Exercises

For all exercises, assume the perpetual inventory system is used unless stated otherwise.

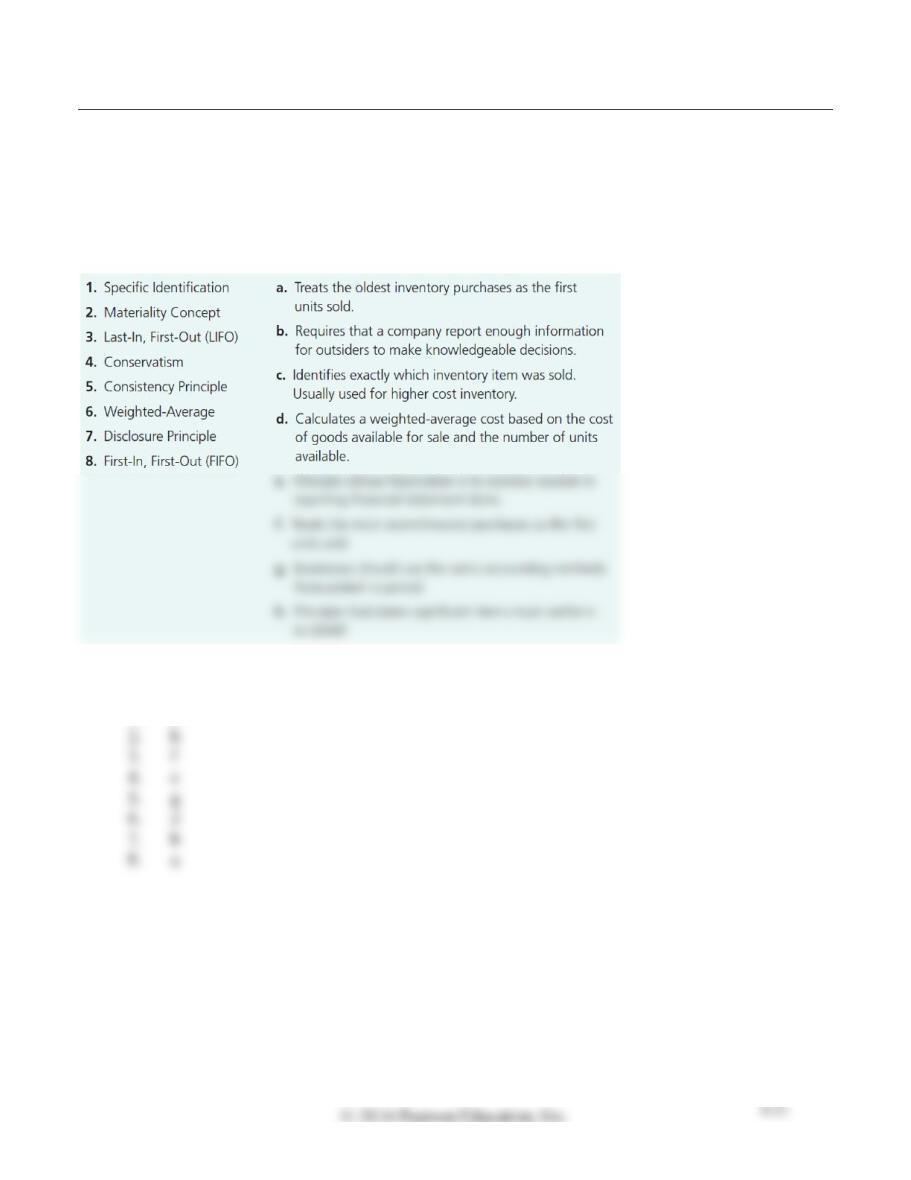

E6-14 Using accounting vocabulary

Learning Objectives 1, 2

Match the accounting terms with the corresponding definitions.

SOLUTION

1.

c

2.

h

3.

f

4.

e

5.

g

6.

d

7.

b

8.

a

6-22

E6-15 Comparing inventory methods

Learning Objective 2

1. Ending Merch. Inv. $20.70

Zippy, a regional convenience store chain, maintains milk inventory by the gallon. The first month’s

milk purchases and sales at its Columbus, Ohio, location follow:

Requirements

1. Determine the amount that would be reported in ending merchandise inventory on November 15

using the FIFO inventory costing method.

2. Determine the amount that would be reported in ending merchandise inventory on November 15

using the LIFO inventory costing method.

3. Determine the amount that would be reported in ending merchandise inventory on November 15

using the weighted-average inventory costing method. Round all amounts to the nearest cent.

SOLUTION

Requirement 1

Calculations:

FIFO

Purchases

Cost of Goods Sold

Inventory on Hand

× $ 2.65

= $ 5.30

× $ 2.00

= $ 22.00

× $ 2.00

= $ 6.00

× $ 2.00

= $ 16.00

× $ 2.70

= $ 5.40

× $ 2.00

= $ 16.00

= $ 5.30

= $ 5.40

× $ 2.00

= $ 6.00

5 units

× $ 2.00

= $ 10.00

×$ 2.65

= $ 5.30

×$ 2.70

= $ 5.40

Unit

Unit

Unit

6-24

E6-15, cont.

Requirement 2

Ending merchandise inventory on November 15 is $18.00 using LIFO.

Calculations:

LIFO

Purchases

Cost of Goods Sold

Inventory on Hand

× $ 2.65

= $ 5.30

× $ 2.00

= $ 22.00

× $ 2.65

= $ 5.30

× $ 2.00

= $ 20.00

1 unit

= $ 2.00

× $ 2.70

= $ 5.40

× $ 2.00

= $ 20.00

= $ 5.40

× $ 2.70

= $ 5.40

× $ 2.00

= $ 18.00

= $ 2.00

Unit

Unit

Unit

E6-15, cont.

Requirement 3

Ending merchandise inventory on November 15 is $19.80 using weighted-average.

Calculations:

Weighted-Average

6-26

Use the following information to answer Exercises E6-16 through E6-18.

Putter’s Choice carries an inventory of putters and other golf clubs. The sales price of each putter is

$119. Company records indicate the following for a particular line of Putter’s Choice putters:

E6-16 Measuring and journalizing merchandise inventory and cost of goods sold—FIFO

Learning Objective 2

1. CoGS $2,940

Requirements

1. Prepare a perpetual inventory record for the putters assuming Putter’s Choice uses the FIFO

inventory costing method. Then identify the cost of ending inventory and cost of goods sold for the

SOLUTION

Requirement 1

Perpetual Inventory Record: FIFO

Purchases

Cost of Goods Sold

Inventory on Hand

Date

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Nov. 1

22 units

× $ 60

= $ 1,320

$ 1,320

× $ 60

= $ 720

× $ 60

= $ 600

× $ 81

= $ 2,025

× $ 60

= $ 600

= $ 2,025

× $ 60

= $ 600

× $ 81

= $ 810

= $1,215

$ 2,025

5 units

E6-16, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Nov. 6

Accounts Receivable

1,428 (a)

Sales Revenue

1,428 (a)

Sale on account.

Cost of Goods Sold

Recorded the cost of goods sold.

Merchandise Inventory

2,025

Accounts Payable

2,025

Purchased inventory on account.

Accounts Receivable

Sales Revenue

Sale on account.

Cost of Goods Sold

Recorded the cost of goods sold.

Accounts Receivable

Sales Revenue

Sale on account.

Cost of Goods Sold

Recorded the cost of goods sold.

E6-16, cont.

Requirement 2, cont.

Calculations:

Total sales revenue

=

Number of putters sold × Sales price per putter

=

12 putters × $119 per putter

=

$1,428

=

25 putters × $119 per putter

=

$2,975

=

5 putters × $119 per putter

=

$595

Calculated in Requirement 1.

E6-17 Measuring ending inventory and cost of goods sold in a perpetual inventory system—LIFO

Learning Objective 2

1. Ending Merch. Inv. $300

Requirements

1. Prepare Putter’s Choice’s perpetual inventory record for the putters assuming Putter’s Choice uses

the LIFO inventory costing method. Then identify the cost of ending inventory and cost of goods

sold for the month.

2. Journalize Putter’s Choice’s inventory transactions using the LIFO inventory costing method.

(Assume purchases and sales are made on account.)

SOLUTION

Requirement 1

Perpetual Inventory Record: LIFO

Purchases

Cost of Goods Sold

Inventory on Hand

Date

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Nov. 1

22 units

× $ 60

= $ 1,320

$ 1,320

$ 2,025

5 units

E6-17, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Nov. 6

Accounts Receivable

1,428 (a)

Sales Revenue

1,428 (a)

Sale on account.

Cost of Goods Sold

Recorded the cost of goods sold.

Merchandise Inventory

2,025

Accounts Payable

2,025

Purchased inventory on account.

Accounts Receivable

Sales Revenue

Sale on account.

Cost of Goods Sold

Recorded the cost of goods sold.

Accounts Receivable

Sales Revenue

Sale on account.

Cost of Goods Sold

Recorded the cost of goods sold.

6-32

E6-17, cont.

Requirement 2, cont.

Calculations:

Total sales revenue

=

Number of putters sold × Sales price per putter

=

12 putters × $119 per putter

=

$1,428

=

25 putters × $119 per putter

=

$2,975

=

5 putters × $119 per putter

=

$595

Calculated in Requirement 1.

E6-18 Measuring ending inventory and cost of goods sold in a perpetual inventory system—

Weighted-average

Learning Objective 2

1. CoGS $2,970

Requirements

1. Prepare Putter’s Choice’s perpetual inventory record for the putters assuming Putter’s Choice uses

the weighted-average inventory costing method. Round weighted-average cost per unit to the nearest

cent and all other amounts to the nearest dollar. Then identify the cost of ending inventory and cost

of goods sold for the month.

2. Journalize Putter’s Choice’s inventory transactions using the weighted-average inventory costing

method. (Assume purchases and sales are made on account.)

SOLUTION

Requirement 1

Perpetual Inventory Record: Weighted-Average

Purchases

Cost of Goods Sold

Inventory on Hand

Date

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total

Cost

Quantity

Unit

Cost

Total Cost

Nov. 1

22 units

× $ 60

= $ 1,320

× $ 60

10 units

× $ 60

= $ 600

× $ 81

= $ 2,025

35 units

= $ 2,625

25 units

× $ 75

= $ 1,875

10 units

× $ 75

= $ 750

5 units

× $ 75

= $ 375

5 units

× $ 75

= $ 375

$ 2,025

42 units

5 units

$ 375

=

Cost of goods available for sale / Number of units available

=

($600 + $2,025) / (10 units + 25 units)

=

$2,625 / 35 units

=

$75 per unit

6-34

E6-18, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Nov. 6

Accounts Receivable

1,428 (a)

Sales Revenue

1,428 (a)

Sale on account.

Cost of Goods Sold

Recorded the cost of goods sold.

Merchandise Inventory

2,025

Accounts Payable

2,025

Purchased inventory on account.

Accounts Receivable

Sales Revenue

Sale on account.

Cost of Goods Sold

1,875 (e)

1,875 (e)

Recorded the cost of goods sold.

Accounts Receivable

Sales Revenue

Sale on account.

Cost of Goods Sold

Recorded the cost of goods sold.

E6-18, cont.

Requirement 2, cont.

Calculations:

Total sales revenue

=

Number of putters sold × Sales price per putter

=

12 putters × $119 per putter

=

$1,428

=

25 putters × $119 per putter

=

$2,975

=

5 putters × $119 per putter

=

$595

Calculated in Requirement 1.

6-36

E6-19 Comparing amounts for cost of goods sold, ending inventory, and gross profit—FIFO and

LIFO

Learning Objectives 2, 3

2. Ending Merch. Inv. $70

Assume that Toyland store bought and sold a line of dolls during December as follows:

Requirements

1. Compute the cost of goods sold, cost of ending merchandise inventory, and gross profit using the

FIFO inventory costing method.

SOLUTION

Requirement 1

Using FIFO, cost of goods sold is $238, ending merchandise inventory is $105, and gross profit is $203.

Calculations:

Purchases

Cost of Goods Sold

Inventory on Hand

Date

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Dec. 1

11 units

× $ 8

= $ 88

$ 255

Less: Cost of Goods Sold

Gross Profit

=

Number of dolls sold × Sales price per doll

=

21 dolls × $21 per doll

E6-19, cont.

Requirement 2

Using LIFO, cost of goods sold is $273, ending merchandise inventory is $70, and gross profit is $168.

Calculations:

Purchases

Cost of Goods Sold

Inventory on Hand

Date

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Dec. 1

11 units

× $ 8

= $ 88

$ 255

$ 70

Less: Cost of Goods Sold

273

Gross Profit

E6-19, cont.

Requirement 3

Requirement 4

Requirement 5

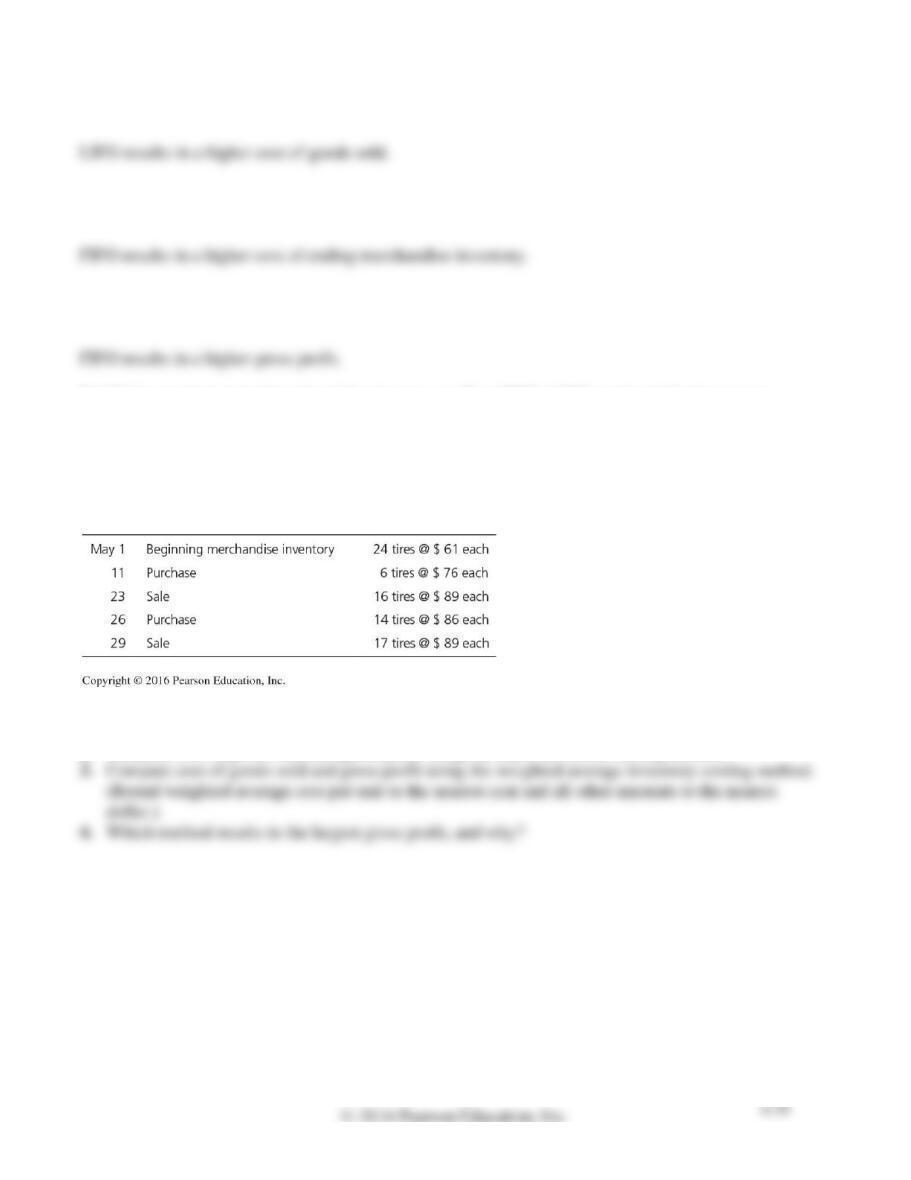

E6-20 Comparing cost of goods sold and gross profit—FIFO, LIFO, and weighted-average

methods

Learning Objectives 2, 3

1. CoGS $2,178

Assume that RK Tire Store completed the following perpetual inventory transactions for a line of tires:

Requirements

1. Compute cost of goods sold and gross profit using the FIFO inventory costing method.

2. Compute cost of goods sold and gross profit using the LIFO inventory costing method.

6-40

SOLUTION

Requirement 1

Using FIFO, cost of goods sold is $2,178 and gross profit is $759.

Calculations:

Purchases

Cost of Goods Sold

Inventory on Hand

Date

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

May 1

24 units

× $ 61

= $ 1,464

$ 1,464

× $ 76

= $ 456

× $ 61

= $ 1,464

× $ 76

× $ 61

= $ 976

× $ 61

= $ 488

× $ 76

= $ 456

× $ 86

= $ 1,204

× $ 61

= $ 488

× $ 76

= $ 456

× $ 86

= $ 1,204

× $ 76

= $ 456

× $ 86

= $ 258

$ 2,178

$ 2,937

Less: Cost of Goods Sold

Gross Profit

$ 759

=

Number of tires sold × Sales price per tire

=

33 tires × $89 per tire