CHAPTER 8 • OPERATING ASSETS: PROPERTY, PLANT, AND EQUIPMENT, AND INTANGIBLES 8-21

PROBLEM 8-8 (Concluded)

3. Original cost of building ………………………………………………………. $364,000

Pollution device capitalized …………………………………………………. 42,000

2015 depreciation …………………………………………………………. (14,000)

2016 depreciation …………………………………………………………. (12,600)

LO 6,10 PROBLEM 8-9 AMORTIZATION OF INTANGIBLE, REVISION OF RATE

1. The $85,000 of research and development costs should be recorded as an expense.

2. *Reynosa should record $595 of amortization expense each fiscal year, for a total of

3. Reynosa should record a loss of $8,925.

8-22 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 8,11 PROBLEM 8-10 PURCHASE AND DISPOSAL OF OPERATING ASSET AND

EFFECTS ON STATEMENT OF CASH FLOWS

1. Partial statement of cash flows for 2016:

Cash flows from operating activities:

Net income ……………………………………………………………… $ XX,XXX

Depreciation expense ………………………………………………. 12,000

2. Castlewood would replace machinery if the replacement would result in additional

net income in the future. Any additional revenues generated as a result of a possible

increase in production capacity (that is, the ability to make and thus sell more prod-

CHAPTER 8 • OPERATING ASSETS: PROPERTY, PLANT, AND EQUIPMENT, AND INTANGIBLES 8-23

LO 9,10,11 PROBLEM 8-11 AMORTIZATION OF INTANGIBLES AND EFFECTS ON

STATEMENT OF CASH FLOWS

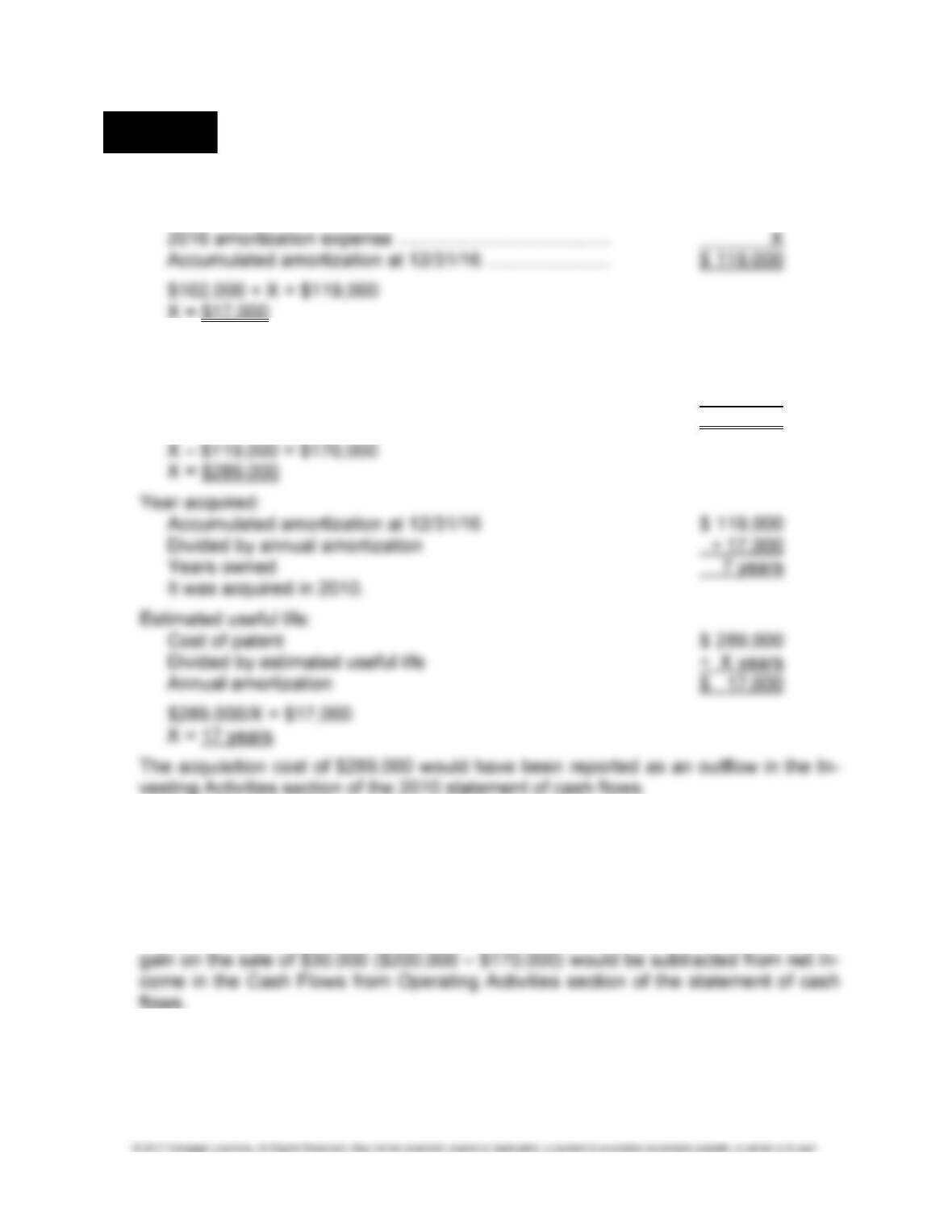

1. 2016 amortization expense:

Accumulated amortization at 12/31/15 …………………… $ 102,000

2. Acquisition cost:

Cost of patent …………………………………………………………. $ X

Accumulated amortization at 12/31/16 …………………… 119,000

Carrying value at 12/31/16 …………………………………… $ 170,000

3. Assuming the indirect method is used, the amortization expense relating to the pa-

tent would be added back to net income in the Cash Flows from Operating Activities

section of the statement of cash flows.

4. The proceeds from the sale of $200,000 would be reported as an inflow in the Cash

Flows from Investing Activities section of the statement of cash flows. In addition, the

8-24 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

ALTERNATE PROBLEMS

LO 3 PROBLEM 8-1A LUMP-SUM PURCHASE OF ASSETS AND SUBSEQUENT EVENTS

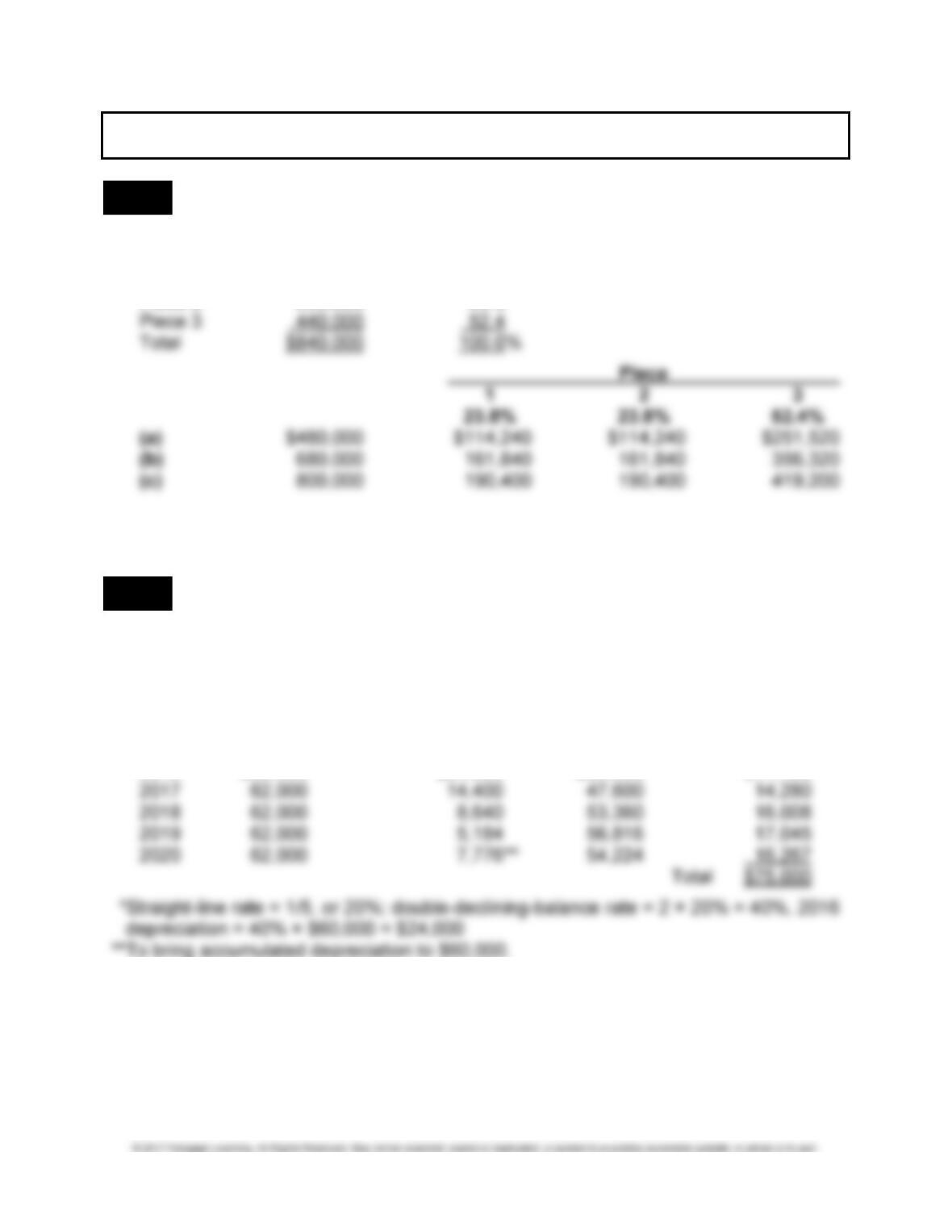

1. Relative fair values:

Piece 1 $200,000 23.8%

Piece 2 200,000 23.8

2. The purchase does not affect total assets; it affects only the composition of the as-

sets. Cash is a current asset; equipment is a long-term asset.

LO 5 PROBLEM 8-2A DEPRECIATION AS A TAX SHIELD

If asset is not purchased:

Annual income tax is $62,000 × 30% = $18,600

If asset is purchased:

Income Before Tax Depreciation Income Tax

and Depreciation Expense Before Tax 30%

2016 $62,000 $24,000* $38,000 $11,400

CHAPTER 8 • OPERATING ASSETS: PROPERTY, PLANT, AND EQUIPMENT, AND INTANGIBLES 8-25

PROBLEM 8-2A (Concluded)

Total tax if not purchased:

$18,600 × 5 years ……………………………………………………………… $93,000

Total tax if purchased …………………………………………………………. 75,000

Depreciation tax shield ……………………………………………………….. $18,000

LO 5 PROBLEM 8-3A BOOK VERSUS TAX DEPRECIATION

1. Year Straight-Line – MACRS = Difference

1 $ 4,700* $ 5,650 $ (950)

2 4,700 9,025 (4,325)

2. The president is correct that a total of $28,200 will be deducted as depreciation

under either method over the six-year life. However, the memo should note that all

other things being equal, Payton should prefer MACRS for taxes, since it results in

lower taxes during the early years in the life of the truck. Money received earlier is

8-26 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 11 PROBLEM 8-4A AMORTIZATION AND CASH FLOW

1. 2016 income = $500,000 – $62,500 – $50,000 = $387,500

LO 11 PROBLEM 8-5A RECONSTRUCT NET BOOK VALUES USING STATEMENT OF

CASH FLOWS

1. Book value of land at time of sale:

Book value …………………………………………………………. $ X

Sales proceeds …………………………………………………… 187,000

2. Net book value of property, plant, and equipment at December 31, 2015:

Net book value at 12/31/15 …………………………………… $ X

3. Net book value of intangibles at December 31, 2015:

Net book value at 12/31/15 …………………………………… $ X

Payment of legal fees during 2016 ………………………… 6,000

Book value of trademark sold during 2016 ……………… (114,000)**

2016 Amortization ……………………………………………….. (3,000)

CHAPTER 8 • OPERATING ASSETS: PROPERTY, PLANT, AND EQUIPMENT, AND INTANGIBLES 8-27

ALTERNATE MULTI-CONCEPT PROBLEMS

LO 1,5,8,9,10 PROBLEM 8-6A COST OF ASSETS, SUBSEQUENT BOOK VALUES, AND

BALANCE SHEET PRESENTATION

Depreciation or amortization and book values:

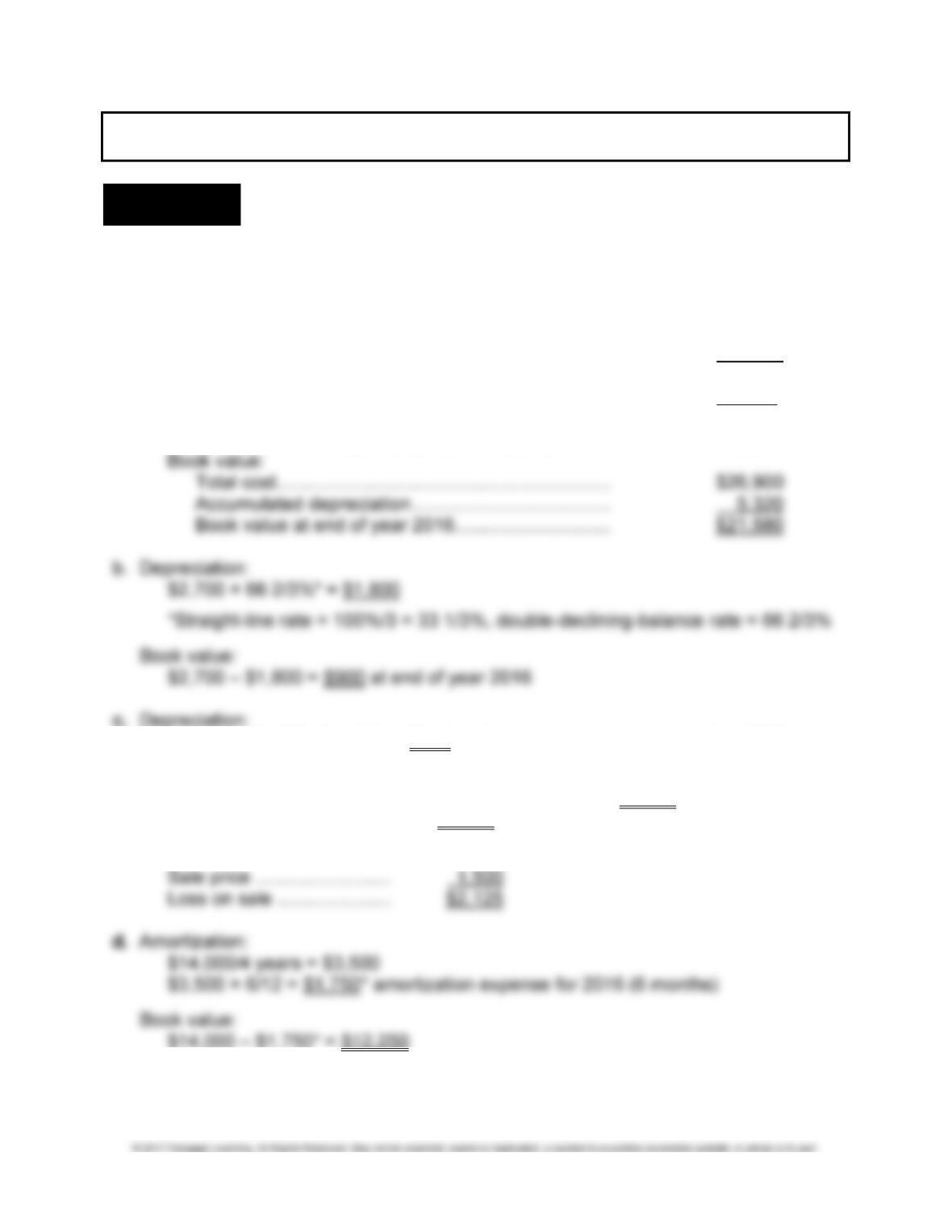

a. Depreciation should be calculated as follows:

Original cost……………………………………………………….. $16,000

Cab/oven …………………………………………………………… 10,900

Total cost …………………………………………………………… $26,900

Residual value ……………………………………………………. (300)

Depreciable amount …………………………………… $26,600

Depreciation expense ($26,600/5 years) ………. $ 5,320

($8,000 – $1,000)/8 × 3/12 = $219 for 3 months (January 1 to April 1, 2016)

Book value at time of sale:

Accumulated depreciation = ($8,000 – $1,000) × 5/8 = $4,375

Book value = $8,000 – $4,375 = $3,625

Book value ……………………. $3,625

8-28 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 2,5 PROBLEM 8-7A COST OF ASSETS AND THE EFFECT ON DEPRECIATION

1. The proper cost to record for the acquisition is $190,000 ($168,000 + $16,500 +

$4,400 + $1,100). All costs, except the operating costs for the first year, should be

capitalized as part of the cost of the equipment. The operating costs of $26,400

should be expensed.

2. Depreciation erroneously reported in Year 1 was $21,640* ($216,400/10). Deprecia-

3. Key reported income of $55,000 – $21,640*, or $33,360. The correct amount of in-

come should be as follows:

4. Key should not include operating costs in the value of the asset recorded on the bal-

LO 7,8 PROBLEM 8-8A CAPITAL EXPENDITURES, DEPRECIATION, AND DISPOSAL

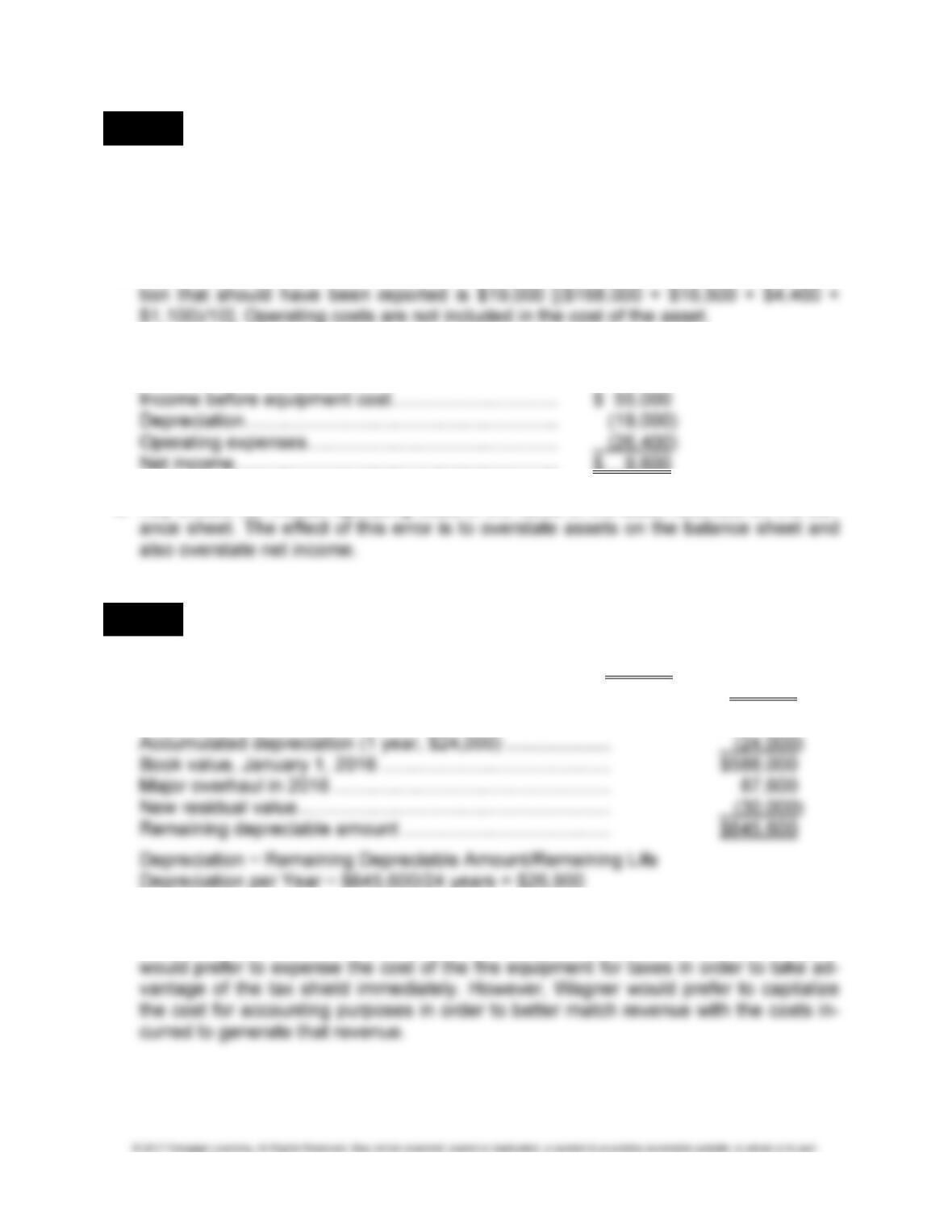

1. 2015 Depreciation = [($612,000 – $12,000)/25 years)] = $24,000

2016 Depreciation = [($612,000 + $87,600 – $30,000 – $24,000)/24)] = $26,900

Original cost, January 1, 2015 …………………………………… $612,000

2. The cost of the fire equipment increased the value of an asset that will last for more

than one year. The cost would have been expensed if it was maintenance. Wagner

CHAPTER 8 • OPERATING ASSETS: PROPERTY, PLANT, AND EQUIPMENT, AND INTANGIBLES 8-29

PROBLEM 8-8A (Concluded)

3. Loss at sale = $612,000 + $87,600 – $24,000 – $26,900 – $360,000 = $288,700

Asset cost ………………………………………………………………………… $612,000

Major overhaul in 2016 ………………………………………………………. 87,600

LO 6,10 PROBLEM 8-9A AMORTIZATION OF INTANGIBLE, REVISION OF RATE

1. The $350,000 of costs that represent research and development should be treated

2. Maciel should record amortization expense of $23,800/20 years, or $1,190 per year.

3. The book value of the patent after five years of amortization is:

$23,800 – (5 × $1,190) = $17,850. Since the patent is worthless, the amount of

8-30 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 8,11 PROBLEM 8-10A PURCHASE AND DISPOSAL OF OPERATING ASSET AND

EFFECTS ON STATEMENT OF CASH FLOWS

1. Partial statement of cash flows for 2016:

Cash flows from operating activities:

Net income ……………………………………………………………… $XX,XXX

Depreciation expense ………………………………………………. 8,000

2. Mansfield would replace the medium-sized delivery truck with a larger truck if the

replacement would result in additional net income in the future. Any additional reve-

nues generated as a result of Mansfield’s ability to deliver and sell more product

would increase net income. On the other hand, this increase would be offset by the

costs of acquiring and operating the new delivery truck.

CHAPTER 8 • OPERATING ASSETS: PROPERTY, PLANT, AND EQUIPMENT, AND INTANGIBLES 8-31

LO 9,10,11 PROBLEM 8-11A AMORTIZATION OF INTANGIBLES AND EFFECTS ON

STATEMENT OF CASH FLOWS

1. 2016 amortization expense:

Accumulated amortization at 12/31/15 …………………………….. $ 1,510,000

2. Acquisition cost:

Cost of patent ………………………………………………………………. $ X

Accumulated amortization at 12/31/16 …………………………….. 1,661,000

Carrying value at 12/31/16 …………………………………………….. $ 1,357,000

3. Assuming that the indirect method is used, the amortization expense relating to the

patent would be added back to net income in the Cash Flows from Operating Activi-

ties section of the statement of cash flows.

4. The proceeds from the sale of the patent for $1,700,000 would be reported as an

inflow in the Cash Flows from Investing Activities section of the statement of cash

8-32 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

DECISION CASES

READING AND INTERPRETING FINANCIAL STATEMENTS

LO 1,9 DECISION CASE 8-1 PANERA BREAD

Property, plant, and equipment consisted of the following (in thousands):

Property and Equipment, net

Major classes of property and equipment consisted of the following (in thousands):

December 30 December 31

2014 2013

Leasehold improvements $ 693,503 $ 607,472

Building and improvements 340,854 305,060

1. A note to the statements indicates the company has the following classes of assets

in the category leasehold improvements, machinery and equipment, furniture and

fixtures, computer hardware and software, and construction in progress, smallwares,

and land.

2. The company uses the straight-line method of depreciation.

3.

Leasehold improvements 15 – 20 years

4. The company discloses the total amount of property, plant, and equipment before

5. The statement of cash flows indicates purchases of $224,217,000. It does not indi-

cate sales of property and equipment.

CHAPTER 8 • OPERATING ASSETS: PROPERTY, PLANT, AND EQUIPMENT, AND INTANGIBLES 8-33

LO 1,9 DECISION CASE 8-2 MAKING BUSINESS DECISIONS: COMPARING TWO COM-

PANIES IN THE SAME INDUSTRY: CHIPOTLE AND PANERA BREAD

A. THE RATIO ANALYSIS MODEL

1. Formulate the Question

What is the average life of the assets?

2. Gather the Information from the Financial Statements

To calculate a company’s average life of assets and average age of assets, it is es-

sential to know its total operating assets and accumulated depreciation from the bal-

ance sheet and depreciation expense from the income statement or statement of

3. Calculate the Ratio and 4. Compare the Ratio to Others

Panera _ Chipotle ____

2014 2013 2014 2013_

Average life of assets 11.85 11.77 15.64 15.52

8-34 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

DECISION CASE 8-2 (Concluded)

5. Interpret the Ratios

The average life and age of assets have been consistent from year to year and are

in line with other companies in the industry. The asset turnover ratio is a measure of

B. THE BUSINESS DECISION MODEL

1. Formulate the Question:

If you were a lender, would you be willing to lend money to either company and use

the operating assets as collateral for the loan?

2. Gather Information from the Financial Statements and Other Sources:

This information will come from a variety of sources, not limited to but including:

• The balance sheet provides information about the age and composition of the

3. Analyze the Information Gathered:

4. Make the Decision:

Taking into account all of the various sources of information, decide either to

• Lend money to the company, or

• Find an alternative use for the money

5. Monitor Your Decision:

If you decide to lend the money, you will need to monitor your investment periodically.

CHAPTER 8 • OPERATING ASSETS: PROPERTY, PLANT, AND EQUIPMENT, AND INTANGIBLES 8-35

MAKING FINANCIAL DECISIONS

LO 1,5 DECISION CASE 8-3 COMPARING COMPANIES

ACCELERATED COMPANY

INCOME STATEMENT

FOR THE YEAR ENDED DECEMBER 31, 2016

Sales ………………………………………………………………………….. $720,000

Cost of goods sold ……………………………………………………….. 360,000

Gross profit ………………………………………………………………….. $360,000

Since the balance of the Accumulated Depreciation account for Straight Company is

$240,000 and the depreciation expense is $120,000 per year, the assets must be two

years old. The amount of depreciation expense for Accelerated Company using the

double-declining-balance method is as follows:

2015: $600,000 × 40% = $240,000

*2016: $600,000 – $240,000 = $360,000 × 40% = $144,000

LO 5 DECISION CASE 8-4 DEPRECIATION ALTERNATIVES

For accounting purposes, the company should use straight-line depreciation because it

will better match the cost of using the asset with the equal production levels. For taxes,

8-36 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

ETHICAL DECISION MAKING

LO 3 DECISION CASE 8-5 VALUING ASSETS

1. Recognize an Ethical Dilemma:

Students should be asked to determine the impact of using the first appraisal versus

2. Analyze the Key Elements in the Situation:

Students should be asked about the nature of the appraisal process. Is it possible for

two appraisers to have different estimates of the fair market value? Should the ac-

countant always accept the first appraisal? When is it acceptable to seek another

3. List Alternatives and Evaluate the Impact of Each on Those Affected:

The proper amount to record for operating assets can have a potential effect on

4. Select the Best Alternative:

It appears that the concept of neutrality has been violated in this case. It is not wrong

for Terry and Tammy to seek a second appraisal if their motive was to develop

questioned.

LO 5 DECISION CASE 8-6 DEPRECIATION ESTIMATES

Both methods will result in the total cost of the asset being recorded on the income

statement over the life of the asset. However, depreciating the asset is preferable be-

cause it matches the cost evenly over the asset’s life. You should try to convince the

manager that it is not correct to depreciate the asset over a longer life and then record a

large loss in the third year. If the manager is not convinced, you may have to consider

whether the matter should be discussed with his/her superior and/or the company’s

auditors.

CHAPTER 8 • OPERATING ASSETS: PROPERTY, PLANT, AND EQUIPMENT, AND INTANGIBLES 8-37

SOLUTION TO INTEGRATIVE PROBLEM

1. PEK COMPANY

INCOME STATEMENT

FOR THE YEAR ENDED DECEMBER 31, 2016

Sales revenue ………………………………………………… $1,250,000

Cost of goods sold ………………………………………….. 636,500

Gross profit ……………………………………………….. $ 613,500

PEK COMPANY

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED DECEMBER 31, 2016

Cash flows from operating activities:

Net income ………………………………………………………………………. $263,830

Adjustments to reconcile net income to net cash provided by

operating activities (includes depreciation expense) ………….. 110,200*

8-38 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

2. PEK COMPANY

INCOME STATEMENT

FOR THE YEAR ENDED DECEMBER 31, 2016

Sales …………………………………………………………….. $1,250,000

Cost of goods sold ………………………………………….. 636,500

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED DECEMBER 31, 2016

Cash flows from operating activities:

Net income ………………………………………………………………………. $248,366

Adjustments to reconcile net income to net

CHAPTER 8 • OPERATING ASSETS: PROPERTY, PLANT, AND EQUIPMENT, AND INTANGIBLES 8-39

3. a. LIFO cost of goods sold:

40,000($3.25) = $130,000

60,000($3.10) = 186,000

75,000($3.00) = 225,000

4. a. Sales on account ………………………………………………………….. $800,000

Times estimated uncollectibles ……………………………………….. 3%

Increase in other expenses ……………………………………….. $ 24,000

b. Increase in other expenses ……………………………………………. $ 24,000