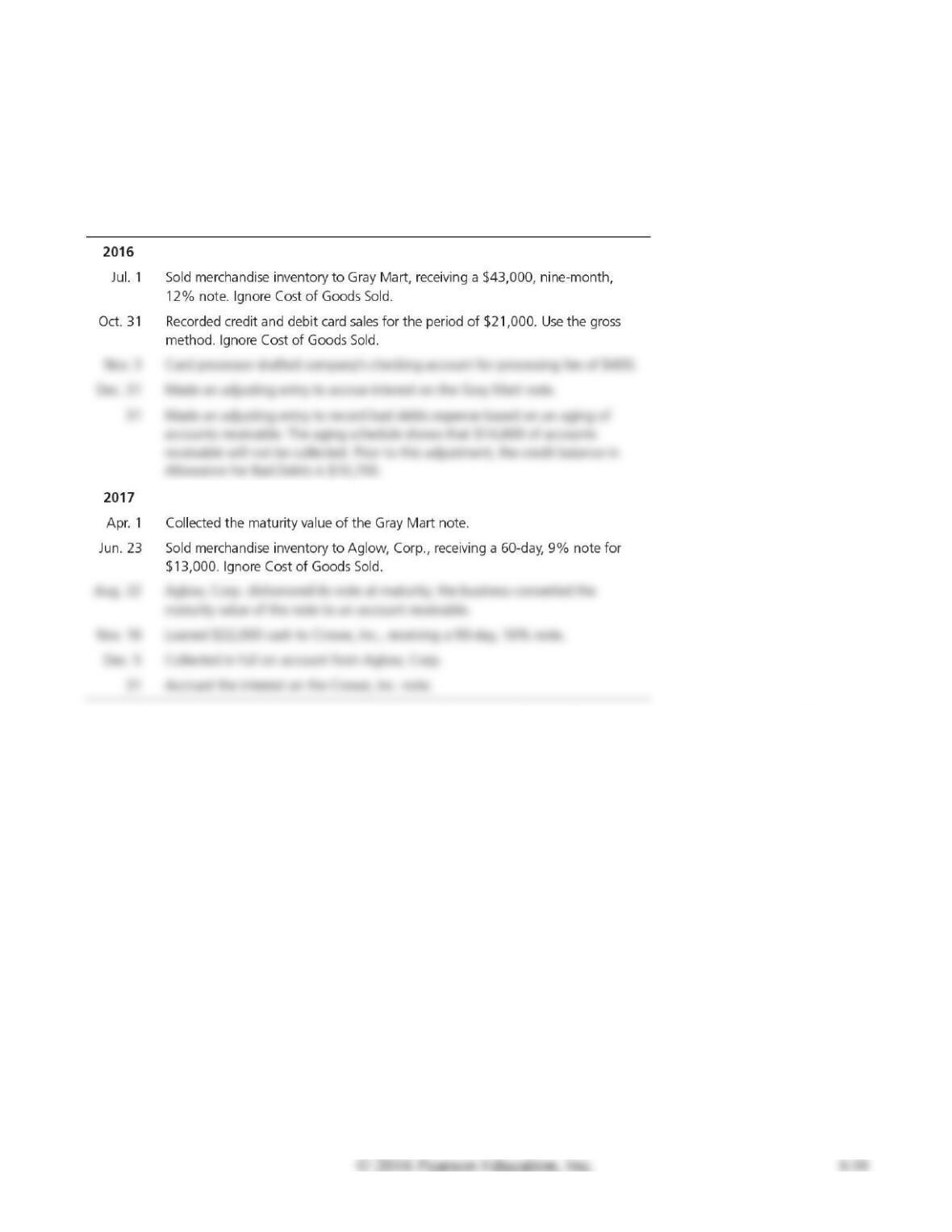

P8-37B Accounting for uncollectible accounts (aging-of-receivables method), credit card sales,

notes receivable, and accrued interest revenue

Learning Objectives 1, 3, 4

Dec. 31, 2016 Bad Debts Expense $3,900

Comfy Recliner Chairs completed the following selected transactions:

Record the transactions in the journal of Comfy Recliner Chairs. Explanations are not required. (For

notes stated in days, use a 360-day year. Round to the nearest dollar.)

SOLUTION

Date

Accounts and Explanation

Debit

Credit

2016

Jul. 1

Notes Receivable—Gray Mart

43,000

Sales Revenue

43,000

Cash

21,000

Sales Revenue

21,000

Nov. 3

Credit Card Expense

Interest Receivable

Interest Revenue

2,580

Bad Debts Expense

Allowance for Bad Debts

3,900

($14,600 – $10,700 = $3,900)

2017

Cash ($43,000 + $2,580 + $1,290)

46,870

2,580

1,290

43,000

Notes Receivable—Aglow, Corp.

13,000

Sales Revenue

13,000

Accounts Receivable—Aglow, Corp.

13,195

13,000

Notes Receivable—Crowe, Inc.

22,000

Cash

22,000

Cash

13,195

Accounts Receivable—Aglow, Corp.

13,195

Interest Receivable

Interest Revenue

($22,000 × 0.16 × 45/360)

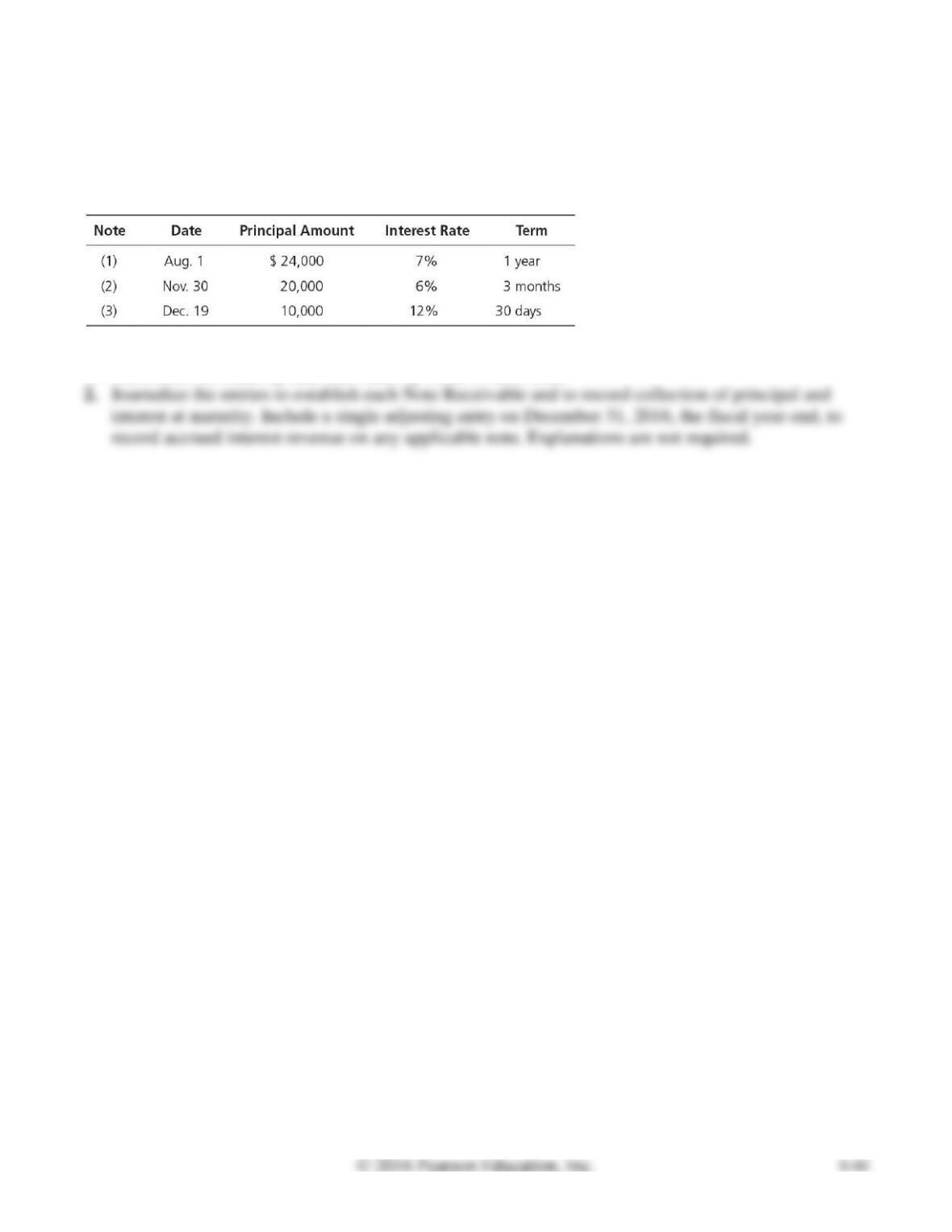

P8-38B Accounting for notes receivable and accruing interest

Learning Objective 4

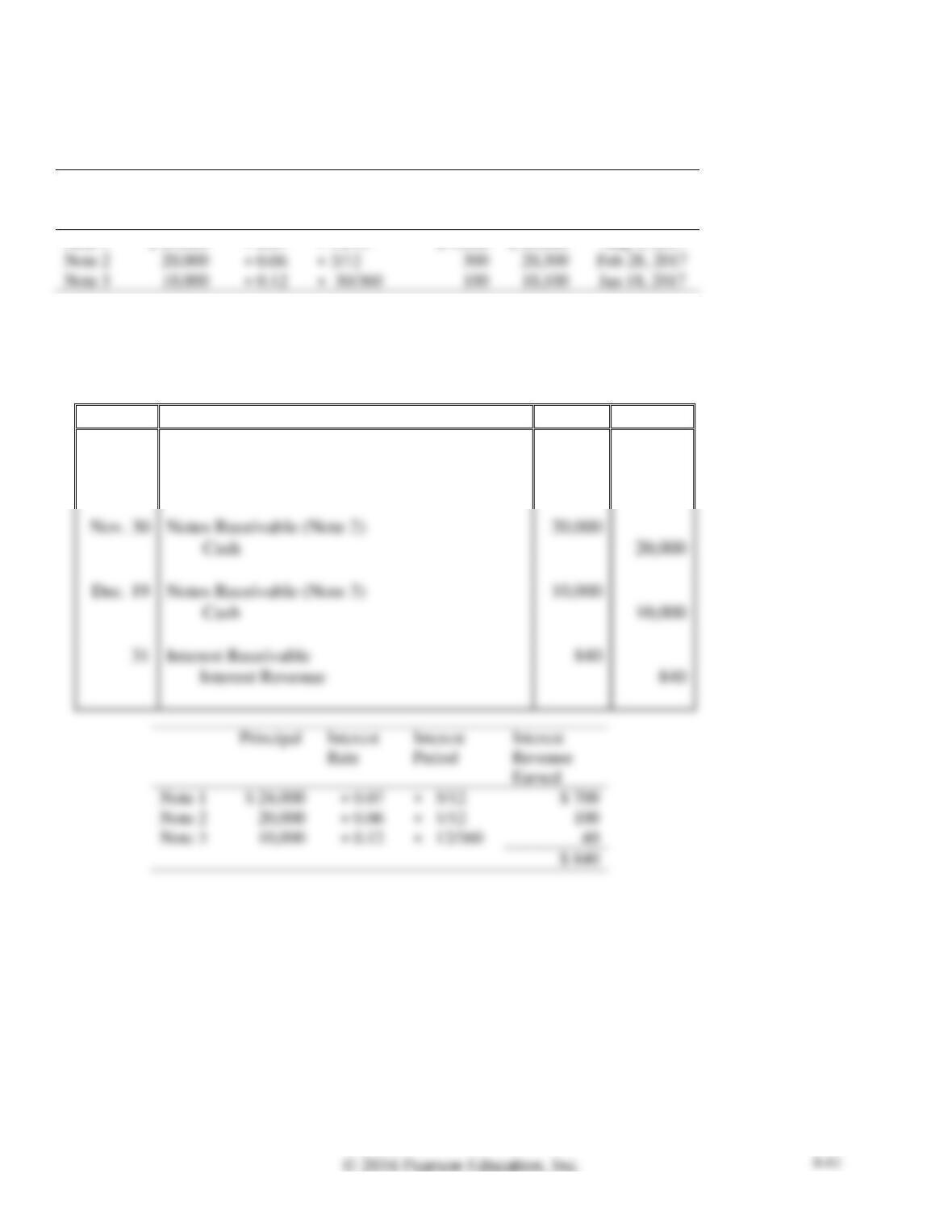

1. Note 2 Maturity Value $20,300

Christie Realty loaned money and received the following notes during 2016.

Requirements

1. Determine the maturity date and maturity value of each note.

SOLUTION

Requirement 1

Principal

Interest

Rate

Interest

Period

Interest

Revenue

Earned

Maturity

Value

(P + I)

Maturity Date

Note 1

$ 24,000

× 0.07

× 12/12

$ 1,680

$ 25,680

Aug 1, 2017

Note 2

20,000

× 0.06

× 3/12

300

20,300

Feb 28, 2017

Requirement 2

Principal

Interest

Interest

Interest

Earned

Note 2

20,000

Notes Receivable (Note 2)

20,000

Cash

20,000

Notes Receivable (Note 3)

10,000

Cash

10,000

Interest Receivable

Interest Revenue

Date

Accounts and Explanation

Debit

Credit

2016

Aug. 1

Notes Receivable (Note 1)

24,000

Cash

24,000

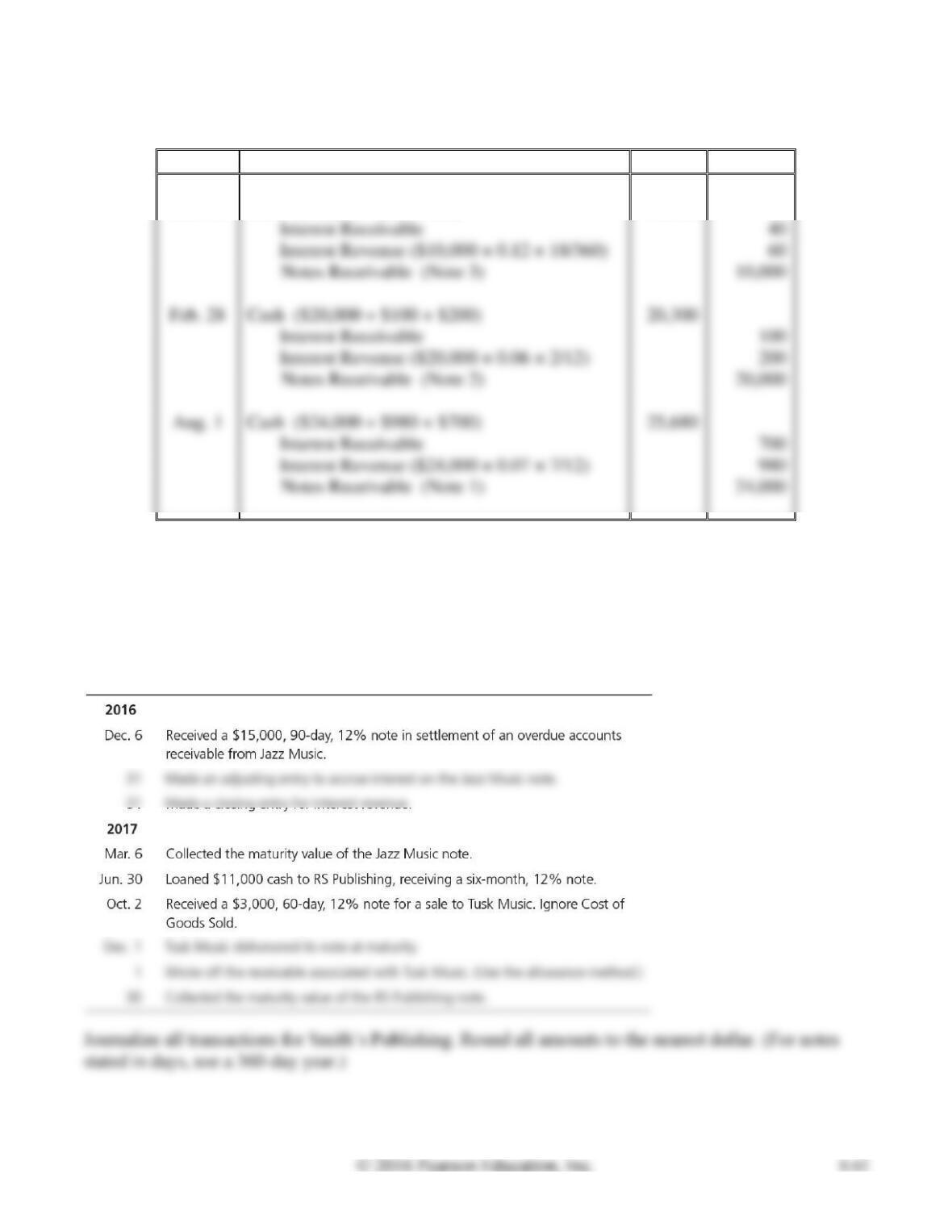

P8-38B, cont.

Requirement 2, cont.

Date

Accounts and Explanation

Debit

Credit

2017

Jan. 18

Cash ($10,000 + $40 + $60)

10,100

Interest Receivable

Cash ($20,000 + $100 + $200)

20,300

Interest Receivable

Cash ($24,000 + $980 + $700)

25,680

Interest Receivable

P8-39B Accounting for notes receivable, dishonored notes, and accrued interest revenue

Learning Objective 4

March 6, 2017 Interest Revenue $325

Consider the following transactions for Smith’s Publishing.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

2016

Dec. 6

Notes Receivable—Jazz Music

15,000

Accounts Receivable—Jazz Music

15,000

Interest Receivable

Interest Revenue ($15,000 × 0.12 × 25/360)

Interest Revenue

2017

Cash

15,450

Interest Receivable

15,000

Notes Receivable—RS Publishing

11,000

Cash

11,000

Notes Receivable—Tusk Music

Sales Revenue

Dec. 1

Accounts Receivable—Tusk Music

Allowance for Bad Debts

Accounts Receivable—Tusk Music

Cash

11,660

11,000

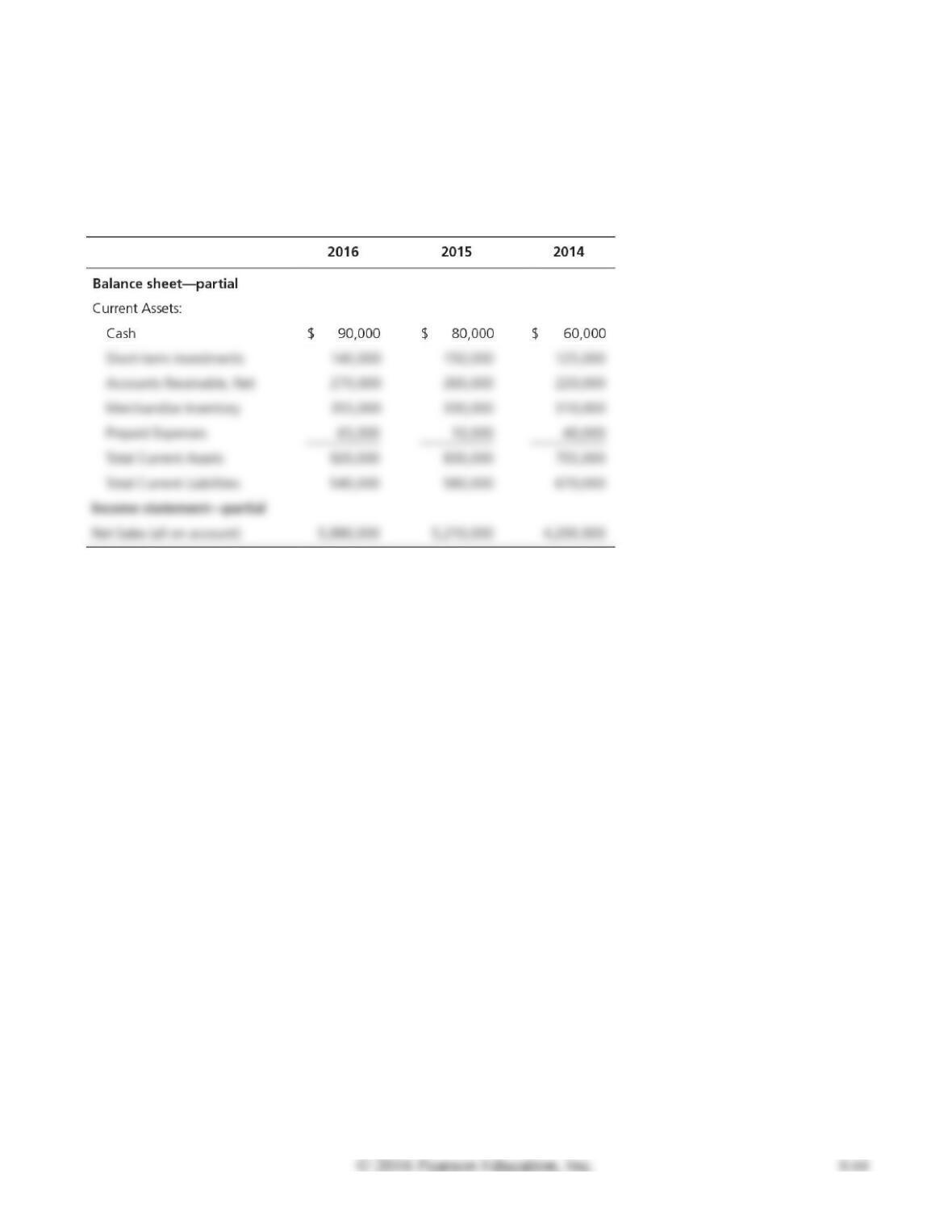

P8–40B Using ratio data to evaluate a company’s financial position

Learning Objective 5

1. Days’ sales in receivables (2016) 16 days

The comparative financial statements of True Beauty Cosmetic Supply for 2016, 2015, and 2014 include

the data shown here:

Requirements

1. Compute these ratios for 2016 and 2015:

a. Acid-test ratio (Round to two decimals.)

b. Accounts receivable turnover (Round to two decimals.)

c. Days’ sales in receivables (Round to the nearest whole day.)

2. Considering each ratio individually, which ratios improved from 2015 to 2016 and which ratios

deteriorated? Is the trend favorable or unfavorable for the company?

SOLUTION

Requirement 1

a. Acid-test ratio = (Cash including cash equivalents + Short-term investments + Net current

Requirement 2

The acid-test ratio increased from 2015 to 2016. This trend is favorable to the company.

Continuing Problem

P8-41 Accounting for uncollectible accounts using the allowance method

This problem continues the Daniels Consulting situation from Problem P7-33 of Chapter 7 and Problem

P6-38 of Chapter 6. Daniels Consulting reviewed the receivables list from the January transactions.

Daniels uses the allowance method for receivables, estimating uncollectibles to be 6% of January sales

revenue of $8,180. Daniels identified on February 15 that a customer was not going to pay his receivable

of $176.

Requirements

1. Journalize the January 31 entry to record and establish the allowance using the percent-of-sales

method for January sales revenue.

2. Journalize the entry to record the write-off of the customer’s bad debt.

SOLUTION

Requirements 1 and 2

Date

Accounts and Explanation

Debit

Credit

Jan. 31

Bad Debts Expense

491

Allowance for Bad Debts

176

Practice Set

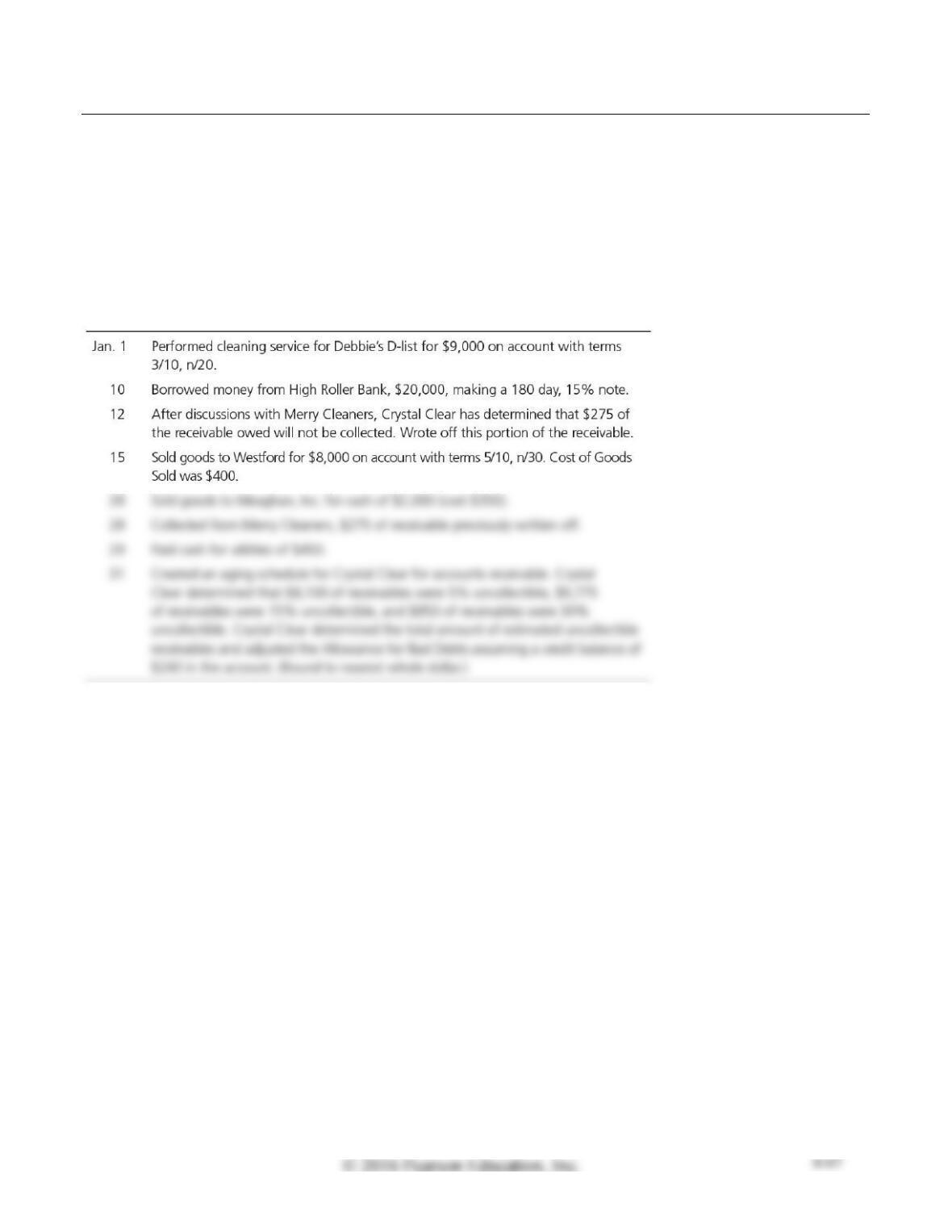

This problem continues the Crystal Clear Cleaning problem begun in Chapter 2 and continued through

Chapters 3–7.

P8-42 Accounting for uncollectible accounts using the allowance method and reporting net

accounts receivable on the balance sheet

Crystal Clear Cleaning uses the allowance method to estimate bad debts. Consider the following January

transactions for Crystal Clear:

Requirements

1. Prepare all required journal entries for Crystal Clear.

2. Show how net accounts receivable would be reported on the balance sheet as of January 31, 2018.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

2018

Jan. 1

Accounts Receivable—Debbie’s D-list

9,000

Service Revenue

9,000

Cash

Notes Payable—High Roller Bank

Allowance for Bad Debts

Accounts Receivable—Westford

8,000

Sales Revenue

8,000

Cost of Goods Sold

Merchandise Inventory

Cash

2,000

Sales Revenue

2,000

Cost of Goods Sold

Merchandise Inventory

Accounts Receivable—Merry Cleaners

Allowance for Bad Debts

Cash

Utilities Expense

Cash

Bad Debts Expense

1,886

1,886

P8-42, cont.

Accounts Receivable

× 30.0%

$ 16,599

Critical Thinking

Decision Case 8-1

Weddings on Demand sells on account and manages its own receivables. Average experience for the

past three years has been as follows:

Unhappy with the amount of bad debts expense she has been experiencing, Aledia Sanchez, controller,

is considering a major change in the business. Her plan would be to stop selling on account altogether

but accept either cash, credit cards, or debit cards from her customers. Her market research indicates that

if she does so, her sales will increase by 10% (i.e., from $350,000 to $385,000), of which $200,000 will

be credit or debit card sales and the rest will be cash sales. With a 10% increase in sales, there will also

be a 10% increase in Cost of Goods Sold. If she adopts this plan, she will no longer have bad debts

expense, but she will have to pay a fee on debit/credit card transactions of 2% of applicable sales. She

also believes this plan will allow her to save $5,000 per year in other operating expenses.

Should Sanchez start accepting credit cards and debit cards? Show the computations of net income

under her present arrangement and under the plan.

SOLUTION

Actual

New Plan

Expected

Sales Revenue

$ 350,000

× 1.10 =

$ 385,000

Cost of Goods Sold

$ 210,000

× 1.10 =

$ 231,000

Bad Debts Expense

4,000

Credit Card Expense (200,000 × 2%)

4,000

Other Expenses

61,000

56,000

Total Expenses

275,000

291,000

Net Income

$ 75,000

$ 94,000

Decision Case 8-2

Pauline’s Pottery has always used the direct write-off method to account for uncollectibles. The

company’s revenues, bad debt write-offs, and year-end receivables for the most recent year follow:

The business is applying for a bank loan, and the loan officer requires figures based on the allowance

method of accounting for bad debts. In the past, bad debts have run about 4% of revenues.

Requirements

Pauline must give the banker the following information:

1. How much more or less would net income be for 2016 if Pauline’s Pottery were to use the allowance

method for bad debts? Assume Pauline uses the percent-of-sales method.

2. How much of the receivables balance at the end of 2016 does Pauline’s Pottery actually expect to

collect? (Disregard beginning account balances for the purpose of this question.)

3. Explain why net income is more or less using the allowance method versus the direct write-off

method for uncollectibles.

SOLUTION

Requirement 1

Fraud Case 8-1

Dylan worked for a propane gas distributor as an accounting clerk in a small Midwestern town. Last

winter, his brother Mike lost his job at the machine plant. By January, temperatures were sub-zero, and

Mike had run out of money. Dylan saw that Mike’s account was overdue, and he knew Mike needed

another delivery to heat his home. He decided to credit Mike’s account and debit the balance to the parts

inventory because he knew the parts manager, the owner’s son, was incompetent and would never notice

the extra entry. Months went by, and Dylan repeated the process until an auditor ran across the charges

by chance. When the owner fired Dylan, he said, “If you had only come to me and told me about Mike’s

situation, we could have worked something out.”

Requirements

1. What can a business like this do to prevent employee fraud of this kind?

2. What effect would Dylan’s actions have on the balance sheet? The income statement?

3. How much discretion does a business have with regard to accommodating hard- ship situations?

SOLUTION

Requirement 1

Dylan’s journal entries should be reviewed by a manager. Employees should not be able to access

Financial Statement Case 8-1

Use Starbucks Corporation’s Fiscal 2013 Annual Report and the Note 1 data on “Allowance for

Requirements

1. How much accounts receivables did Starbucks report as of September 29, 2013? As of September

30, 2012?

2. Refer to Note 1, “Allowance for Doubtful Accounts.” How does Starbucks calculate allowance for

doubtful accounts? What was the amount of the account as of September 29, 2013? As of September

30, 2012?

3. Compute Starbucks’s acid-test ratio at the end of 2013. If all the current liabilities came due

immediately, could Starbucks pay them?

4. Compute Starbucks’s accounts receivable turnover at the end of 2013. Use total net revenues.

5. Compute Starbucks’s days’ sales in receivables at the end of 2013.

6. How does Starbucks compare to Green Mountain Coffee Roasters, Inc. on the basis of the acid-

test ratio, accounts receivable turnover, and days’ sales in receivables?

SOLUTION

Requirement 1

Financial Statement Case 8-1, cont.

Requirement 3

Requirement 4

Requirement 5

Days’ sales in receivables = 365 days / Accounts receivable turnover ratio

2011

= 365 days / 28.44

= 13 days (rounded)

Requirement 6

Starbucks has much better ratios regarding collectability of receivables while falling short of Green