83

CASE 7

SUGGESTED ANSWERS TO DISCUSSION QUESTIONS

(1)

A company profit-sharing arrangement is a matter of auditor concern because it

(2)

This case describes the payroll system used by the Lakeside Company. Tests of

controls are designed by the auditor to verify that specific control features

identified as possible strengths are operating effectively. A sample of such tests

would include the following:

a. Compare the payroll records produced by Sarah Sweet to time tickets

completed by hourly employees noting agreement as to hours

worked;

84

(3)

Existence or Occurrence – For payroll expense, the auditor would want to

determine that all employees do, indeed, work for the company. If 48 employees

are paid each period, the auditor needs to ensure that 48 individuals are working

for Lakeside. The auditor should be concerned that one or more employees are

Completeness – Completeness is not usually a major problem in the area of

payroll expense, where misstatements most often result from having extra

expense recorded (because of theft) rather than from having transactions

Rights and Obligations – For payroll expense, the auditor would want to ascertain

that work did occur during the period for which the company does have a legal

Valuation or Allocation – Since an expense rather than an asset is involved, the

auditor is more interested in allocation than valuation. Verification should be

85

made that the proper expense is being allocated to the current year. Hence, the

auditor should recompute the cutoff made of the payroll calculation at both the

beginning and ending of the fiscal year. Determination needs to be made that

the figure being reported is for 2009 only.

Presentation and Disclosure – The auditor wants to make certain that the

(4)

Types of evidence-gathering procedures that are used by an auditor during an

examination would include the following. (One method for approaching this

question is to ask the students to identify the accounts that could be tested

through each procedure.)

a) Observation of activities and conditions – usually a test of controls to

provide evidence of operating efficiency.

b) Physical examination and count – used to prove that an item physically

exists and agrees with the ledger balance.

f) Retracing transactions from origination to final reporting – ensures that

accounting system is functioning properly so that balances will be correctly

reported.

g) Scanning accounting records – an analytical procedure designed to highlight

significant or unusual differences.

86

h) Inquiry (including discussion, questioning, etc.) – helps auditors to learn

design of accounting systems and internal control and to evaluate efficiency

of operations.

This question also asks about the competence (significance and reliability) of these

procedures. Each test is potentially quite important and produces reliable evidence,

but only if used in the appropriate circumstances. For example, confirmation is one of

the most important steps in auditing cash bank balances but is rarely used in

connection with an account such as land. Physical examination is essential in

auditing marketable securities where ownership and value can often be ascertained

visually. This same procedure is much less of a factor in examining equipment. An

audit procedure must match an account and the type of evidence needed.

(5)

Maintaining a separate payroll bank account is a common control procedure

encountered by auditors. Having a separate payroll account:

Allows for easier application of control procedures, such as limit tests, item

counts, and validity checks;

87

(6)

Some of the more critical potential problems involving payroll include:

A. Checks are issued to fictitious employees or to former employees who have

left Lakeside, with the checks being diverted and fraudulently cashed.

Substantive tests that may disclose this problem:

Observe distribution of payroll checks.

Review personnel files for a sample of employees to verify current

status is maintained.

B. Payroll deductions are recorded or computed incorrectly, through error or

as part of a defalcation scheme.

Substantive tests that may disclose this problem:

Review W-4 forms, voluntary deduction forms, and employee

contracts for completeness.

Compare payroll register to W-4 forms recomputing appropriate

deductions.

Mathematically verify payroll deductions (foot and cross-foot) and

88

C. Year-end accrual may be ignored or incorrectly computed.

Substantive tests that may disclose this problem:

Review last payroll for the year to verify that recording was made in

SUGGESTED ANSWERS TO EXERCISES

(1)

This problem extends the students’ introduction to working paper construction by

placing them in the role of supervisor. A number of errors exist in the example

presented in Exhibit 7-1, and the students should be able to identify most of

them.

The working paper is not properly dated so that a reviewing auditor cannot

be certain that this testing applies to 2012.

The columns are not labeled. No method exists for identifying the

information that has been gathered.

89

Comment A is vague and does not indicate any reason for the exception

(2)

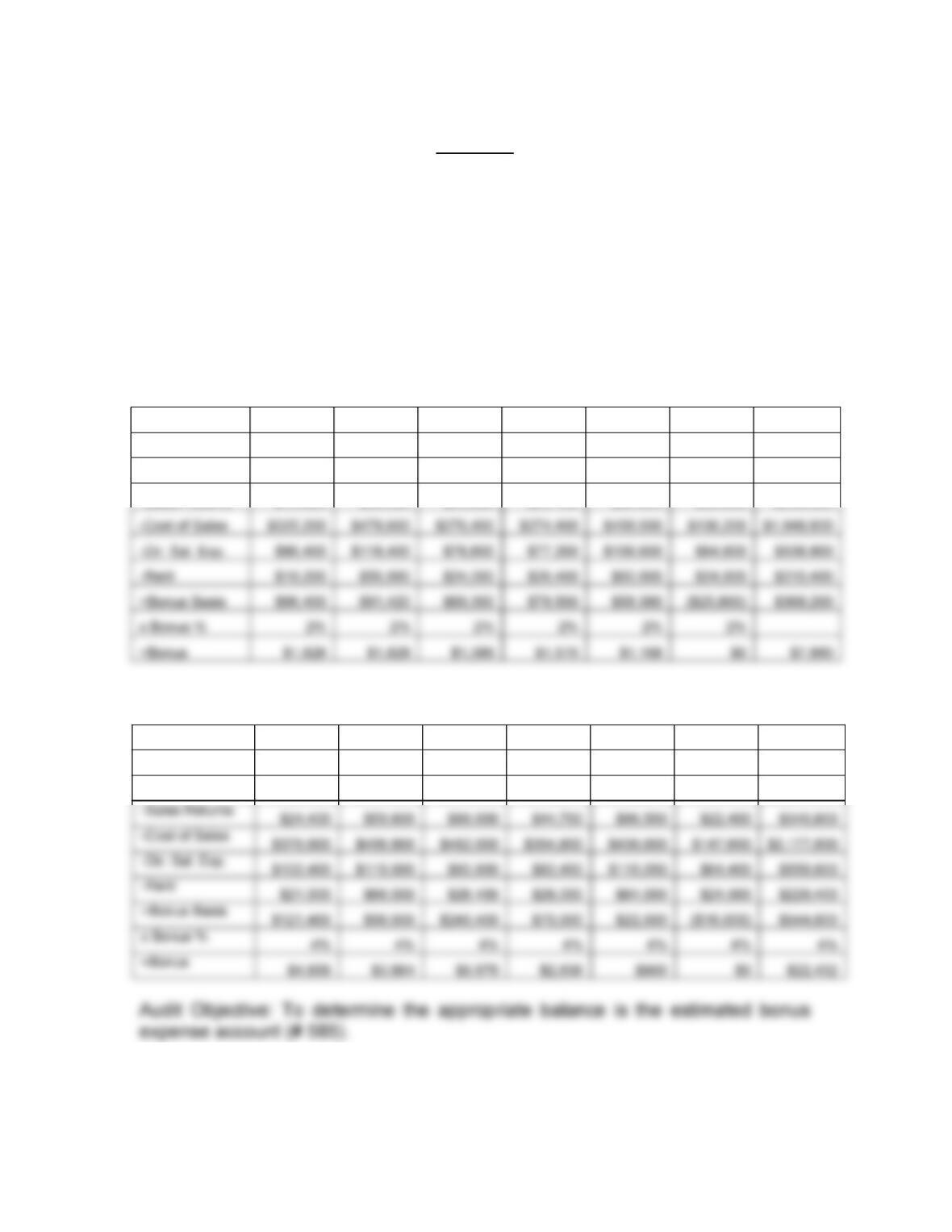

a. A completed Exhibit 7 worksheet is shown on the following page.

90

Exhibit 7

Lakeside Company

Account 585, Estimated Bonus Expense, for Nine Months ended

September 30, 2011 and 2012

Doc. No.

Prepared by

Reviewed by

2011 Bonus Plan

STORE STORE STORE STORE STORE STORE TOTAL

No.1 No.2 No.3 No.4 No.5 No.6 STORES

Sales $547,000

$795,600

$472,200

$484,600

$746,000

$221,600

$3,267,000

-Sales Returns $15,800

$50,380

$23,900

$28,100

$60,020

$22,600

$200,800

2012 Bonus Plan

STORE STORE STORE STORE STORE STORE TOTAL

No.1 No.2 No.3 No.4 No.5 No.6 STORES

Sales

$639,800

$

797,800

$917,600

$530,800

$729,200

$242,400

$3,857,600

$24,400

$59,800

$99,000

$44,700

$96,500

$22,400

$346,800

$102,400

$118,600

$80,800

$82,400

$110,200

$64,400

$558,800

$21,000

$66,000

$26,400

$28,000

$64,000

$24,000

$229,400

56

$3,864

$9,976

$2,836

$900

$0

$22,432

Scope: The bonus calculations for all six stores.

91

Audit Procedures:

Agreed all sales, cost of sales, and salary expense amounts to the

Comments: Client makes an “imputed rent” charge to Store No. 6 for the purpose

Audit Conclusion:

The 2011 bonus expense account is overstated (actual balance = $12,000 v.

SUGGESTED ANSWERS TO SARBANES-OXLEY QUESTIONS

During the audit of the internal control system (Sect 404), the CPAs can conclude

that the management report on their evaluation and audit of the system is fairly

stated and that the system works as it was designed and the design is effective.

Management will state its responsibility for maintaining

adequate internal control over financial reporting and give its assessment of

92

whether or not internal control over financial reporting is effective. According to

the rules, management cannot state that internal control over financial reporting

is effective if even one material weakness exists at year-end.

The independent auditor will evaluate and report on the

Documenting a significant deficiency could appear as in this example:

A material weakness is a control deficiency, or combination of control

deficiencies, that results in more than a remote likelihood that a material

misstatement of the annual or interim financial statements will not be prevented

or detected. The following material weakness has been identified and included in

no effective human resource