Accounting Information Systems, 10e 1

SOLUTIONS FOR CHAPTER 7

Each end-of-chapter question in the Solutions Manual is tagged to correspond with AACSB, AICPA

and CISA standards, allowing professors to more easily manage the task of reporting outcomes to these

professional and accrediting bodies. Please see the corresponding spreadsheet file for the tagging

information.

Discussion Questions

DQ 7-1 Recently, the U.S. federal government and the American Institute of Certified

Public Accountants (AICPA) have taken aggressive steps aimed at ensuring the

quality of organizational governance. What are these changes, how might they

change organizational governance procedures, and do you believe that these

actions will really improve internal control of business organizations?

ANS. First, the U.S. Congress passed the Sarbanes-Oxley Act of 2002 (SOX). This

groundbreaking legislation is intended to set the foundation for improved

organizational governance. Most notably, SOX disallows auditors of public

DQ 7-2 “Enterprise Risk Management is a process for organizational governance.”

Discuss why this might be correct and why it might not.

ANS. Let’s look at the elements of the definitions of these two concepts side-by-side:

2 Solutions for Chapter 7

DQ 7-3 “If it weren’t for the potential of computer crime, the emphasis on controlling

computer systems would decline significantly in importance.” Do you agree?

Discuss fully.

ANS. Without computer crime, and the attendant, fascinating stories, public awareness

of the importance of controlling computer systems might decline. However, while

DQ 7-4 Provide five examples of potential conflict between the control goals of ensuring

effectiveness of operations and of ensuring efficient employment of resources.

ANS. 1. By striving to answer many customer telephone calls, a customer service

Accounting Information Systems, 10e 3

DQ 7-5 Discuss how the efficiency and effectiveness of a mass-transit system in a large

city can be measured.

ANS. The main purpose of this question is to reinforce the ideas that (1) effectiveness

must be judged in light of objectives and (2) efficiency is the relationship of

inputs to outputs.

DQ 7-6 “If input data are entered into the system completely and accurately, then the

information system control goals of ensuring update completeness and of ensuring

update accuracy will be automatically achieved.” Do you agree? Discuss fully.

ANS. No, we do not agree. The text distinguishes input and update because these steps

DQ 7-7 “Section 404 of SOX has not been a good idea. It has been too costly and it has

not had its intended effect.” Do you agree? Discuss fully.

4 Solutions for Chapter 7

ANS. As reported in the chapter, reviews of the results of SOX Section 404 are mixed.

Certainly, its implementations have been quite costly. Also, some foreign firms

Section 404.

DQ 7-8 How does this text’s definition of internal control differ from COSO? How does it

differ from the controls that are subject to review under Section 404 of SOX?

ANS. The text’s definition of internal control is aimed at all reporting, not just financial

reporting. Both COSO and SOX 404 are interested only in controls over the

information systems and output reporting that are related to financial reporting.

DQ 7-9 What, if anything, is wrong with the following control hierarchy? Discuss fully.

Highest level of control Pervasive control plans

The control environment

Application controls

Business process control plans

Lowest level of control IT general controls

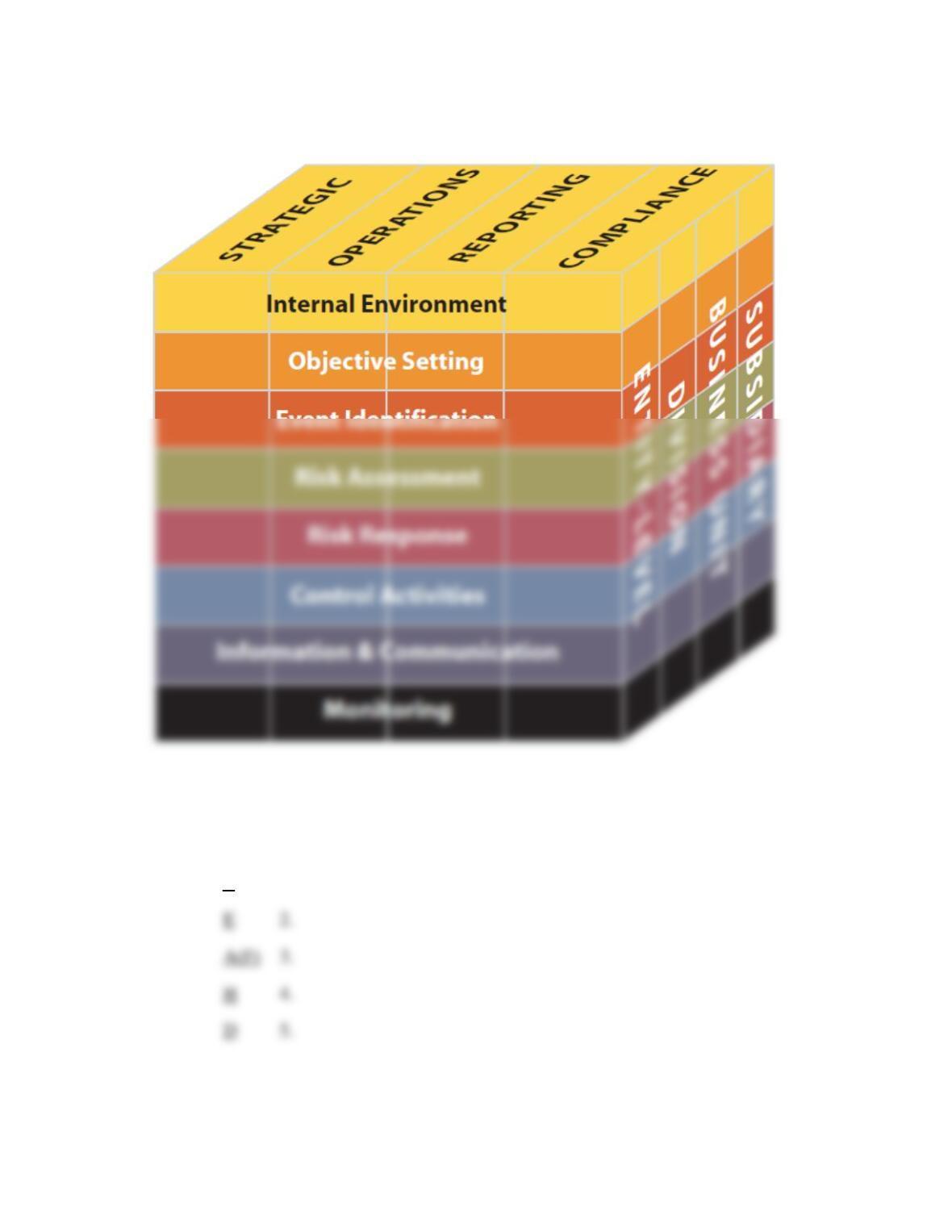

ANS. The correct order from highest to lowest level of control is (see also Figure 7.6)

the following:

Accounting Information Systems, 10e 5

Short Problems

SP 7-1 ANS. The answer should note the differences in the following two internal control

6 Solutions for Chapter 7

Accounting Information Systems, 10e 7

SP 7-2 ANS.

B 1.

8 Solutions for Chapter 7

SP 7-3 ANS.

H(B) 1.

SP 7-4 ANS. Answers will vary among students.

Problems

P 7-1 ANS.

E 1.

H 2.

Accounting Information Systems, 10e 9

P 7-2 ANS. The major implication is that management can be held legally accountable for the

organization’s control system. Under the Foreign Corrupt Practices Act (FCPA),

for example, an officer of an organization must ensure that the organization

maintains adequate accounting records. Recently, Section 404 of the Sarbanes–

Oxley Act of 2002 has reinforced this management responsibility by requiring

nonconflict of interest affidavits, control policies, and reward systems that

support, rather than undermine, the control policies.

• Being actively and continuously involved in the design, operation, review, and

modification of the organization’s systems and related control systems. This

may involve participation in—or at least approval of—the systems

10 Solutions for Chapter 7

P 7-3 ANS.

Situation

Control Goal

Explanation

1.

E and A

Checking to make sure that shipping notices are received for all

sales orders issued addresses the goal of ensuring that event data

2.

F and D

Double checking unit prices helps to ensure that the prices

actually billed are accurate.

Answer D is appropriate if we explain that checking prices

against an authorized price list helps to ensure that the event

was an authorized one (input validity).

the update run, must equal $3,900. If not, something went wrong

during the run. Some payments were not posted (UC), or some

were posted incorrectly (UA).

5.

E

A vendor is unlikely to send two different invoices with the

same number. Thus, the second instance of invoice #12345 is

probably a duplicate of the first. The second invoice should be

rejected to ensure that the invoice is processed once and only

once (input completeness).

Under the definitions given in the chapter, data elements missing

from an input document are instances of lack of input accuracy

as opposed to input completeness, which relates to recording all

events that occurred.

timeliness in cash receipts processing, an operations process by

Answer B is appropriate if we explain that it is more efficient to

manually.

P 7-4 ANS. Description Answer

Answer A is appropriate here if we assume– that timely

Accounting Information Systems, 10e 11

1. J

2. C

P 7-5 ANS.

Part A: Current Scenario:

Dollar loss (sales) per hour of downtime

$10,000

Internal downtime incidents per year

50

External downtime incidents per year

50

Total downtime incidents per year

100

Expected Gross Risk

Preventative Measures

Annualized cost of ISP

Total annualized cost of preventive measures

Residual Expected Risk

Part B: Additional Redundant Technology

Dollar loss (sales) per hour of downtime

$10,000

Internal downtime incidents per year

15

External downtime incidents per year

50

Total downtime incidents per year

65

Preventive Measures

Annualized cost of redundant technology

Annualized cost of ISP

Total annualized cost of preventive measures

Residual Expected Risk

Part C: Additional Redundant Technology and Additional ISP Support

12 Solutions for Chapter 7

the expected residual risk is (see Part C.2 below).

If the company moves to a higher support level of no more than 20 downtime incidents,

the residual expected risk is (see Part C.3 below).

900,000

If the company moves to a higher support level of no more than 10 downtime incidents,

the residual expected risk is (see Part C.4 below).

925,000

If the company moves to a higher support level of no more than 0 downtime incidents,

the residual expected risk is (see Part C.5 below).

950,000

$900,000.00. Thus, management would be prudent to pay for a guarantee of only 20 rather than 30 incidents

because the former would also result in less customer dissatisfaction if and when downtime incidents occur.

Part C.1: Additional Redundant Technology and Additional ISP Support for 40 Downtime Incidents

Dollar loss (sales) per hour of downtime

$10,000

Internal downtime incidents per year

15

External downtime incidents per year

40

Total downtime incidents per year

55

Expected Gross Risk

$550,000

Preventive Measures

Annualized cost of redundant technology

Annualized cost of ISP

Total annualized cost of preventive measures

Residual Expected Risk

tolerance.

If the company remains with the current ISP contract of no more than 50 downtime

incidents, the residual expected risk is (see Part B above).

If the company moves to a higher support level of no more than 40 downtime incidents,

the residual expected risk is (see Part C.1 below).

950,000

If the company moves to a higher support level of no more than 30 downtime incidents,

900,000

Accounting Information Systems, 10e 13

Part C.2: Additional Redundant Technology and Additional ISP Support for 30 Downtime Incidents

Dollar loss (sales) per hour of downtime

$10,000

Internal downtime incidents per year

15

External downtime incidents per year

30

Total downtime incidents per year

45

Part C.3: Additional Redundant Technology and Additional ISP Support for 20 Downtime Incidents

Dollar loss (sales) per hour of downtime

$10,000

Internal downtime incidents per year

15

External downtime incidents per year

20

Total downtime incidents per year

35

Expected Gross Risk

Preventive Measures

Annualized cost of redundant technology

Annualized cost of ISP

Total annualized cost of preventive measures

Residual Expected Risk

Part C.4: Additional Redundant Technology and Additional ISP Support for 10 Downtime Incidents

Dollar loss (sales) per hour of downtime

$10,000

Internal downtime incidents per year

15

External downtime incidents per year

10

Total downtime incidents per year

25

Preventive Measures

Annualized cost of redundant technology

Annualized cost of ISP

Total annualized cost of preventive measures

Residual Expected Risk

Expected Gross Risk

Preventive Measures

Annualized cost of redundant technology

Annualized cost of ISP

Total annualized cost of preventive measures

Residual Expected Risk

14 Solutions for Chapter 7

Part C.5: Additional Redundant Technology and Additional ISP Support for 0 Downtime Incidents

Dollar loss (sales) per hour of downtime

$10,000

Internal downtime incidents per year

15

P 7-6 ANS. We might compare the elements of these two control matrices as follows:

Figure 7.7 (the textbook)

Figure 7.8 (PwC)

Comment

Control goals of the Lenox cash receipts

business process.

Subprocess.

Both name the process.

Control goals of the operations process.

PwC matrix relates to controls over

financial reporting and operations are

beyond the scope of the PwC matrix.

Ensure efficient employment of

resources.

Operations are beyond the scope of

the PwC matrix.

Information processing

objective (restricted access).

to information resources. Figure

7.7’s objective also includes other

assets.

Control goals of the information

process.

Control objective.

goals.

objective (validity).

Input completeness/update

completeness.

Information processing

objective (completeness).

Same, but PwC does not address

updates.

Input accuracy/update accuracy.

control activity.

frequency of the control activity.

PwC states an overall objective for

each process. In Figure 7.7, this is a

heading for more specific control

External downtime incidents per year

Total downtime incidents per year

Expected Gross Risk

Preventive Measures

Annualized cost of redundant technology

Annualized cost of ISP

Total annualized cost of preventive measures

Residual Expected Risk

Accounting Information Systems, 10e 15

Figure 7.7 (the textbook)

Figure 7.8 (PwC)

Comment

NA

Financial statement area.

PwC matrix is for controls over

financial reporting and states the area

of interest.

The overall assessment is that the matrices are quite similar. In fact, the control

matrix for this textbook was adapted from earlier versions of a PwC matrix (one

that was developed by Coopers & Lybrand, one of the firms that became part of

PwC). The PwC matrix, focused as it is on the financial statement audit, has

financial statement audit. Testing of

NA

P or D.

Figure 7.7 does not specifically

A or M.

Figure 7.7 does not classify controls

as automated or manual.