Chapter 7

Internal Control and Cash

Review Questions

1. What is internal control?

Internal control is the organizational plan and all the related measures adopted by an entity to

2. How does the Sarbanes-Oxley Act relate to internal controls?

The Sarbanes-Oxley Act requires public companies to issue an internal control report, which is a

report on the internal controls as part of the audit report.

3. What are the five components of internal control? Briefly explain each component.

The five components of internal control are: control procedures, risk assessment, information

4. What is the difference between an internal auditor and external auditor?

Internal auditors are employees of the business who ensure that the company’s employees are

5. What is separation of duties?

Separation of duties limits fraud and promotes the accuracy of the accounting records by dividing

6. List internal control procedures related to e-commerce.

Internal control procedures related to e-commerce are encryption and firewalls.

7. What are some limitations of internal controls?

Limitations to internal controls relate to cost and benefit. The better the controls, the more they can

8. How do businesses control cash receipts over the counter?

Businesses control cash receipts over the counter by using a cash register. The cash register only

9. How do businesses control cash receipts by mail?

Businesses control cash receipts by mail by separating the check and the remittance advice in the

10. What are the steps taken to ensure control over purchases and payments by check?

11. What are the controls needed to secure the petty cash fund?

12. When are the only times the Petty Cash account is used in a journal entry?

The only times the Petty Cash account is debited are when the fund is started or when its amount is

increased. If the Petty Cash account is decreased, the account is credited.

7-3

13. What are some common controls used with a bank account?

Common controls used with a bank account are the use of a signature card, deposit tickets, checks,

bank statements, and bank reconciliations.

14. What is a bank reconciliation?

15. List some examples of timing differences, and for each difference, determine if it would affect the

book side of the reconciliation or the bank side of the reconciliation.

Examples of timing differences are:

16. Why is it necessary to record journal entries after the bank reconciliation has been prepared? Which

side of the bank reconciliation requires journal entries?

Once the bank reconciliation is complete, all items that affect the book side of the reconciliation

17. What does the cash ratio help determine, and how is it calculated?

The cash ratio helps to determine a company’s ability to meet its short-term obligations. It is

calculated as follows: Cash ratio = (Cash + Cash equivalents) / Total current liabilities

Short Exercises

S7-1 Defining internal control

Learning Objective 1

Internal controls are designed to safeguard assets, encourage employees to follow company policies,

promote operational efficiency, and ensure accurate accounting records.

Requirements

1. Which objective do you think is most important?

2. Which objective do you think the internal controls must accomplish for the business to survive?

Give your reason.

7-4

SOLUTION

Requirement 1

S7-2 Applying internal control over cash receipts

Learning Objective 2

Sandra Kristof sells furniture for McKinney Furniture Company. Kristof is having financial problems

and takes $650 that she received from a customer. She rang up the sale through the cash register. What

will alert Megan McKinney, the controller, that something is wrong?

SOLUTION

S7-3 Applying internal control over cash receipts by mail

Learning Objective 2

Review the internal controls over cash receipts by mail presented in the chapter. Exactly what is

accomplished by the final step in the process, performed by the controller?

SOLUTION

S7-4 Applying internal control over cash payments by check

Learning Objective 3

A purchasing agent for Franklin Office Supplies receives the goods that he purchases and also approves

payment for the goods.

Requirements

1. How could this purchasing agent cheat his company?

2. How could Franklin avoid this internal control weakness?

7-5

SOLUTION

Requirement 1

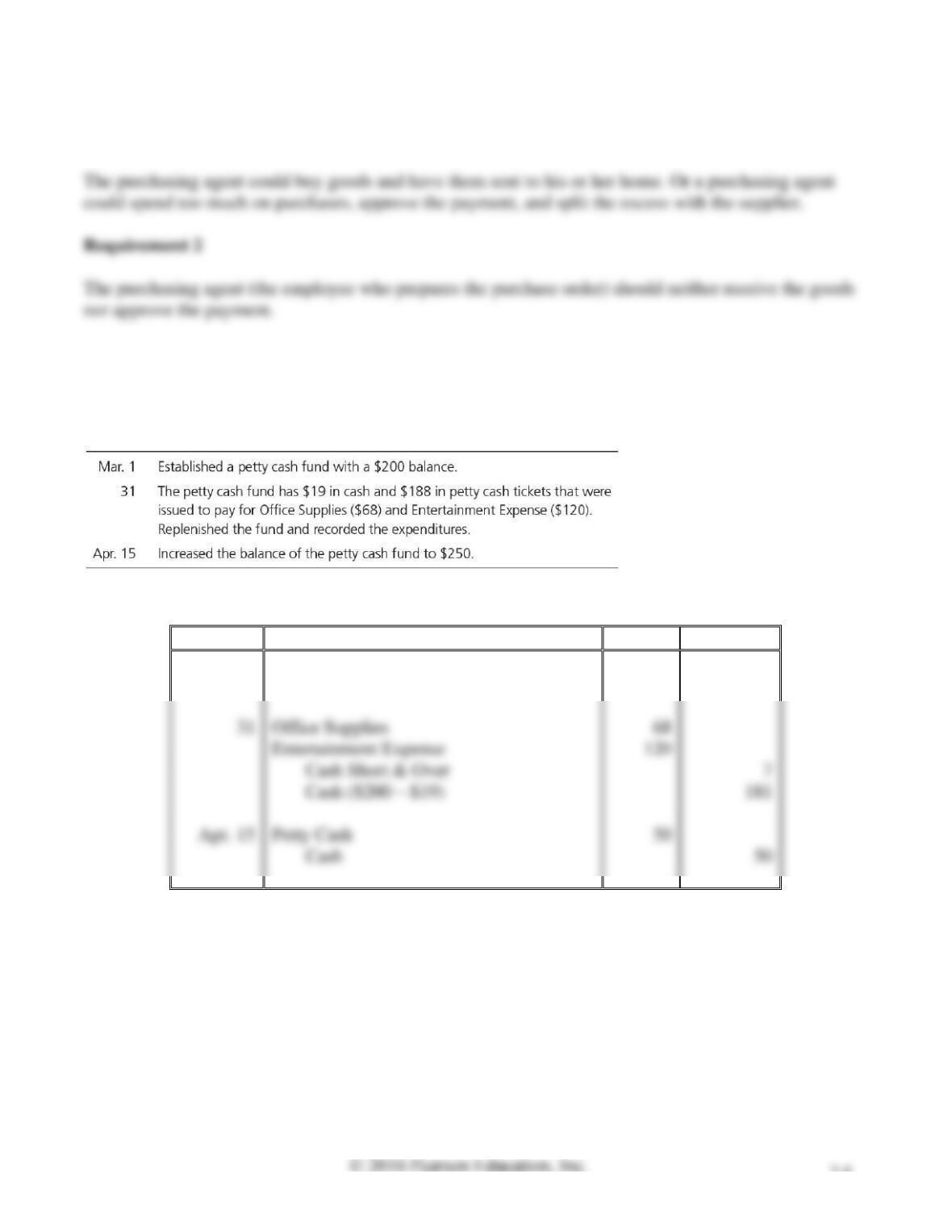

S7-5 Journalizing petty cash

Learning Objective 4

Prepare the journal entries for the following petty cash transactions of Pawnee Gaming Supplies:

SOLUTION

Date

Accounts and Explanation

Debit

Credit

Mar. 1

Petty Cash

200

Cash

200

Office Supplies

Entertainment Expense

120

Cash Short & Over

Cash ($200 – $19)

181

Petty Cash

Cash

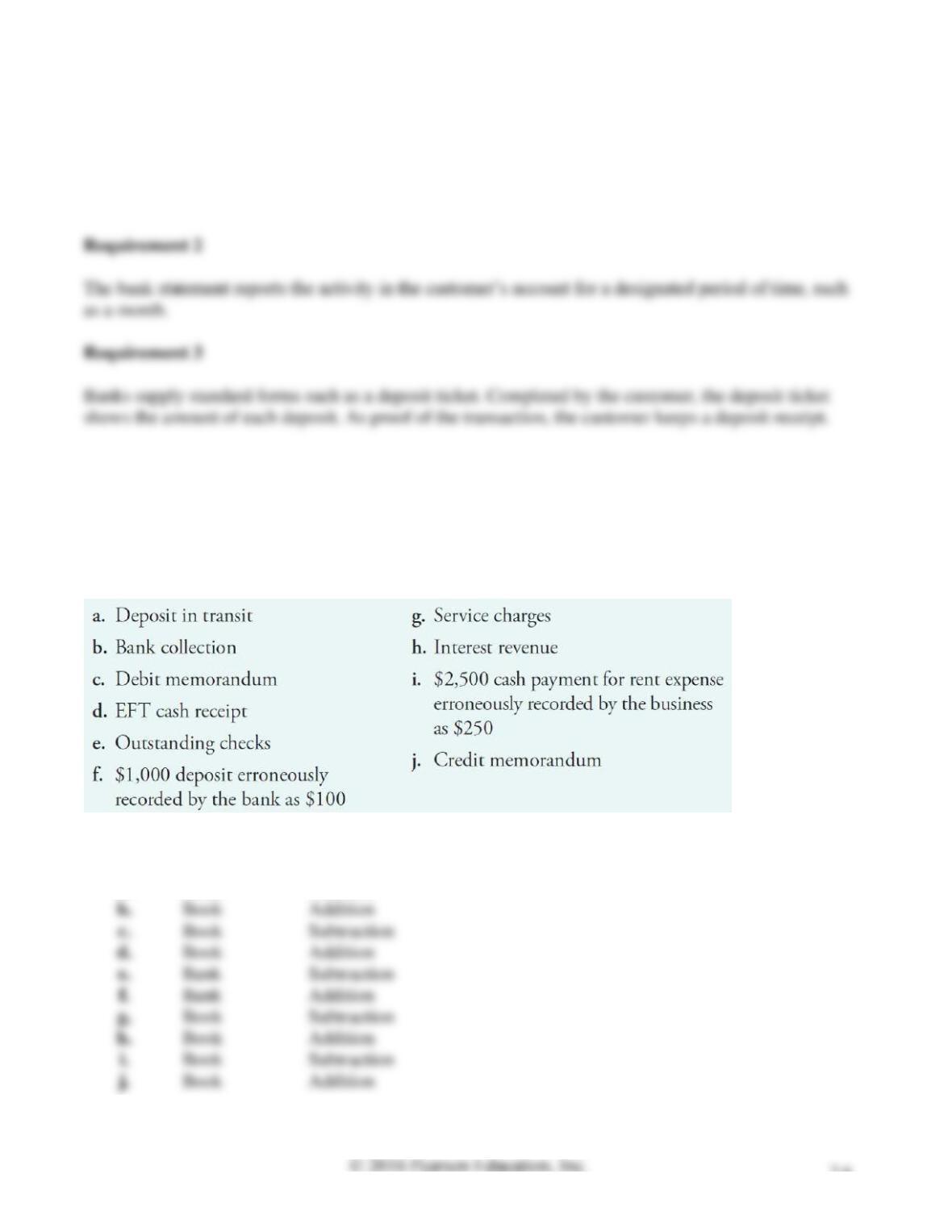

S7-6 Understanding bank account controls

Learning Objective 5

Answer the following questions about the controls in bank accounts:

Requirements

1. Which bank control protects against forgery?

2. Which bank control reports the activity in the customer’s account each period?

3. Which bank control confirms the amount of money put into the bank account?

7-6

SOLUTION

Requirement 1

The bank’s requirement that each authorized person sign a signature card will help protect against

forgery.

S7-7 Identifying timing differences related to a bank reconciliation

Learning Objective 5

For each timing difference listed, identify whether the difference would be reported on the book side of

the reconciliation or the bank side of the reconciliation. In addition, identify whether the difference

would be an addition or subtraction.

SOLUTION

a.

Bank

Addition

Book

Addition

Book

Subtraction

Book

Addition

Bank

Subtraction

Bank

Addition

g.

Book

Subtraction

Book

Addition

Book

Subtraction

S7-8 Preparing a bank reconciliation

Learning Objective 5

The Cash account of Safety Security Systems reported a balance of $2,450 at December 31, 2016. There

were outstanding checks totaling $1,700 and a December 31 deposit in transit of $300. The bank

statement, which came from Park Cities Bank, listed the December 31 balance of $4,460. Included in

the bank balance was a collection of $620 on account from Brendan Ballou, a Safety customer who pays

the bank directly. The bank statement also shows a $20 service charge and $10 of interest revenue that

Safety earned on its bank balance. Prepare Safety’s bank reconciliation at December 31.

SOLUTION

SAFETY SECURITY SYSTEMS

Bank Reconciliation

December 31, 2016

BANK

BOOK

7-8

Note: Short Exercise S7-8 must be completed before attempting Short Exercise S7-9.

S7-9 Recording transactions from a bank reconciliation

Learning Objective 5

Review your results from preparing Safety Security Systems’s bank reconciliation in Short Exercise S7–

8. Journalize the company’s transactions that arise from the bank reconciliation. Include an explanation

with each entry.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

Dec. 31

Cash

620

31

Cash

31

Bank Expense

S7-10 Computing the cash ratio

Learning Objective 6

Beautiful Banners reported the following figures in its financial statements:

Compute the cash ratio for Beautiful Banners.

SOLUTION

7-9

Exercises

E7-11 Understanding Sarbanes-Oxley and identifying internal control strengths and weaknesses

Learning Objective 1

The following situations suggest a strength or a weakness in internal control.

a. Top managers delegate all internal control procedures to the accounting department.

b. Accounting department staff (or the bookkeeper) orders merchandise and approves invoices for

payment.

c. Cash received over the counter is controlled by the sales clerk, who rings up the sale and places the

cash in the register. The sales clerk matches the total recorded by the register to each day’s cash

sales.

d. The employee who signs checks need not examine the payment packet because he is confident the

amounts are correct.

Requirements

1. Define internal control.

2. The system of internal control must be tested by external auditors. What law or rule requires this

testing?

3. Identify each item in the list above as either a strength or a weakness in internal control, and give

your reason for each answer.

SOLUTION

Requirement 1

Internal control is the organizational plan and all the related measures adopted by an entity to safeguard

7-10

E7-12 Identifying internal controls

Learning Objective 1

Consider each situation separately. Identify the missing internal control procedure from these

characteristics:

• Assignment of responsibilities

• Separation of duties

• Audits

• Electronic devices

• Other controls (specify)

a. While reviewing the records of Quality Pharmacy, you find that the same employee orders

merchandise and approves invoices for payment.

b. Business is slow at Amazing Amusement Park on Tuesday, Wednesday, and Thursday nights. To

reduce expenses, the business decides not to use a ticket taker on those nights. The ticket seller

(cashier) is told to keep the tickets as a record of the number sold.

c. The same trusted employee has served as cashier for 12 years.

d. When business is brisk, Fast Mart deposits cash in the bank several times during the day. The

manager at one store wants to reduce the time employees spend delivering cash to the bank, so he

starts a new policy. Cash will build up over weekends, and the total will be deposited on Monday.

e. Grocery stores such as Convenience Market and Natural Foods purchase most merchandise from a

few suppliers. At another grocery store, the manager decides to reduce paperwork. He eliminates the

requirement that the receiving department prepare a receiving report listing the goods actually

received from the supplier.

SOLUTION

a.

Separation of duties

Separation of duties

c.

Other controls (no job rotation)

competent, reliable and ethical personnel)

e.

Other controls (documents and records – no receiving report)

E7-13 Evaluating internal control over cash receipts

Learning Objective 2

Dogtopia sells pet supplies and food and handles all sales with a cash register. The cash register displays

the amount of the sale. It also shows the cash received and any change returned to the customer. The

register also produces a customer receipt but keeps no internal record of the transactions. At the end of

the day, the clerk counts the cash in the register and gives it to the cashier for deposit in the company

bank account.

Requirements

1. Identify the internal control weakness over cash receipts.

2. What could you do to correct the weakness?

SOLUTION

Requirement 1

There is a weakness in internal control over cash receipts.

• The cash register does not keep an internal record of sales.

E7-14 Evaluating internal control over cash payments

Learning Objective 3

Gary’s Great Cars purchases high-performance auto parts from a Nebraska vendor. Dave Simon, the

accountant for Gary’s, verifies receipt of merchandise and then prepares, signs, and mails the check to

the vendor.

Requirements

1. Identify the internal control weakness over cash payments.

2. What could the business do to correct the weakness?

SOLUTION

Requirement 1

The same person is responsible for verifying receipt of merchandise, authorizing payment, and preparing

the payment.

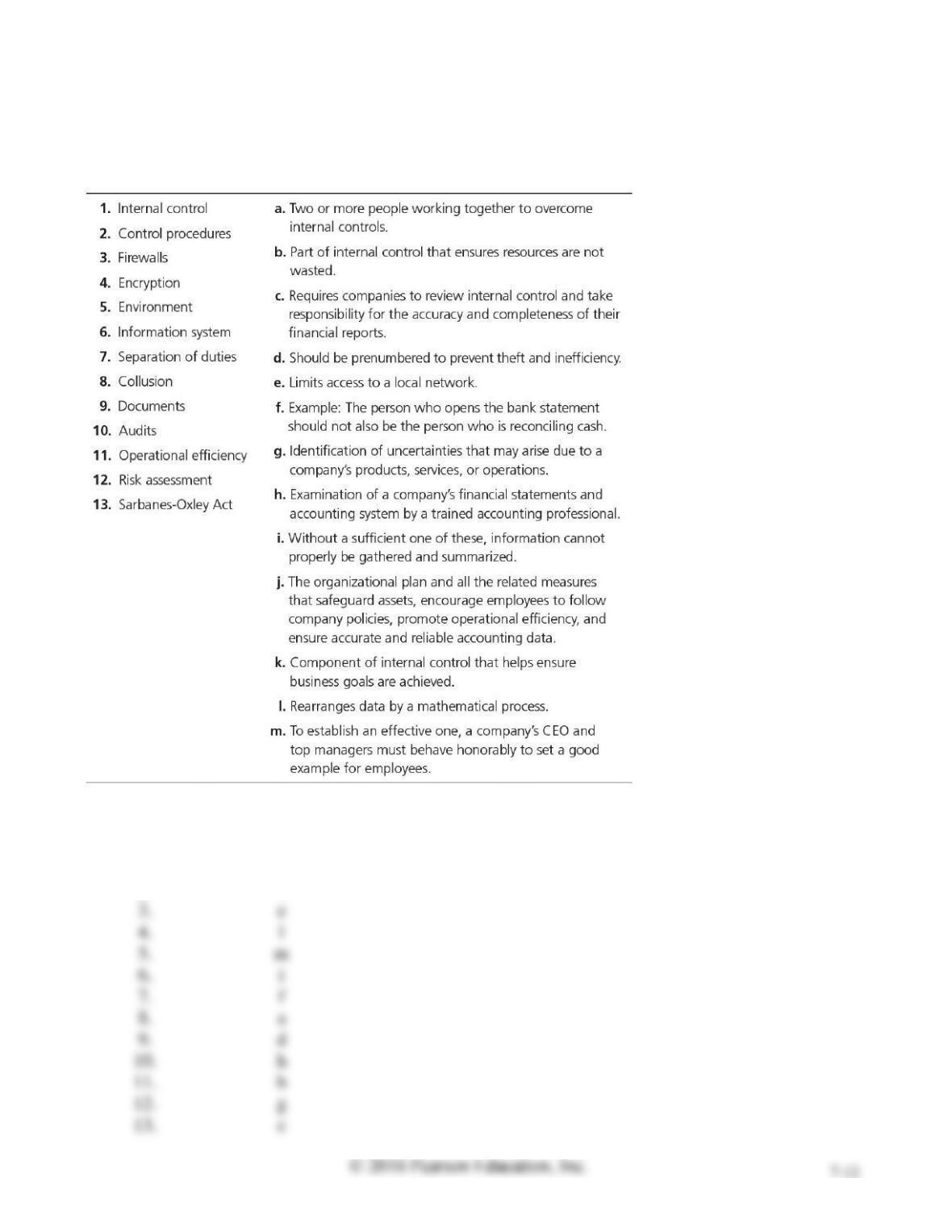

E7-15 Understanding internal control, components, procedures, and laws

Learning Objectives 1, 2, 3

Match the following terms with their definitions.

SOLUTION

1.

j

2.

k

3.

e

4.

l

5.

6.

i

7.

f

8.

a

9.

d

h

7-13

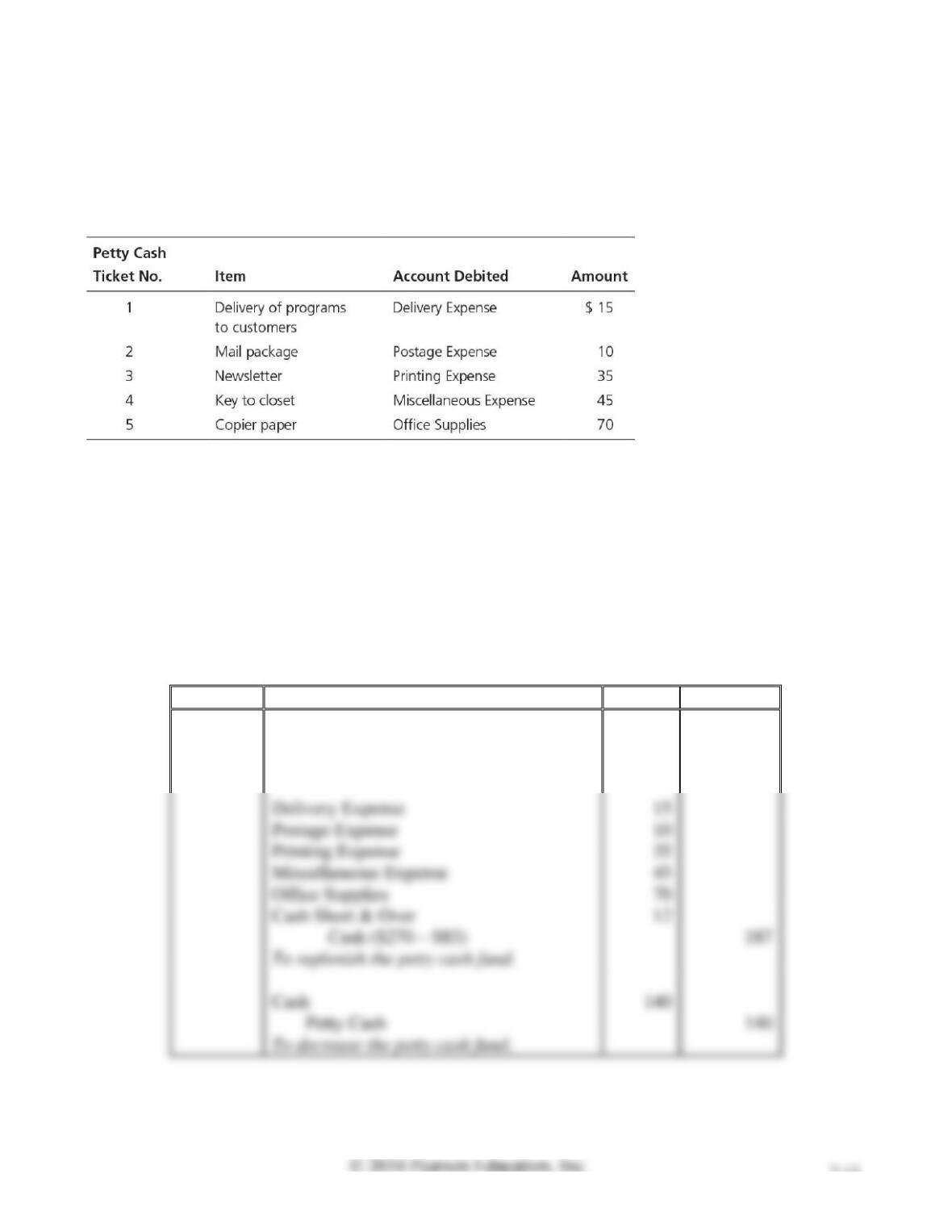

E7-16 Accounting for petty cash

Learning Objective 4

2. Cash Short & Over $12

Joy’s Dance Studio created a $270 imprest petty cash fund. During the month, the fund custodian

authorized and signed petty cash tickets as follows:

Requirements

1. Make the general journal entry to create the petty cash fund. Include an explanation.

2. Make the general journal entry to record the petty cash fund replenishment. Cash in the fund totals

$83. Include an explanation.

3. Assume that Joy’s Dance Studio decides to decrease the petty cash fund to $130. Make the general

journal entry to record this decrease.

SOLUTION

Requirement 1, 2, 3

Date

Accounts and Explanation

Debit

Credit

Petty Cash

270

Cash

270

To open the petty cash fund.

Delivery Expense

Postage Expense

Printing Expense

Miscellaneous Expense

Office Supplies

Cash Short & Over

Cash ($270 – $83)

187

To replenish the petty cash fund.

Cash

140

Petty Cash

140

To decrease the petty cash fund.

E7-17 Controlling petty cash

Learning Objective 4

2. March 31, Cash CR $226

Jazzy Night Club maintains an imprest petty cash fund of $250, which is under the control of Sandra

Morgan. At March 31, the fund holds $24 cash and petty cash tickets for office supplies, $224, and

delivery expense, $15.

Requirements

1. Explain how an imprest petty cash system works.

2. Journalize the establishment of the petty cash fund on March 1 and the replenishing of the fund on

March 31.

3. Prepare a T-account for Petty Cash, and post to the account. What is the balance of the Petty Cash

account at all times?

SOLUTION

Requirement 1

Maintaining the Petty Cash account at its designated balance is the nature of an imprest system. The

Requirement 3

E7-18 Classifying bank reconciliation items

Learning Objective 5

The following items could appear on a bank reconciliation:

a. Outstanding checks, $670.

b. Deposits in transit, $1,500.

c. NSF check from customer, #548, for $175.

d. Bank collection of note receivable of $800, and interest of $80.

e. Interest earned on bank balance, $20.

f. Service charge, $10.

g. The business credited Cash for $200. The correct amount was $2,000.

h. The bank incorrectly decreased the business’s account by $350 for a check written by another

business.

Classify each item as (1) an addition to the book balance, (2) a subtraction from the book balance, (3) an

addition to the bank balance, or (4) a subtraction from the bank balance.

SOLUTION

a.

(4) a subtraction from the bank balance

(3) an addition to the bank balance

(2) a subtraction from the book balance

(1) an addition to the book balance

(1) an addition to the book balance

(2) a subtraction from the book balance

(2) a subtraction from the book balance

(3) an addition to the bank balance

7-16

E7-19 Preparing a bank reconciliation

Learning Objective 5

1. Adjusted Balance $1,270

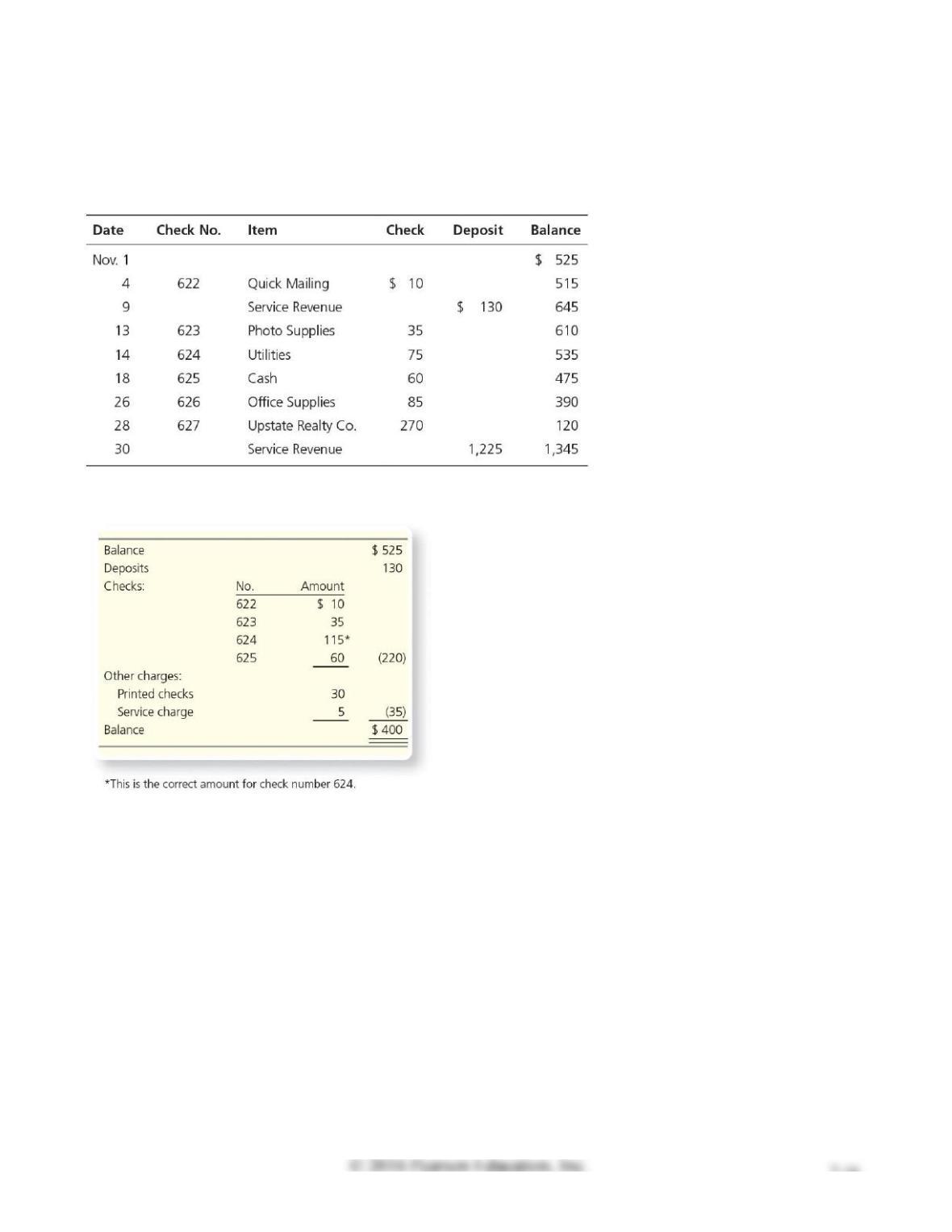

Henderson Photography’s checkbook lists the following:

Henderson’s November bank statement shows the following:

Requirements

1. Prepare Henderson Photography’s bank reconciliation at November 30, 2016.

2. How much cash does Henderson actually have on November 30, 2016?

3. Journalize any transactions required from the bank reconciliation.

SOLUTION

Requirement 1

HENDERSON PHOTOGRAPHY

Bank Reconciliation

November 30, 2016

BANK

BOOK

Balance, November 30, 2016

Balance, November 30, 2016

Deposit in transit

LESS:

LESS:

No. 626

Printed checks

No. 627

Service charge

Requirement 2

Henderson has $1,270 in cash on November 30, 2016.

Requirement 3

Date

Accounts and Explanation

Debit

Credit

Nov. 30

Utilities Expense

40

Cash

40

Bank Expense

30

Cash

30

Bank Expense

Cash

7-18

E7-20 Preparing a bank reconciliation

Learning Objective 5

1. Book Deductions $348

Fred White Corporation operates four bowling alleys. The business just received the October 31, 2016,

bank statement from City National Bank, and the statement shows an ending balance of $885. Listed on

the statement are an EFT rent collection of $410, a service charge of $10, NSF checks totaling $65, and

a $30 charge for printed checks. In reviewing the cash records, the business identified outstanding

checks totaling $470 and a deposit in transit of $1,785. During October, the business recorded a $270

check by debiting Salaries Expense and crediting Cash for $27. The business’s Cash account shows an

October 31 balance of $2,138.

Requirements

1. Prepare the bank reconciliation at October 31.

2. Journalize any transactions required from the bank reconciliation.

SOLUTION

Requirement 1

FRED WHITE CORPORATION

Bank Reconciliation

October 31, 2016

BANK

BOOK

Balance, October 31, 2016

$ 885

Balance, October 31, 2016

$ 2,138

ADD:

ADD:

Deposit in transit

EFT collection on rent

LESS:

Correction of book error

NSF checks

LESS:

Printed checks

Outstanding checks

Service charge

October 31, 2016

$ 2,200

October 31, 2016

$ 2,200

7-19

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Oct. 31

Cash

410

Rent Revenue

410

To record EFT rent collection.

Salaries Expense

243

Cash

243

Accounts Receivable

Cash

Bank Expense

Bank Expense

To record bank service charges incurred.

7-20

Problems (Group A)

P7-21A Identifying internal control weakness in cash receipts

Learning Objective 2

Seacrest Productions makes all sales on credit. Cash receipts arrive by mail. Justin Broaddus, the

mailroom clerk, opens envelopes and separates the checks from the accompanying remittance advices.

Broaddus forwards the checks to another employee, who makes the daily bank deposit but has no access

to the accounting records. Broaddus sends the remittance advices, which show cash received, to the

accounting department for entry in the accounts. Broaddus’s only other duty is to grant sales allowances

to customers. (A sales allowance decreases the customer’s account receivable.) When Broaddus receives

a customer check for $225 less a $60 allowance, he records the sales allowance and forwards the

document to the accounting department.

Requirements

1. Identify the internal control weakness in this situation.

2. Who should record sales allowances?

3. What is the amount that should be shown in the ledger for cash receipts?

SOLUTION

Requirement 1

The job of receiving customers’ payments is performed by the same person who is responsible for