144

Chapter 8

of Taxation

WHAT’S NEW IN THE SIXTH EDITION:

A new

In the News

box on “New Research on Taxation” has been added.

LEARNING OBJECTIVES:

By the end of this chapter, students should understand:

➢ how taxes reduce consumer and producer surplus.

CONTEXT AND PURPOSE:

Chapter 8 is the second chapter in a three-chapter sequence dealing with welfare economics. In the

previous section on supply and demand, Chapter 6 introduced taxes and demonstrated how a tax affects

the price and quantity sold in a market. Chapter 6 also described the factors that determine how the

burden of the tax is divided between the buyers and sellers in a market. Chapter 7 developed welfare

economics—the study of how the allocation of resources affects economic well-being. Chapter 8

8

APPLICATION: THE COSTS OF

TAXATION

Chapter 8 /Application: The Costs of Taxation ❖ 145

KEY POINTS:

• A tax on a good reduces the welfare of buyers and sellers of the good, and the reduction in

consumer and producer surplus usually exceeds the revenue raised by the government. The fall in

total surplus—the sum of consumer surplus, producer surplus, and tax revenue—is called the

deadweight loss of the tax.

CHAPTER OUTLINE:

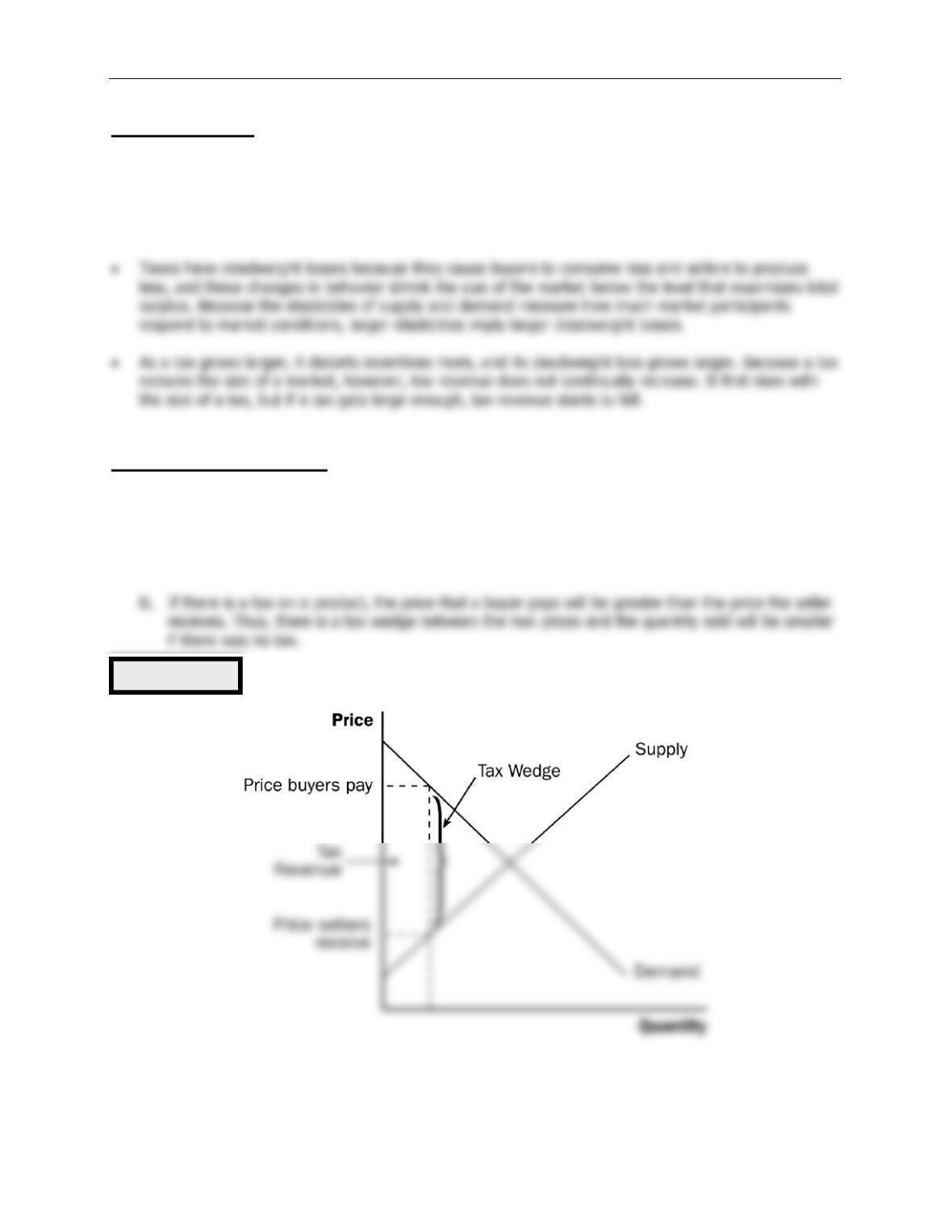

I. The Deadweight Loss of Taxation

A. Remember that it does not matter who a tax is levied on; buyers and sellers will likely share in

the burden of the tax.

Figure 1

146 ❖ Chapter 8 /Application: The Costs of Taxation

C. How a Tax Affects Market Participants

1. We can measure the effects of a tax on consumers by examining the change in consumer

surplus. Similarly, we can measure the effects of the tax on producers by looking at the

change in producer surplus.

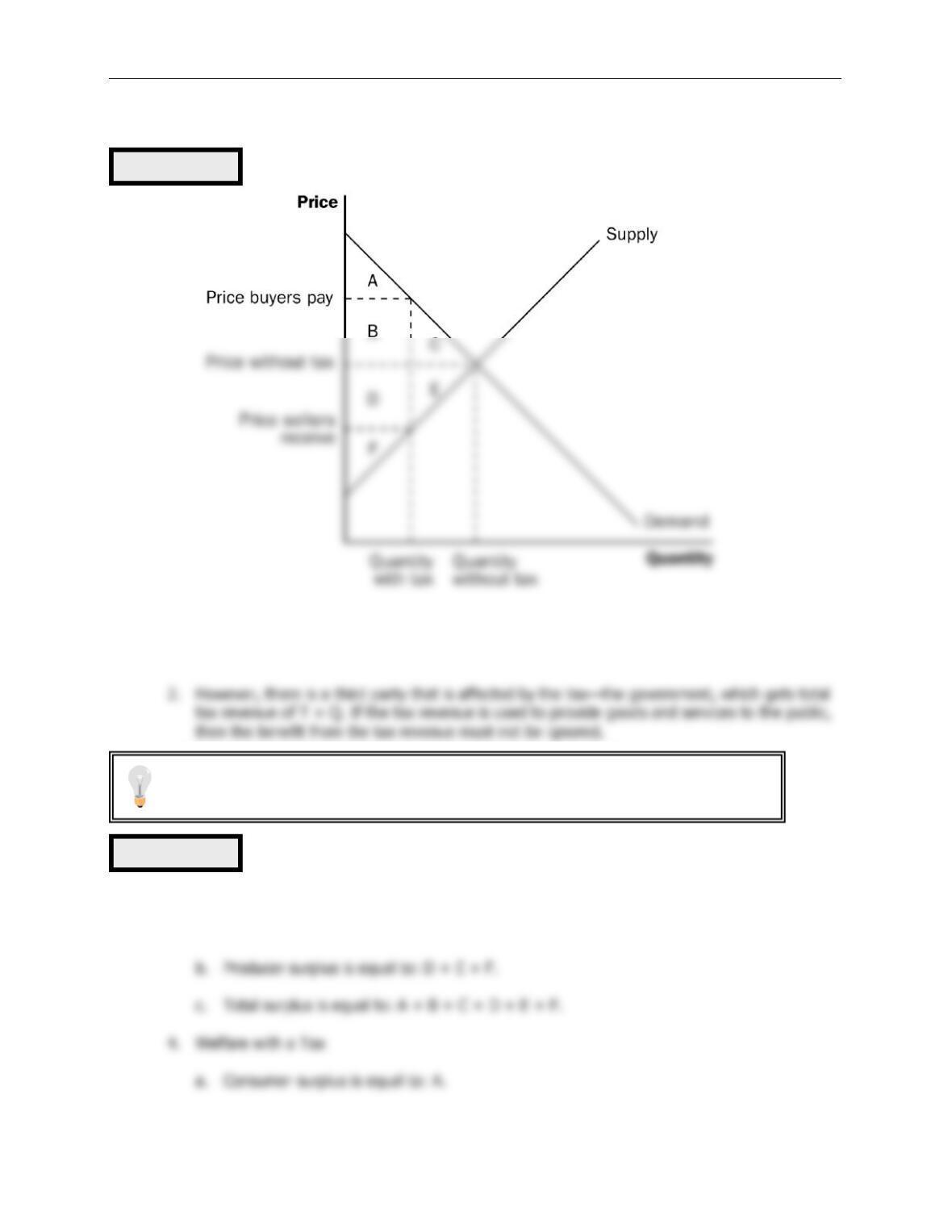

3. Welfare without a Tax

a. Consumer surplus is equal to: A + B + C.

Figure 2

Figure 3

If you spent enough time covering consumer and producer surplus in Chapter 7,

students should have an easy time with this concept.

Chapter 8 /Application: The Costs of Taxation ❖ 147

5. Changes in Welfare

a. Consumer surplus changes by: –(B + C).

6. Definition of deadweight loss: the fall in total surplus that results from a market

distortion, such as a tax.

D. Deadweight Losses and the Gains from Trade

1. Taxes cause deadweight losses because they prevent buyers and sellers from benefiting from

trade.

3. The deadweight loss is equal to areas C and E (the drop in total surplus).

Figure 4

148 ❖ Chapter 8 /Application: The Costs of Taxation

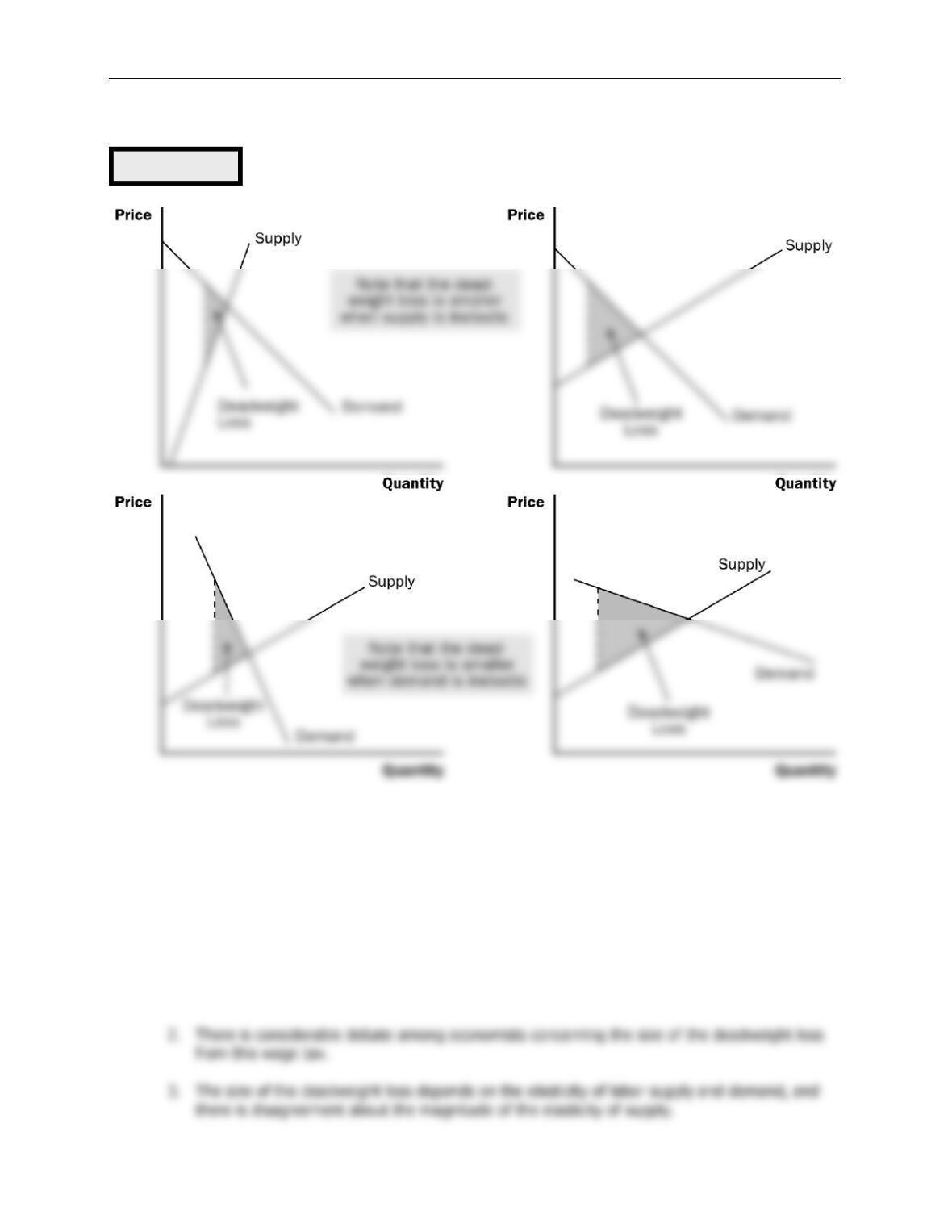

II. The Determinants of the Deadweight Loss

A. The price elasticities of supply and demand will determine the size of the deadweight loss that

occurs from a tax.

1. Given a stable demand curve, the deadweight loss is larger when supply is relatively elastic.

2. Given a stable supply curve, the deadweight loss is larger when demand is relatively elastic.

B.

Case Study: The Deadweight Loss Debate

1. Social Security tax and federal income tax are taxes on labor earnings. A labor tax places a

tax wedge between the wage the firm pays and the wage that workers receive.

Figure 5

Chapter 8 /Application: The Costs of Taxation ❖ 149

a. Economists who argue that labor taxes do not greatly distort market outcomes believe

that labor supply is fairly inelastic.

b. Economists who argue that labor taxes lead to large deadweight losses believe that labor

supply is more elastic.

III. Deadweight Loss and Tax Revenue as Taxes Vary

A. As taxes increase, the deadweight loss from the tax increases.

B. In fact, as taxes increase, the deadweight loss rises more quickly than the size of the tax.

Activity 1—Labor Taxes

Type: In-class discussion

Topics: Deadweight loss, taxation

Materials needed: None

Time: 10 minutes

Class limitations: Works in any size class

Purpose

Most students have not spent a great deal of time considering the effects of taxation on labor

supply. This in-class exercise gives them the opportunity to consider the effects of proposed

tax rates on their own willingness to supply labor.

Instructions

Ask students to assume that they are full-time workers earning $10 per hour, $80 per day,

$400 per week, $20,000 per year.

Points for Discussion

Many students have no idea that current marginal tax rates are greater than 30% for many

taxpayers.

Figure 6

150 ❖ Chapter 8 /Application: The Costs of Taxation

2. If we double the size of a tax, the base and height of the triangle both double so the area of

the triangle (the deadweight loss) rises by a factor of four.

D.

Case Study: The Laffer Curve and Supply-Side Economics

1. The relationship between the size of a tax and the level of tax revenues is called a Laffer

curve.

2. Supply-side economists in the 1980s used the Laffer curve to support their belief that a drop

in tax rates could lead to an increase in tax revenue for the government.

E.

In the News:

New Research on Taxation

1. The latest economic research indicates that some European countries may be on the

declining side of the Laffer curve.

ALTERNATIVE CLASSROOM EXAMPLE:

Draw a graph showing the demand and supply of paper clips. (Draw each curve as a 45–

degree line so that buyers and sellers will share any tax equally.) Mark the equilibrium price

as $0.50 (per box) and the equilibrium quantity as 1,000 boxes. Show students the areas of

producer and consumer surplus.

Impose a $0.20 tax on each box. Assume that sellers are required to “pay” the tax to the

government. Show students that:

Chapter 8 /Application: The Costs of Taxation ❖ 151

Activity 2—Tax Alternatives

Type: In-class assignment

Topics: Taxes and deadweight loss

Materials needed: None

Time: 20 minutes

Class limitations: Works in any size class

Purpose

The market impact of taxes can be a new concept to many students. This exercise helps them

think about the effects of taxes on different goods. Taxes that may be appealing for equity

reasons can be distortionary from a market perspective.

Instructions

Tell the class, “The state has decided to increase funding for public education. They are

considering four alternative taxes to finance these expenditures. All four taxes would raise the

same amount of revenue.” List these options on the board:

1. A sales tax on food.

2. A tax on families with school-age children.

Common Answers and Points for Discussion

A. Taxes change incentives. How might individuals change their behavior because of

each of these taxes?

1. A sales tax on food: At the margin, some consumers will purchase less food.

Overall food purchases will not decrease substantially because the tax will be

spread over a large number of consumers and demand is relatively inelastic.

2. A tax on families with school-age children: No families would put their children up

152 ❖ Chapter 8 /Application: The Costs of Taxation

SOLUTIONS TO TEXT PROBLEMS:

Quick Quizzes

1. Figure 1 shows the supply and demand curves for cookies, with equilibrium quantity

Q

1 and

equilibrium price

P

1. When the government imposes a tax on cookies, the price to buyers

rises to

P

B, the price received by sellers declines to

P

S, and the equilibrium quantity falls to

2. The deadweight loss of a tax is greater the greater is the elasticity of demand. Therefore, a

tax on beer would have a larger deadweight loss than a tax on milk because the demand for

beer is more elastic than the demand for milk.

B. Rank these taxes from smallest deadweight loss to largest deadweight loss.

Lowest deadweight loss—tax on children, very inelastic.

Then—tax on food. Demand is inelastic; supply is elastic.

Third—tax on vacation homes. Demand is elastic; short-run supply is inelastic.

Most deadweight loss—tax on jewelry. Demand is elastic; supply is elastic.

Chapter 8 /Application: The Costs of Taxation ❖ 153

3. If the government doubles the tax on gasoline, the revenue from the gasoline tax could rise

or fall depending on whether the size of the tax is on the upward or downward sloping

Questions for Review

1. When the sale of a good is taxed, both consumer surplus and producer surplus decline. The

2. Figure 2 illustrates the deadweight loss and tax revenue from a tax on the sale of a good.

Without a tax, the equilibrium quantity would be

Q

1, the equilibrium price would be

P

1,

3. The greater the elasticities of demand and supply, the greater the deadweight loss of a tax.

4. Experts disagree about whether labor taxes have small or large deadweight losses because

they have different views about the elasticity of labor supply. Some believe that labor supply

154 ❖ Chapter 8 /Application: The Costs of Taxation

5. The deadweight loss of a tax rises more than proportionally as the tax rises. Tax revenue,

however, may increase initially as a tax rises, but as the tax rises further, revenue eventually

declines.

Problems and Applications

1. a. Figure 3 illustrates the market for pizza. The equilibrium price is

P

1, the equilibrium

quantity is

Q

1, consumer surplus is area A + B + C, and producer surplus is area D + E +

F. There is no deadweight loss, as all the potential gains from trade are realized; total

Figure 3

b. With a $1 tax on each pizza sold, the price paid by buyers,

P

B, is now higher than the

price received by sellers,

P

S, where

P

B =

P

S + $1. The quantity declines to

Q

2, consumer

surplus is area A, producer surplus is area F, government revenue is area B + D, and

deadweight loss is area C + E. Consumer surplus declines by B + C, producer surplus

declines by D + E, government revenue increases by B + D, and deadweight loss

increases by C + E.

Chapter 8 /Application: The Costs of Taxation ❖ 155

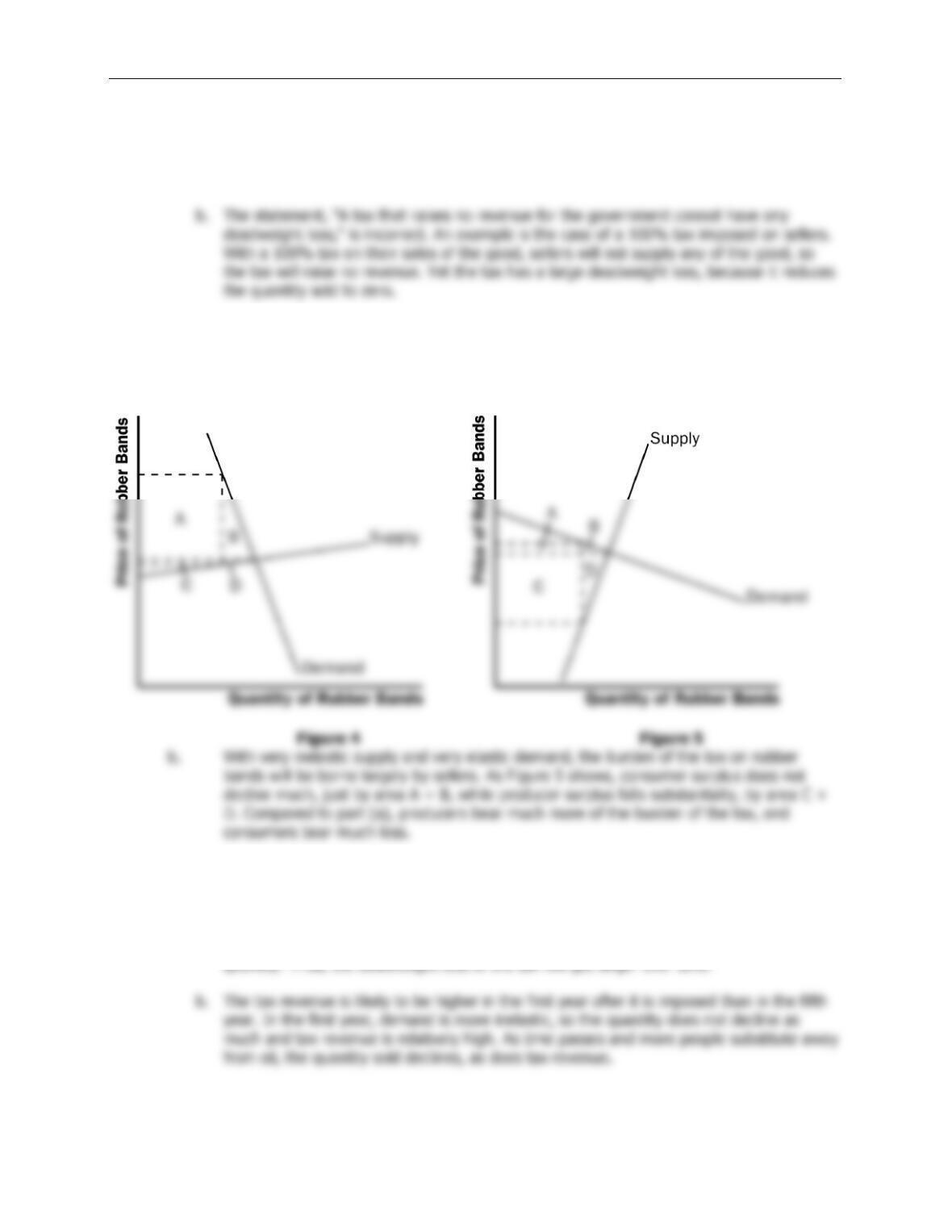

2. a. The statement, “A tax that has no deadweight loss cannot raise any revenue for the

government,” is incorrect. An example is the case of a tax when either supply or demand

is perfectly inelastic. The tax has neither an effect on quantity nor any deadweight loss,

but it does raise revenue.

3. a. With very elastic supply and very inelastic demand, the burden of the tax on rubber

bands will be borne largely by buyers. As Figure 4 shows, consumer surplus declines

considerably, by area A + B, but producer surplus does not fall much at all, just by area

C + D.

4. a. The deadweight loss from a tax on heating oil is likely to be greater in the fifth year after

it is imposed rather than the first year. In the first year, the elasticity of demand is fairly

low, as people who own oil heaters are not likely to get rid of them right away. But over

time they may switch to other energy sources and people buying new heaters for their

homes will more likely choose gas or electric, so the tax will have a greater impact on

156 ❖ Chapter 8 /Application: The Costs of Taxation

5. Because the demand for food is inelastic, a tax on food is a good way to raise revenue

because it does not lead to much of a deadweight loss; thus taxing food is less inefficient

6. a. This tax has such a high rate that it is not likely to raise much revenue. Because of the

7. a. Figure 6 illustrates the market for socks and the effects of the tax. Without a tax, the

equilibrium quantity would be

Q

1, the equilibrium price would be

P

1, total spending by

consumers equals total revenue for producers, which is

P

1 x

Q

1, which equals area B + C

+ D + E + F, and government revenue is zero. The imposition of a tax places a wedge

between the price buyers pay,

P

B, and the price sellers receive,

P

S, where

P

B =

P

S + tax.

The quantity sold declines to

Q

2. Now total spending by consumers is

P

B x

Q

2, which

equals area A + B + C + D, total revenue for producers is

P

S x

Q

2, which is area C + D,

and government tax revenue is

Q

2 x tax, which is area A + B.

c. The price paid by consumers rises, unless demand is perfectly elastic or supply is

perfectly inelastic. Whether total spending by consumers rises or falls depends on the

price elasticity of demand. If demand is elastic, the percentage decline in quantity

Chapter 8 /Application: The Costs of Taxation ❖ 157

8. Because the tax on gadgets was eliminated, all tax revenue must come from the tax on

widgets. The tax revenue from the tax on widgets equals the tax per unit times the quantity

9. Figure 7 illustrates the effects of the $2 subsidy on a good. Without the subsidy, the

equilibrium price is

P

1 and the equilibrium quantity is

Q

1. With the subsidy, buyers pay price

P

B, producers receive price

P

S (where

P

S =

P

B + $2), and the quantity sold is

Q

2. The

following table illustrates the effect of the subsidy on consumer surplus, producer surplus,

158 ❖ Chapter 8 /Application: The Costs of Taxation

10. a. Figure 8 shows the effect of a $10 tax on hotel rooms. The tax revenue is represented by

areas A + B, which are equal to ($10)(900) = $9,000. The deadweight loss from the tax

is represented by areas C + D, which are equal to (0.5)($10)(100) = $500.

b. Figure 9 shows the effect of a $20 tax on hotel rooms. The tax revenue is represented by

areas A + B, which are equal to ($20)(800) = $16,000. The deadweight loss from the tax

is represented by areas C + D, which are equal to (0.5)($20)(200) = $2,000.

When the tax is doubled, the tax revenue rises by less than double, while the deadweight

loss rises by more than double.

11. a. Setting quantity supplied equal to quantity demanded gives 2

P

= 300 –

P

. Adding

P

to

200.

b. Now P is the price received by sellers and

P

+

T

is the price paid by buyers. Equating

quantity demanded to quantity supplied gives

2P

= 300 − (

P

+

T

). Adding

P

to both sides

Chapter 8 /Application: The Costs of Taxation ❖ 159

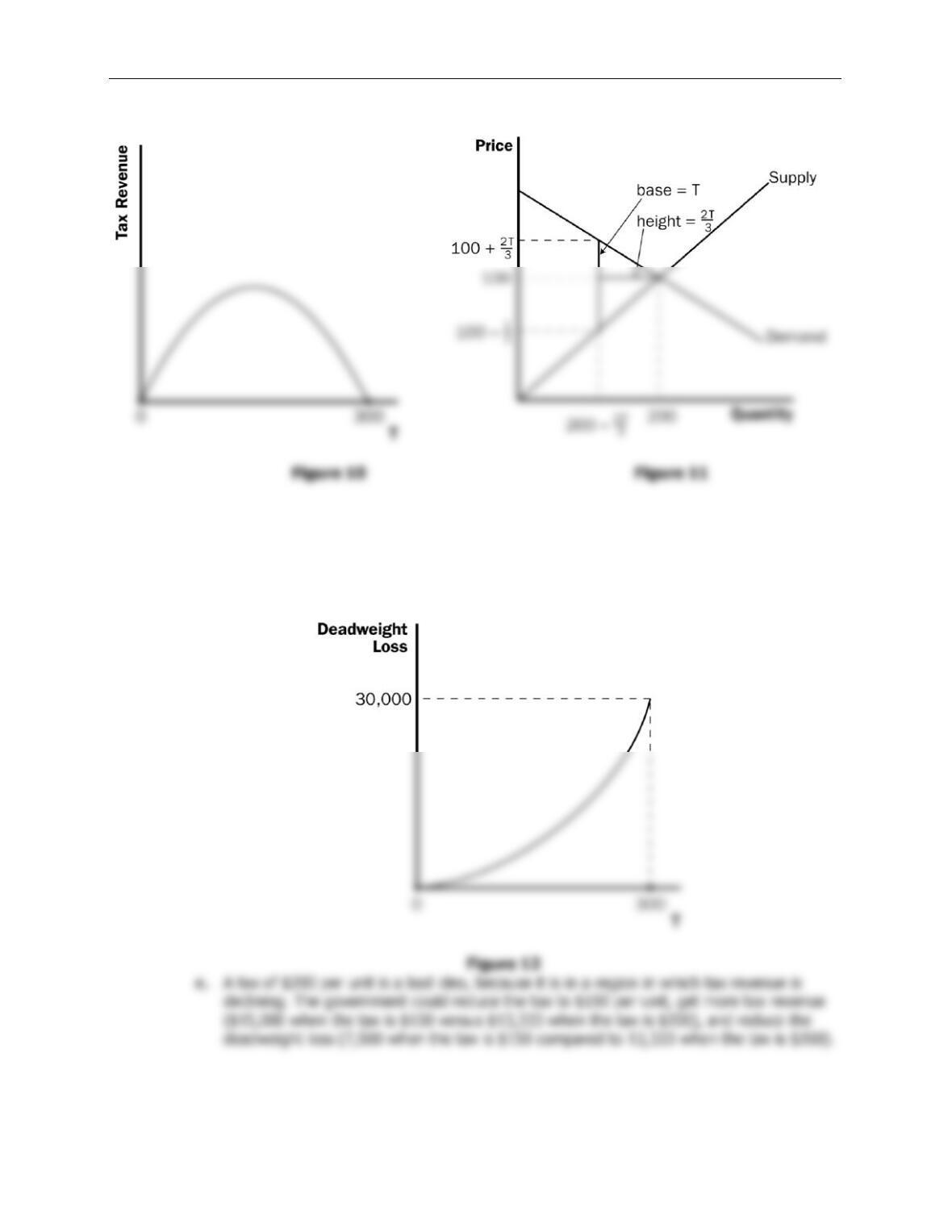

d. As Figure 11 shows, the area of the triangle (laid on its side) that represents the

deadweight loss is 1/2 × base × height, where the base is the change in the price, which

is the size of the tax (

T

) and the height is the amount of the decline in quantity (2

T

/3).

So the deadweight loss equals 1/2 ×

T

× 2

T

/3 =

T

2/3. This rises exponentially from 0

(when

T

= 0) to 30,000 when

T

= 300, as shown in Figure 12.