CHAPTER 7 • RECEIVABLES AND INVESTMENTS 7-21

PROBLEM 7-2 (Concluded)

3. Partial balance sheet at December 31, 2016:

Current Assets

Accounts receivable …………………………………………………. $271,000

Allowance for doubtful accounts ………………………………… 29,600

Net accounts receivable ……………………………………………. $241,400

LO 2 PROBLEM 7-3 MAKING BUSINESS DECISIONS: ANALYZING THE COCA-COLA

COMPANY’S ACCOUNTS RECEIVABLE TURNOVER RATIO

Part A. Ratio Analysis Model

1. Formulate the Question:

How many times a year does The Coca-Cola Company turn over its accounts

receivable?

2. Gather the Information from the Financial Statements:

3. Calculate the Ratio:

Accounts Receivable Turnover Ratio = Net Credit Sales*

7-22 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 7-3 (Continued)

4. Compare the Ratio with Other Ratios:

Accounts Receivable Turnover Ratio

9.7 times 9.9 times 9.5 times 9.4 times

Calculations:

Coca-Cola:

5. Interpret the Ratios:

Coca-Cola turned over its accounts receivable 9.7 times during 2013. This means

that, on average, the company collects its receivables every 37 days (360 days/9.7).

Part B. Business Decision Model

1. Formulate the Question:

After considering all relevant information, should I loan money to The Coca-Cola

Company?

2. Gather Information from the Financial Statements and Other Sources:

The information will come from a variety of sources, not limited to but including:

a. The balance sheet provides information about liquidity.

CHAPTER 7 • RECEIVABLES AND INVESTMENTS 7-23

PROBLEM 7-3 (Concluded)

3. Analyze the Information Gathered:

The information gathered in (2) above must be analyzed. Among the relevant ques-

tions that must be answered are the following:

a. Refer to part (5) of the Ratio Analysis Model for a comparison of the turnover

ratios for Coca-Cola and its competitor, PepsiCo, over the last two years. Which

company turns over its receivables more often?

4. Make the Decision:

Taking into account all of the various sources of information, decide either to loan

money to The Coca-Cola Company or find an alternative use for the money.

5. Monitor Your Decision:

LO 4 PROBLEM 7-4 CREDIT CARD SALES

1. Gross margin $0.99

Cost of goods sold 2.00

Net selling price $2.99

2. If his normal charge is $3.05 to credit card customers, he can offer a $0.06 discount

to cash customers and still maintain his gross margin.

7-24 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

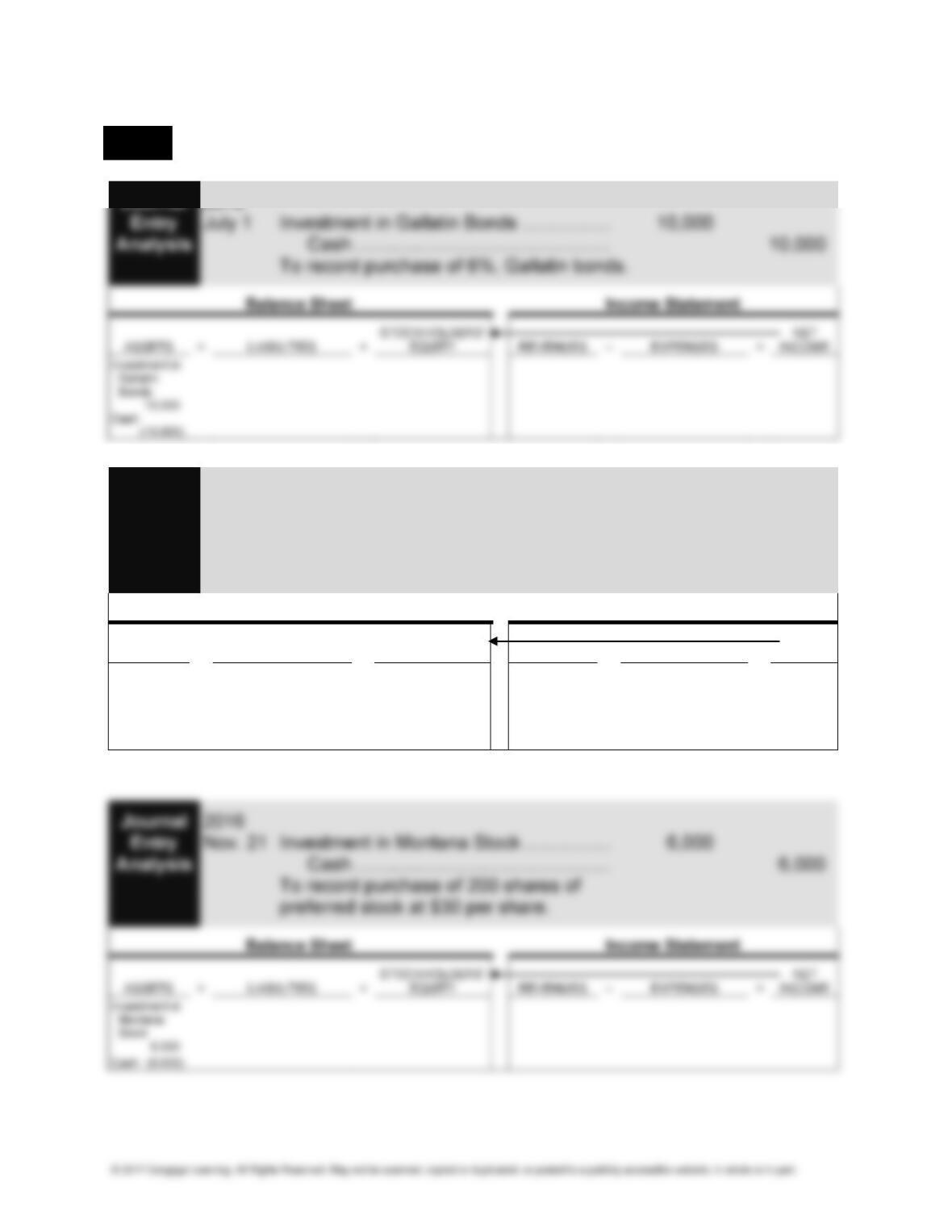

LO 5 PROBLEM 7-5 INVESTMENTS IN BONDS AND STOCK

Journal 2016

Journal 2016

Entry Oct. 23 Investment in Eagle Rock Stock ………………. 12,000

Analysis Cash ………………………………………………. 12,000

To record purchase of 600 shares of

common stock at $20 per share.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Investment in

Eagle Rock

Stock

12,000

Cash

(12,000)

CHAPTER 7 • RECEIVABLES AND INVESTMENTS 7-25

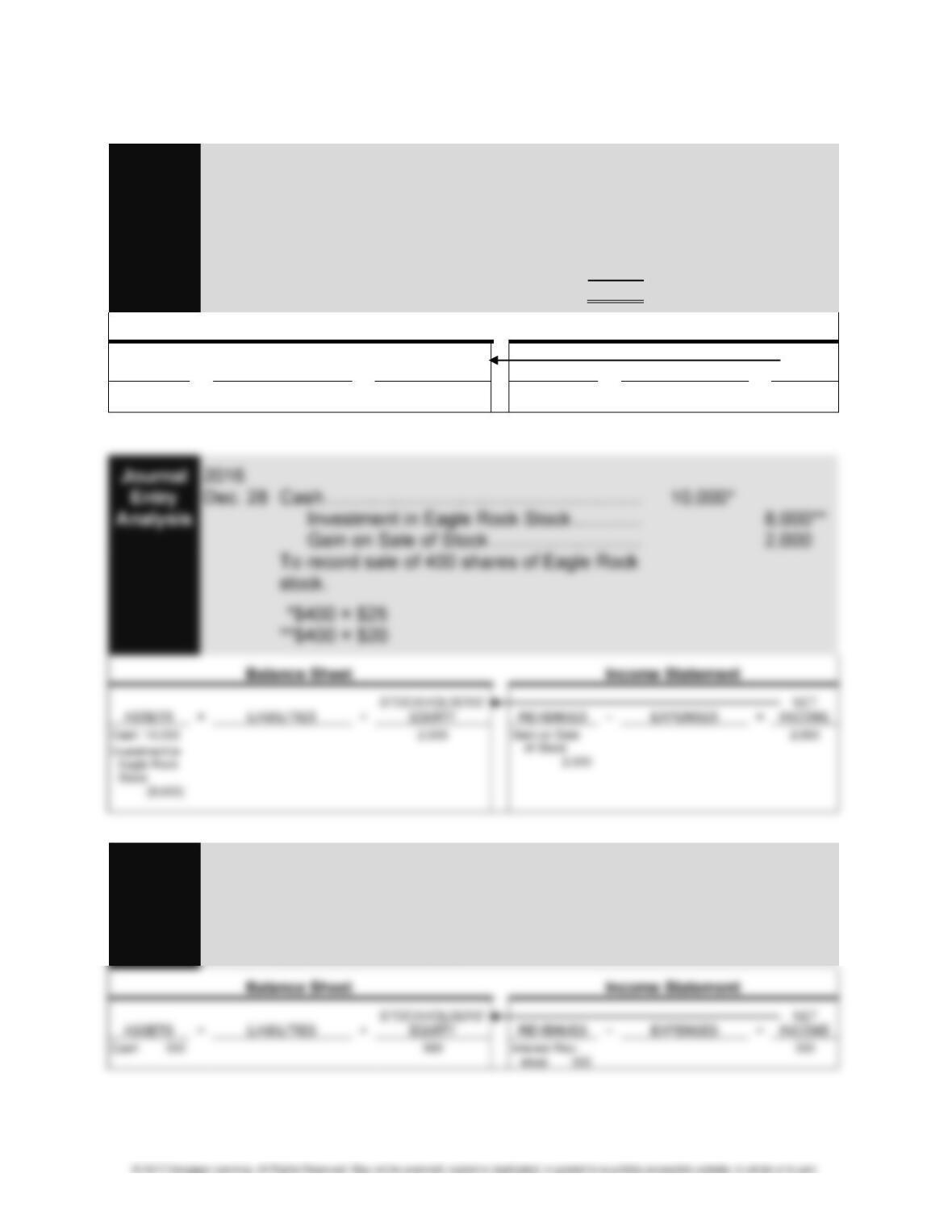

PROBLEM 7-5 (Concluded)

Journal 2016

Entry Dec. 10 Cash ……………………………………………………. 1,300

Analysis Dividend Income ………………………………. 1,300

To record receipt of dividends on securities:

Eagle Rock—600 × $1.50 $ 900

Montana—200 × $2.00 400

$1,300

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash 1,300

1,300

Dividend

Income 1,300

1,300

Journal 2016

Entry Dec. 31 Cash ………………………………………………. 300

Analysis Interest Revenue ………………………… 300

To record receipt of interest:

$10,000 × 6% × 6/12.

7-26 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

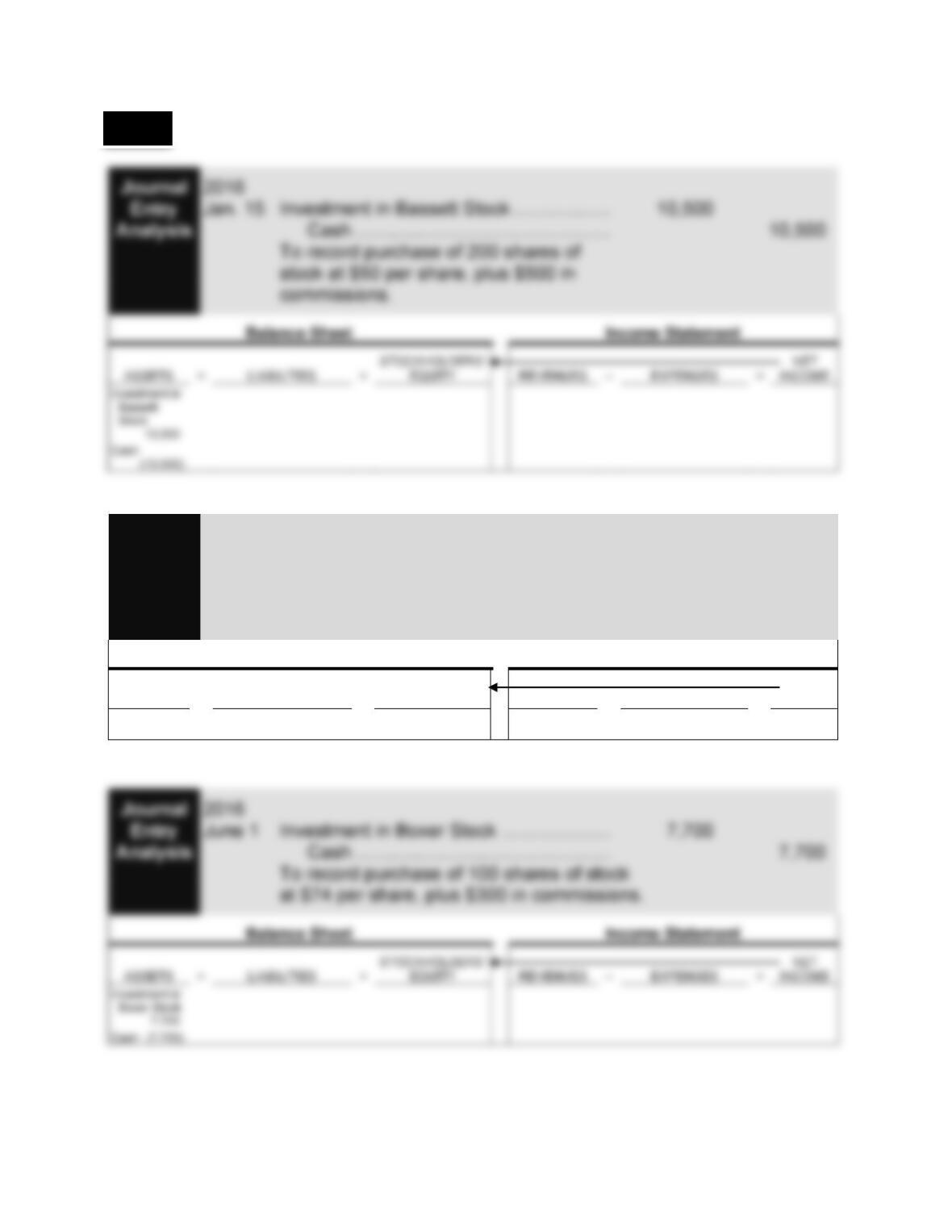

LO 5 PROBLEM 7-6 INVESTMENTS IN STOCK

Journal 2016

Entry May 23 Cash ……………………………………………………. 400

Analysis Dividend Income ………………………………. 400

To record receipt of dividends of $2 per

share on 200 shares of Bassett stock.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash 400

400

Dividend

Income 400

400

CHAPTER 7 • RECEIVABLES AND INVESTMENTS 7-27

PROBLEM 7-6 (Concluded)

Journal 2016

Entry Oct. 20 Cash ……………………………………………………. 8,000

Analysis Loss on Sale of Stock ……………………………. 2,500

Investment in Bassett Stock ……………….. 10,500

To record sale of Bassett stock:

(200 shares × $42) – $400 = $8,000.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash 8,000

Investment in

Bassett

Stock

(10,500)

(2,500)

Loss on Sale of

Stock 2,500

(2,500)

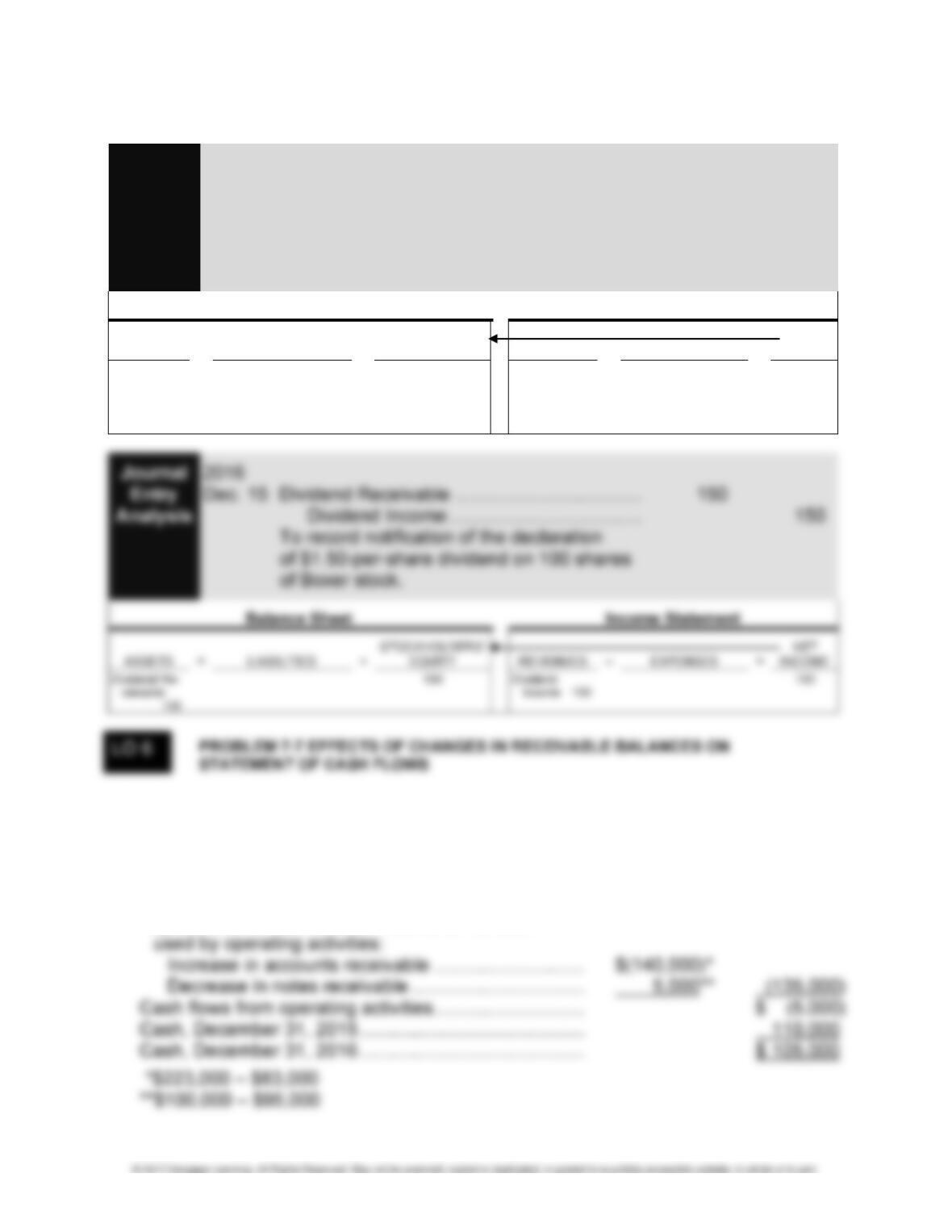

1. Statement of cash flows:

STEGNER INC.

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED DECEMBER 31, 2016

Net income …………………………………………………………. $ 130,000

Adjustments to reconcile net income to net cash

PROBLEM 7-7 (Concluded)

2. Memorandum to the president:

TO: Owner of Stegner, Inc.

FROM: Student’s name

DATE: January XX, 2017

SUBJECT: Cash Flows

MULTI-CONCEPT PROBLEM

LO 1,3 PROBLEM 7-8 ACCOUNTS AND NOTES RECEIVABLE

1. Journal entries:

Journal 2016

Entry May 15 Accounts Receivable—M. Baxter ……….. 5,000

Analysis Sales Revenue …………………………… 5,000

To record sale on credit; terms n/30.

CHAPTER 7 • RECEIVABLES AND INVESTMENTS 7-29

PROBLEM 7-8 (Continued)

Journal 2016

Entry Aug. 10 Allowance for Doubtful Accounts ………… 5,000

Analysis Accounts Receivable—M. Baxter ….. 5,000

To write off uncollectible account.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Journal 2016

Entry Dec. 1 Accounts Receivable—M. Baxter ……….. 5,000

Analysis Allowance for Doubtful Accounts …… 5,000

To restore account previously written off.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Accounts Re–

ceivable—

M. Baxter

7-30 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 7-8 (Concluded)

Journal 2016

Entry Dec. 31 Interest Receivable ……………………………….. 30

Analysis Interest Revenue ……………………………… 30

To accrue interest: $4,000 × 9% × 1/12.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Interest Re-

ceivable 30

30

Interest

Revenue 30

30

Journal 2017

Entry Jan. 31 Cash ………………………………………………. 4,060

Analysis Interest Receivable ……………………… 30

Interest Revenue ………………………… 30

Notes Receivable ………………………… 4,000

To record collection of note and interest.

Balance Sheet Income Statement

2. Baxter is interested in reestablishing a good credit standing with its supplier, Lenox,

and for this reason has sent the check and signed a note for the balance.

CHAPTER 7 • RECEIVABLES AND INVESTMENTS 7-31

ALTERNATE PROBLEMS

LO 1 PROBLEM 7-1A ALLOWANCE METHOD FOR ACCOUNTING FOR BAD DEBTS

1.

Journal Cash …………………………………………………………… 502,500

Entry Accounts Receivable ……………………………….. 502,500

Analysis To record collection of customer accounts.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash

502,500

Accounts

Receivable

(502,500)

7-32 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 7-1A (Continued)

2. a.

Journal Bad Debts Expense ………………………………………. 18,900

Entry Allowance for Doubtful Accounts ……………….. 18,900

Analysis To record estimated bad debts expense:

$630,000 × 3%.

b.

Journal Bad Debts Expense ………………………………………. 14,820

Entry Allowance for Doubtful Accounts ……………….. 14,820

Analysis To record estimated bad debts expense:

Accounts receivable at December 31, 2016

($105,000 + $630,000 – $502,500 – $3,000) = $229,500

× 0.06

Allowance balance needed $ 13,770 (Cr.)

Balance before adjustment:

Beginning balance $1,950 (Cr.)

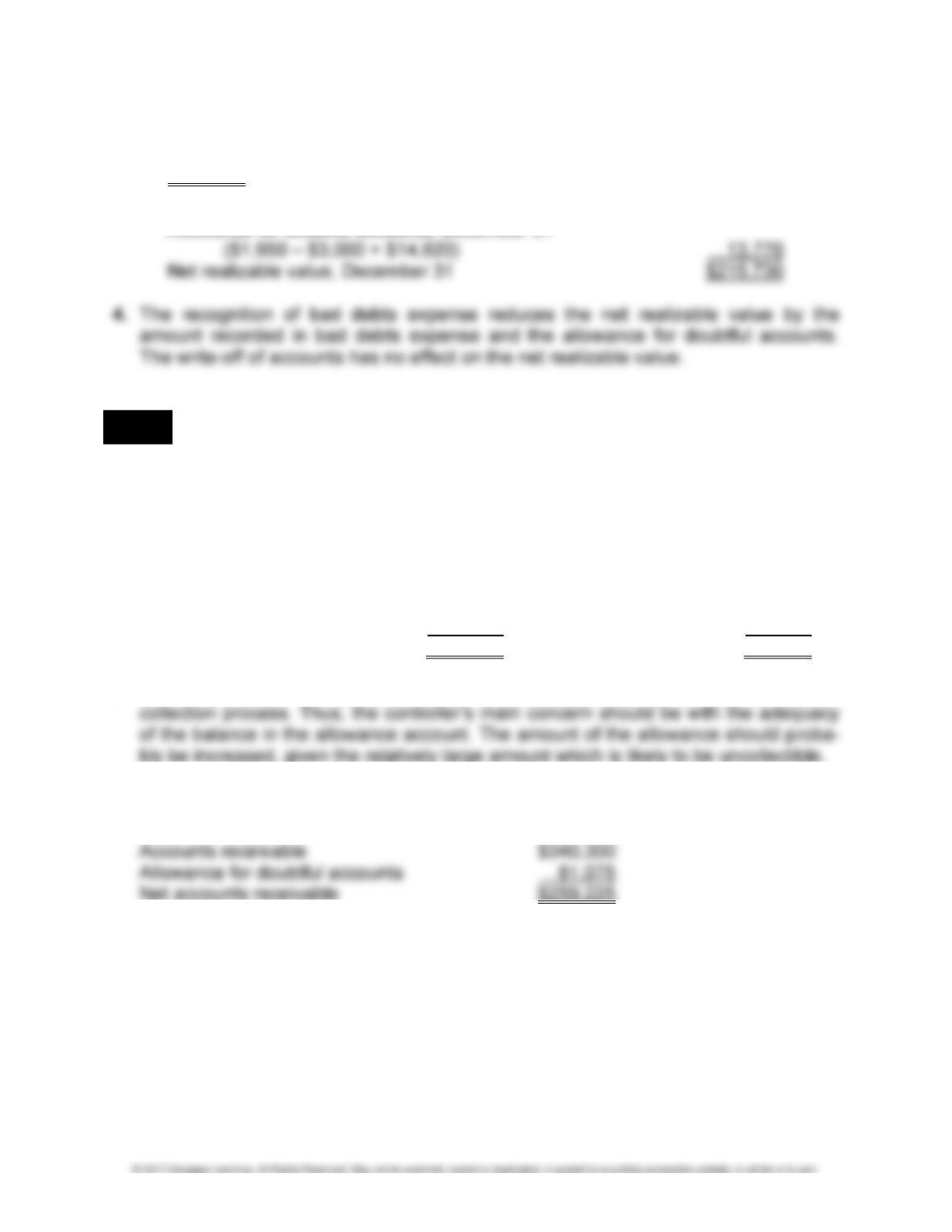

3. a. The net realizable value of accounts receivable on December 31, 2016, is $211,650:

Accounts receivable, December 31 [from part (2b)] $229,500

CHAPTER 7 • RECEIVABLES AND INVESTMENTS 7-33

PROBLEM 7-1A (Concluded)

b. The net realizable value of accounts receivable on December 31, 2016, is

$215,730:

Accounts receivable, December 31 [from part (2b)] $229,500

Allowance for doubtful accounts, December 31

LO 1 PROBLEM 7-2A USING AN AGING SCHEDULE TO ACCOUNT FOR BAD DEBTS

1. Estimated Estimated

Percent Amount

Category Amount Uncollectible Uncollectible

Current $200,000 10% $20,000

Past due:

Less than one month 60,300 25 15,075

One to two months 35,000 35 12,250

Over two months 45,000 75 33,750

Totals $340,300 $81,075

2. The controller is primarily responsible for the accuracy of the records, rather than the

3. Partial balance sheet at December 31, 2016:

Current Assets