6-1

CHAPTER 6

Cash and Internal Control

OVERVIEW OF EXERCISES, PROBLEMS, AND CASES

Estimated

Time in

Learning Objectives Exercises Minutes Level

Module 1

1. Identify and describe the various forms of cash reported 1 10 Easy

on a balance sheet. 2 10 Easy

9* 15 Mod

Module 2

3. Explain the importance of internal control to a business and the

significance of the Sarbanes-Oxley Act of 2002.

6-2 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

Problems Estimated

and Time in

Learning Objectives Alternates Minutes Level

Module 1

Module 2

3. Explain the importance of internal control to a business and the 5* 20 Mod

significance of the Sarbanes-Oxley Act of 2002.

CHAPTER 6 • CASH AND INTERNAL CONTROL 6-3

Estimated

Time in

Learning Objectives Cases Minutes Level

Module 1

1. Identify and describe the various forms of cash reported 1 20 Mod

on a balance sheet. 3 30 Mod

4* 20 Mod

Module 2

3. Explain the importance of internal control to a business and the 2 25 Mod

significance of the Sarbanes-Oxley Act of 2002. 5* 30 Mod

6-4 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISES

LO 1 EXERCISE 6-1 CASH EQUIVALENTS

Cash equivalents at December 31, 2016:

Certificate of deposit, due March 30, 2017 ……………………………. $150,000

LO 1 EXERCISE 6-2 CASH AND CASH EQUIVALENTS AND THE STATEMENT OF CASH

FLOWS

Beginning balance in cash and cash equivalents ……… $ 23,500*

Cash provided by operating activities ……………. $ 140,000

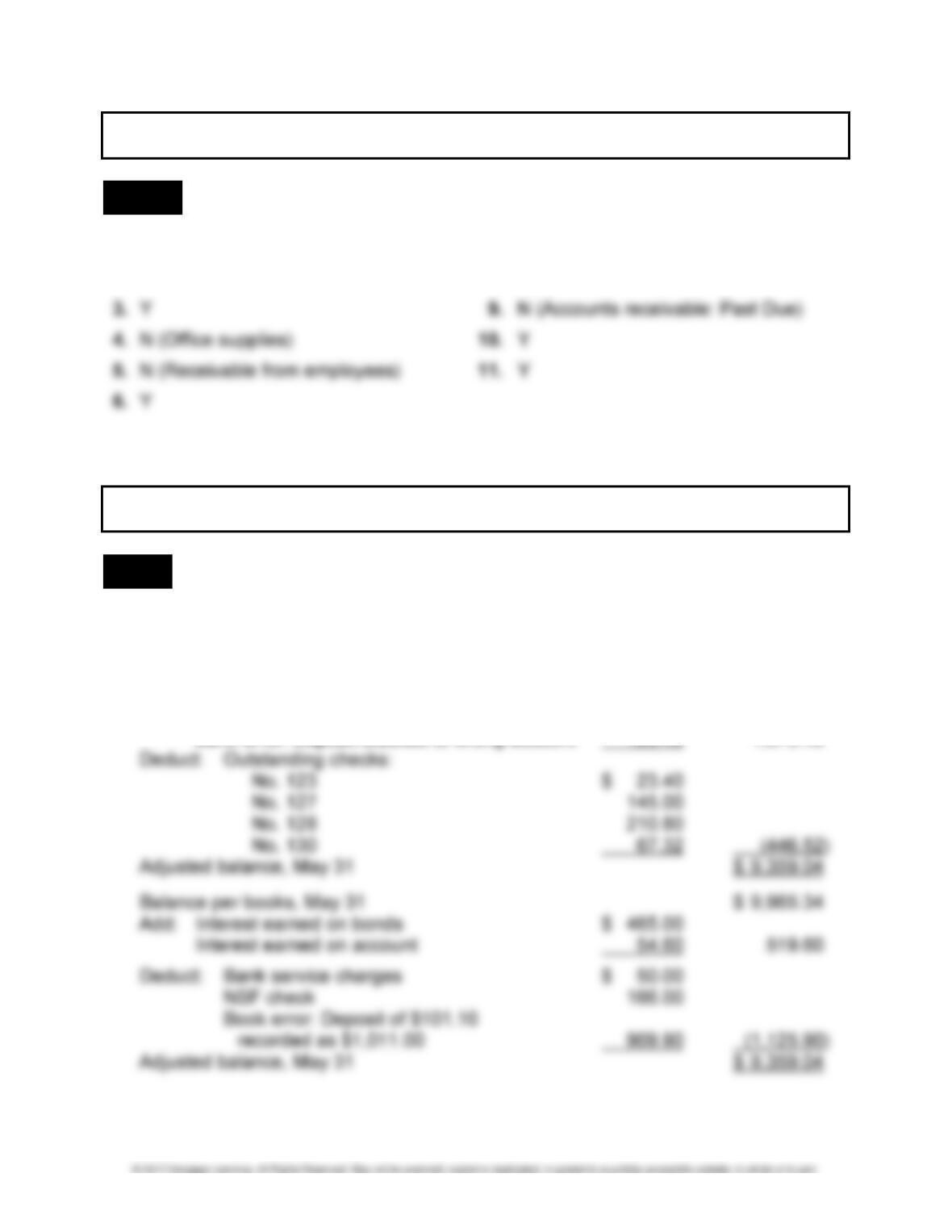

LO 2 EXERCISE 6-3 ITEMS ON A BANK RECONCILIATION

1. D-Bank 4. D-Book, JE 7. NA

CHAPTER 6 • CASH AND INTERNAL CONTROL 6-5

LO 2 EXERCISE 6-4 WORKING BACKWARD: BANK RECONCILIATION

The amounts on the bank statement and on the books prior to adjustment can be de-

termined by working backwards:

DEXTER COMPANY

BANK RECONCILIATION

Balance per bank statement $ ?

Add: Deposit in transit ……………………………………………………… 332.10

Deduct: Outstanding checks (560.55)

Adjusted balance, May 31 ……………………………………………………….. $3,254.33

6-6 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

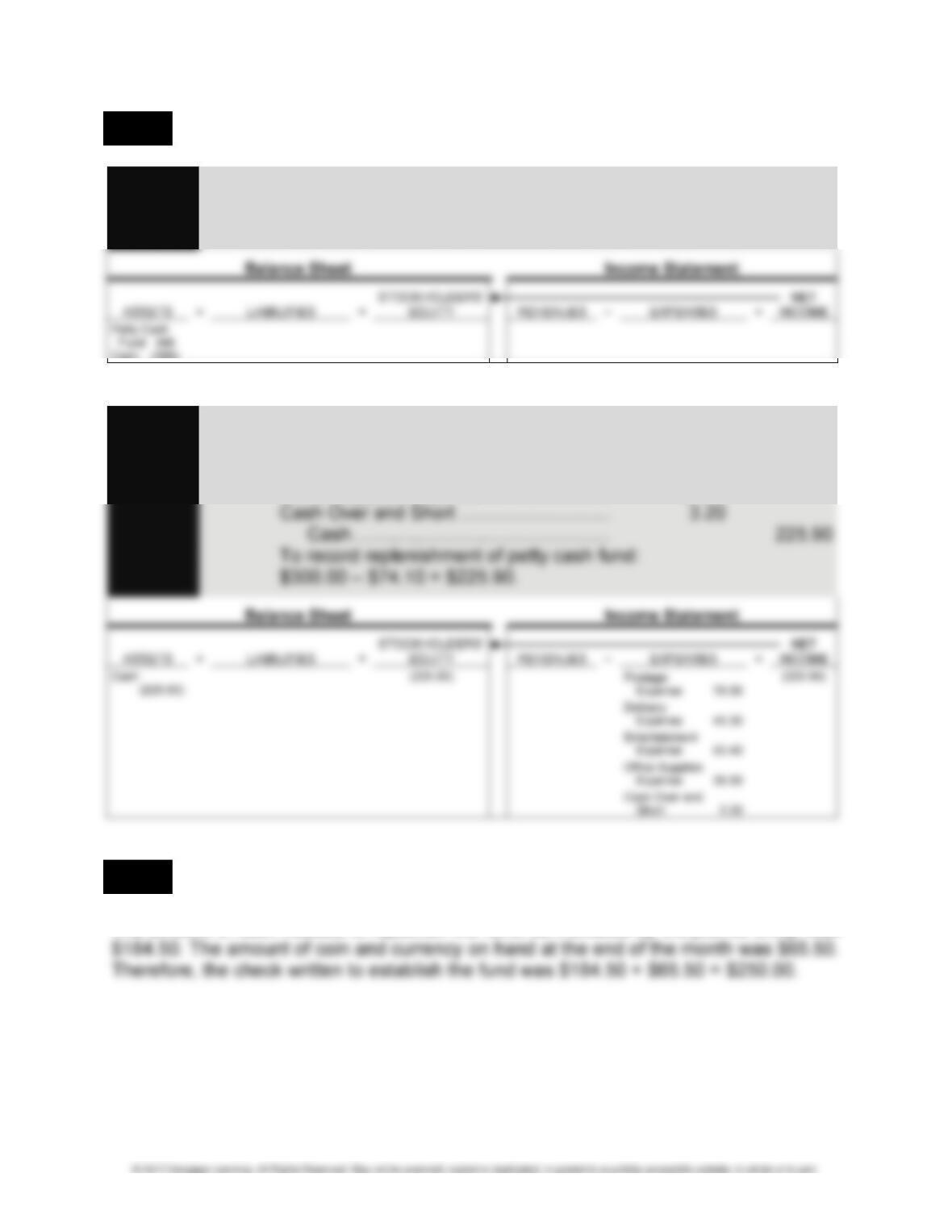

LO 2 EXERCISE 6-5 PETTY CASH FUND

Journal Jan. 2 Petty Cash Fund ……………………………… 300.00

Entry Cash …………………………………………. 300.00

Analysis To record establishment of petty cash fund.

Cash (300)

Journal Jan. 31 Postage Expense …………………………….. 76.00

Entry Delivery Expense …………………………….. 45.30

Analysis Entertainment Expense …………………….. 65.40

Office Supplies Expense …………………… 36.00

LO 2 EXERCISE 6-6 WORKING BACKWARD: PETTY CASH FUND

The amount of cash needed to replenish the fund, as indicated by the journal entry, was

CHAPTER 6 • CASH AND INTERNAL CONTROL 6-7

LO 4 EXERCISE 6-7 INTERNAL CONTROL

1. Students’ answers to this question will vary. Among the possible guidelines the club

should follow are:

2. The president would like verification that all money is collected and recorded. It

would be difficult, if not impossible, to be completely sure that this happens. For ex-

LO 4 EXERCISE 6-8 SEGREGATION OF DUTIES

Many possible combinations are possible. One appropriate way to segregate the duties

would be as follows:

Employee

Task Mary Sue John

Prepare invoices X

Mail invoices X

Pick up mail from post office X

6-8 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

MULTI-CONCEPT EXERCISE

LO 1,2 EXERCISE 6-9 COMPOSITION OF CASH

1. Y 7. N (Short-term investments: CD)

2. Y 8. Y

PROBLEMS

LO 2 PROBLEM 6-1 BANK RECONCILIATION

1. CALICO CORNERS

BANK RECONCILIATION

MAY 31

Balance per bank statement, May 31 $ 8,432.11

Add: Deposit in transit $1,250.00

Bank error: Deposit credited to wrong account 123.45 1,373.45

PROBLEM 6-1 (Concluded)

2.

Journal May 31 Cash ………………………………………………. 519.60

Entry Interest Revenue ………………………… 519.60

Analysis To record interest earned.

enue 519.60

Journal May 31 Bank Service Fees Expense ……………… 50.00

Entry Cash …………………………………………. 50.00

Analysis To record bank service charges.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash (50.00)

(50.00)

Bank Service Fees

Expense 50.00

(50.00)

Journal May 31 Accounts Receivable ………………………… 166.00

Entry Cash …………………………………………. 166.00

Analysis To record customer’s NSF check.

(166.00)

Journal May 31 Accounts Receivable ………………………… 909.90

Entry Cash …………………………………………. 909.90

Analysis To correct error in recording customer’s check.

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

6-10 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 4 PROBLEM 6-2 INTERNAL CONTROL PROCEDURES

1. List of procedures to follow:

a. Ring the sale on the cash register, and give every customer a receipt.

2. Procedures to follow at end of day to close out:

a. Count the coins and currency in the drawer. Record on daily cash and sales re-

3. The primary concern in this operation is control over cash, because all sales are

cash. This concern was addressed by using a cash register, having the lead person

check the cash, and depositing it intact daily.

LO 5 PROBLEM 6-3 THE DESIGN OF INTERNAL CONTROL DOCUMENTS

1. The old system of allowing each motel to buy supplies from local distributors offered

very little internal control. For example, the corporate office had no control over the

PROBLEM 6-3 (Concluded)

2. The purchase requisition form should be in triplicate, with the original filled out by the

requesting department and copies to the purchasing and accounting departments.

The form should show the following:

a. requesting department

b. date requested

The receiving report should be in duplicate, with the original filled out by the receiv-

ing department with a copy to the accounting department. It should show the follow-

ing:

a. purchase order number

b. vendor

c. carrier/shipper

6-12 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

MULTI-CONCEPT PROBLEMS

LO 1,2 PROBLEM 6-4 CASH AND LIQUID ASSETS ON THE BALANCE SHEET

In order of liquidity on the balance sheet:

1. Petty Cash Fund

2. Money Market Fund

The first two items would be included in cash and cash equivalents on the balance

sheet. All other items are not as liquid and require either collection or sale to generate

cash. Prepaid rent is considered current because the benefits will normally expire within

LO 3,4 PROBLEM 6-5 INTERNAL CONTROL

1. Morris Mart suffers from a lack of segregation of duties. Mary handles all tasks as-

sociated with collection of customer accounts.

2. Mary should not handle all aspects of accounts receivable, billing, and collection.

Two different employees should mail invoices and record the amounts billed. Two

3. Someone should explain to Mary that she personally is not the problem but that a

good system of internal control requires certain changes to be made. This could be

CHAPTER 6 • CASH AND INTERNAL CONTROL 6-13

ALTERNATE PROBLEMS

LO 2 PROBLEM 6-1A BANK RECONCILIATION

1. Amounts can be found by preparing a bank reconciliation:

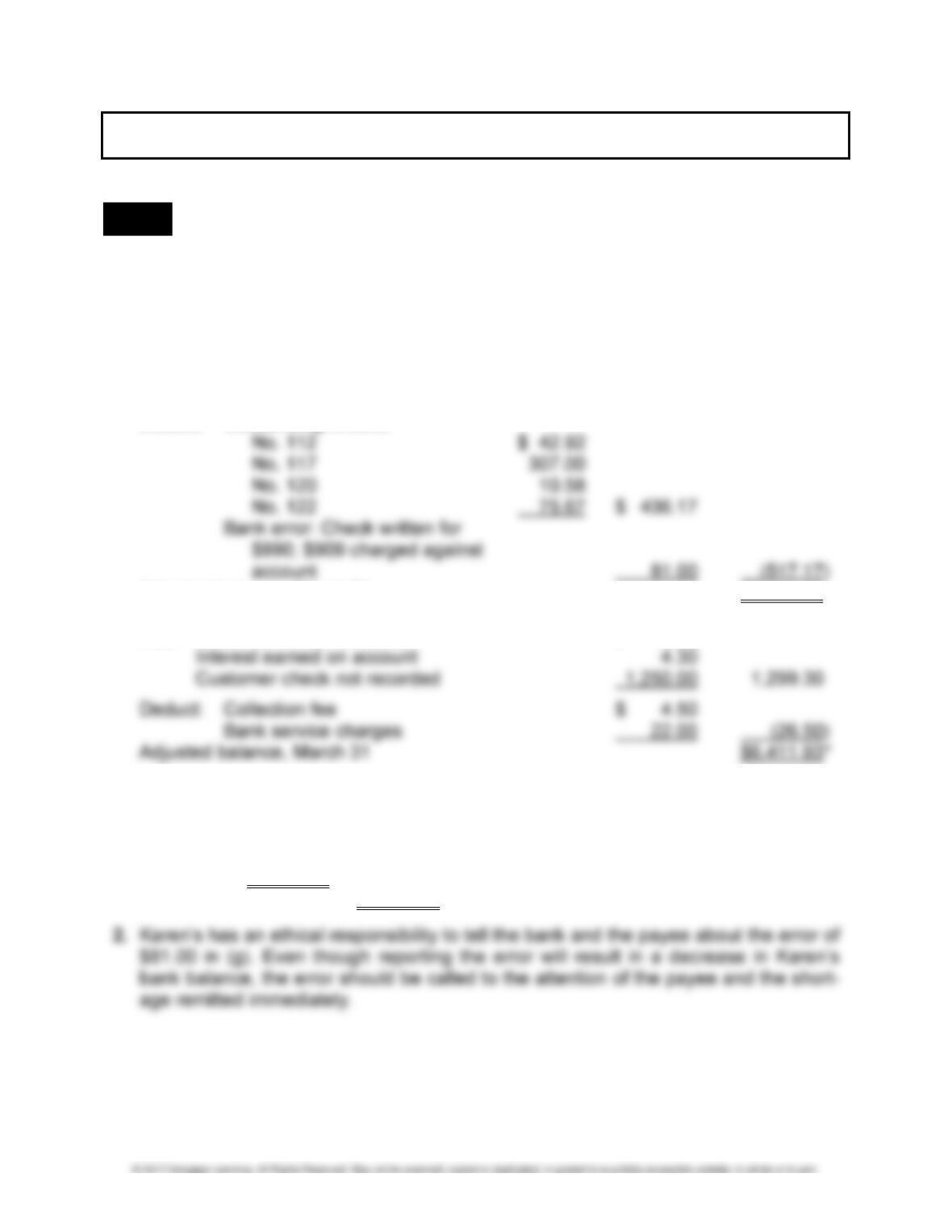

KAREN’S CATERING

BANK RECONCILIATION

MARCH 31

Balance per bank statement, March 31 $6,506.10

Add: Deposit in transit 423.00

Deduct: Outstanding checks:

Adjusted balance, March 31 $6,411.93

Balance per books, March 31 $ ?

Add: Customer check collected $ 45.00

*Adjusted balance per the books must be the same amount as the adjusted balance

per the bank.

Conclusion: The balance on the books before any adjustments is the ? in the bank

reconciliation and can be found by working backwards: $6,411.93 + $26.50 –

$1,299.30 = $5,139.13. The corrected balance to be reported on the balance sheet

is the adjusted balance of $6,411.93.

6-14 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 4 PROBLEM 6-2A INTERNAL CONTROL PROCEDURES

1. The bank and regulatory agency are concerned with these documents because

without proper documentation the legal agreement could be invalid. For example,

2. Internal control procedures to ensure that the documents are obtained and safe-

guarded are as follows:

a. The accuracy and completeness of all information on the note, insurance policy,

and title should be verified and reviewed.

LO 5 PROBLEM 6-3A THE DESIGN OF INTERNAL CONTROL DOCUMENTS

1. Procedures to ensure that all royalties are paid to the actors are as follows:

a. All payments must be made by check.

2. The shipping form should be in duplicate, with the original filled out by the shipping

department and a copy to the accounting department. It should include the following:

a. authorizations

CHAPTER 6 • CASH AND INTERNAL CONTROL 6-15

ALTERNATE MULTI-CONCEPT PROBLEMS

LO 1,2 PROBLEM 6-4A CASH AND LIQUID ASSETS ON THE BALANCE SHEET

1. Cash in the checking account and the petty cash fund are cash. The three-month

certificates of deposit and the money market fund are both cash equivalents.

2. Accounts receivable and marketable securities should be classified on the balance

sheet as current assets and listed in the order of their liquidity (marketable securities

are more liquid than accounts receivable).

LO 3,4 PROBLEM 6-5A INTERNAL CONTROL

1. There are two major problems with the proposed personnel arrangements. First, re-

gardless of how ethical and honest the two individuals might be, from the viewpoint

2. Regardless of how effective a system of internal control, it can be easily circum-

vented by collusion, that is, two or more employees working together to perpetrate a

3. The above should be explained to the two individuals. They personally are not the

6-16 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

DECISION CASES

READING AND INTERPRETING FINANCIAL STATEMENTS

LO 1 DECISION CASE 6-1 COMPARING TWO COMPANIES IN THE SAME INDUSTRY:

CHIPOTLE AND PANERA BREAD

1. The balance in Cash and cash equivalents on Chipotle’s balance sheet at the end of

the year was $419,465,000, an increase of $96,262,000 from the $323,203,000 bal-

ance at the end of the prior year. The balance in Cash and cash equivalents on Pa-

nera Bread’s balance sheet at the end of the year was $196,493,000, an increase of

$71,248,000 from the $125,245,000 balance at the end of the prior year.

LO 3 DECISION CASE 6-2 READING AND INTERPRETING IBM’S REPORT OF

MANAGEMENT

1. IBM relies on clear definitions of responsibility and delegation of authority as part of

2. IBM’s external auditor is PricewaterhouseCoopers LLP. In addition to auditing the

company’s financial statements, PricewaterhouseCoopers LLP also performs an

3. IBM’s Audit Committee is made up entirely of members of the board of directors who

are independent from the company and not part of the company’s management

team. One of the key duties of the Audit Committee is to recommend to the board of

CHAPTER 6 • CASH AND INTERNAL CONTROL 6-17

MAKING FINANCIAL DECISIONS

LO 1 DECISION CASE 6-3 LIQUIDITY

TO: The President of FNB of Verona Heights

FROM: Joe Smith, Loan Officer

DATE: X/X/XX

SUBJECT: Loan proposals

I have reviewed the loan proposals recently submitted by R Montague and J Capulet

and have summarized my findings. Because of limited resources available for short-

term loans, my recommendation is that we make a six-month $10 million loan to

J Capulet only.

4.35%.

In summary, J Capulet is a better candidate at the present time for a loan. I recom-

mend that we make a six-month $10 million loan to J Capulet at the current market rate

of interest. Please call if you need any further details in connection with these two loan

requests.

6-18 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

ETHICAL DECISION MAKING

LO 1,2 DECISION CASE 6-4 USING A BANK RECONCILIATION TO DETERMINE CASH

BALANCE

1. Recognize an ethical dilemma:

You realize that cash will be overstated if the check is not treated as an NSF check

2. Analyze the key elements in the situation:

a. Your boss may benefit and users of the company’s financial statements may be

harmed.

b. Your boss may benefit if his performance is evaluated on the relative liquidity of

the company and whether receivables are collected in a timely fashion. The

3. List alternatives and evaluate the impact of each on those affected:

The alternatives are to go along with your boss’s instructions or to insist that the

NSF appear on the bank reconciliation and an entry made to reduce Cash. An NSF

check is handled by reducing the Cash account and reinstating Accounts Receiva-

4. Select the best alternative:

You should explain to your boss why it is important to report the NSF check on

the reconciliation and to make an entry to reduce Cash. If this does not resolve the

issue, you should discuss the issue with the person your boss reports to in the

organization.

CHAPTER 6 • CASH AND INTERNAL CONTROL 6-19

LO 3,4 DECISION CASE 6-5 CASH RECEIPTS IN A BOOKSTORE

Memo to the store manager:

Thank you for the opportunity to spend a week at one of our stores and learn more

about the bookstore business. During my training, I received valuable experience that

will benefit me as I begin working for the company. I am concerned, however, about one