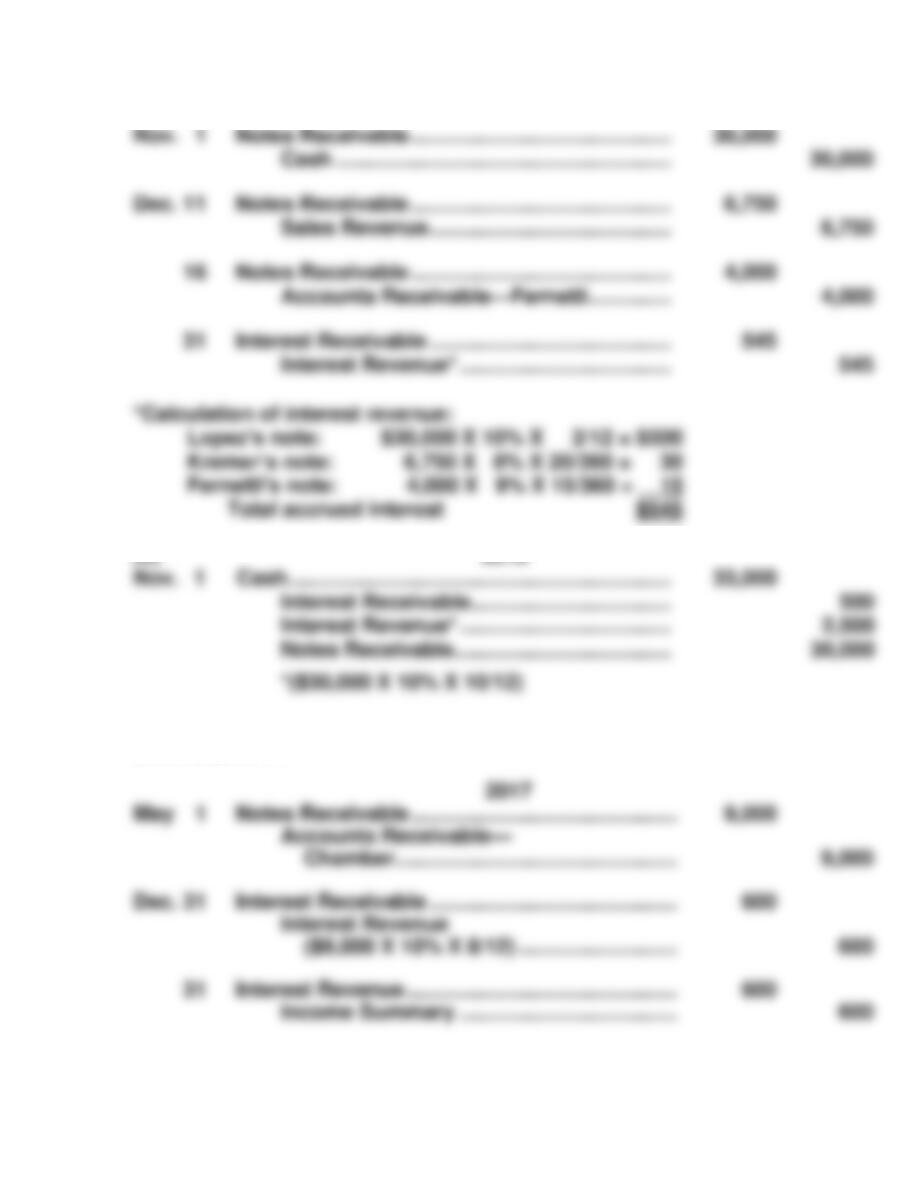

(a) Oct. 7 Accounts Receivable …………………………….. 6,900

Sales Revenue ……………………………….. 6,900

15 Cash …………………………………………………….. 12,160

Notes Receivable …………………………... 12,000

(b)

Notes Receivable

Date

Explanation

Ref.

Debit

Credit

Balance

PROBLEM 8-6A (Continued)

Accounts Receivable

Date

Explanation

Ref.

Debit

Credit

Balance

(c) Current assets

Date

Explanation

Ref.

Debit

Credit

Balance

PROBLEM 8-7A

Jan. 5 Accounts Receivable—Sheldon Company ……… 20,000

Sales Revenue …………………………………….. 20,000

May 25 Notes Receivable ……………………………………….. 6,000

Accounts Receivable—Potter Inc. ………… 6,000

COMPREHENSIVE PROBLEM SOLUTION

(a)

Jan. 1

Notes Receivable …………………………………….

Accounts Receivable—

Merando Company …………………………

1,200

1,200

Allowance for Doubtful Accounts …………….

Accounts Receivable ………………………..

Inventory ………………………………………………..

Accounts Payable …………………………….

Cost of Goods Sold …………………………..…….

Inventory …………………………………………

Cash ………………………………………………………

Accounts Payable …………………………………..

Cash ………………………………………………………

Supplies …………………………………………………

COMPREHENSIVE PROBLEM SOLUTION (Continued)

Adjusting Entries

Cash ……………………………………………………

Notes Receivable …………………………………

Accounts Receivable …………………………...

Allowance for Doubtful Accounts ………….

Interest Receivable ………………………………

Inventory ……………………………………………..

Supplies ………………………………………………

Accounts Payable ………………………………..

Common Stock …………………………………….

20,000

Retained Earnings …………………………..……

Sales Revenue ……………………………………..

Cost of Goods Sold ………………………………

Supplies Expense ………………………………..

Service Charge Expense ………………………

Other Operating Expenses ……………………

Interest Revenue ………………………………….

(b) WINTER COMPANY

Adjusted Trial Balance

January 31, 2017

Interest Revenue ($1,200 X 8% X 1/12) …….

Allowance for Doubtful Accounts……….

Supplies ($1,400 – $560) ……………………

COMPREHENSIVE PROBLEM SOLUTION (Continued)

(b) Optional T accounts for accounts with multiple transactions

Cash

COMPREHENSIVE PROBLEM SOLUTION (Continued)

(c) WINTER COMPANY

Income Statement

For the Month Ending January 31, 2017

COMPREHENSIVE PROBLEM SOLUTION (Continued)

WINTER COMPANY

Retained Earnings Statement

For the Month Ending January 31, 2017

WINTER COMPANY

Balance Sheet

January 31, 2017

BYP 8-1 FINANCIAL REPORTING PROBLEM

(a) RLF COMPANY

Accounts Receivable Aging Schedule

May 31, 2017

(b) RLF COMPANY

Analysis of Allowance for Doubtful Accounts

May 31, 2017

BYP 8-1 (Continued)

(c)

1.

Steps to Improve the

Accounts Receivable Situation

2.

Risks and

Costs Involved

BYP 8-2 COMPARATIVE ANALYSIS PROBLEM

(a)

(1)

Accounts receivable turnover

PepsiCo

Coca-Cola

(2)

Average collection period

BYP 8-3 COMPARATIVE ANALYSIS PROBLEM

(a)

(1)

Accounts receivable turnover ratio

Amazon

Wal-Mart

$473,076

(2)

Average collection period

BYP 8-4 REAL-WORLD FOCUS

(a) Factoring invoices enhances cash flow and allows a company to meet

business expenses and take on new opportunities. The benefits of

factoring include:

BYP 8-5 DECISION MAKING ACROSS THE ORGANIZATION

(a)

2018

2017

2016

Net credit sales ……………………………….

$500,000

$550,000

$400,000

(c) The analysis shows that the credit card fee of 4% of net credit sales will

BYP 8-5 (Continued)

Finally, the decision hinges on: (1) the accuracy of the estimate of

BYP 8-6 COMMUNICATION ACTIVITY

Of course, this solution will differ from student to student. Important factors

to look for would be definitions of the methods, how they are similar and how

they differ. Also, look for use of good sentence structure, correct spelling, etc.

Example:

Dear Jill,

The three methods you asked about are methods of dealing with uncollectible

accounts receivable. Two of them, percentage-of-sales and percentage-of–

BYP 8-7 ETHICS CASE

(a) The stakeholders in this situation are:

BYP 8-8 ALL ABOUT YOU

BYP 8-9 FASB CODIFICATION ACTIVITY

(a) Receivables represent contractual rights to receive money on fixed or

IFRS8-1 INTERNATIONAL FINANCIAL REPORTING PROBLEM

(a) Note 1.16 states: Trade accounts receivable are recorded at their face