6-96

P6A-37B, cont.

Requirement 1, cont.

FIFO Cost of Goods Sold:

Cost of Goods Available for Sale

$ 19,680

Ending Merchandise Inventory

(11,080)

Cost of Goods Sold

Cost of Goods Available for Sale

Ending Merchandise Inventory

(10,200)

Cost of Goods Sold

P6A-37B, cont.

Requirement 1, cont.

Weighted-average

cost per unit

=

$19,680 cost of goods available for sale

/ 240 units available for sale

=

$82 per unit

=

130 units × $82 per unit

=

$10,660

Cost of Goods Available for Sale

Ending Merchandise Inventory

(10,660)

Cost of Goods Sold

=

110 units sold × $82 per unit

=

$9,020

Requirement 2

Gross profit is $14,400 using FIFO, $13,520 using LIFO, and $13,980 using weighted-average.

Calculations:

Sales Revenue

Cost of Goods Sold *

Gross Profit

$ 14,400

Requirement 3

LIFO results in the lowest income taxes and FIFO results in the highest net income. Under LIFO, the

last costs into inventory are the first costs out to cost of goods sold. When inventory costs are rising,

LIFO results in the highest cost of goods sold; thus, the lowest gross profit, net income, and taxable

6-98

Continuing Problem

P6-38 Accounting for inventory using the perpetual inventory system—FIFO

This problem continues the Daniels Consulting situation from Problem P5-45

in Chapter 5. Consider the January transactions for Daniels Consulting that were presented in Chapter 5.

(Cost data have been removed from the sale transactions.) Daniels uses the perpetual inventory system.

Requirements

1. Prepare perpetual inventory records for January for Daniels using the FIFO inventory costing

method. (Note: You must calculate the cost of goods sold on the 18th, 28th, and 31st.)

2. Journalize the transactions for January 18th, 28th, and 31st (adjusting entry d only) using the

perpetual inventory record created in Requirement 1.

SOLUTION

Requirement 1

Perpetual Inventory Record: FIFO

Purchases

Cost of Goods Sold

Inventory on Hand

Date

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Jan. 7

50 units

× $ 22(a)

= $ 1,100(a)

50 units

× $ 22

= $ 1,100

18

× $ 22

= $ 880

10 units

× $ 22

= $ 220

22

= $ 4,810

10 units

× $ 22

= $ 220

185 units

× $ 26

= $ 4,810

28

10 units

× $ 22

= $ 220

60 units

× $ 26

= $ 1,560

31

× $ 26

= $ 260

50 units

× $ 26

= $ 1,300

Totals

50 units

6-100

P6-38, cont.

Requirement 1, cont.

Calculations:

Unit cost of inventory purchased

=

Total cost / Total number of units

=

($1,050 + $50 freight-in) / 50 units

=

$1,100 / 50 units

=

$22 per unit

=

$4,810 / 185 units

=

$26 per unit

50 units

per physical count

(60 units)

per inventory records

(10 units)

adjustment needed

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Jan. 18

Accounts Receivable

2,625

Sales Revenue

2,625

Sales on account.

Cost of Goods Sold

880 (e)

Software Inventory

880 (e)

Recorded the cost of goods sold.

5,265

Sales Revenue

Cash sales.

Cost of Goods Sold

Software Inventory

Recorded the cost of goods sold.

Cost of Goods Sold

Software Inventory

Adjustment for inventory shrinkage.

Practice Set

This problem continues the Crystal Clear Cleaning problem begun in Chapter 2 and continued through

Chapter 5.

P6-39 Accounting for inventory using the perpetual inventory system—FIFO

Consider the December transactions for Crystal Clear Cleaning that were presented in Chapter 5. (Cost

data have been removed from the sale transactions.) Crystal Clear uses the perpetual inventory system.

Requirements

1. Prepare perpetual inventory records for December for Crystal Clear Cleaning using the FIFO

inventory costing method. (Note: You must calculate the cost of goods sold on the 11th, 28th, and

31st.)

2. Journalize the transactions for December 11th, 28th, and 31st (adjusting entry a only) using the

perpetual inventory record created in Requirement 1.

6-102

SOLUTION

Requirement 1

Perpetual Inventory Record: FIFO

Purchases

Cost of Goods Sold

Inventory on Hand

Date

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Dec. 2

475 units

× $ 6.00(a)

= $ 2,850

475 units

× $ 6.00

= $ 2,850

$ 2,850

= $ 4,500

× $ 6.00

= $ 2,850

× $ 6.00

= ($ 450)

× $ 6.00

= $ 2,400

× $ 6.00

= $ 2,400

(22 units)

× $ 6.00

× $ 6.00

= $ 132

× $ 6.00

= $ 132

= $ 3,472

× $ 5.37

× $ 7.355

= $ 324

428 units

× $ 7.355

= $ 3,148

P6-39, cont.

Requirement 1, cont.

Calculations:

Unit cost of inventory purchased

=

Total cost / Total number of units

(a) Dec. 2 purchase:

=

$2,850 / 475 units

=

$6.00 per unit

(b) Dec. 5 purchase:

=

$4,500 / 600 units

=

$7.50 per unit

December 9:

=

$4,350

× 0.02 percentage purchase discount

=

$87

=

$4,413

=

$7.355 per unit

P6-39, cont.

Requirement 1, cont.

December 12:

Amount due,

net of purchase return

=

$2,850 cost of 475 units – $450 cost of 75 units returned

=

$2,400

× 0.03 percentage purchase discount

=

$72

=

$618

=

$5.37 per unit

per physical count

per inventory records

Adjustment needed

P6-39, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Dec. 11

Accounts Receivable

3,990

Sales Revenue

3,990

Sales on account.

Cost of Goods Sold

Merchandise Inventory

Recorded the cost of goods sold.

28

Cash

Sales Revenue

Cash sale.

Cost of Goods Sold

Merchandise Inventory

Recorded the cost of goods sold.

31

Cost of Goods Sold

Merchandise Inventory

Adjustment for inventory shrinkage.

6-106

Critical Thinking

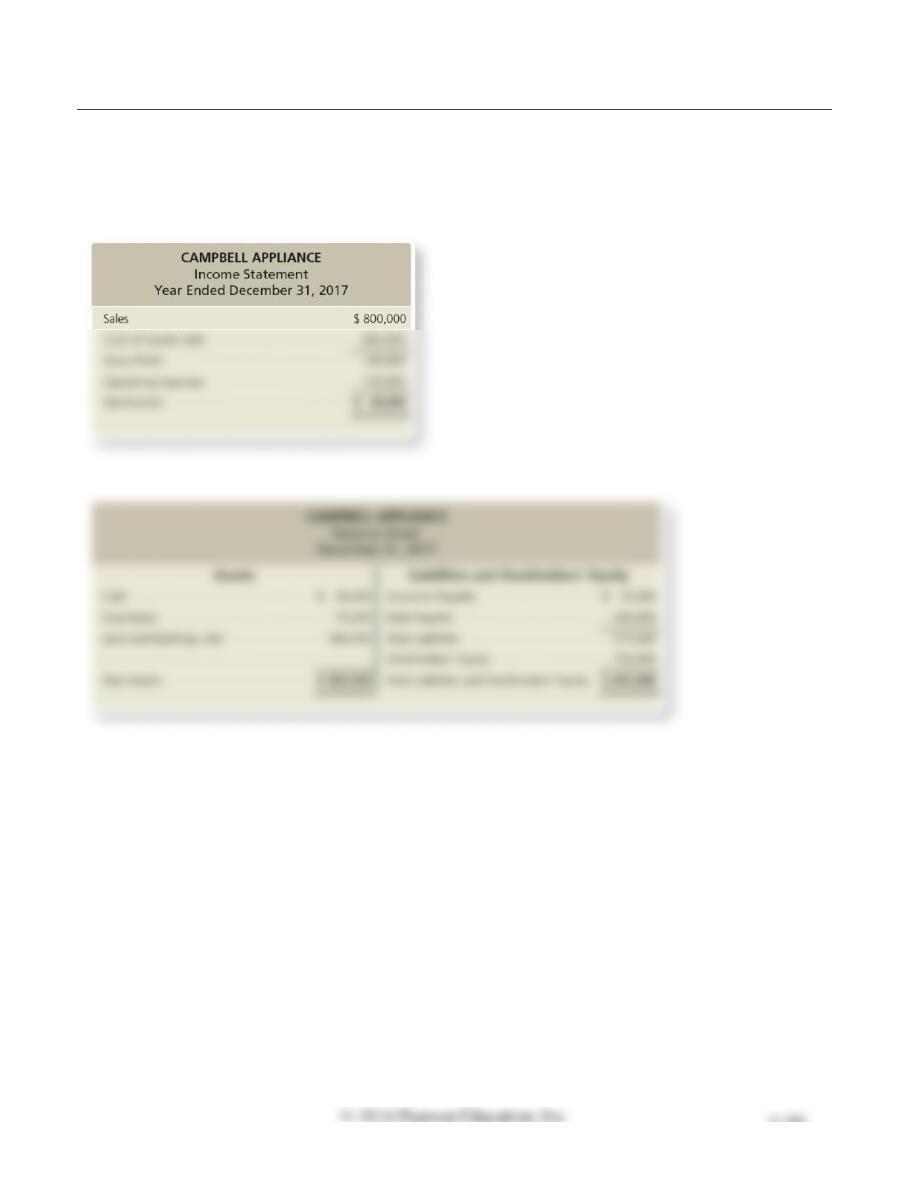

Decision Case 6-1

Suppose you manage Campbell Appliance. The store’s summarized financial state– ments for 2017, the

most recent year, follow:

Assume that you need to double net income. To accomplish your goal, it will be very difficult to raise

the prices you charge because there is a discount appliance store nearby. Also, you have little control

over your cost of goods sold because the appliance manufacturers set the amount you must pay.

Identify several strategies for doubling net income.

SOLUTION

Strategies for doubling net income include the following:

• Analyze the mix and level of operating expenses to identify opportunities to increase efficiencies

Fraud Case 6-1

Ever since he was a kid, Carl Montague wanted to be a pro football player. When that didn’t work out,

he found another way to channel his natural competitive spirit: He bought a small auto parts store in

Kentucky that was deep in red ink (negative earnings). At the end of the year, he created “ghost”

inventory by recording fake inventory purchases. He offset these transactions by “adjustments” to Cost

of Goods Sold, thereby boosting profit and strengthening the balance sheet. Fortified with great

financials, he got bank loans that allowed him to build up a regional chain of stores, buy a local sports

franchise, and take on the lifestyle of a celebrity. When the economy in the region tanked, he could no

longer cover his losses with new debt or equity infusions, and the whole empire fell like a house of

cards.

Requirements

1. Name several parties that could have been hurt by the actions of Carl Montague.

2. What kind of adjustment to Cost of Goods Sold (debit or credit) would have the effect of boosting

earnings?

SOLUTION

Requirement 1

Parties that could have been hurt by the actions of Carl Montague include creditors who weren’t paid

Requirement 2

6-108

Financial Statement Case 6-1

The notes are an important part of a company’s financial statements, giving valuable details that would

Requirements

1. Which inventory costing method does Starbucks use? How does Starbucks value its inventories? See

Note 1.

2. By using the cost of goods sold formula, you can compute net purchases, which are not reported in

the Starbucks statements. How much were Starbucks’s inventory purchases during the year ended

September 29, 2013?

3. Determine Starbucks’s inventory turnover and days’ sales in inventory for the year ended September

29, 2013. (Round each ratio to one decimal place.) How do Starbucks’s inventory turnover and days’

sales in inventory compare with Green Mountain Coffee Roasters, Inc.’s for the year ended

September 28, 2013? Explain.

SOLUTION

Requirement 1

Requirement 2

Starbucks’s net purchases of inventory were $6,252 (in millions) during the year ended September 29,

2013.

Calculations:

Financial Statement Case 6-1, cont.

Requirement 3

For the fiscal year ended September 28, 2013, Green Mountain Coffee Roasters had an inventory

turnover of 3.79 times and days’ sales in inventory of 96.3 days.

For the fiscal year ended September 29, 2013, Starbucks’ inventory turnover is 5.4 times, and days’

sales in inventory is 67.6 days.

Team Project 6-1

Obtain the annual reports of as many companies as you have team members—one company per team

member. Most companies post their financial statements on their Web sites.

Requirements

1. Identify the inventory method used by each company.

2. Compute each company’s gross profit percentage, inventory turnover, and days’ sales in inventory

for the most recent two years.

3. For the industries of the companies you are analyzing, obtain the industry averages for gross profit

percentage and inventory turnover from Robert Morris Associates, Annual Statement Studies; Dun

and Bradstreet, Industry Norms and Key Business Ratios; or Leo Troy, Almanac of Business and

Industrial Financial Ratios.

4. How well does each of your companies compare with the average for its industry? What insight

about your companies can you glean from these ratios?

SOLUTION