CHAPTER 6

Inventories

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

1. Discuss how to classify

and determine inventory.

1, 2, 3, 4, 5,

6

1

1

1, 2

1A

2. Apply inventory cost flow

methods and discuss their

financial effects.

7, 8, 9, 10,

11, 12, 19

2, 3, 4, 5

2

3, 4, 5, 6, 7,

8

2A, 3A, 4A,

5A, 6A, 7A

financial statements.

of inventory.

17, 18

inventory records.

*6. Describe the two methods

of estimating inventories.

22, 23, 24,

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time Allotted

(min.)

1A

Determine items and amounts to be recorded in inventory.

Moderate

15–20

2A

Determine cost of goods sold and ending inventory using

FIFO, LIFO, and average-cost with analysis.

Simple

30–40

3A

Determine cost of goods sold and ending inventory using

FIFO, LIFO, and average-cost with analysis.

Simple

30–40

4A

Compute ending inventory, prepare income statements, and

answer questions using FIFO and LIFO.

30–40

results.

periodic method; use cost flow assumption to justify price

increase.

7A

Compute ending inventory, prepare income statements, and

answer questions using FIFO and LIFO.

30–40

LIFO, FIFO, and moving-average cost under the perpetual

system; compare gross profit under each assumption.

system.

Compute gross profit rate and inventory loss using gross

profit method.

30–40

Compute ending inventory using retail method.

Moderate

20–30

WEYGANDT FINANCIAL AND MANAGERIAL ACCOUNTING 2E

CHAPTER 6

INVENTORIES

Number

LO

BT

Difficulty

Time (min.)

BE1

1

C

Simple

4–6

BE2

2

K

Simple

2–4

BE3

2

AP

Simple

4–6

BE4

2

AP

Simple

2–4

EX1

1

AN

Simple

4–6

EX2

1

AN

Simple

6–8

EX3

2

AN, E

Moderate

6–8

EX4

2

AN, E

Simple

8–10

EX5

2

AP

Simple

6–8

EX6

2

AP

Simple

8–10

EX7

2

AP

Simple

8–10

EX8

2

AP

Simple

EX9

3

AP

Simple

EX10

3

AP

Simple

EX11

4

AN

Simple

EX12

4

AN

Simple

EX13

4

AP

Simple

EX14

4

AP

Simple

8–10

EX15

5

AP

Simple

8–10

BE5

2

AP

Simple

2–4

BE6

3

AP

Moderate

6–8

BE7

4

AP

Simple

4–6

BE8

4

AN

Simple

4–6

BE9

5

AP

Simple

4–6

BE10

6

AP

Simple

BE11

6

AP

Simple

4–6

DI1

1

AN

Simple

4–6

DI2

2

AP

Simple

6–8

DI3

3

AP

Simple

6–8

DI4

4

AP

Simple

4–6

INVENTORIES (Continued)

Number

LO

BT

Difficulty

Time (min.)

EX17

5

AP, E

Moderate

12–15

EX18

6

AP

Simple

8–10

EX19

6

AP

Simple

10–12

EX20

6

AP

Moderate

10–12

P1A

1

AN

Moderate

15–20

P2A

2

AP

Simple

30–40

P3A

2

AP

Simple

30–40

P4A

2

AN

Moderate

30–40

P5A

2

AP, E

Moderate

30–40

P6A

2

AP, E

Moderate

20–30

P7A

2

AN

Moderate

30–40

P8A

5

AP, E

Moderate

30–40

P9A

5

AP

Moderate

40–50

P10A

6

AP

Moderate

30–40

P11A

6

AP

Moderate

20–30

AP

Simple

10–15

4

10–15

4

Simple

10–15

AN

Simple

10–15

6

AP

Moderate

20–25

3

AN

Simple

10–15

2

Simple

10–15

3

Simple

10–15

AP

Simple

10–15

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

1. Discuss how to classify and determine

inventory.

Q6-2

Q6-6

Q6-1

Q6-3

Q6-4

BE6-1

Q6-5

E6-1

DI6-1

E6-1

E6-2

P6–1A

2. Apply inventory cost flow methods

and discuss their financial effects.

Q6-8

Q6–10

Q6–19

BE6-2

BE6-5

Q6-7

Q6-9

Q6–11

Q6–12

BE6-3

BE6-4

BE6-5

BE6-6

DI6-2

E6–5

E6-6

E6-7

E6-8

P6–2A

P6–3A

P6–5A

P6–6A

E6-3

E6-4

P6–4A

P6–7A

E6-3

E6-4

P6–5A

E6-9

E6–10

Q6–16

BE6-8

4. Explain the statement presentation

and analysis of inventory.

Q6–13

Q6–17

Q6–14 BE6-9

BE6-7 E6–13

Q6–18 E6–11

BE6-9 E6–12

Q6–25

E6–19

E6–20

P6-10A

ANSWERS TO QUESTIONS

1. Agree. Effective inventory management is frequently the key to successful business operations.

5. Inventoriable costs are $3,020 (invoice cost $3,000 + freight charges $50 – purchase discounts $30).

Questions Chapter 6 (Continued)

13. Josh should know the following:

*21. In a periodic system, the average is a weighted average based on total goods available for sale for the

Questions Chapter 6 (Continued)

*24. The estimated cost of the ending inventory is $40,000:

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 6-1

BRIEF EXERCISE 6-2

BRIEF EXERCISE 6-3

BRIEF EXERCISE 6-4

Average unit cost is $6.89 computed as follows:

BRIEF EXERCISE 6-5

BRIEF EXERCISE 6-6

BRIEF EXERCISE 6-7

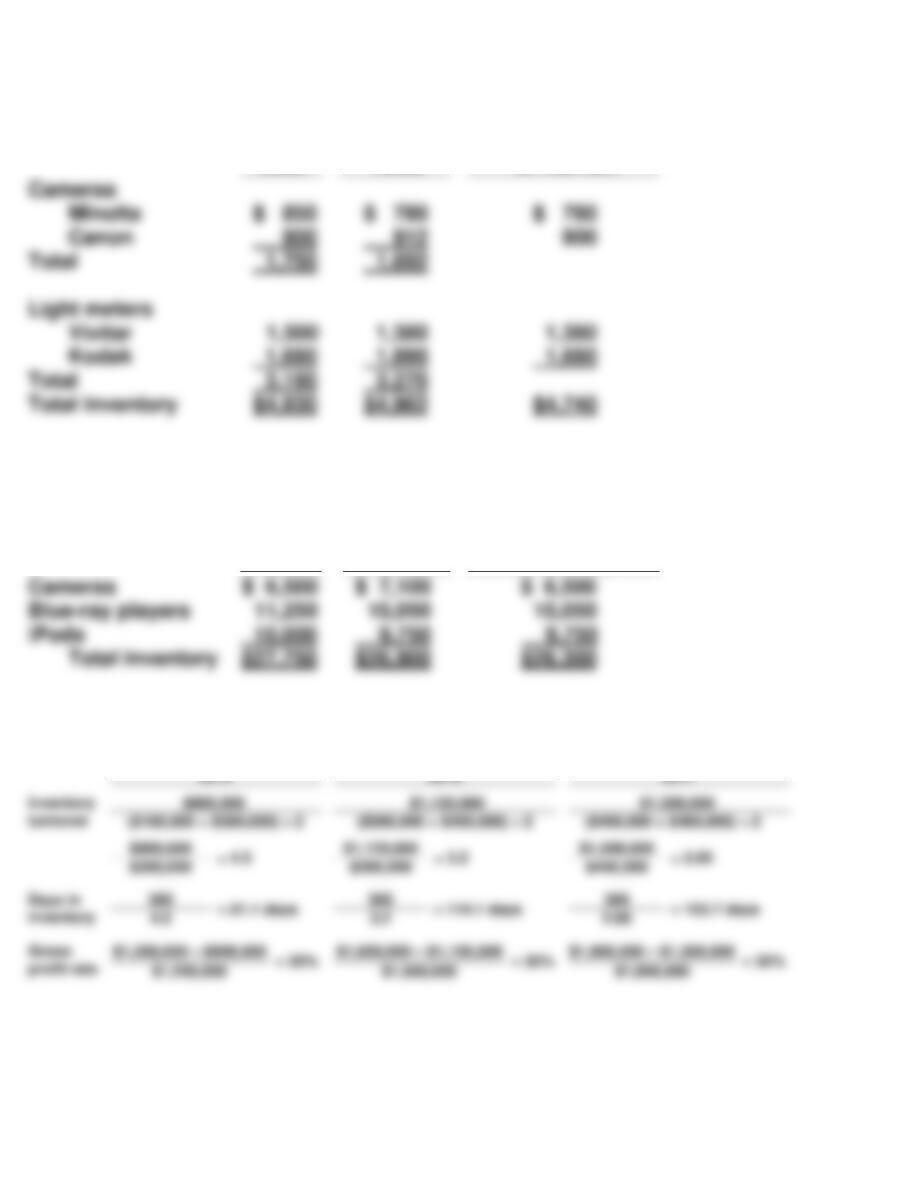

Inventory Categories

Cost

Market

LCM

Camcorders

Total valuation

BRIEF EXERCISE 6-8

*BRIEF EXERCISE 6-9

(a) FIFO Method

Product E2-D2

(b) LIFO Method

Product E2-D2

*BRIEF EXERCISE 6-9 (Continued)

(c) Average-Cost

Product E2-D2

*BRIEF EXERCISE 6-10

*BRIEF EXERCISE 6-11

At Cost

At Retail

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 6-1

DO IT! 6-2

DO IT! 6-3

DO IT! 6-4

DO IT! 6-4 (Continued)

(b)

SOLUTIONS TO EXERCISES

EXERCISE 6-1

EXERCISE 6-2

EXERCISE 6-2 (Continued)

EXERCISE 6-3

EXERCISE 6-4

EXERCISE 6-4 (Continued)

(b)

EXERCISE 6-5 (Continued)

Proof

Proof

EXERCISE 6-6

EXERCISE 6-6 (Continued)

EXERCISE 6-7

(a) (1) FIFO

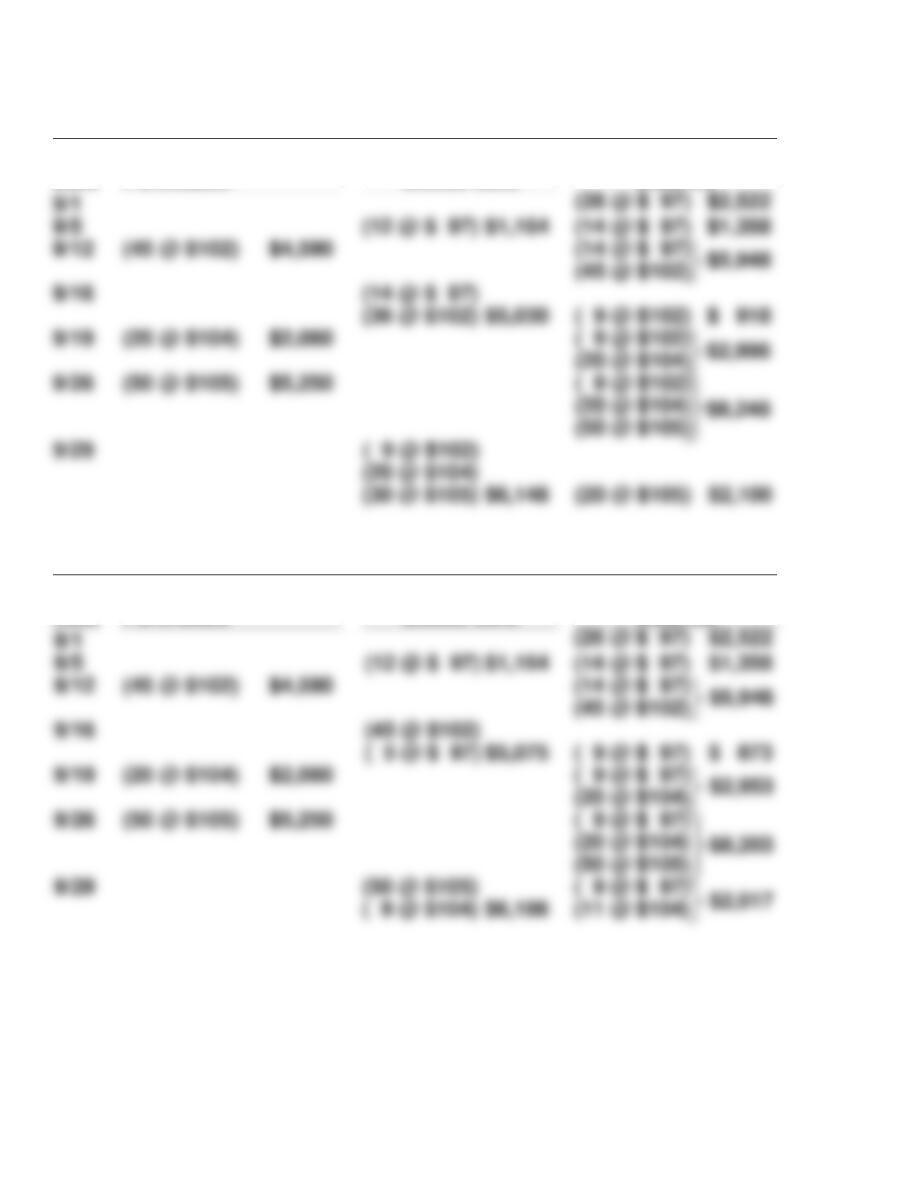

EXERCISE 6-8

EXERCISE 6-9

EXERCISE 6-10

(a)

2016

2017

EXERCISE 6-10 (Continued)

(b) The cumulative effect on total gross profit for the two years is zero as

shown below:

(c) Dear Mr./Ms. President:

EXERCISE 6-11

Cost

Market

Value

Lower-of-Cost

–or-Market:

EXERCISE 6-12

Cost

Market

Value

Lower-of-Cost

–or-Market:

EXERCISE 6-13

2015

2016

2017

EXERCISE 6-13 (Continued)

EXERCISE 6-14

*EXERCISE 6-15

(1)

FIFO

Date

Purchases

Cost of Goods Sold

Balance

Jan. 1

(3 @ $600)

(6 @ $660) $3,960

(1 @ $600)

(3 @ $660) $2,580

(3 @ $660)

*EXERCISE 6-15 (Continued)

(2)

LIFO

Date

Purchases

Cost of Goods Sold

Balance

Jan. 1

(3 @ $600)

$1,800

8

(2 @ $600) $1,200

(1 @ $600)

(6 @ $660) $3,960

(1 @ $600)

(6 @ $660)

(4 @ $660) $2,640

(1 @ $600)

(2 @ $660)

(3)

MOVING-AVERAGE COST

Date

Purchases

Cost of Goods Sold

Balance

Jan. 1

(3 @ $600) $1,800

8

(2 @ $600) $1,200

(1 @ $600) 600

(6 @ $660) $3,960

(7 @ $651.43)* 4,560

(4 @ $651.43) $2,606

(3 @ $651.43) 1,954

*EXERCISE 6-16

(a) The cost of goods available for sale is:

LIFO

Ending inventory: $500. Cost of goods sold: $5,500 – $500 = $5,000.

Moving-Average Cost

*EXERCISE 6-17

(a)

FIFO

Date

Purchases

Cost of

Goods Sold

Balance

LIFO

Date

Purchases

Cost of

Goods Sold

Balance

*EXERCISE 6-17 (Continued)

Moving-Average Cost

Cost of

(b)

Periodic

Perpetual

*EXERCISE 6-18

(12 @ $97) $1,164

(50 @ $100.81) $5,041*

(59 @ $104.27) $6,152*

*EXERCISE 6-18 (Continued)

*EXERCISE 6-19

(a) Net sales ($51,000 – $1,000) ………………………………………….. $50,000

(b) Net sales ……………………………………………………………………… $50,000

*EXERCISE 6-20

Women’s Shoes

Men’s Shoes

Cost

Retail

Cost

Retail

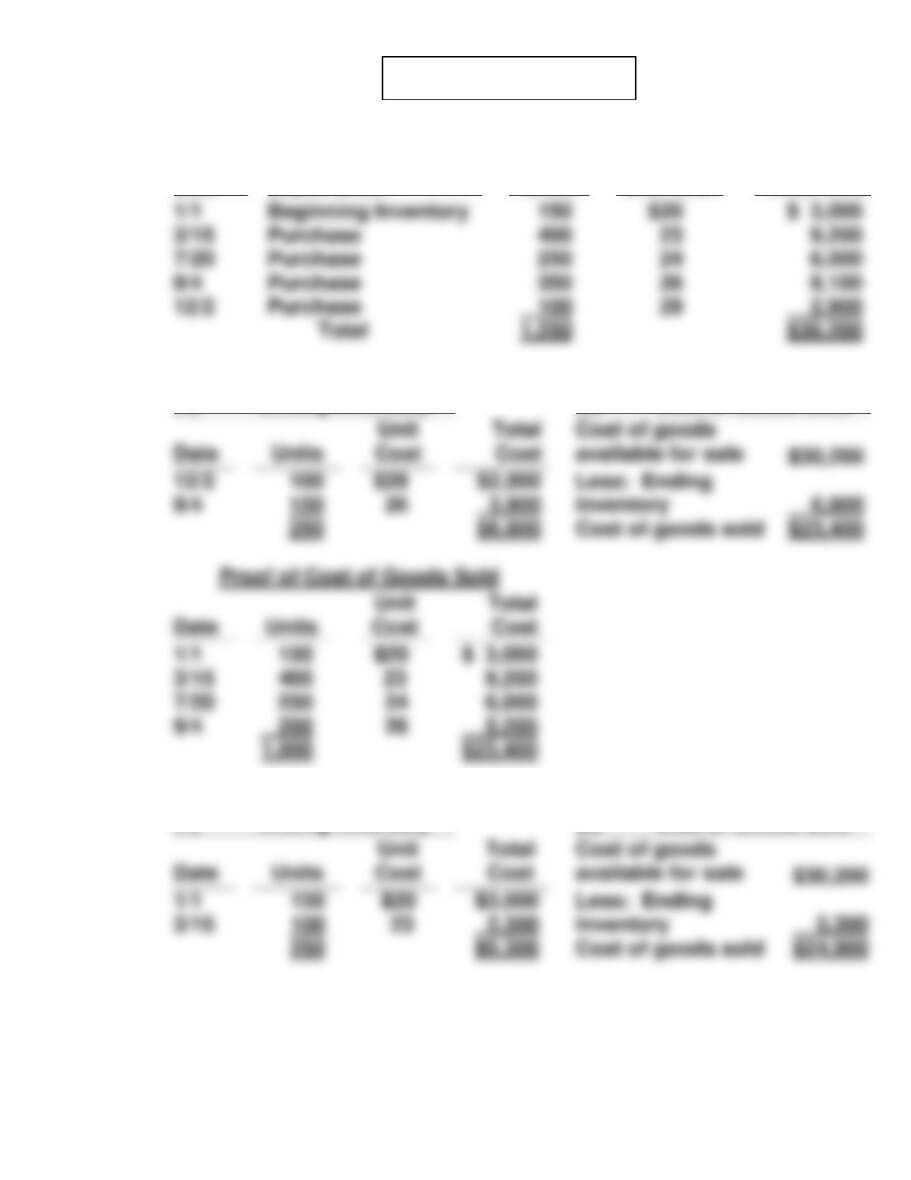

PROBLEM 6-1A

PROBLEM 6-2A

(a)

COST OF GOODS AVAILABLE FOR SALE

Date

Explanation

Units

Unit Cost

Total Cost

(b)

FIFO

(1)

Ending Inventory

(2)

Cost of Goods Sold

$11

inventory

1,000

Cost of goods sold

Unit Cost

8

9

LIFO

(1)

Ending Inventory

(2)

Cost of Goods Sold

$14,000

inventory

3

8

Cost of goods sold

Beginning Inventory

Purchase

Purchase

Purchase

Purchase

PROBLEM 6-2A (Continued)

Proof of Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

AVERAGE COST

(1)

Ending Inventory

(2)

Cost of Goods Sold

Total Cost

Oct. 25

$11

$ 44,000

9

9

PROBLEM 6-3A

(a)

COST OF GOODS AVAILABLE FOR SALE

Date

Explanation

Units

Unit Cost

Total Cost

(b)

FIFO

(1)

Ending Inventory

(2)

Cost of Goods Sold

12/2

$29

inventory

9/4

Cost of goods sold

Cost

1/1

3/15

7/20

9/4

LIFO

(1)

Ending Inventory

(2)

Cost of Goods Sold

1/1

inventory

3/15

Cost of goods sold

1/1

Beginning Inventory

3/15

Purchase

7/20

Purchase

9/4

Purchase

12/2

Purchase

PROBLEM 6-3A (Continued)

AVERAGE COST

(1)

Ending Inventory

(2)

Cost of Goods Sold

Cost of goods sold

(c) (1) FIFO results in the highest inventory amount, $6,800, as shown in

9/4

3/15

6,900

$24,900

PROBLEM 6-4A

(a) Felipe INC.

Condensed Income Statements

For the Year Ended December 31, 2017

(b) (1) The FIFO method produces the most meaningful inventory amount

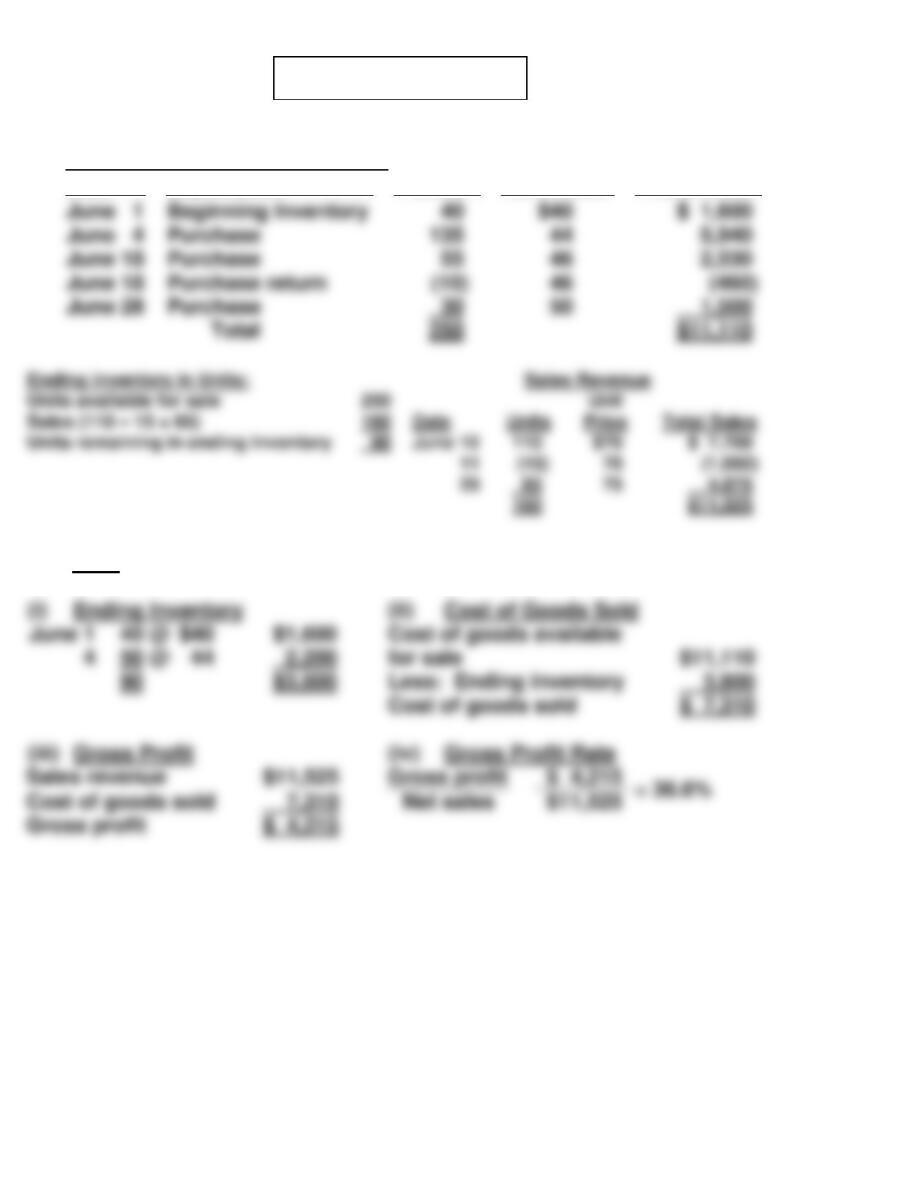

PROBLEM 6-5A

(a)

Cost of Goods Available for Sale

Date

Explanation

Units

Unit Cost

Total Cost

(1)

LIFO

(i)

Ending Inventory

(ii)

Cost of Goods Sold

for sale

$3,800

Less: Ending inventory

Cost of goods sold

(iii)

Gross Profit

(iv)

Gross Profit Rate

Sales revenue

Gross profit

Cost of goods sold

Gross profit

June 1

Beginning Inventory

$ 1,600

June 4

Purchase

5,940

June 18

Purchase

2,530

June 18

Purchase return

(460)

June 28

Purchase

1,500

PROBLEM 6-5A (Continued)

(2)

FIFO

(3)

Average-Cost

for sale

Cost of goods sold

45 @ $46

for sale

Sales revenue

Gross profit

Gross profit

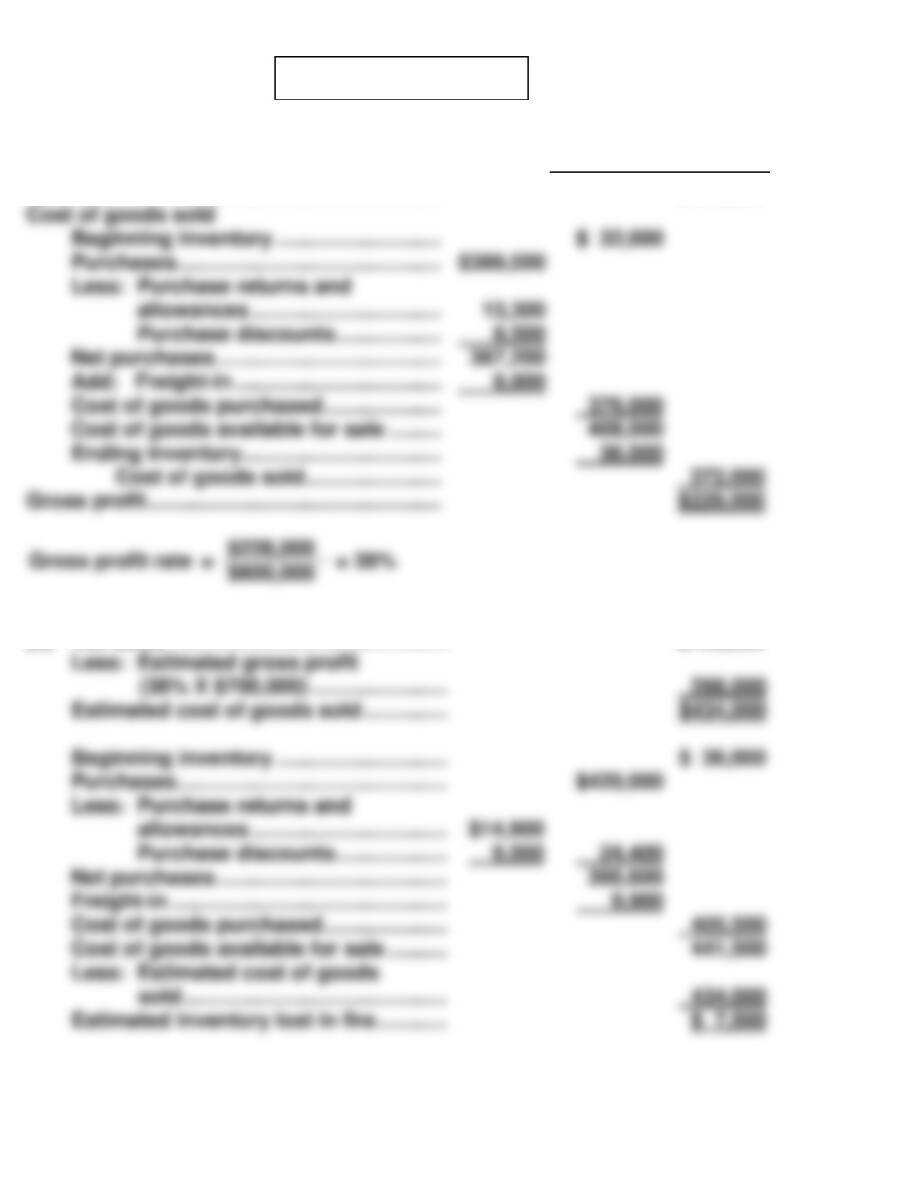

PROBLEM 6-6A

(a) Barton INC.

Income Statement (partial)

For the Year Ended December 31, 2017

FIFO ending inventory consists of:

3,500 liters

$2,175

(b) Companies can choose a cost flow method that produces the highest

PROBLEM 6-7A

(a) Sherlynn CO.

Condensed Income Statement

For the Year Ended December 31, 2017

(b) Answers to questions:

(1) The FIFO method produces the most meaningful inventory amount

*PROBLEM 6-8A

(a)

(1)

LIFO

Date

Purchases

Cost of Goods Sold

Balance

January 1

January 8

(110 @ $18) $1,980

*PROBLEM 6-8A (Continued)

(2)

FIFO

(3)

Moving-Average Cost

Date

Purchases

Cost of Goods Sold

Balance

January 1

(100 @ $15)

January 10

($ 168)

(140 @ $16.75)

January 20

(90 @ $17.605)

*PROBLEM 6-8A (Continued)

(b)

Gross profit:

LIFO

FIFO

Moving-Average Cost

Sales

$5,680

Gross profit

Ending inventory

*PROBLEM 6-9A

(a)

(1)

FIFO

(2)

MOVING-AVERAGE COST

Date

Purchases

Cost of Goods Sold

Balance

$ 600

(4 @ $120)

$ 952

(3 @ $134)

(6 @ $142)

(3)

LIFO

Purchases

$ 600

(4 @ $120)

$ 120

(5 @ $120)

(4 @ $120)

(7 @ $136)

(1 @ $120)

(2 @ $136)

(5 @ $136)

(1 @ $147)

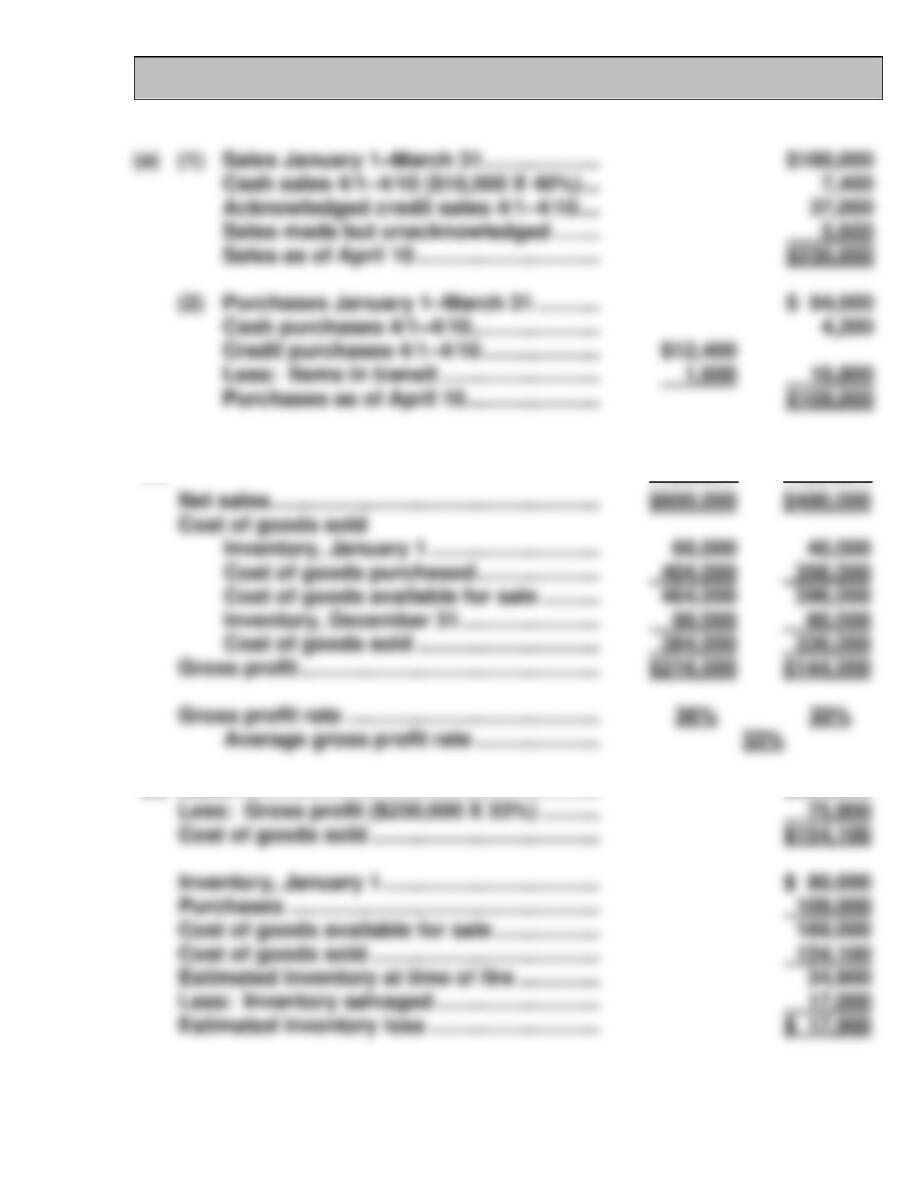

*PROBLEM 6-10A

(a)

November

Net sales ……………………………………………… $600,000

(b) Net sales ……………………………………….. $700,000

*PROBLEM 6-11A

(a)

Hardcovers

Paperbacks

Cost

Retail

Cost

Retail

COMPREHENSIVE PROBLEM SOLUTION

(a)

Dec. 3

Inventory (4,000 X $0.72) ………………………

2,880

Accounts Payable ………………………….

(1,400 X $0.72) …………………………….

Cost of Good Sold …………………………

Cash …………………………………………….

Inventory ………………………………………

COMPREHENSIVE PROBLEM SOLUTION (Continued)

(b) General Ledger

Cash

Accounts Receivable

COMPREHENSIVE PROBLEM SOLUTION (Continued)

(c) Matthias COMPANY

Adjusted Trial Balance

December 31, 2017

Less: Sales returns and allowances ……..

Net sales ……………………………………………..

Gross profit …………………………………………

Operating expenses

Depreciation expense …………………….

Net income…………………………………………..

(d) Matthias COMPANY

Income Statement

For the Month Ending December 31, 2017

Cash ……………………………………………………..

Inventory ……………………………………………….

Accounts Payable …………………………..……..

Salaries and Wages Payable …………………..

Retained Earnings ………………………………….

Sales Revenue ……………………………………….

Cost of Goods Sold ………………………………..

Salaries and Wages Expense ………………….

COMPREHENSIVE PROBLEM SOLUTION (Continued)

Matthias COMPANY

Balance Sheet

December 31, 2017

COMPREHENSIVE PROBLEM SOLUTION (Continued)

(e) FIFO Method

Units

Unit Cost

Cost of Goods

Available for Sales

(f) LIFO Method

Ending Inventory

Cost of Goods Sold

4,000

2,200

BYP 6-1 FINANCIAL REPORTING PROBLEM

(a)

September 28, 2013

September 29, 2012

Inventories

$1,764 million

$1,791 million

(d)

Apple (in millions)

2013

2012

2011

Cost of Goods Sold

BYP 6-2 COMPARATIVE ANALYSIS PROBLEM

(a) (1) Inventory turnover:

(2) Days in inventory:

BYP 6-3 COMPARATIVE ANALYSIS PROBLEM

(a) (1) Inventory turnover:

(2) Days in inventory:

BYP 6-4 REAL-WORLD FOCUS

The following responses are based on the 2013 annual report:

BYP 6-5 DECISION MAKING ACROSS THE ORGANIZATION

*(b)

2016

2015

*(c) Sales …………………………………………………….. $230,000

BYP 6-6 COMMUNICATION ACTIVITY

MEMO

To: Marta Johns, President

From: Student

Re: 2016 ending inventory error

BYP 6-7 ETHICS CASE

(a) The higher cost of the items ordered, received, and on hand at year–

BYP 6-8 ALL ABOUT YOU

Students responses to this question will vary depending on the inventory

BYP 6-9 FASB CODIFICATION ACTIVITY

(a) The primary basis of accounting for inventories is cost, which has

IFRS EXERCISES

IFRS6-1

Key Similarities are (1) the definitions for inventory are essentially the same,

IFRS6-2

Under IFRS, LaTour’s inventory turnover is computed as follows:

IFRS6-3 INTERNATIONAL FINANCIAL REPORTING PROBLEM

(a) Inventories are stated at the lower-of-cost-or-net realizable value, using

first-in-first out cost flow assumption.