7-21

P7-22A Correcting internal control weakness

Learning Objectives 1, 2, 3

Each of the following situations has an internal control weakness.

a. Upside-Down Applications develops custom programs to customer’s specifications. Recently,

development of a new program stopped while the programmers redesigned Upside-Down’s

accounting system. Upside-Down’s accountants could have performed this task.

sales. To reduce expenses, one store manager ceases purchasing fidelity bonds on the cashiers.

f. Cornelius’s Corndogs keeps all cash receipts in an empty box for a week because the owner likes to

go to the bank on Tuesdays when Joann is working.

Requirements

1. Identify the missing internal control characteristics in each situation.

2. Identify the possible problem caused by each control weakness.

3. Propose a solution to each internal control problem.

SOLUTION

Requirement 1

Requirement 2

Requirement 3

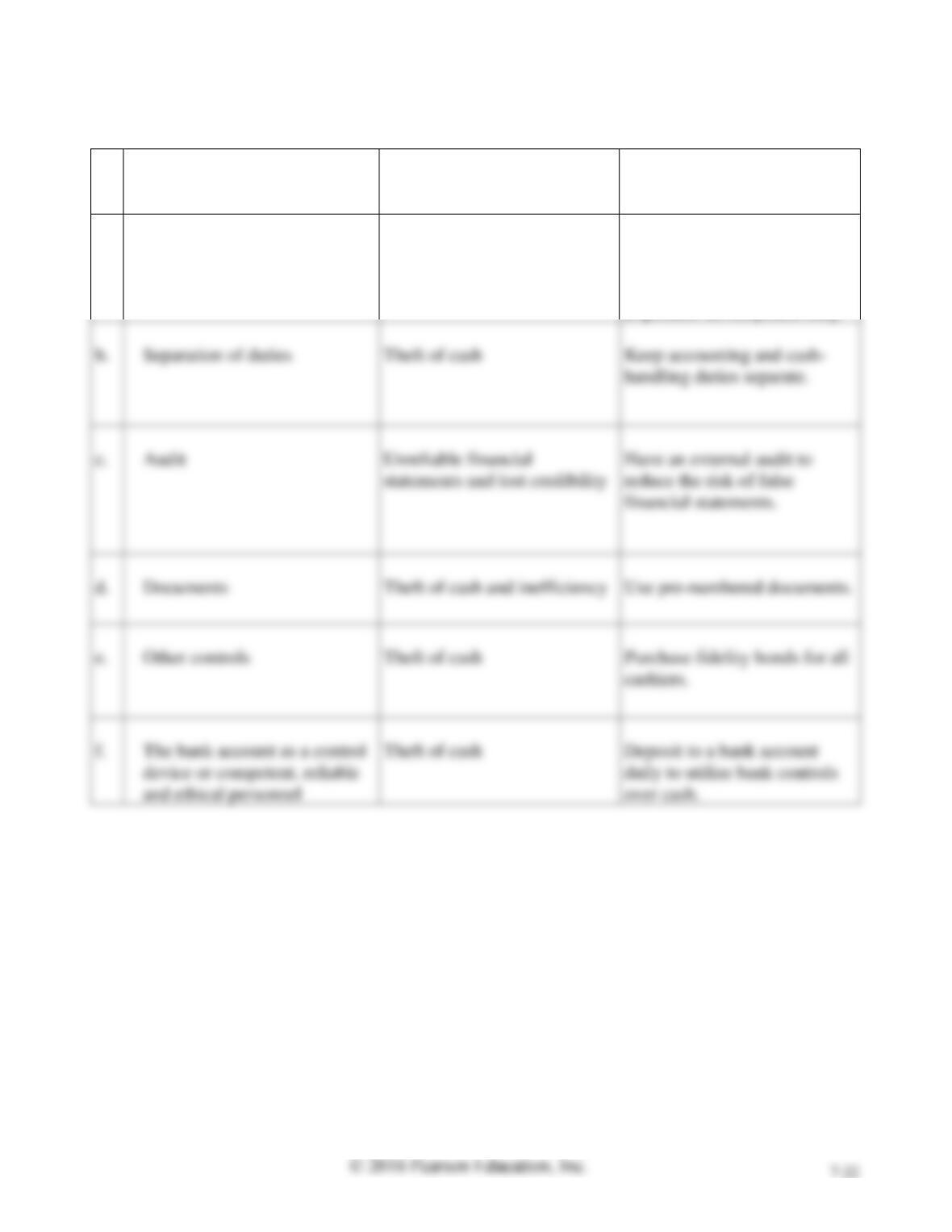

Missing Internal

Control Characteristic

Possible Problem

Solution

a.

Assignment of responsibilities

Lost sales due to delay of

product development

Assign company accountants

to redesign the accounting

system. Assign programmers

to product development only.

The bank account as a control

device or competent, reliable

and ethical personnel

Theft of cash

Deposit to a bank account

daily to utilize bank controls

over cash.

7-23

P7-23A Accounting for petty cash transactions

Learning Objective 4

3. June 30, Cash CR $230

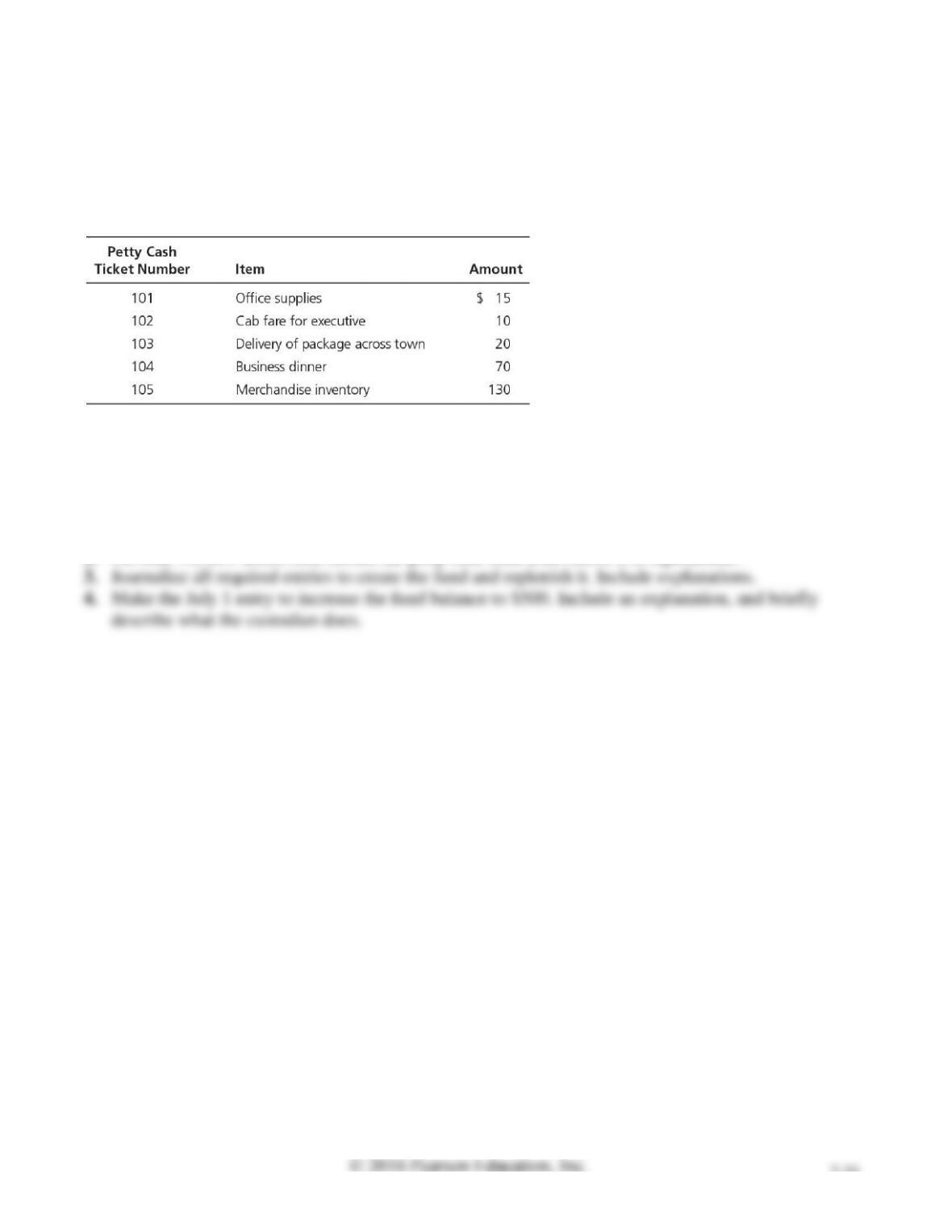

On June 1, Meadow Salad Dressings creates a petty cash fund with an imprest balance of $400. During

June, Al Franklin, the fund custodian, signs the following petty cash tickets:

On June 30, prior to replenishment, the fund contains these tickets plus cash of $170. The accounts

affected by petty cash payments are Office Supplies, Travel Expense, Delivery Expense, Entertainment

Expense, and Merchandise Inventory.

Requirements

1. Explain the characteristics and the internal control features of an imprest fund.

2. On June 30, how much cash should the petty cash fund hold before it is replenished?

7-24

SOLUTION

Requirement 1

Maintaining the Petty Cash account at its designated balance is the nature of an imprest system. The

P7-24A Accounting for petty cash transactions

Learning Objective 4

2. June 30, Cash CR $158

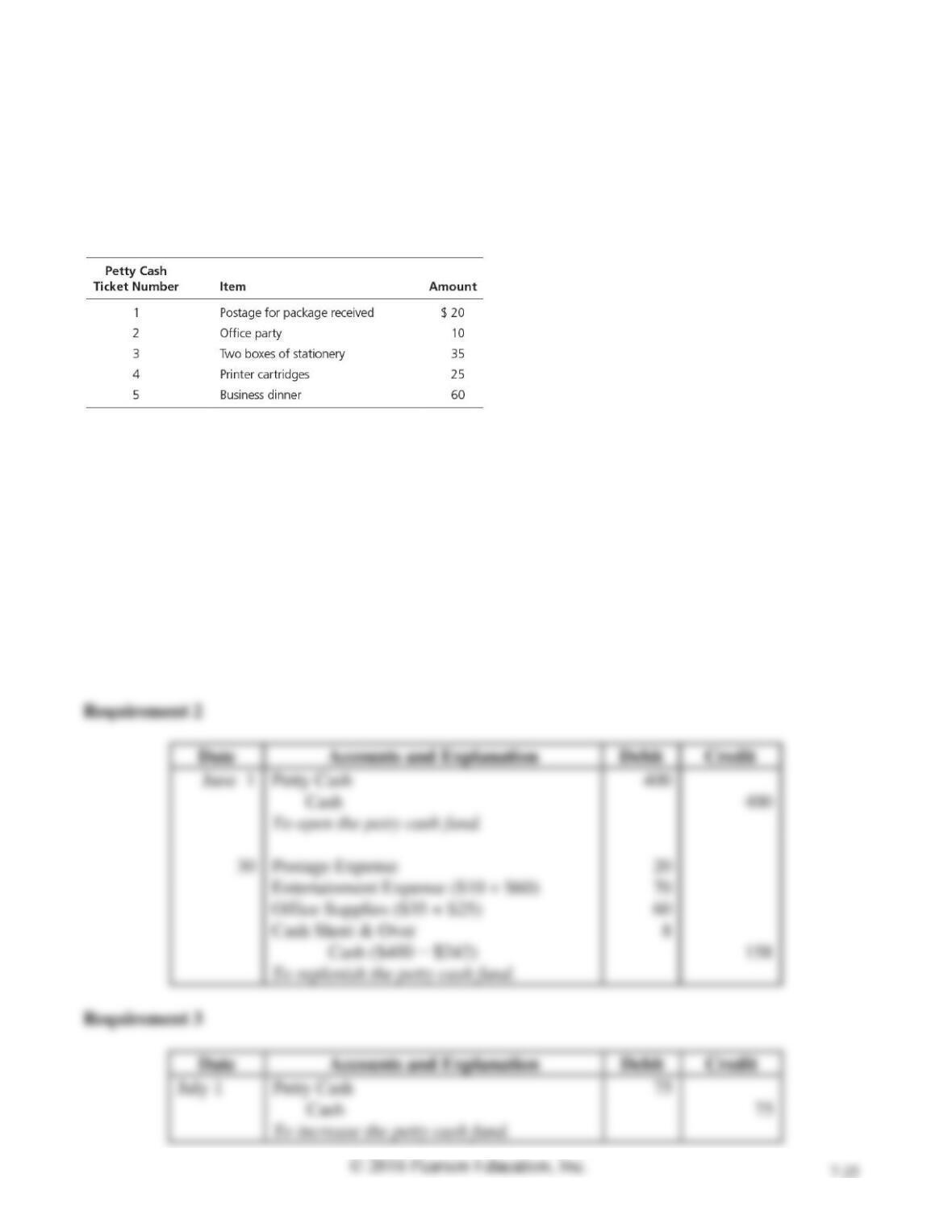

Suppose that on June 1, Jammin’ Gyrations, a disc jockey service, creates a petty cash fund with an

imprest balance of $400. During June, Michael Martell, fund custodian, signs the following petty cash

tickets:

On June 30, prior to replenishment, the fund contains these tickets plus cash of $242. The accounts

affected by petty cash payments are Office Supplies, Entertainment Expense, and Postage Expense.

Requirements

1. On June 30, how much cash should this petty cash fund hold before it is replenished?

2. Journalize all required entries to (a) create the fund and (b) replenish it. Include explanations.

3. Make the entry on July 1 to increase the fund balance to $475. Include an explanation.

SOLUTION

Requirement 1

Before replenishment, the petty cash fund should hold cash of $250. ($400 – total payments of $150).

P7-25A Preparing a bank reconciliation and journal entries

Learning Objective 5

1. Adjusted Balance $17,010

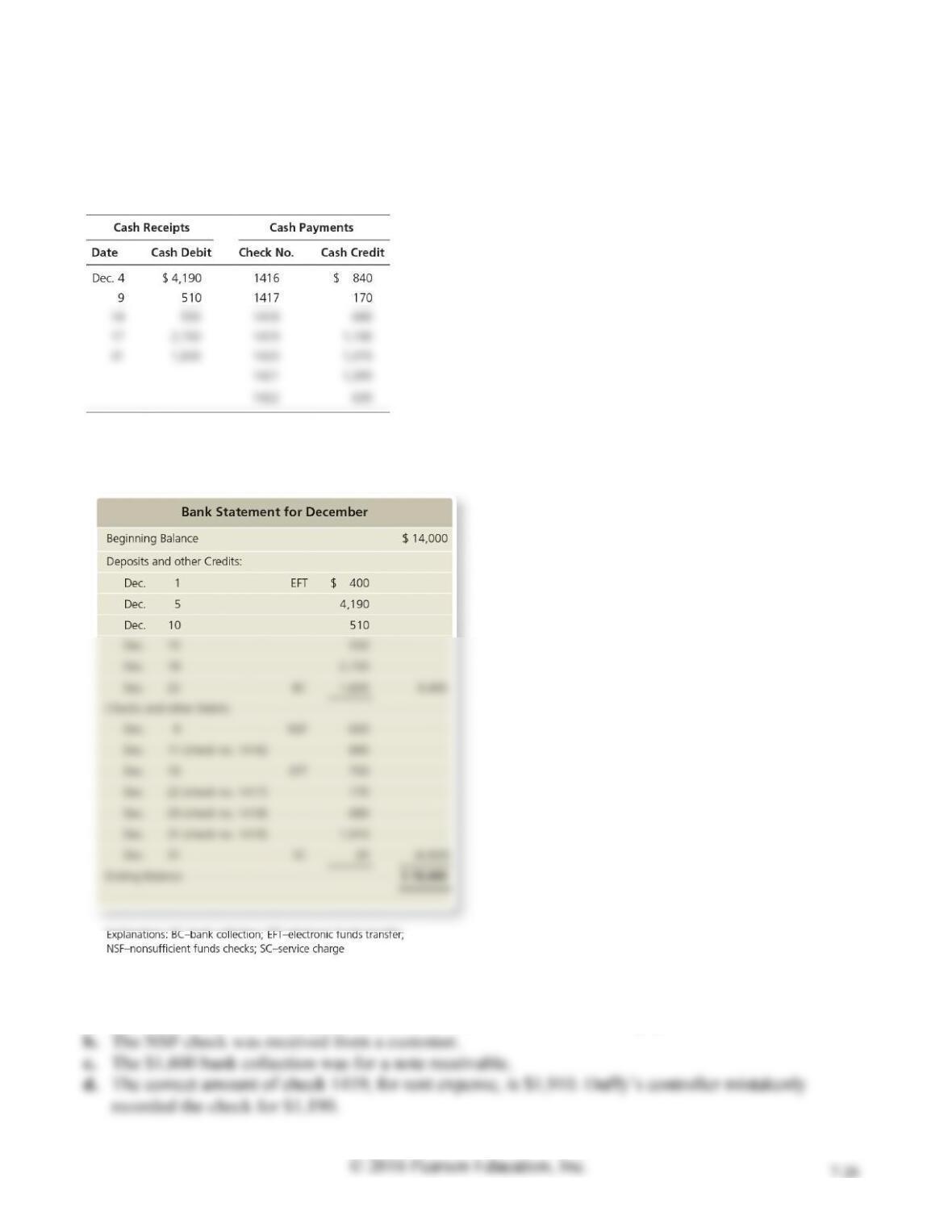

The December cash records of Duffy Insurance follow:

Duffy’s Cash account shows a balance of $17,050 at December 31. On December 31, Duffy Insurance

received the following bank statement:

Additional data for the bank reconciliation follow:

a. The EFT credit was a receipt of rent. The EFT debit was an insurance payment.

7-27

Requirements

1. Prepare the bank reconciliation of Duffy Insurance at December 31, 2016.

2. Journalize any required entries from the bank reconciliation.

SOLUTION

Requirement 1

DUFFY INSURANCE

Bank Reconciliation

December 31, 2016

BANK

BOOK

Balance, December 31, 2016

$ 18,480

Balance, December 31, 2016

$ 17,050

Bank collection of note

LESS:

LESS:

Outstanding checks

Correction of book error

No. 1420

NSF check

No. 1421

EFT – insurance payment

No. 1422

Service charge

December 31, 2016

$ 17,010

December 31, 2016

$ 17,010

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Dec. 31

Cash

400

Rent Revenue

400

To record EFT rent collection.

31

Cash

Notes Receivable

To record bank collection of notes receivable.

31

Rent Expense

720

Cash

720

To record error on check 1419.

31

Accounts Receivable

600

Cash

600

To record NSF check.

31

Insurance Expense

700

700

To record EFT insurance payment.

31

Bank Expense

To record bank service charges incurred.

7-29

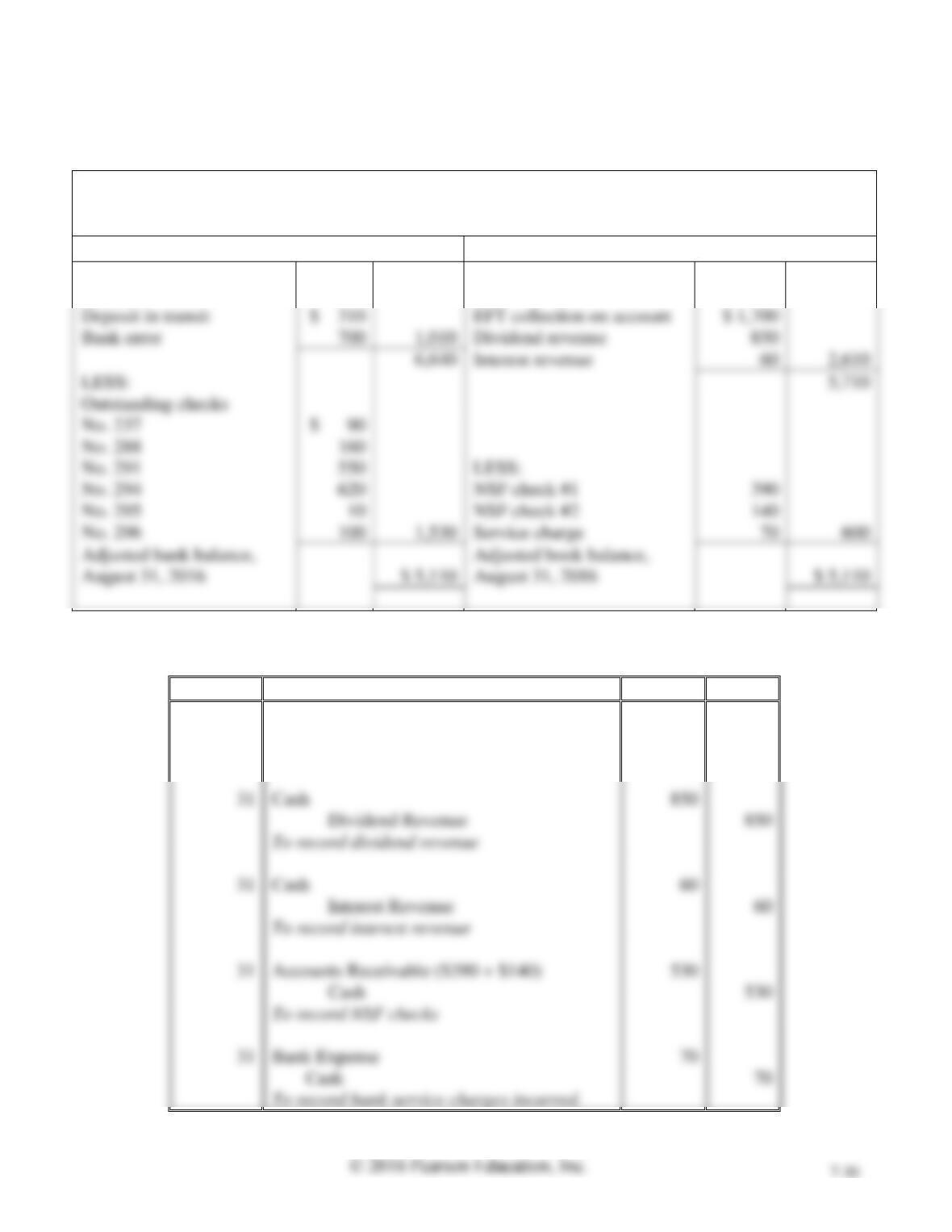

P7-26A Preparing a bank reconciliation and journal entries

Learning Objective 5

1. Book Additions $2,610

The August 31 bank statement of Watson Healthcare has just arrived from United Bank. To prepare the

bank reconciliation, you gather the following data:

a. The August 31 bank balance is $5,630.

b. The bank statement includes two charges for NSF checks from customers. One is for $390 (#1), and

the other is for $140 (#2).

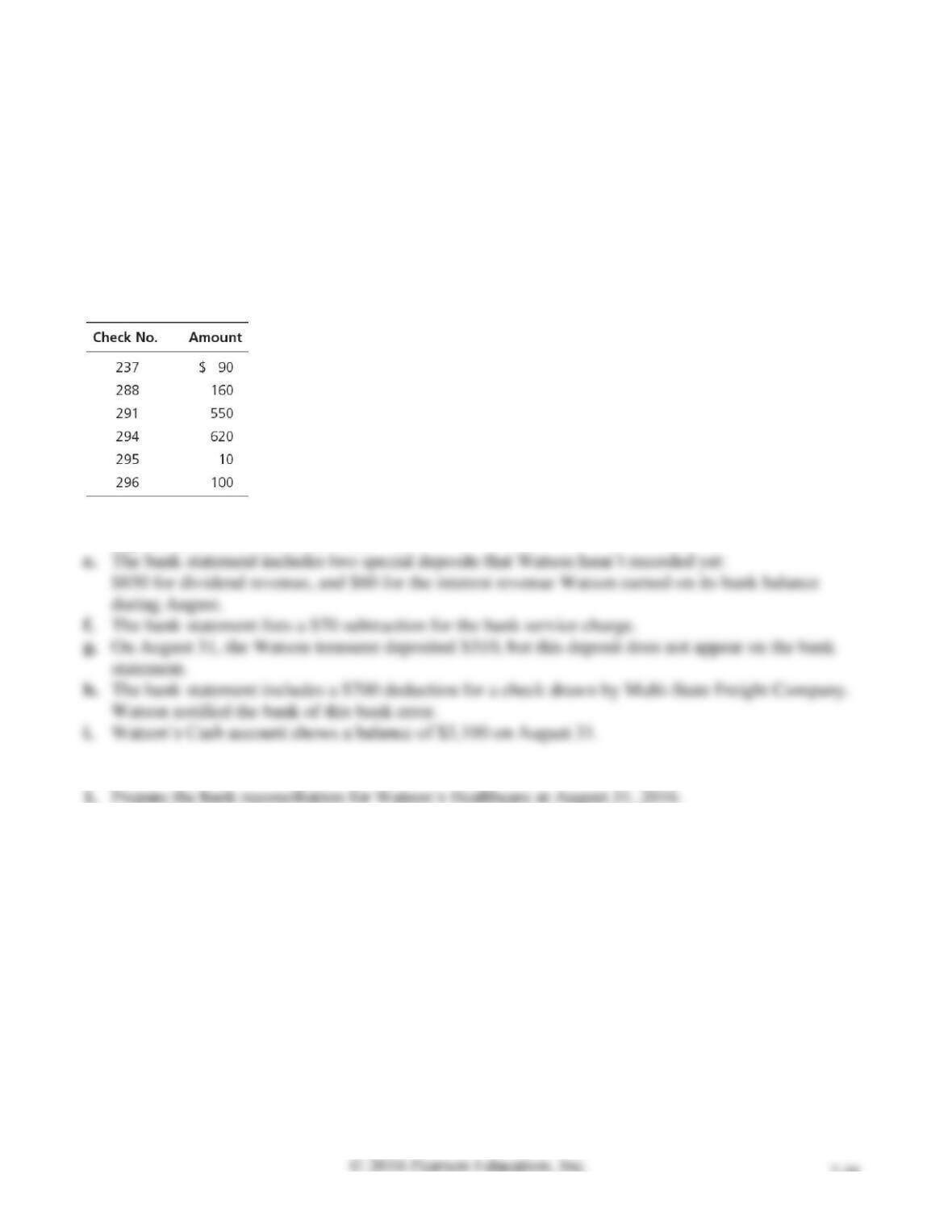

c. The following Watson checks are outstanding at August 31:

d. Watson collects from a few customers by EFT. The August bank statement lists a $1,700 EFT

deposit for a collection on account.

Requirements

2. Journalize any required entries from the bank reconciliation. Include an explanation for each entry.

SOLUTION

Requirement 1

WATSON HEALTHCARE

Bank Reconciliation

August 31, 2016

BANK

BOOK

Balance, August 31, 2016

$ 5,630

Balance, August 31, 2016

$ 3,100

ADD:

ADD:

Deposit in transit

EFT collection on account

$ 1,700

Bank error

Dividend revenue

Interest revenue

60

Outstanding checks

No. 237

No. 288

No. 291

LESS:

No. 294

NSF check #1

No. 295

NSF check #2

No. 296

Service charge

70

August 31, 2016

$ 5,110

August 31, 2016

$ 5,110

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Aug. 31

Cash

1,700

Accounts Receivable

1,700

To record EFT collection on account

31

Cash

Dividend Revenue

To record dividend revenue

31

Cash

Interest Revenue

To record interest revenue

31

Accounts Receivable ($390 + $140)

Cash

To record NSF checks

31

Bank Expense

Problems (Group B)

P7-27B Identifying internal control weakness in cash receipts

Learning Objective 2

Black Water Productions makes all sales on credit. Cash receipts arrive by mail. Larry Padgitt, the

mailroom clerk, opens envelopes and separates the checks from the accompanying remittance advices.

Padgitt forwards the checks to another employee, who makes the daily bank deposit but has no access to

the accounting records. Padgitt sends the remittance advices, which show cash received, to the

accounting department for entry in the accounts. Padgitt’s only other duty is to grant sales allowances to

customers. (A sales allowance decreases the customer’s account receivable.) When Padgitt receives a

customer check for $575 less a $45 allowance, he records the sales allowance and forwards the

document to the accounting department.

Requirements

1. Identify the internal control weakness in this situation.

2. Who should record sales allowances?

3. What is the amount that should be shown in the ledger for cash receipts?

SOLUTION

Requirement 1

The job of receiving customers’ payments is performed by the same person who is responsible for

7-32

P7-28B Correcting internal control weakness

Learning Objectives 1, 2, 3

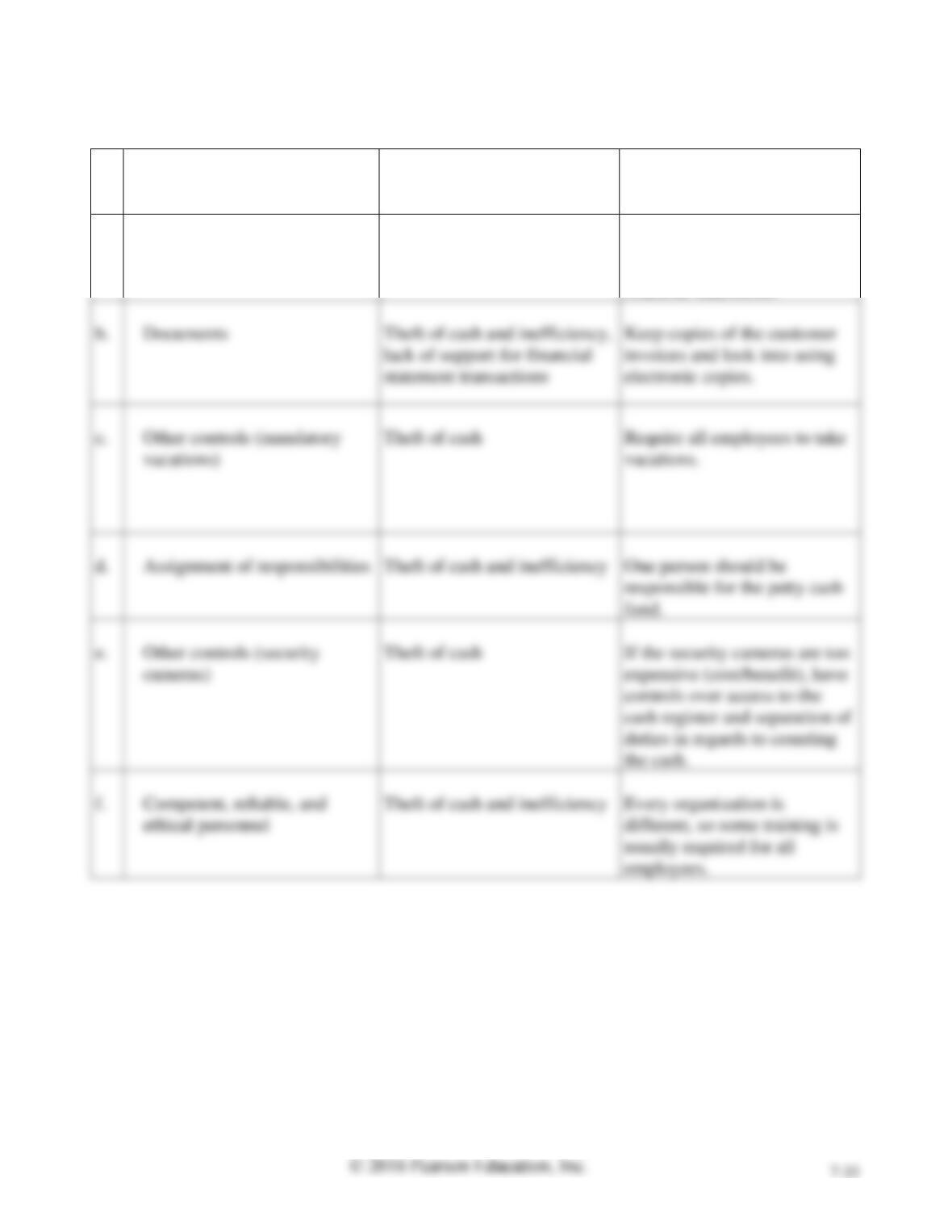

Each of the following situations has an internal control weakness.

a. Jade Applications has decided that one way to cut costs in the upcoming year is to fire the external

auditor. The business believes that the internal auditor should be able to efficiently monitor the

company’s internal controls.

Requirements

1. Identify the missing internal control characteristics in each situation.

2. Identify the possible problem caused by each control weakness.

3. Propose a solution to each internal control problem.

SOLUTION

Requirement 1

Requirement 2

Requirement 3

Missing Internal

Control Characteristic

Possible Problem

Solution

a.

Audit

Unreliable financial

statements and lost credibility

Have an external audit to

reduce the risk of false

financial statements.

d.

Assignment of responsibilities

Theft of cash and inefficiency

One person should be

responsible for the petty cash

fund.

cash register and separation of

duties in regards to counting

the cash.

ethical personnel

different, so some training is

usually required for all

employees.

7-34

P7-29B Accounting for petty cash transactions

Learning Objective 4

3. Cash Short & Over CR $10

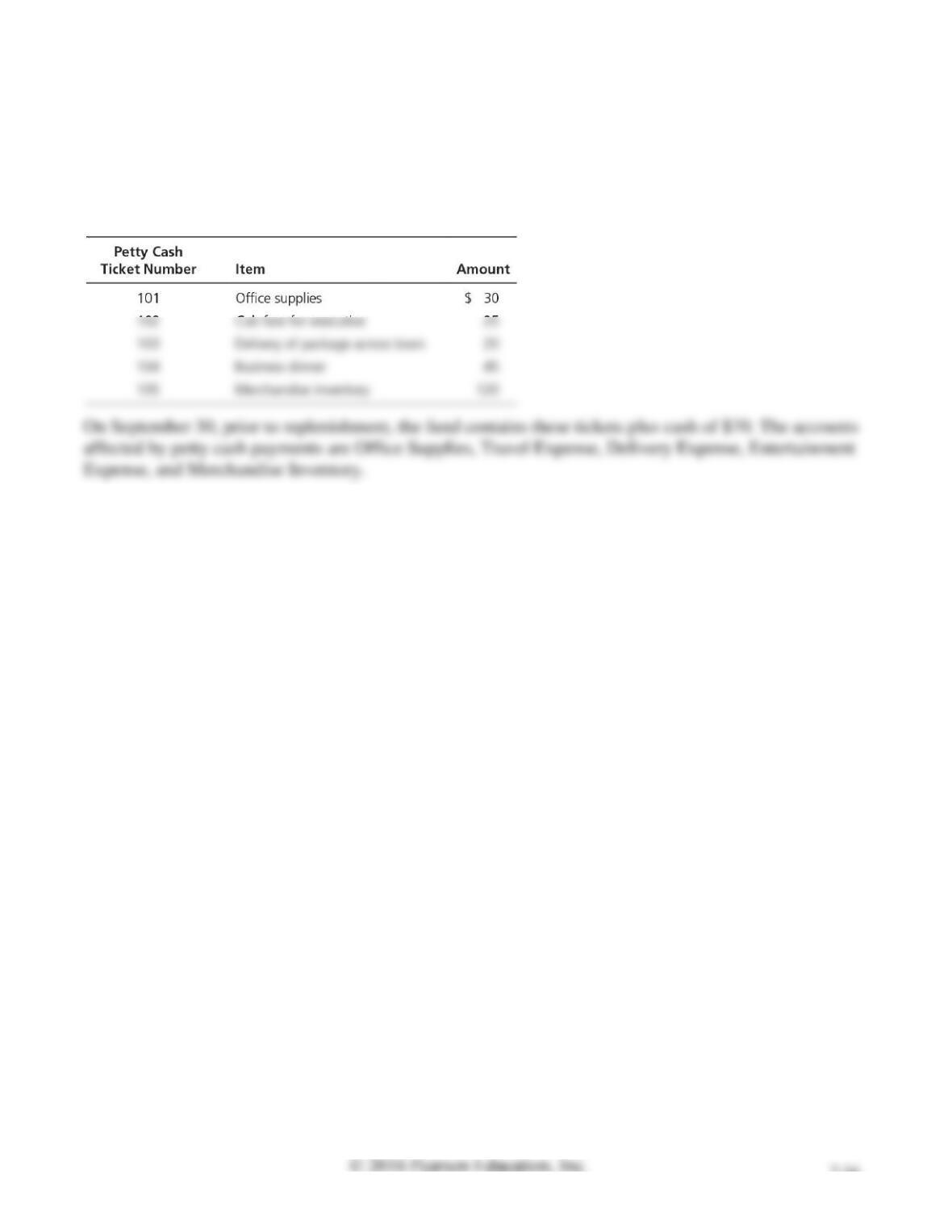

On September 1, Top Taste Salad Dressings creates a petty cash fund with an imprest balance of $300.

During September, Michael Martell, the fund custodian, signs the following petty cash tickets:

Requirements

1. Explain the characteristics and the internal control features of an imprest fund.

2. On September 30, how much cash should the petty cash fund hold before it is replenished?

3. Journalize all required entries to create the fund and replenish it. Include explanations.

4. Make the October 1 entry to increase the fund balance to $350. Include an explanation, and briefly

describe what the custodian does.

7-35

SOLUTION

Requirement 1

Maintaining the Petty Cash account at its designated balance is the nature of an imprest system. The

Date

Accounts and Explanation

Debit

Credit

Petty Cash

Cash

Office Supplies

30

Travel Expense

25

Delivery Expense

20

Entertainment Expense

45

Merchandise Inventory

10

Requirement 4

Date

Accounts and Explanation

Debit

Credit

Oct. 1

Petty Cash

50

Cash

50

P7-30B Accounting for petty cash transactions

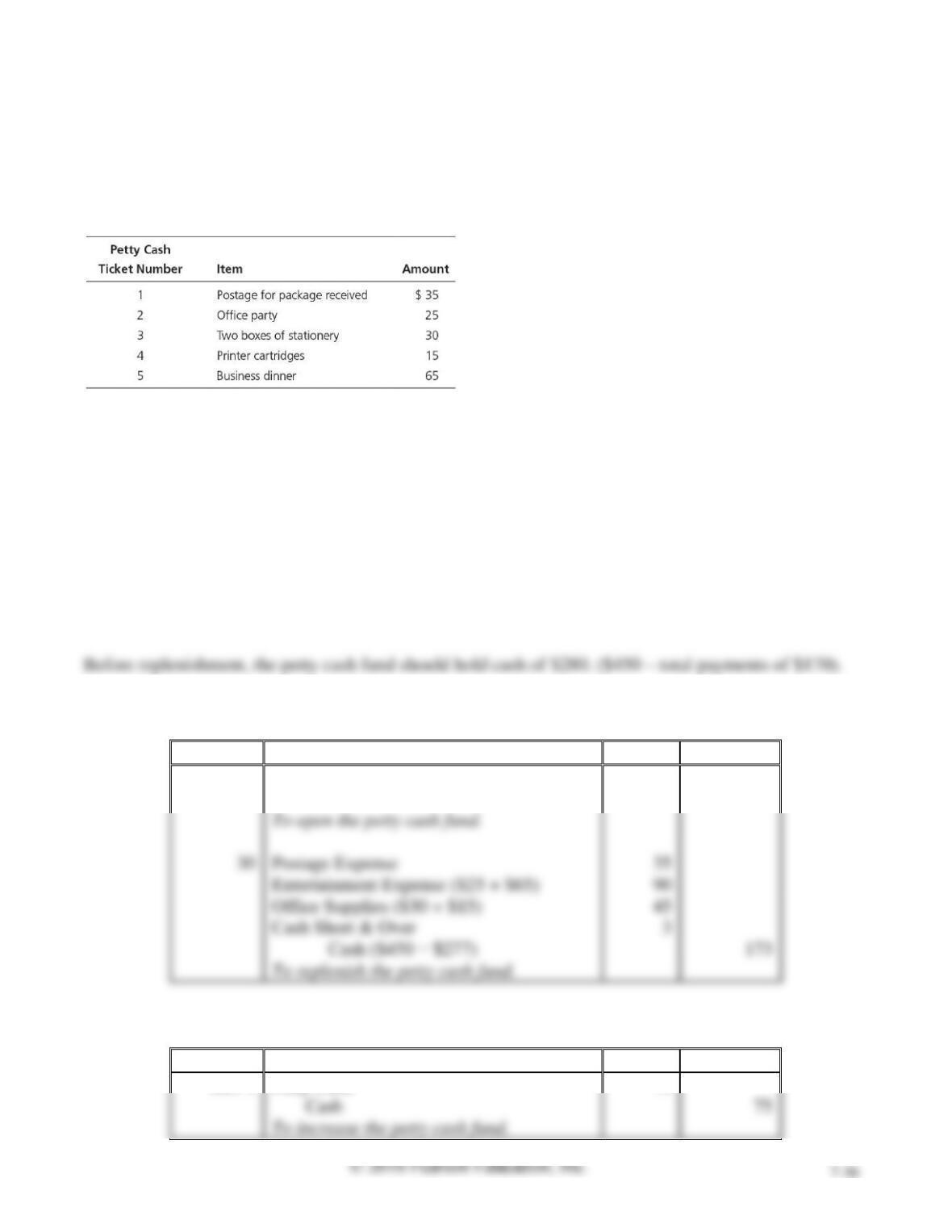

Learning Objective 4

2. Sep. 30, Cash CR $173

Suppose that on September 1, Rockin’ Gyrations, a disc jockey service, creates a petty cash fund with an

imprest balance of $450. During September, Ruth Mangan, fund custodian, signs the following petty

cash tickets:

On September 30, prior to replenishment, the fund contains these tickets plus cash of $277. The

accounts affected by petty cash payments are Office Supplies, Entertainment Expense, and Postage

Expense.

Requirements

1. On September 30, how much cash should this petty cash fund hold before it is replenished?

2. Journalize all required entries to (a) create the fund and (b) replenish it. Include explanations.

3. Make the entry on October 1 to increase the fund balance to $525. Include an explanation.

SOLUTION

Requirement 1

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Sep. 1

Petty Cash

450

Cash

450

Postage Expense

Entertainment Expense ($25 + $65)

Office Supplies ($30 + $15)

Cash Short & Over

173

Requirement 3

Date

Accounts and Explanation

Debit

Credit

Oct. 1

Petty Cash

75