CHAPTER 6

INTEREST RATES AND BOND VALUTION

Answers to Concepts Review and Critical Thinking Questions

1. No. As interest rates fluctuate, the value of a Treasury security will fluctuate. Long-term Treasury

securities have substantial interest rate risk.

4. Prices and yields move in opposite directions. Since the bid price must be lower, the bid yield must be

higher.

5. There are two benefits. First, the company can take advantage of interest rate declines by calling in an

issue and replacing it with a lower coupon issue. Second, a company might wish to eliminate a

covenant for some reason. Calling the issue does this. The cost to the company is a higher coupon. A

put provision is desirable from an investor’s standpoint, so it helps the company by reducing the

coupon rate on the bond. The cost to the company is that it may have to buy back the bond at an

unattractive price.

7. Yes. Some investors have obligations that are denominated in dollars; i.e., they are nominal. Their

primary concern is that an investment provides the needed nominal dollar amounts. Pension funds, for

example, often must plan for pension payments many years in the future. If those payments are fixed

in dollar terms, then it is the nominal return on an investment that is important.

10. Bond ratings have a subjective factor to them. Split ratings reflect a difference of opinion among credit

agencies.

11. As a general constitutional principle, the federal government cannot tax the states without their consent

if doing so would interfere with state government functions. At one time, this principle was thought

to provide for the tax-exempt status of municipal interest payments. However, modern court rulings

make it clear that Congress can revoke the municipal exemption, so the only basis now appears to be

historical precedent. The fact that the states and the federal government do not tax each other’s

securities is referred to as “reciprocal immunity.”

14. A 100-year bond looks like a share of preferred stock. In particular, it is a loan with a life that almost

certainly exceeds the life of the lender, assuming that the lender is an individual. With a junk bond,

the credit risk can be so high that the borrower is almost certain to default, meaning that the creditors

are very likely to end up as part owners of the business. In both cases, the “equity in disguise” has a

significant tax advantage.

15. a. The bond price is the present value when discounting the future cash flows from a bond; YTM is

the interest rate used in discounting the future cash flows (coupon payments and principal) back

to their present values.

b. If the coupon rate is higher than the required return on a bond, the bond will sell at a premium,

since it provides periodic income in the form of coupon payments in excess of that required by

investors on other similar bonds. If the coupon rate is lower than the required return on a bond,

Solutions to Questions and Problems

NOTE: All end-of-chapter problems were solved using a spreadsheet. Many problems require multiple

steps. Due to space and readability constraints, when these intermediate steps are included in this solutions

manual, rounding may appear to have occurred. However, the final answer for each problem is found

without rounding during any step in the problem.

Basic

1. The yield to maturity is the required rate of return on a bond expressed as a nominal annual interest

2. Price and yield move in opposite directions; if interest rates rise, the price of the bond will fall. This is

because the fixed coupon payments determined by the fixed coupon rate are not as valuable when

interest rates rise–hence, the price of the bond decreases.

3. The price of any bond is the PV of the interest payment, plus the PV of the par value. Notice this

problem assumes an annual coupon. The price of the bond will be:

which stands for Present Value Interest Factor

PVIFAR,t = ({1 – [1/(1 + R)]t } / R)

which stands for Present Value Interest Factor of an Annuity

4. Here, we need to find the YTM of a bond. The equation for the bond price is:

P = $961.50 = $70(PVIFAR%,9) + $1,000(PVIFR%,9)

Notice the equation cannot be solved directly for R. Using a spreadsheet, a financial calculator, or trial

and error, we find:

5. Here we need to find the coupon rate of the bond. All we need to do is to set up the bond pricing

equation and solve for the coupon payment as follows:

P = $963 = C(PVIFA6.14%,12) + $1,000(PVIF6.14%,12)

Solving for the coupon payment, we get:

6. To find the price of this bond, we need to realize that the maturity of the bond is 14 years. The bond

was issued one year ago, with 15 years to maturity, so there are 14 years left on the bond. Also, the

coupons are semiannual, so we need to use the semiannual interest rate and the number of semiannual

periods. The price of the bond is:

P = $30.50(PVIFA2.65%,28) + $1,000(PVIF2.65%,28)

P = $1,078.37

7. Here, we are finding the YTM of a semiannual coupon bond. The bond price equation is:

P = $940 = $27(PVIFAR%,26) + $1,000(PVIFR%,26)

8. Here, we need to find the coupon rate of the bond. All we need to do is to set up the bond pricing

equation and solve for the coupon payment as follows:

P = $945 = C(PVIFA3.1%,21) + $1,000(PVIF3.1%,21)

Solving for the coupon payment, we get:

9. The approximate relationship between nominal interest rates (R), real interest rates (r), and inflation

(h), is:

R = r + h

Approximate r = .045 – .016

Approximate r =.0285, or 2.85%

10. The Fisher equation, which shows the exact relationship between nominal interest rates, real interest

rates, and inflation, is:

(1 + R) = (1 + r)(1 + h)

11. The Fisher equation, which shows the exact relationship between nominal interest rates, real interest

rates, and inflation, is:

(1 + R) = (1 + r)(1 + h)

12. The Fisher equation, which shows the exact relationship between nominal interest rates, real interest

rates, and inflation, is:

(1 + R) = (1 + r)(1 + h)

13. The coupon rate, located in the second column of the quote is 6.125%. The bid price is:

Bid price = 146.1719%

$1,000

Bid price = $1,461.719

The previous day’s ask price is found by:

14. This is a premium bond because it sells for more than 100 percent of face value. The current yield is

based on the asked price, so the current yield is:

Current yield = Annual coupon payment / Price

Current yield = $47.50 / $1,373.672

Current yield = .0346, or 3.46%

15. To find the price of a zero coupon bond, we need to find the value of the future cash flows. With a

zero coupon bond, the only cash flow is the par value at maturity. We find the present value assuming

semiannual compounding to keep the YTM of a zero coupon bond equivalent to the YTM of a coupon

bond, so:

P = $10,000(PVIF2.45%,34)

P = $4,391.30

17. To find the price of this bond, we need to find the present value of the bond’s cash flows. So, the price

of the bond is:

18. Here, we are finding the price of annual coupon bonds for various maturity lengths. The bond price

equation is:

P = C(PVIFAR%,t) + $1,000(PVIFR%,t)

P8 = $35(PVIFA4.25%,5) + $1,000(PVIF4.25%,5) = $939.92

P12 = $35(PVIFA4.25%,1) + $1,000(PVIF4.25%,1) = $985.90

P13 = $1,000

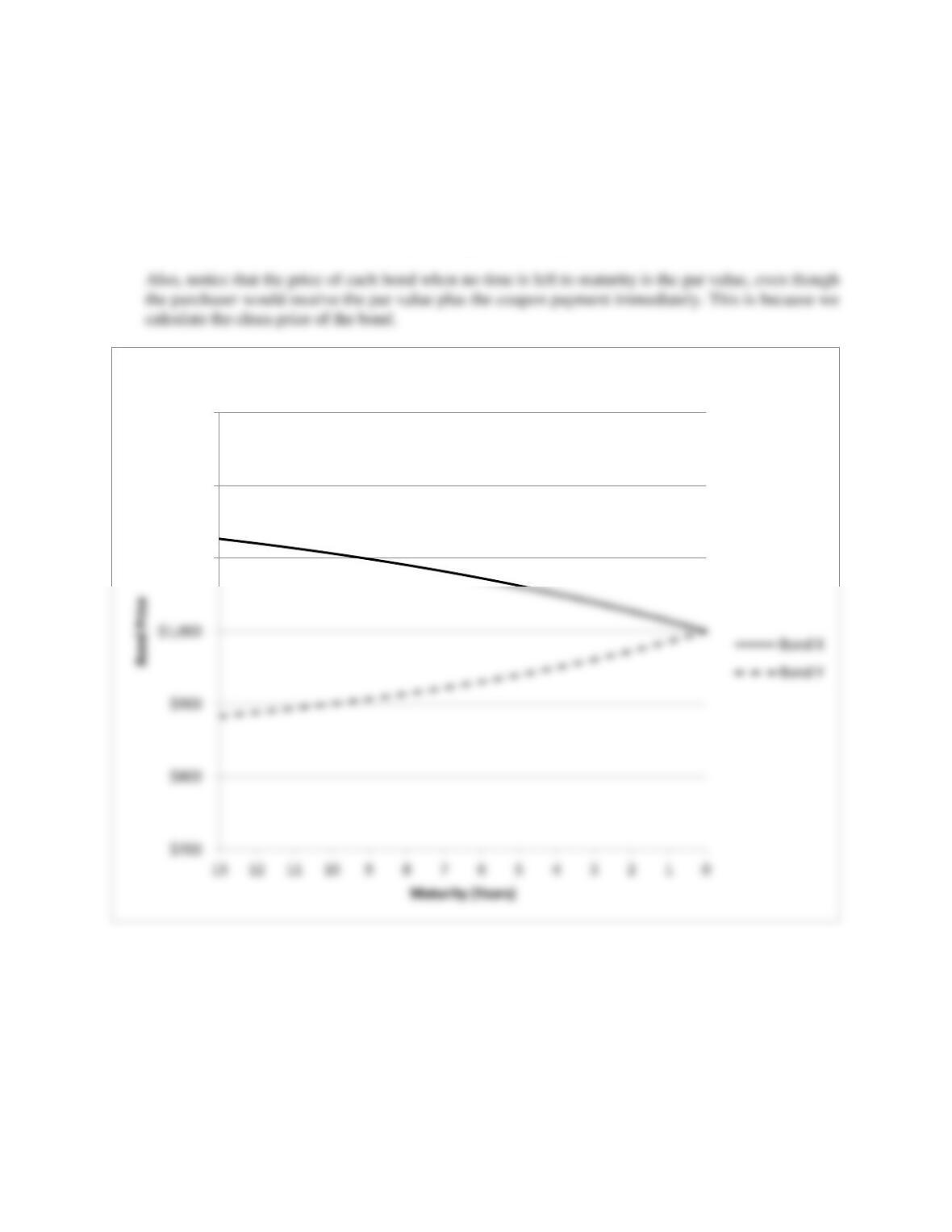

All else held equal, the premium over par value for a premium bond declines as maturity approaches,

and the discount from par value for a discount bond declines as maturity approaches. This is called

“pull to par.” In both cases, the largest percentage price changes occur at the shortest maturity lengths.

$1,100

$1,200

$1,300

Maturity and Bond Price

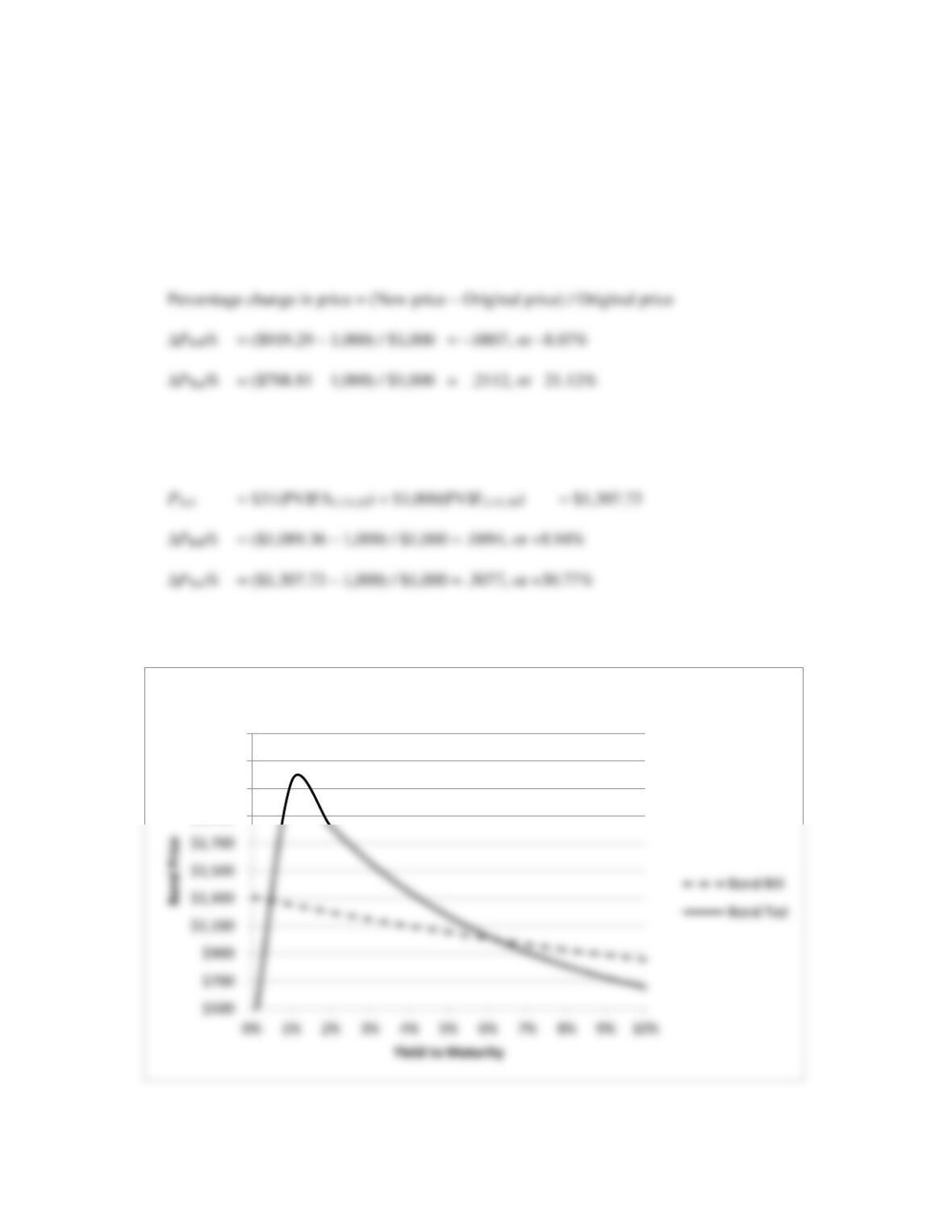

19. Any bond that sells at par has a YTM equal to the coupon rate. Both bonds sell at par, so the initial

YTM on both bonds is the coupon rate, 6.2 percent. If the YTM suddenly rises to 8.2 percent:

PBill = $31(PVIFA4.1%,10) + $1,000(PVIF4.1%,10) = $919.29

PTed = $31(PVIFA4.1%,50) + $1,000(PVIF4.1%,50) = $788.81

The percentage change in price is calculated as:

If the YTM suddenly falls to 4.2 percent:

PBill = $31(PVIFA2.1%,10) + $1,000(PVIF2.1%,10) = $1,089.36

All else the same, the longer the maturity of a bond, the greater is its price sensitivity to changes in

interest rates.

$1,900

$2,100

$2,300

$2,500

YTM and Bond Price

20. Initially, at a YTM of 8 percent, the prices of the two bonds are:

PJ = $20(PVIFA4%,26) + $1,000(PVIF4%,26) = $680.34

PS = $70(PVIFA4%,26) + $1,000(PVIF4%,26) = $1,479.48

If the YTM rises from 8 percent to 10 percent:

If the YTM declines from 8 percent to 6 percent:

PJ = $20(PVIFA3%,26) + $1,000(PVIF3%,26) = $821.23

PS = $70(PVIFA3%,26) + $1,000(PVIF3%,26) = $1,715.07

All else the same, the lower the coupon rate on a bond, the greater is its price sensitivity to changes in

interest rates.

21. The current yield is:

Current yield = Annual coupon payment / Price

Current yield = $63 / $970

Current yield =.0649, or 6.49%

The bond price equation for this bond is:

The effective annual yield is the same as the EAR, so using the EAR equation from the previous

chapter:

22. The company should set the coupon rate on its new bonds equal to the required return of the existing

bonds. The required return can be observed in the market by finding the YTM on outstanding bonds

of the company. So, the YTM on the bonds currently sold in the market is:

P = $1,074 = $28(PVIFAR%,50) + $1,000(PVIFR%,50)

23. Accrued interest is the coupon payment for the period times the fraction of the period that has passed

since the last coupon payment. Since we have a semiannual coupon bond, the coupon payment per six

months is one-half of the annual coupon payment. There are five months until the next coupon

payment, so one month has passed since the last coupon payment. The accrued interest for the bond

is:

Accrued interest = $57/2 × 1/6

Accrued interest = $4.75

24. Accrued interest is the coupon payment for the period times the fraction of the period that has passed

since the last coupon payment. Since we have a semiannual coupon bond, the coupon payment per six

months is one-half of the annual coupon payment. There are two months until the next coupon

payment, so four months have passed since the last coupon payment. The accrued interest for the bond

is:

Accrued interest = $59/2 × 4/6

Accrued interest = $19.67

25. The bond has 15 years to maturity, so the bond price equation is:

P = $916.45 = $42.50(PVIFAR%,30) + $1,000(PVIFR%,30)

Using a spreadsheet, financial calculator, or trial and error, we find:

26. a. The coupon bonds have coupon rate of 6.8 percent which matches the 6.8 percent required return,

so they will sell at par. The number of bonds that must be sold is the amount needed divided by

the bond price, so:

Number of coupon bonds to sell = $35,000,000 / $1,000

Number of coupon bonds to sell = 35,000

b. The repayment of the coupon bond will be the par value plus the last coupon payment times the

number of bonds issued. So:

Coupon bonds repayment = 35,000($1,000) + 35,000($1,000)(.068 / 2)

Coupon bonds repayment = $36,190,000

c. The total coupon payment for the coupon bonds will be the number bonds times the coupon

payment. For the cash flow of the coupon bonds, we need to account for the tax deductibility of

the interest payments. To do this, we will multiply the total coupon payment times one minus the

tax rate. So:

P1 = $1,000 / 1.03438

P1 = $280.69

The Year 1 interest deduction per bond will be this price minus the price at the beginning of the

year, which we found in part b, so:

Notice the cash flow for the zeroes is a cash inflow. This is because of the tax deductibility of the

imputed interest expense. That is, the company gets to write off the interest expense for the year,

even though the company did not have a cash flow for the interest expense. This reduces the

company’s tax liability, which is a cash inflow.

During the life of the bond, the zero generates cash inflows to the firm in the form of the interest

tax shield of debt. We should note an important point here: If you find the PV of the cash flows

from the coupon bond and the zero coupon bond, they will be the same. This is because of the

much larger repayment amount for the zeroes.

27. The maturity is indeterminate. A bond selling at par can have any length of maturity.

28. The bond asked price is 104.3850, so the dollar price is:

Using a spreadsheet, financial calculator, or trial and error, we find:

R = 2.659%

29. The coupon rate of the bond is 6.125 percent and the bond matures in 20 years. The bond coupon

payments are semiannual, so the asked price is:

P = $30.625(PVIFA1.935%,40) + $1,000(PVIF1.935%,40)

P = $1,311.98

30. Here, we need to find the coupon rate of the bond. The price of the bond is:

Dollar price = 103.8235% × $1,000

Dollar price = $1,038.235

So the bond price equation is:

31. Here we need to find the yield to maturity. The dollar price of the bond is:

Dollar price = 96.153% × $2,000

Dollar price = $1,923.06

So, the bond price equation is:

P = $1,923.06 = $54(PVIFAR%,8) + $2,000(PVIFR%,8)

32. The bond price equation is:

P = $71.25(PVIFA3.01%,10) + $2,000(PVIF3.01%,10)

P = $2,094.21

The current yield is the annual coupon payment divided by the bond price, so:

33. Here, we need to find the coupon rate of the bond. The dollar price of the bond is:

Dollar price = 94.735% × $2,000

Dollar price = $1,894.70

Now, we need to do is to set up the bond pricing equation and solve for the coupon payment as follows:

P = $1,894.70 = C(PVIFA3.425%,24) + $2,000(PVIF3.425%,24)

Challenge

34. To find the capital gains yield and the current yield, we need to find the price of the bond. The current

price of Bond P and the price of Bond P in one year is:

P: P0 = $85(PVIFA7%,5) + $1,000(PVIF7%,5) = $1,061.50

P1 = $85(PVIFA7%,4) + $1,000(PVIF7%,4) = $1,050.81

D: P0 = $55(PVIFA7%,5) + $1,000(PVIF7%,5) = $938.50

P1 = $55(PVIFA7%,4) + $1,000(PVIF7%,4) = $949.19

Current yield = $55 / $938.50 = .0586, or 5.86%

Capital gains yield = ($949.19 – 938.50) / $938.50 = +.0114, or +1.14%

35. a. The rate of return you expect to earn if you purchase a bond and hold it until maturity is the YTM.

The bond price equation for this bond is:

P0 = $875 = $70(PVIFAR%,10) + $1,000(PVIF R%,10)

b. To find our HPY, we need to find the price of the bond in two years. The price of the bond in two

years, at the new interest rate, will be:

P2 = $70(PVIFA7.94%,8) + $1,000(PVIF7.94%,8) = $945.70

Calculator Solutions

3.

Enter

9

8.4%

$70

$1,000

N

I/Y

PV

PMT

FV

Solve for

$913.98

Coupon rate = $56.95 / $1,000

Coupon rate = .0570, or 5.70%

6.

Enter

14 2

5.3% / 2

$61 / 2

$1,000

N

I/Y

PV

PMT

FV

Solve for

$1,078.37

7.

Enter

13 2

$54 / 2

$1,000

N

I/Y

PV

PMT

FV

Solve for

8.

Enter

10.5 2

6.2% / 2

±$945

$1,000

N

I/Y

PV

PMT

FV

Solve for

$27.40

Annual coupon = $27.40 2

Annual coupon = $54.80

Coupon rate = $54.80 / $1,000

Coupon rate = .0548, or 5.48%

Enter

Solve for

4.

Enter

$1,000

N

I/Y

PV

PMT

FV

Solve for

5.

Enter

$1,000

N

I/Y

PV

PMT

FV

Solve for

16.

Enter

26

3.8% / 2

±$49 / 2

±$2,000

N

I/Y

PV

PMT

FV

Solve for

$2,224.04

Enter

12

7% / 2

$42.50

$1,000

N

I/Y

PV

PMT

FV

Solve for

$1,120.44

Enter

10

7% / 2

$42.50

$1,000

N

I/Y

PV

PMT

FV

Solve for

$1,106.59

Enter

7% / 2

$42.50

$1,000

N

I/Y

PV

PMT

FV

Solve for

$1,062.37

Enter

7% / 2

$42.50

$1,000

N

I/Y

PV

PMT

FV

Solve for

$1,014.25

Bond Y

Enter

13

8.5% / 2

$35

$1,000

N

I/Y

PV

PMT

FV

Solve for

$883.33

Enter

12

8.5% / 2

$35

$1,000

N

I/Y

PV

PMT

FV

Solve for

$888.52

Enter

10

8.5% / 2

$35

$1,000

N

I/Y

PV

PMT

FV

Solve for

$900.29

17.

Enter

32

3.9% / 2

±$5,000

N

I/Y

PV

PMT

FV

Solve for

$4,881.80

18.

Bond X

Enter

13

7% / 2

$42.50

$1,000

N

I/Y

PV

PMT

FV

Solve for

$1,126.68

Enter

5

8.5% / 2

$35

$1,000

N

I/Y

PV

PMT

FV

Solve for

$939.92

19. If both bonds sell at par, the initial YTM on both bonds is the coupon rate, 6.2 percent. If the YTM

suddenly rises to 8.2 percent:

PBill

Enter

5× 2

8.2% / 2

$62 / 2

$1,000

N

I/Y

PV

PMT

FV

Solve for

$919.29

PTed

Enter

8.2% / 2

$62 / 2

$1,000

N

I/Y

PV

PMT

FV

Solve for

$788.81

If the YTM suddenly falls to 4.2 percent:

PBill

Enter

5 × 2

4.2% / 2

$62 / 2

$1,000

N

I/Y

PV

PMT

FV

Solve for

$1,089.36

PTed

Enter

25 × 2

4.2% / 2

$62 / 2

$1,000

N

I/Y

PV

PMT

FV

Solve for

20. Initially, at a YTM of 8 percent, the prices of the two bonds are:

PJ

Enter

13 × 2

4%

$40 / 2

$1,000

N

I/Y

PV

PMT

FV

Solve for

$680.34

Enter

1

8.5% / 2

$35

$1,000

N

I/Y

PV

PMT

FV

Solve for

$985.90

PS

Enter

13 × 2

4%

$140 / 2

$1,000

N

I/Y

PV

PMT

FV

Solve for

$1,479.48

If the YTM rises from 8 percent to 10 percent:

N

I/Y

PV

PMT

FV

Solve for

$1,287.50

PJ% = ($568.74 – 680.34) / $680.34 = –16.40%

PS% = ($1,287.50 – 1,479.48) / $1,479.48 = –12.98%

If the YTM declines from 8 percent to 6 percent:

PJ

Enter

13 × 2

3%

$40 / 2

$1,000

N

I/Y

PV

PMT

FV

Solve for

$821.23

PS

Enter

13 × 2

3%

$140 / 2

$1,000

N

I/Y

PV

PMT

FV

Solve for

21.

Enter

22 2

±$970

$63 / 2

$1,000

N

I/Y

PV

PMT

FV

Solve for

3.280%

YTM = 2 3.280%

YTM = 6.56%

Enter

13 × 2

5%

$40 / 2

$1,000

N

I/Y

PV

PMT

FV

Solve for

$568.74

Enter

13 × 2

5%

$1,000

Effective annual yield:

Enter

6.56%

2

NOM

EFF

C/Y

Solve for

6.67%

22. The company should set the coupon rate on its new bonds equal to the required return; the required

return can be observed in the market by finding the YTM on outstanding bonds of the company.

25.

Enter

15 × 2

±$916.45

$85 / 2

$1,000

N

I/Y

PV

PMT

FV

Solve for

4.780%

Solve for

$262.53

N

I/Y

PV

PMT

FV

Solve for

$280.69

YTM = 2 4.780%

YTM = 9.56%

28.

Enter

11 × 2

±$1,043.850

$58.50 / 2

$1,000

N

I/Y

PV

PMT

FV

Solve for

2.659%

YTM = 2 2.659%

YTM = 5.32%

Solve for

2.537%

29.

Enter

20 × 2

3.87% / 2

$61.25 / 2

$1,000

N

I/Y

PV

PMT

FV

Solve for

$1,311.98

31.

Enter

4 × 2

±$1,923.06

$54

$2,000

N

I/Y

PV

PMT

FV

Solve for

3.254%

32.

Enter

5 × 2

N

I/Y

PV

PMT

FV

Solve for

Enter

±$1,894.70

$2,000

N

I/Y

PV

PMT

FV

Solve for

$61.99

YTM = 2 3.254%

YTM = 6.51%

Enter

2.18% / 2

N

I/Y

PV

PMT

FV

Solve for

34.

Bond P

P0

Enter

5

7%

$85

$1,000

N

I/Y

PV

PMT

FV

Solve for

$1,061.50

Bond D

P0

Enter

5

7%

$55

$1,000

N

I/Y

PV

PMT

FV

Solve for

$938.50

P1

Enter

4

7%

$55

$1,000

N

I/Y

PV

PMT

FV

Solve for

$949.19

35.

a.

Enter

10

±$875

$70

$1,000

N

I/Y

PV

PMT

FV

Solve for

8.94%

This is the rate of return you expect to earn on your investment when you purchase the bond.

Enter

4

7%

$85

$1,000

N

I/Y

PV

PMT

FV

Solve for

b.

Enter

8

7.94%

$70

$1,000

N

I/Y

PV

PMT

FV

Solve for

$945.70

Enter

Solve for