Chapter 6

Merchandise Inventory

Review Questions

1. Which principle states that businesses should use the same accounting methods and procedures from

period to period?

2. What does the disclosure principle require?

The disclosure principle requires that a company must report enough information in its financial

statements for outsiders to make knowledgeable decisions about the company.

3. Discuss the materiality concept. Is the dollar amount that is material the same for a company that has

annual sales of $10,000 compared with a company that has annual sales of $1,000,000?

The materiality concept states that a company must perform strictly proper accounting only for

4. What is the goal of conservatism?

5. Discuss some measures that should be taken to maintain control over merchandise inventory.

Maintaining goods controls over merchandise inventory is very important for a merchandiser. Good

6. Under a perpetual inventory system, what are the four inventory costing methods and how does each

method determine ending merchandise inventory and cost of goods sold?

The four inventory costing methods are specific identification, FIFO (First-In, First-Out), LIFO

(Last-In, First-Out), and weighted-average. The specific identification method uses the specific cost

7. When using a perpetual inventory system and the weighted-average inventory costing method, when

does the business compute a new weighted-average cost per unit?

8. During periods of rising costs, which inventory costing method produces the highest gross profit?

During periods of rising costs, the FIFO inventory costing method produces the highest gross profit.

9. What does the lower-of-cost-or-market (LCM) rule require?

10. What account is debited when recording the adjusting entry to write down merchandise inventory

under the LCM rule?

11. What is the effect on cost of goods sold, gross profit, and net income if ending merchandise

inventory is understated?

12. When does an inventory error cancel out, and why?

One period’s ending merchandise inventory becomes the next period’s beginning merchandise

13. How is inventory turnover calculated, and what does it measure?

Inventory turnover measures how rapidly merchandise inventory is sold during a period (the number

14. How is days’ sales in inventory calculated, and what does it measure?

Days’ sales in inventory measures the average number of days merchandise inventory is held by a

company. Days’ sales in inventory = 365 days / Inventory turnover.

15A. When using the periodic inventory system, which inventory costing method(s)

always produces the same result as when using the perpetual inventory system?

16A. When using the periodic inventory system and weighted-average inventory costing method,

when is the weighted-average cost per unit computed?

When using the periodic inventory system and weighted-average inventory costing method, the

6-4

Short Exercises

For all short exercises, assume the perpetual inventory system is used unless stated otherwise.

S6-1 Determining inventory accounting principles

Learning Objective 1

Ward Hardware used the FIFO inventory costing method in 2017. Ward plans to continue using the

FIFO method in future years. Which accounting principle is most relevant to Ward’s decision?

SOLUTION

S6-2 Determining inventory costing methods

Learning Objective 2

Ward Hardware does not expect costs to change dramatically and wants to use an inventory costing

method that averages cost changes.

Requirements

1. Which inventory costing method would best meet Ward’s goal?

2. Assume Ward wanted to expense out the newer purchases of goods instead. Which inventory costing

method would best meet that need?

SOLUTION

Requirement 1

Use the following information to answer Short Exercises S6-3 through S6-6.

Montana Cycles started July with 25 bicycles that cost $36 each. On July 16, Montana bought 35

bicycles at $60 each. On July 31, Montana sold 33 bicycles for $105 each.

S6-3 Preparing a perpetual inventory record and journal entries—Specific identification

Learning Objective 2

Requirements

1. Prepare Montana Cycle’s perpetual inventory record assuming the company uses the specific

identification inventory costing method. Assume that Montana sold 20 bicycles that cost $36 each

and 13 bicycles that cost $60 each.

2. Journalize the July 16 purchase of merchandise inventory on account and the July 31 sale of

merchandise inventory on account.

SOLUTION

Requirement 1

Perpetual Inventory Record: Specific Identification

Purchases

Cost of Goods Sold

Inventory on Hand

Date

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

16

35 units

× $ 60

= $ 2,100

25 units

× $ 36

= $ 900

35 units

31

20 units

× $ 36

= $ 720

5 units

× $ 36

= $ 180

13 units

22 units

6-6

S6-3, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Jul. 16

Merchandise Inventory

2,100

Accounts Payable

2,100

Purchased inventory on account.

Accounts Receivable

Sales Revenue

Sale on account.

Cost of Goods Sold

Recorded the cost of goods sold.

S6-4 Preparing a perpetual inventory record and journal entries—FIFO

Learning Objective 2

Requirements

1. Prepare Montana Cycle’s perpetual inventory record assuming the company uses the FIFO inventory costing method.

2. Journalize the July 16 purchase of merchandise inventory on account and the July 31 sale of merchandise inventory on account.

SOLUTION

Requirement 1

Perpetual Inventory Record: FIFO

Purchases

Cost of Goods Sold

Inventory on Hand

Date

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

16

35 units

31

Totals

35 units

S6-4, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Jul. 16

Merchandise Inventory

2,100

Accounts Payable

2,100

Purchased inventory on account.

Accounts Receivable

Sales Revenue

Sale on account.

Cost of Goods Sold

Recorded the cost of goods sold.

Calculations:

S6-5 Preparing a perpetual inventory record and journal entries—LIFO

Learning Objective 2

Requirements

1. Prepare Montana Cycle’s perpetual inventory record assuming the company uses the LIFO inventory costing method.

2. Journalize the July 16 purchase of merchandise inventory on account and the July 31 sale of merchandise inventory on account.

SOLUTION

Requirement 1

Perpetual Inventory Record: LIFO

Purchases

Cost of Goods Sold

Inventory on Hand

Date

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

Quantity

Unit

Cost

Total Cost

16

35 units

31

Totals

35 units

6-10

S6-5, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Jul. 16

Merchandise Inventory

2,100

Accounts Payable

2,100

Purchased inventory on account.

Accounts Receivable

Sales Revenue

Sale on account.

Cost of Goods Sold

Merchandise Inventory

Recorded the cost of goods sold.

Calculations:

(a)

Total sales revenue

=

Number of bicycles sold x Sales price per bicycle

=

33 bicycles x $105 per bicycle

=

$3,465

(b)

Calculated in Requirement 1.

S6-6 Preparing a perpetual inventory record and journal entries—Weighted-average

Learning Objective 2

Requirements

1. Prepare Montana Cycle’s perpetual inventory record assuming the company uses the weighted-average inventory costing method.

2. Journalize the July 16 purchase of merchandise inventory on account and the July 31 sale of merchandise inventory on account.

SOLUTION

Requirement 1

Perpetual Inventory Record: Weighted-Average

S6-6, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Jul. 16

Merchandise Inventory

2,100

Accounts Payable

2,100

Purchased inventory on account.

Accounts Receivable

Sales Revenue

Sale on account.

Cost of Goods Sold

Recorded the cost of goods sold.

Note: Short Exercises S6-4, S6-5, and S6-6 must be completed before attempting Short Exercise S6-7.

S6-7 Comparing Cost of Goods Sold under FIFO, LIFO, and Weighted-average

Learning Objective 3

Refer to Short Exercises S6-4 through S6-6. After completing those exercises, answer the following

questions:

Requirements

1. Which inventory costing method produced the lowest cost of goods sold?

2. Which inventory costing method produced the highest cost of goods sold?

3. If costs had been declining instead of rising, which inventory costing method would have produced

the highest cost of goods sold?

SOLUTION

Requirement 1

S6-8 Applying the lower-of-cost-or-market rule

Learning Objective 4

Assume that a Mega Burger restaurant has the following perpetual inventory record for hamburger

patties:

6-14

SOLUTION

No adjusting entry is needed because the current replacement cost (market value) is higher than the

S6-9 Determining the effect of an inventory error

Learning Objective 5

Mountain Pool Supplies’s merchandise inventory data for the year ended December 31, 2017, follow:

Requirements

1. Assume that the ending merchandise inventory was accidentally overstated by

$1,300. What are the correct amounts for cost of goods sold and gross profit?

2. How would the inventory error affect Mountain Pool Supplies’s cost of goods sold and gross profit

for the year ended December 31, 2018, if the error is not corrected in 2017?

SOLUTION

Requirement 1

For the year ended December 31, 2017, the correct amounts for cost of goods sold and gross profit are

$29,400 and $16,600, respectively.

If ending inventory is overstated by $1,300,

then cost of goods sold is understated by $1,300.

$ 28,100

Incorrect cost of goods sold

Understatement

Correct cost of goods sold

If cost of goods sold is understated by $1,300,

then gross profit is overstated by $1,300.

$ 17,900

Incorrect gross profit

(1,300)

Overstatement

Correct gross profit

This can be proved as follows:

Sales Revenue

$ 46,000

Cost of Goods Sold:

$ 3,500

Gross Profit

$ 16,600

Requirement 2

Ending merchandise inventory on December 31, 2017 is the same as beginning merchandise inventory

6-16

S6-10 Computing the rate of inventory turnover and days’ sales in inventory

Learning Objective 6

Clear Communications reported the following figures in its annual financial statements:

Compute the rate of inventory turnover and days’ sales in inventory for Clear Communications. (Round

to two decimal places.)

SOLUTION

Inventory turnover is 35.85 times and days’ sales in inventory is 10.18 days.

Calculations:

Use the following information to answer Short Exercises S6A-11 through S6A-13.

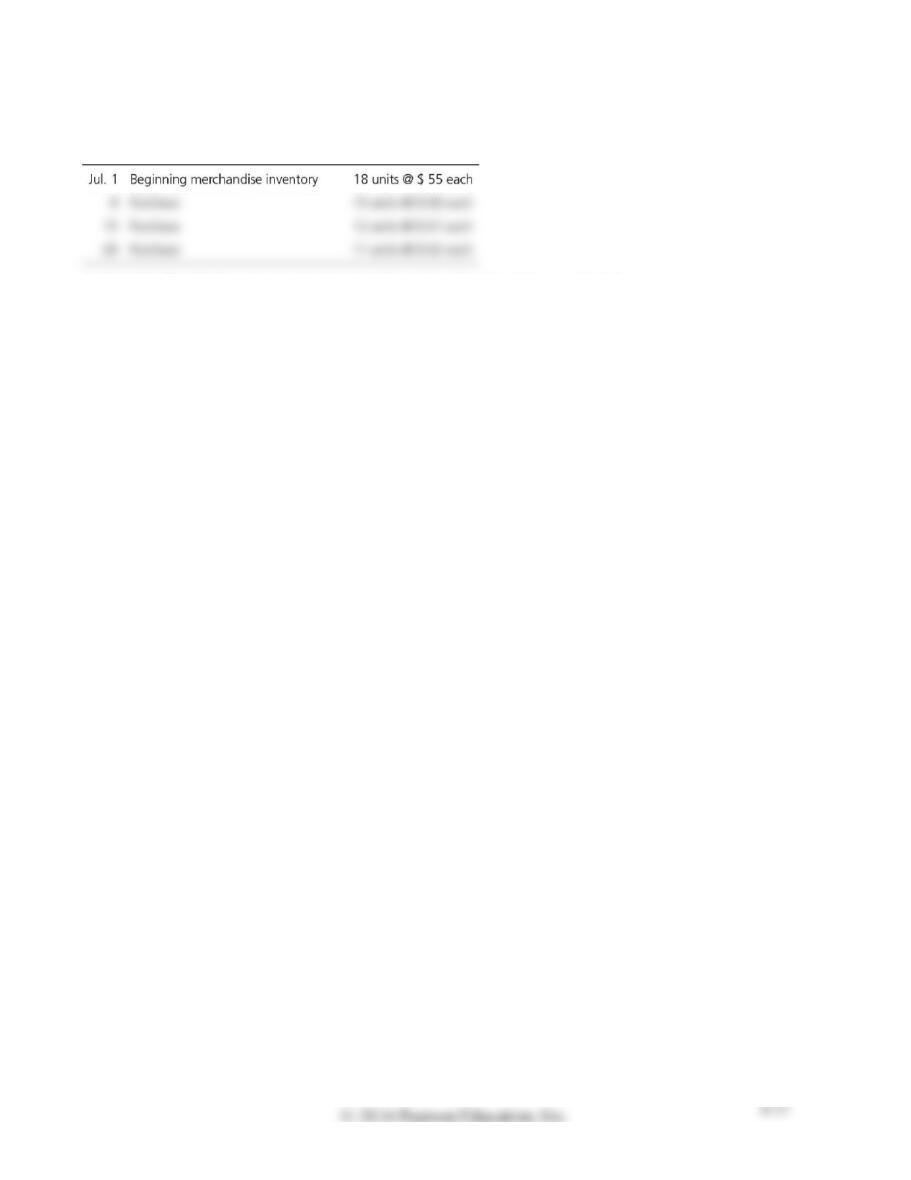

The periodic inventory records of Cambridge Prosthetics indicate the following for the month of July:

At July 31, Cambridge counts nine units of merchandise inventory on hand.

S6A-11 Computing periodic inventory amounts—FIFO

Learning Objective 7

Appendix 6A

Compute ending merchandise inventory and cost of goods sold for Cambridge using the FIFO inventory

costing method.

6-18

SOLUTION

Using FIFO, ending merchandise inventory is $558 and cost of goods sold is $2,746.

Calculations:

S6A-12 Computing periodic inventory amounts—LIFO

Learning Objective 7

Appendix 6A

Compute ending merchandise inventory and cost of goods sold for Cambridge using the LIFO inventory

costing method.

SOLUTION

Using LIFO, ending merchandise inventory is $495 and cost of goods sold is $2,809.

6-20

S6A-13 Computing periodic inventory amounts—Weighted-average

Learning Objective 7

Appendix 6A

Compute ending merchandise inventory and cost of goods sold for Cambridge using the weighted-

average inventory costing method.

SOLUTION

Using weighted-average, ending merchandise inventory is $531 and cost of goods sold is $2,773.