P6-28A, cont.

Requirement 2

Using LIFO, cost of goods sold is $28,080, ending merchandise inventory is $2,655, and gross profit is $6,530.

Perpetual Inventory Record: LIFO

Purchases

Cost of Goods Sold

Inventory on Hand

Date

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Jan. 1

65 units

× $ 59 (b)

= $ 3,835

145 units

× $ 80

= $ 11,600

65 units

× $ 59

= $ 3,835

145 units

× $ 80

145 units

× $ 80

= $ 11,600

50 units

× $ 59

= $ 2,950

15 units

× $ 59

170 units

× $ 90

= $ 15,300

50 units

× $ 59

= $ 2,950

170 units

× $ 90

= $ 15,300

45 units

× $ 59

= $ 2,655

5 units

= $ 295

315 units

$ 26,900

335 units

$ 28,080

45 units

Gross Profit

6-62

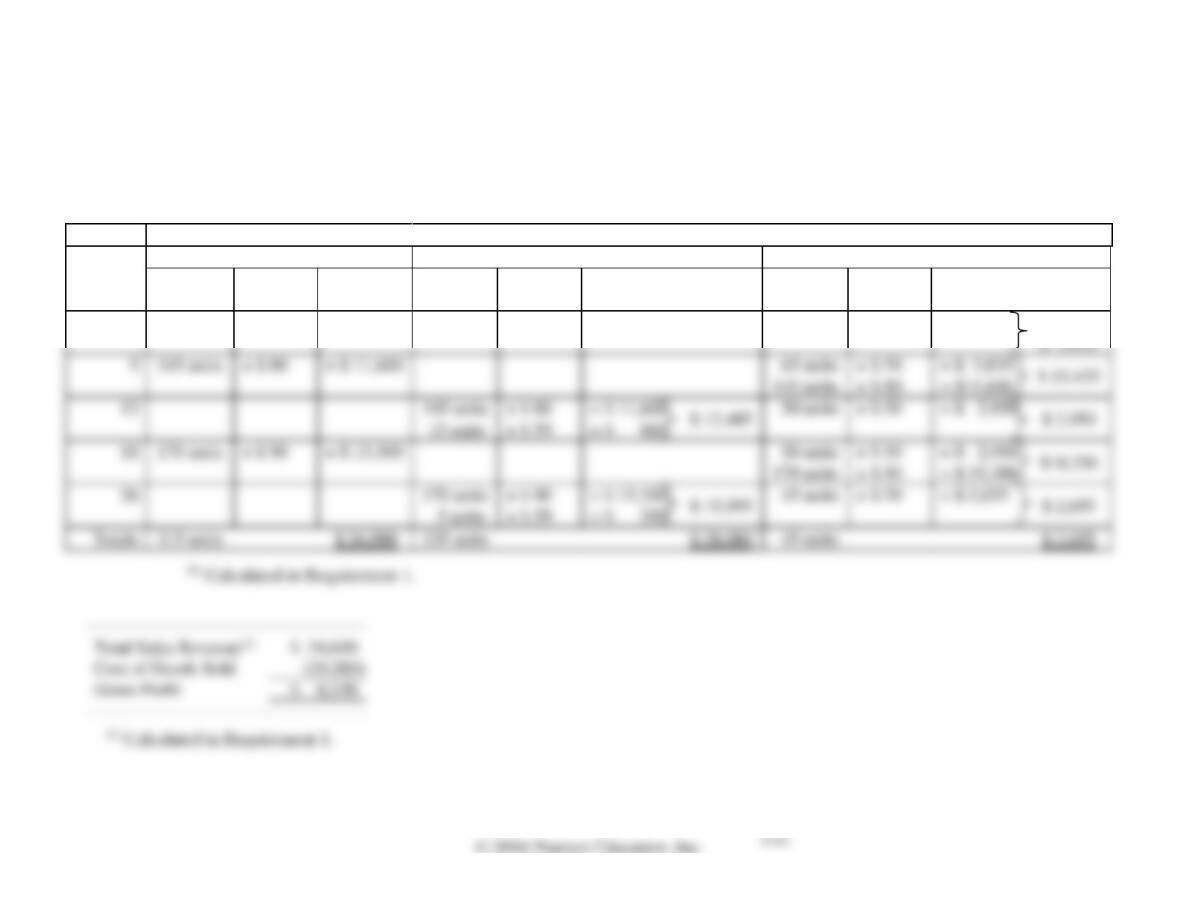

P6-28A, cont.

Requirement 3

Using weighted-average, cost of goods sold is $26,854, ending merchandise inventory is $3,881, and gross profit is $7,756.

Perpetual Inventory Record: Weighted-Average

Purchases

Cost of Goods Sold

Inventory on Hand

Date

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

65 units

= $ 3,835

145 units

× $ 80

= $ 11,600

210 units

= $ 15,435

160 units

× $73.50

= $ 11,760

50 units

× $ 73.50

= $ 3,675

170 units

× $ 90

= $ 15,300

220 units

= $ 18,975

175 units

× $86.25

= $ 15,094

45 units

× $ 86.25

= $ 3,881

315 units

$ 26,900

335 units

$ 26,854

45 units

$ 3,881

=

Cost of goods available for sale / Number of units available

=

=

$15,435 / 210 units

=

$73.50 per unit

=

($3,675 + $15,300) ÷ (50 units + 170 units)

=

$18,975 / 220 units

=

$86.25 per unit

P6-28A, cont.

Requirement 3, cont.

Requirement 4

If the business wanted to pay the least amount of income taxes possible, they would choose LIFO.

P6-29A Accounting for inventory using the perpetual inventory system—FIFO, LIFO, and

weighted-average, and comparing FIFO, LIFO, and weighted-average

Learning Objectives 2, 3

5. FIFO GP $4,850

Iron Man began August with 65 units of iron inventory that cost $30 each. During

August, the company completed the following inventory transactions:

Requirements

1. Prepare a perpetual inventory record for the merchandise inventory using the FIFO inventory costing

method.

6-64

SOLUTION

Requirement 1

Perpetual Inventory Record: FIFO

Purchases

Cost of Goods Sold

Inventory on Hand

Date

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Aug. 1

65 units

× $ 30

= $ 1,950

$ 1,950

× $ 30

= $ 1,500

× $ 30

= $ 450

85 units

× $ 50

= $ 4,250

× $ 30

× $ 50

= $ 4,250

× $ 30

= $ 450

× $ 50

= $ 1,000

= $ 900

130 units

$ 1,900

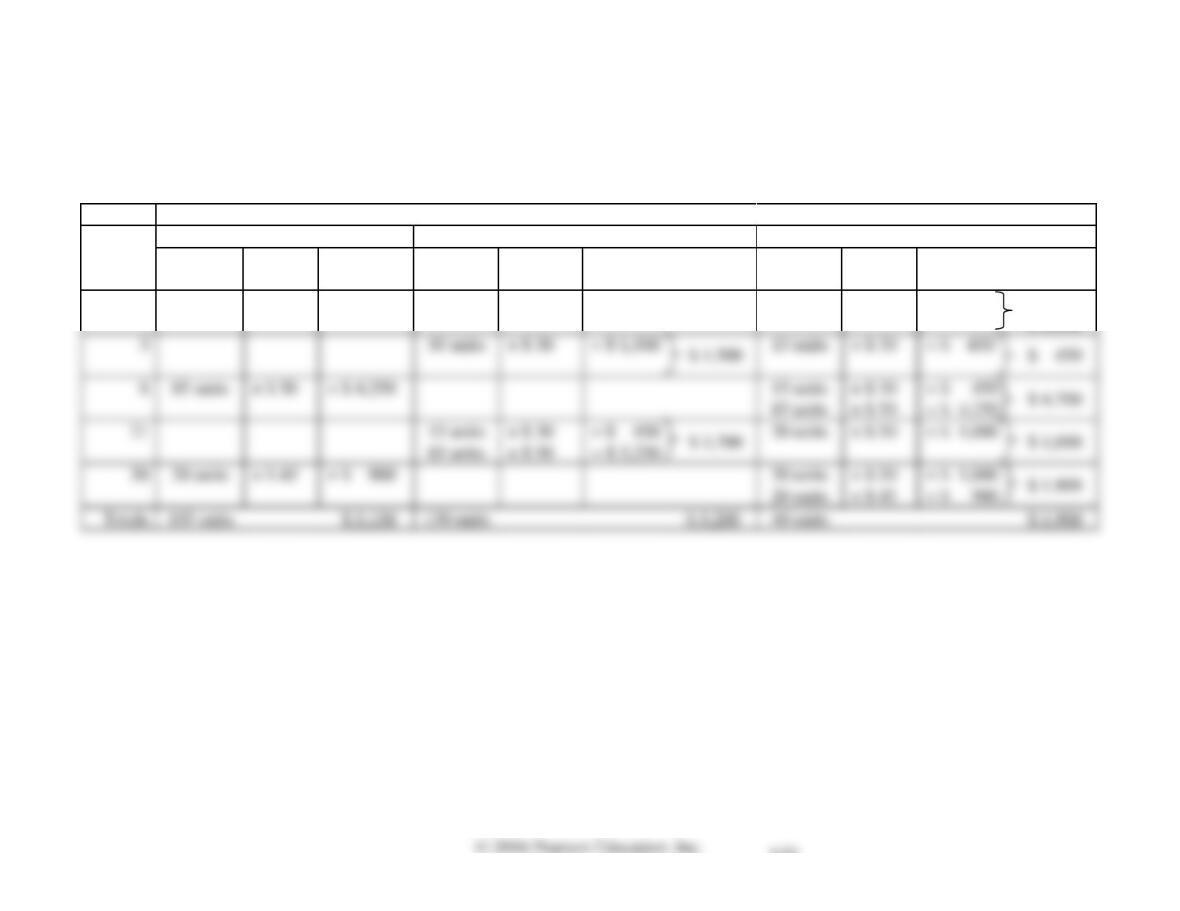

P6-29A, cont.

Requirement 2

Perpetual Inventory Record: LIFO

Purchases

Cost of Goods Sold

Inventory on Hand

Date

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Aug. 1

65 units

× $ 30

= $ 1,950

× $ 30

= $ 1,500

× $ 30

= $ 450

× $ 50

= $ 4,250

× $ 30

= $ 450

= $ 4,250

21

× $ 50

= $ 4,000

× $ 30

= $ 450

30

× $ 45

= $ 900

× $ 30

= $ 450

× $ 50

= $ 250

× $ 45

= $ 900

130 units

6-66

P6-29A, cont.

Requirement 3

Perpetual Inventory Record: Weighted-Average

Purchases

Cost of Goods Sold

Inventory on Hand

Date

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Aug. 1

65 units

× $ 30

= $ 1,950

3

× $30

= $ 1,500

× $ 30

= $ 450

8

× $ 50

= $ 4,250

100 units

= $ 4,700

× $47

= $ 3,760

20 units

× $ 47

= $ 940

× $ 45

= $ 900

40 units

= $ 1,840

105 units

$ 5,150

130 units

$ 5,260

40 units

$ 1,840

=

Cost of goods available for sale / Number of units available

=

=

$4,700 / 100 units

=

$47 per unit

=

=

$1,840 / 40 units

=

$46 per unit

P6-29A, cont.

Requirement 4

Requirement 5

Gross profit is $4,850 using FIFO, $4,550 using LIFO, and $4,790 using weighted-average.

Calculations:

Requirement 6

6-68

P6-30A Accounting principles for inventory and applying the lower-of-cost- or-market rule

Learning Objectives 1, 4

3. CoGS $420,000

Some of E and S Electronics’s merchandise is gathering dust. It is now December 31, 2016, and the

current replacement cost of the ending merchandise inventory is $20,000 below the business’s cost of

the goods, which was $105,000. Before any adjustments at the end of the period, the company’s Cost of

Goods Sold account has a balance of $400,000.

Requirements

1. Journalize any required entries.

2. At what amount should the company report merchandise inventory on the balance sheet?

3. At what amount should the company report cost of goods sold on the income statement?

4. Which accounting principle or concept is most relevant to this situation?

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Dec. 31

Cost of Goods Sold

20,000

Requirement 2

Merchandise inventory should be reported at $85,000 on the balance sheet.

Requirement 3

Cost of goods sold should be reported at $420,000 on the income statement.

P6-31A Correcting inventory errors over a three-year period and computing inventory turnover

and days’ sales in inventory

Learning Objectives 5, 6

2. 2017, overstated $7,000

Lake Air Carpets’s books show the following data. In early 2018, auditors found that the ending

merchandise inventory for 2015 was understated by $6,000 and that the ending merchandise inventory

for 2017 was overstated by $7,000. The ending merchandise inventory at December 31, 2016, was

correct.

Requirements

1. Prepare corrected income statements for the three years.

2. State whether each year’s net income—before your corrections—is understated or overstated, and

indicate the amount of the understatement or overstatement.

6-70

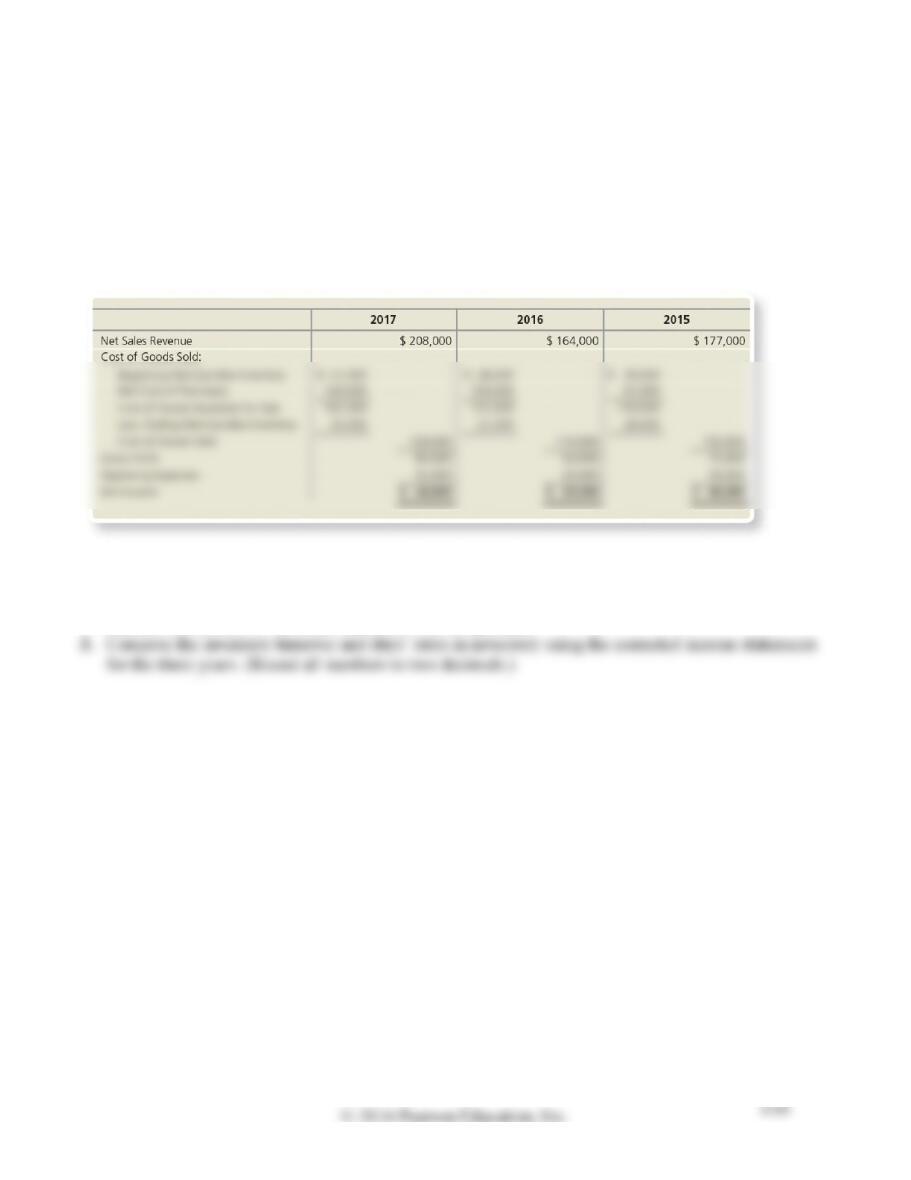

SOLUTION

Requirement 1

Corrected income statements:

LAKE AIR CARPETS

Income Statements

Years Ended December 31,

2017, 2016, and 2015

2017

2016

2015

Net Sales Revenue

Cost of Goods Sold:

$ 21,000

$ 39,000

140,000

103,000

91,000

161,000

137,000

130,000

21,000

Gross Profit

Operating Expenses

35,000

Net Income

2017

2015

Incorrect Merchandise Inventory

$ 33,000

$ 28,000

Understatement (Overstatement)

(7,000)

6,000

Correct Merchandise Inventory

P6-31A, cont.

Requirement 2

Before correction, net income is overstated by $7,000 in 2017, overstated by $6,000 in 2016, and

understated by $6,000 in 2015.

Calculations:

2017

2016

2015

$ 21,000

$ 23,000

$ 46,000

Incorrect Net Income

(28,000)

(29,000)

(40,000)

Understatement (Overstatement)

$( 7,000)

$( 6,000)

$ 6,000

Requirement 3

Inventory turnover is 5.74 times in 2017, 4.22 times in 2016, and 2.63 in 2015. Days’ sales in inventory

is 63.59 days in 2017, 86.49 days in 2016, and 138.78 days in 2015.

Calculations:

Average merchandise inventory

=

(Beginning merchandise inventory

+ Ending merchandise inventory) / 2

Year Ended Dec. 31, 2017:

=

($21,000 + $26,000) / 2

=

$23,500

Year Ended Dec. 31, 2016:

=

($34,000 + $21,000) / 2

=

$27,500

Year Ended Dec. 31, 2015:

6-72

P6-31A, cont.

Requirement 3, cont.

Inventory turnover

=

Cost of goods sold

/ Average merchandise inventory

Year Ended Dec. 31, 2017:

=

$135,000 / $23,500

=

5.74 times for the year

Year Ended Dec. 31, 2016:

=

$116,000 / $27,500

=

4.22 times for the year

Year Ended Dec. 31, 2015:

$96,000 / $36,500

2.63 times for the year

=

365 days / Inventory turnover

Year Ended Dec. 31, 2017:

=

365 days / 5.74 times

=

63.59 days

Year Ended Dec. 31, 2016:

=

365 days / 4.22 times

=

86.49 days

Year Ended Dec. 31, 2015:

365 days / 2.63 times

138.78 days

P6A-32A Accounting for inventory using the periodic inventory system— FIFO, LIFO, and

weighted-average, and comparing FIFO, LIFO, and weighted-average

Learning Objectives 3, 7

Appendix 6A

1. LIFO Ending Merch. Inv., $7,800

Jepson uses the periodic inventory system, and the physical count at October 31 indicates that 110 units

of merchandise inventory are on hand.

Requirements

1. Determine the ending merchandise inventory and cost of goods sold amounts for the October

financial statements using the FIFO, LIFO, and weighted-average inventory costing methods.

6-74

SOLUTION

Requirement 1

Using FIFO, ending merchandise inventory is $8,910 and cost of goods sold is $7,050.

P6A-32A, cont.

Requirement 1, cont.

FIFO Cost of Goods Sold:

Cost of Goods Available for Sale

$ 15,960

Ending Merchandise Inventory

(8,910)

Cost of Goods Sold

Cost of Goods Available for Sale

$ 15,960

Ending Merchandise Inventory

(7,800)

Cost of Goods Sold

6-76

P6A-32A, cont.

Requirement 1, cont.

Weighted-average

cost per unit

=

15,960 cost of goods available for sale

/ 210 units available for sale

=

$76 per unit

Weighted-Average Ending

Merchandise Inventory

=

110 units × $76 per unit

=

$8,360

Cost of Goods Available for Sale

Ending Merchandise Inventory

(8,360)

Cost of Goods Sold

=

100 units sold × $76 per unit

=

$7,600

Requirement 2

Gross profit is $19,950 using FIFO, $18,840 using LIFO, and $19,400 using weighted-average.

Calculations:

FIFO

LIFO

Weighted-

Average

Sales Revenue

$ 27,000

$ 27,000

$ 27,000

Cost of Goods Sold *

Gross Profit

$ 19,950

$ 18,840

$ 19,400

Requirement 3

LIFO results in the lowest income taxes and FIFO results in the highest net income. Under LIFO, the

last costs into inventory are the first costs out to cost of goods sold. When inventory costs are rising,

Problems (Group B)

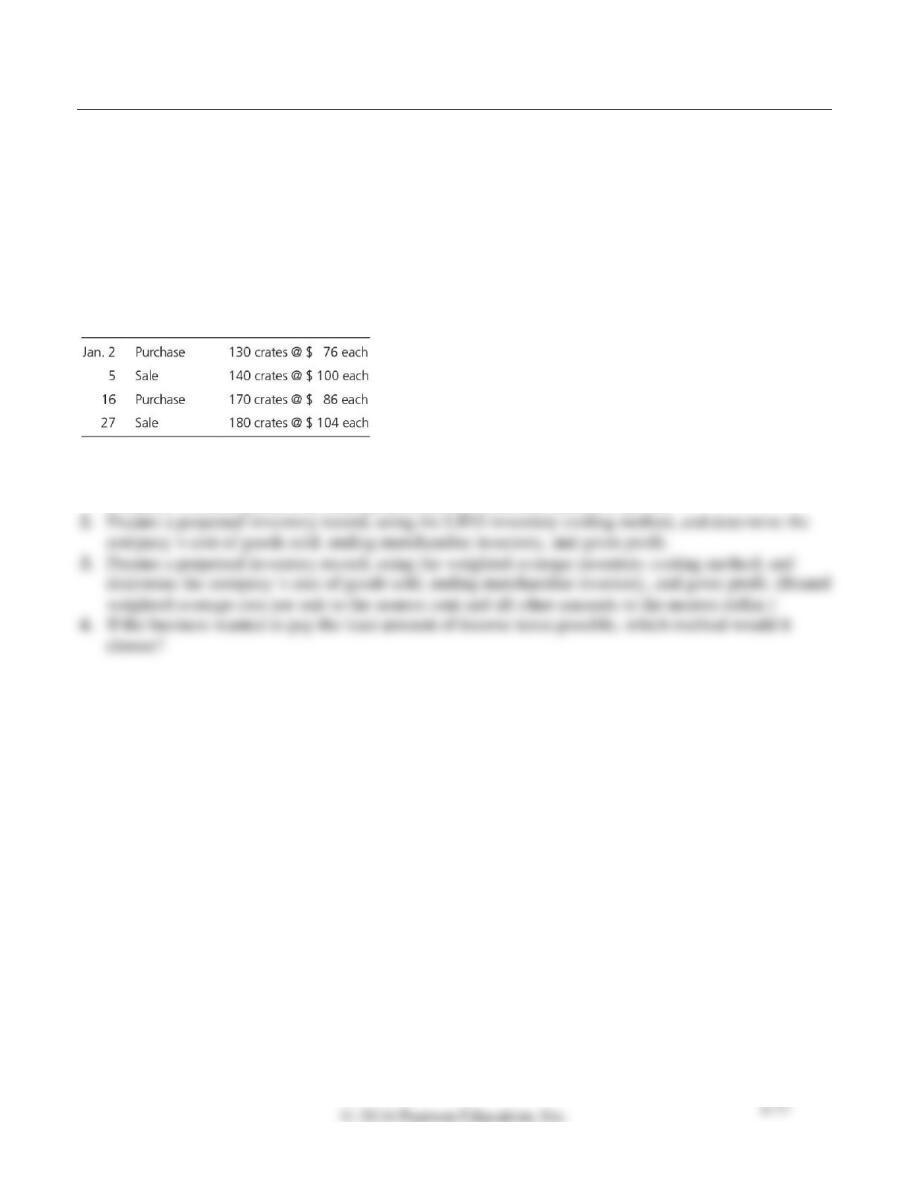

For all problems, assume the perpetual inventory system is used unless stated otherwise.

P6-33B Accounting for inventory using the perpetual inventory system—FIFO, LIFO, and

weighted-average

Learning Objectives 2, 3

2. Ending Merch. Inv., $4,550

Fit World began January with merchandise inventory of 90 crates of vitamins that cost a total of $5,850.

During the month, Fit World purchased and sold merchandise on account as follows:

Requirements

1. Prepare a perpetual inventory record, using the FIFO inventory costing method, and determine the

company’s cost of goods sold, ending merchandise inventory, and gross profit.

SOLUTION

Requirement 1

Using FIFO, cost of goods sold is $24,330, ending merchandise inventory is $6,020, and gross profit is $8,390.

Perpetual Inventory Record: FIFO

Purchases

Cost of Goods Sold

Inventory on Hand

Date

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Jan. 1

90 units

× $ 65 (a)

= $ 5,850

$ 5,850

130 units

90 units

130 units

90 units

80 units

50 units

170 units

80 units

70 units

100 units

300 units

$24,500

320 units

$ 24,330

70 units

P6-33B, cont.

Requirement 1, cont.

Calculations:

(a) Jan. 1 inventory unit cost

=

Total cost / Total number of units

=

$5,850 / 90 units

=

$65 per unit

=

Number of crates sold × Sales price per crate

Sale 1:

=

140 crates × $100 per crate

=

$14,000

Sale 2:

=

180 crates × $104 per crate

=

$18,720

=

Sales revenue from Sale 1 + Sales revenue from Sale 2

=

$14,000 + $18,720

=

$32,720

Total Sales Revenue

Cost of Goods Sold

(24,330)

Gross Profit

6-80

P6-33B, cont.

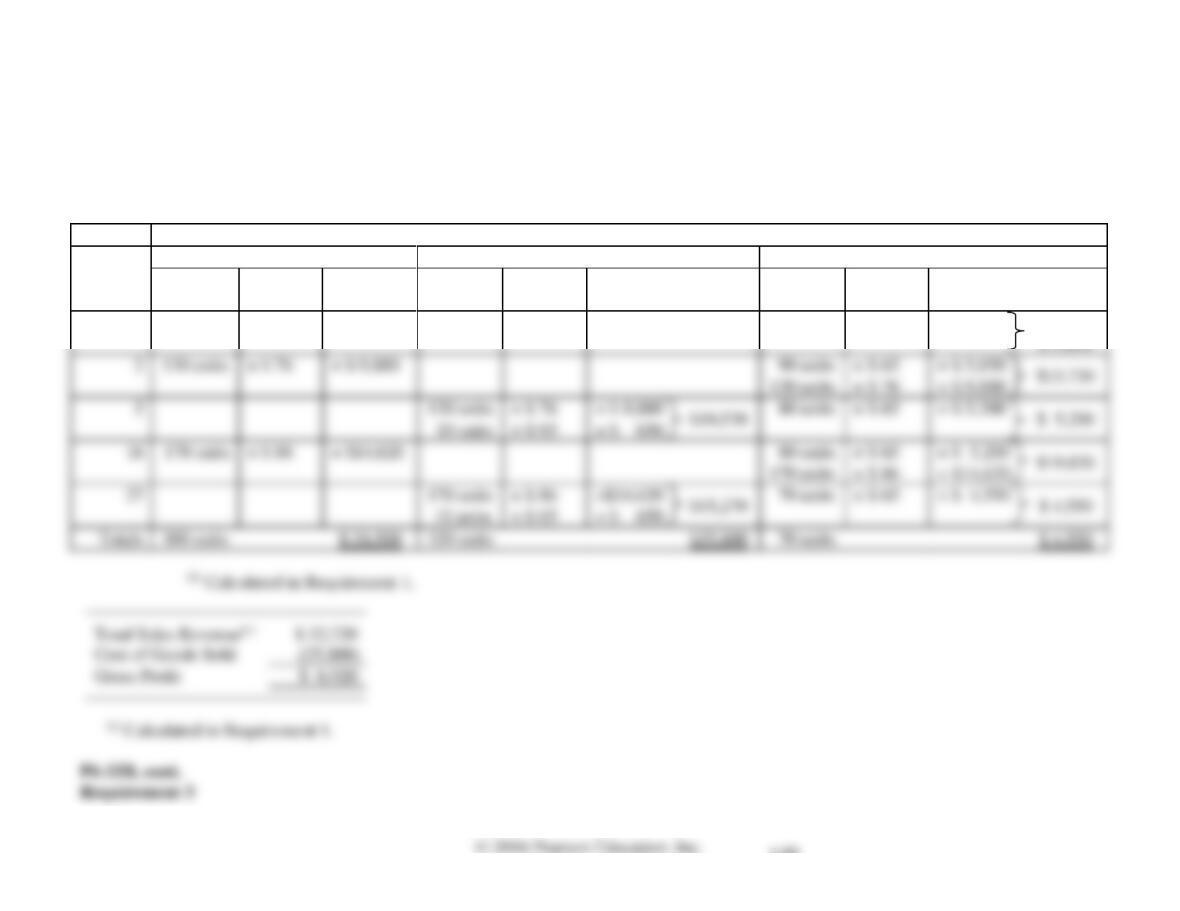

Requirement 2

Using LIFO, cost of goods sold is $25,800, ending merchandise inventory is $4,550, and gross profit is $6,920.

Perpetual Inventory Record: LIFO

Purchases

Cost of Goods Sold

Inventory on Hand

Date

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Jan. 1

90 units

× $ 65 (b)

= $ 5,850

130 units

90 units

130 units

130 units

80 units

10 units

170 units

80 units

170 units

70 units

10 units

300 units

320 units

$25,800

70 units

Cost of Goods Sold

(25,800)

Gross Profit