5-56 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 5-10A (Concluded)

2. The Total column represents the pool of costs (beginning inventory plus purchases)

3. Income statements for the month of November:

Weighted

Average

FIFO LIFO

4. The company will pay $125 more in taxes if it uses FIFO:

FIFO tax …………….. $806

LO 5,7,12 PROBLEM 5-11A COMPARISON OF INVENTORY COSTING METHODS—

PERPETUAL SYSTEM (Appendix)

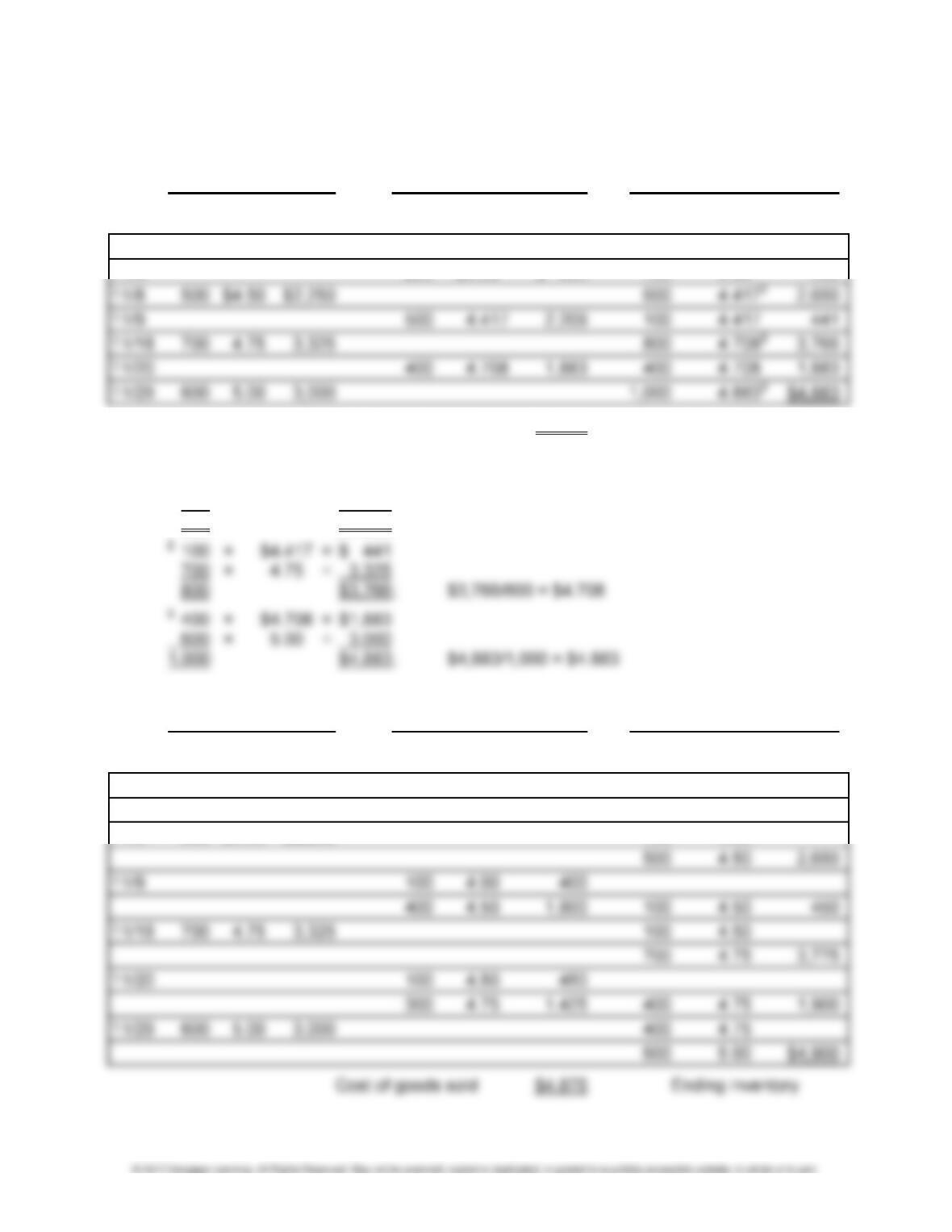

1. Cost of Ending

Goods Sold Inventory Total

a. Moving average ……………………………….. $4,892 $4,883 $9,775

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-57

PROBLEM 5-11A (Continued)

a. Moving average:

Purchases

Sales Balance

Unit Total Unit Total Unit

Date Units Cost Cost Units Cost Cost Units Cost Balance

11/1 300 $4.00 $1,200

11/4 200 $4.00 $ 800 100 4.00 400

Cost of goods sold $4,892 Ending inventory

All amounts rounded to agree with total cost.

1 100 × $4.00 = $ 400

500 × 4.50 = 2,250

600 $ 2,650; $2,650/600 = $4.417

b. FIFO:

Purchases

Sales Balance

Unit Total Unit Total Unit

Date Units Cost Cost Units Cost Cost Units Cost Balance

11/1 300 $4.00 $1,200

11/4 200 $4.00 $ 800 100 4.00 400

11/8 500 $4.50 $2,250 100 4.00

5-58 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

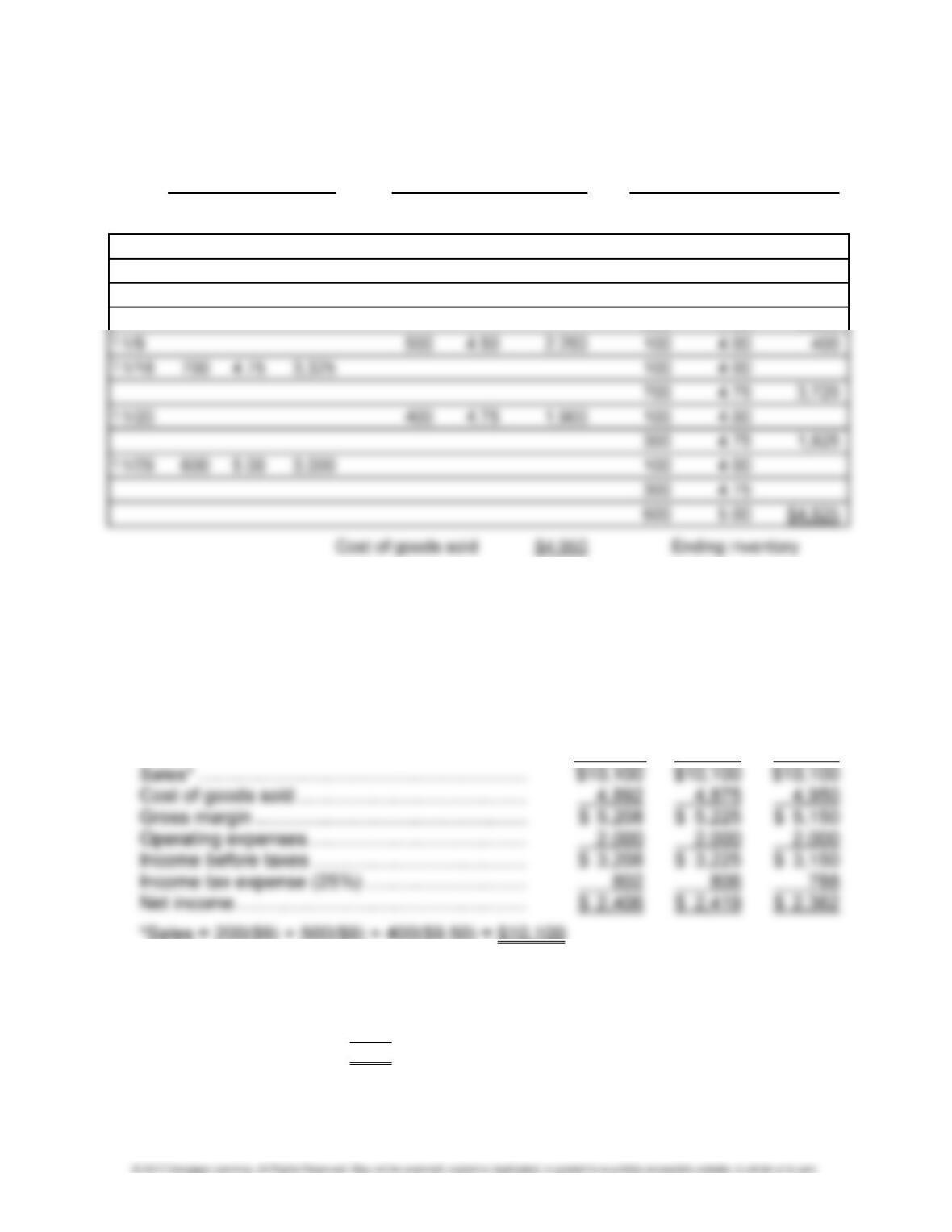

PROBLEM 5-11A (Concluded)

c. LIFO:

Purchases

Sales Balance

Unit Total Unit Total Unit

Date Units Cost Cost Units Cost Cost Units Cost Balance

11/1 300 $4.00 $1,200

11/4 200 $4.00 $ 800 100 4.00 400

11/8 500 $4.50 $2,250 100 4.00

500 4.50 2,650

2. The Total column represents the pool of costs (beginning inventory plus purchases)

to be distributed between an asset, ending inventory on the balance sheet, and an

expense, cost of goods sold on the income statement. In accounting, this pool of

costs is called cost of goods available for sale.

3. Income statements for the month of November:

Moving

Average FIFO LIFO

4. The company will pay $18 more in taxes if it uses FIFO:

FIFO tax …………….. $806

LIFO tax …………….. 788

Difference ………….. $ 18

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-59

LO 5,6,7 PROBLEM 5-12A INVENTORY COSTING METHODS—PERIODIC SYSTEM

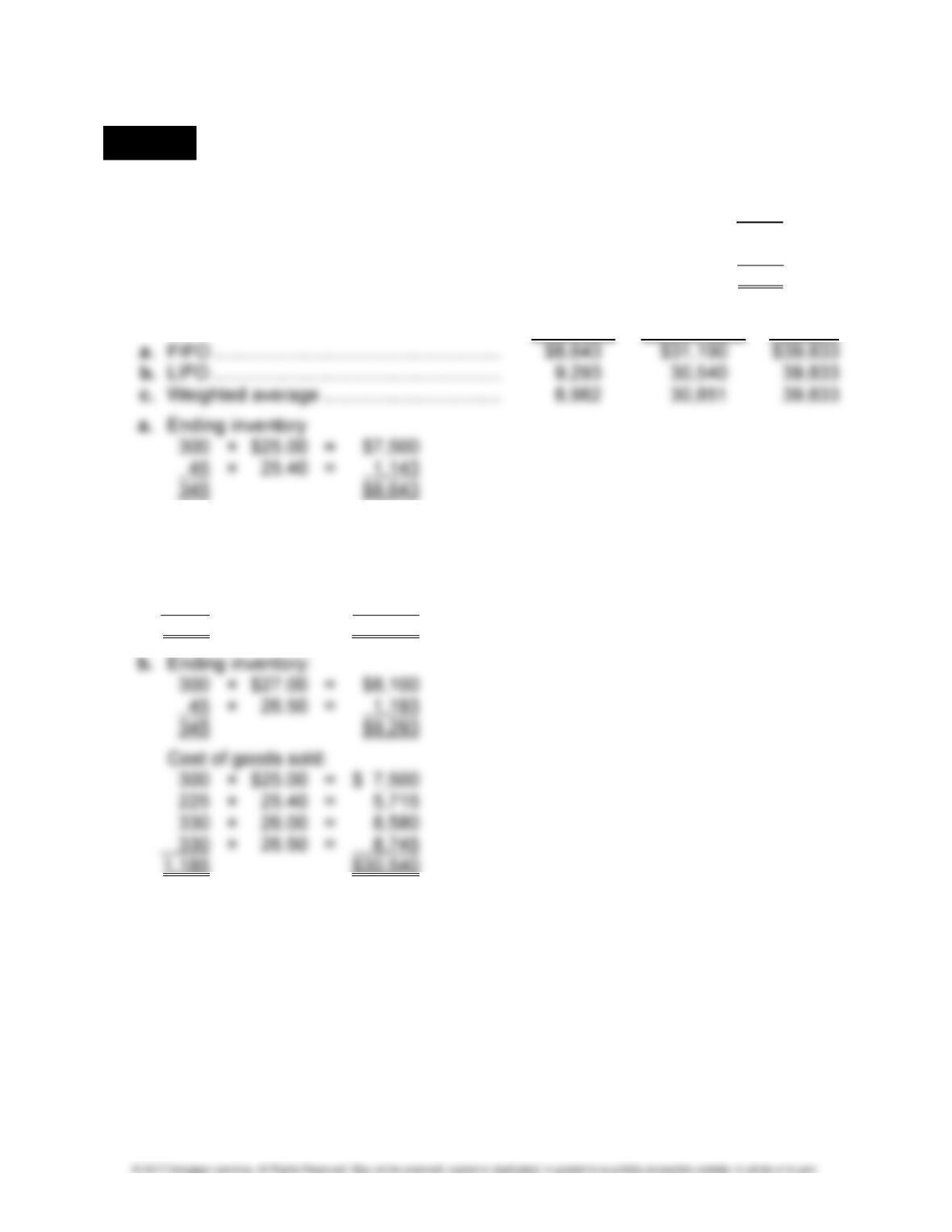

1. Units in beginning inventory ………………………………………………… 300

Units purchased (375 + 330 + 225 + 300) ……………………………… 1,230

Units available ………………………………………………………………….. 1,530

Units sold (450 + 570 + 165) ……………………………………………….. (1,185)

Units in ending inventory …………………………………………………….. 345

Ending Cost of

Inventory Goods Sold Total

Cost of goods sold:

300 × $27.00 = $ 8,100

375 × 26.50 = 9,938

330 × 26.00 = 8,580

180 × 25.40 = 4,572

1,185 $31,190

5-60 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 5-12A (Concluded)

c. Beginning inventory 300 × $27.00 = $ 8,100

Nov. 4 375 × 26.50 = 9,938

2. Weighted

FIFO LIFO Average

Sales* ……………………………………………………… $75,330 $75,330 $75,330

Cost of goods sold …………………………………….. 31,190 30,540 30,851

3. Story pays the least taxes under the first-in, first-out method since it has the highest

cost of goods sold.

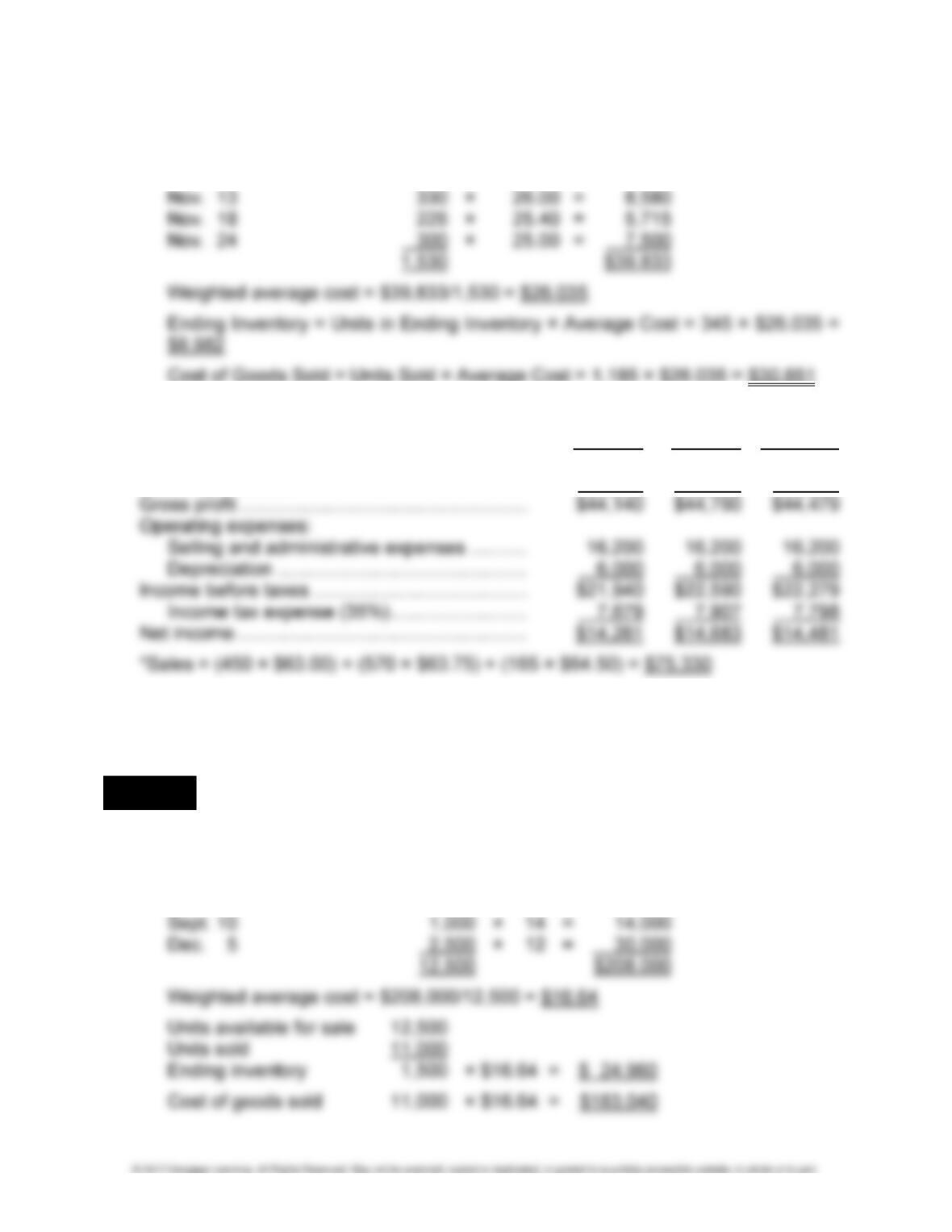

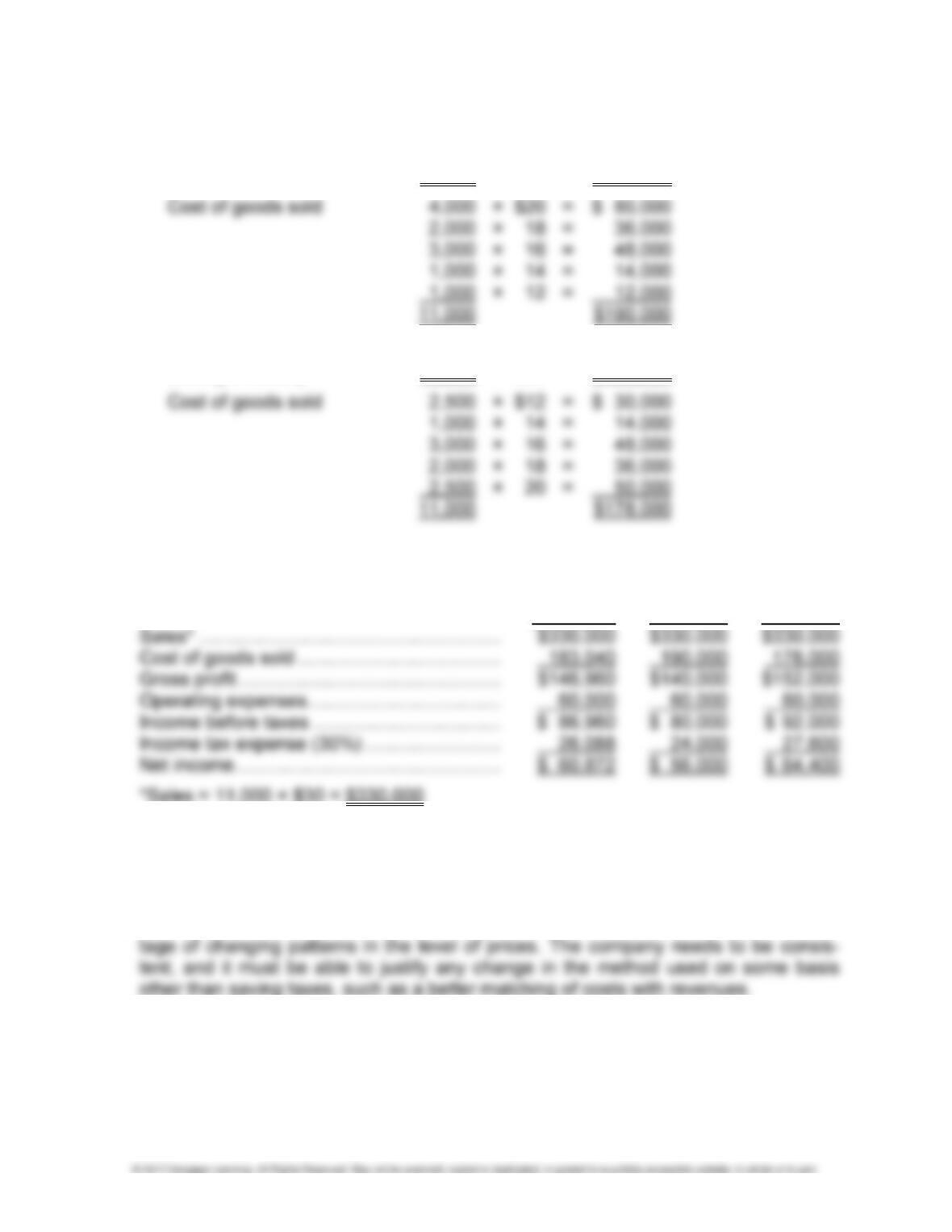

LO 5,6,7 PROBLEM 5-13A INVENTORY COSTING METHODS—PERIODIC SYSTEM

1. a. Weighted average:

Beginning inventory 4,000 × $20 = $ 80,000

Feb. 4 2,000 × 18 = 36,000

Apr. 12 3,000 × 16 = 48,000

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-61

PROBLEM 5-13A (Concluded)

b. FIFO:

Ending inventory 1,500 × $12 = $ 18,000

c. LIFO:

Ending inventory 1,500 × $20 = $ 30,000

2. Income statements for the year ended December 31, 2016:

Weighted

Average

FIFO LIFO

3. Fees can minimize its tax bill by using FIFO. In a period of declining prices, FIFO

results in the highest cost of goods sold, the least amount of income before taxes,

and thus the least amount of income tax expense.

4. A company is not free to change inventory methods from year to year to take advan-

5-62 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 1,7,8 PROBLEM 5-14A INTERPRETING THE NEW YORK TIMES COMPANY’S

FINANCIAL STATEMENTS

1. Newsprint costs are comparable to raw materials in a manufacturing company. A

newspaper company, however, does not keep an inventory of finished goods. Its

2. Some companies use different methods to value different types of inventory. The

methods should be chosen because they provide the most accurate matching of

DECISION CASES

READING AND INTERPRETING FINANCIAL STATEMENTS

LO 1,3 DECISION CASE 5-1 COMPARING TWO COMPANIES IN THE SAME INDUSTRY:

CHIPOTLE AND PANERA BREAD

1 . Chipotle’s inventories amount to $15,332,000,000, which represents $15,332/

2,546,285, or only 0.6% of its total assets. Panera Bread’s inventories amount to

$22,811,000,000 which represents $22,811/$1,390,902, or only 1.6% of its total as-

sets. Both companies are in the restaurant business and thus its inventories on hand

at any point in time are relatively insignificant.

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-63

LO 6,7 DECISION CASE 5-2 READING AND INTERPRETING WALGREEN CO.’S

INVENTORY NOTE

1. Walgreen Co. uses LIFO. A business should employ the method that most accurate-

ly matches inventory costs with the revenues of the period. Walgreen Co. may use

LIFO because prices change frequently and it wants to match the most recent costs

with revenues generated in the current period.

LO 6,9 DECISION CASE 5-3 READING AND INTERPRETING GAP INC.’S INVENTORY

NOTE

1. Gap Inc. uses the weighted average cost method. A company chooses an inventory

5-64 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

MAKING FINANCIAL DECISIONS

LO 2,3,4 DECISION CASE 5-4 GROSS PROFIT FOR A MERCHANDISER

1. According to the income statement prepared by the controller, Emblems’ gross profit

ratio is $6,750/$15,000, or 45%.

Selling price ……………………………….. $ 20.00 per unit

Costs per unit:

Purchase price ……………………….. $10.00

Tax (10%) ……………………………… 1.00

Shipping ……………………………….. 0.50

LO 2,3,4 DECISION CASE 5-5 PRICING DECISION

1. Cost per pound …………………………………………………………………. $5.00

Sales tax (5% × $5.00) ………………………………………………………. 0.25

Gross cost ………………………………………………………………………… $5.25

2. Selling price – $5.90 = 40% (selling price)

60% (selling price) = $5.90

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-65

DECISION CASE 5-5 (Concluded)

3. Before deciding whether this is a sufficient profit, Caroline’s Candy should check indus-

try averages and the price local competitors are charging. If the price charged is too

LO 3 DECISION CASE 5-6 USE OF A PERPETUAL INVENTORY SYSTEM

1. Memo to Darrell:

The purpose of this memo is to clarify for you the costs and benefits of a perpetual

inventory system. The purpose of a perpetual system is to provide a continuously

updated record of the number of units and cost of all inventory items. A perpetual

2. The suitability of a perpetual inventory system is certainly dependent on the type of

products a company sells. The system is ideally suited to a product such as auto-

5-66 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 6,7 DECISION CASE 5-7 INVENTORY COSTING METHODS

1. Georgetown must use the periodic inventory system at least for the first year

because it did not keep a record of the cost of the units sold as each sale was made.

2. Units on hand at the end of the year:

January ……………………………………………………………………………. 1,000

3. Unless a company specifically identifies the cost of each unit sold, it must adopt an

assumption about which particular units were sold. Each of the inventory costing

methods takes the pool of costs (cost of goods available for sale) and makes an

assumption about which units were sold and which units remain on hand.

*3,000 units sold at $15 each

** 1,000 × $8 = $ 8,000

1,200 × 8 = 9,600

1,500 × 9 = 13,500

Available 3,700 $31,100

Ending inventory:

FIFO 700 × $9 = $6,300

LIFO 700 × $8 = $5,600

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-67

LO 8 DECISION CASE 5-8 INVENTORY ERRORS

The first error resulted in an understatement of the ending inventory in 2014 by $28,700.

Thus, cost of goods sold in 2014 was overstated, and gross profit was understated by

the same amount. The effect on net income would be less than the amount of unders-

tatement of gross profit because of the effect of taxes.

ETHICAL DECISION MAKING

LO 7 DECISION CASE 5-9 SELECTION OF AN INVENTORY METHOD

1. Recognize an Ethical Dilemma

The chief executive officer is concerned with reporting the highest amount of income

2. Analyze the Key Elements in the Situation

a. The chief executive officer could benefit. Stockholders could be harmed.

b. The chief executive officer would benefit if his or her compensation is tied to the

5-68 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

DECISION CASE 5-9 (Concluded)

3. List Alternatives and Evaluate the Impact of Each on Those Affected

As controller, you can either go along with the instructions from the chief executive

officer or you can insist that LIFO be used. The chief executive officer is primarily

4. Select the Best Alternative

The best alternative is to explain to the chief executive officer that the interests of

LO 9 DECISION CASE 5-10 WRITE-DOWN OF OBSOLETE INVENTORY

1. The write-off of the inventory that has become obsolete would reduce the current

year’s income. The amount of the reduction depends on the extent of the write-off. If

2. If the inventory is not adjusted, total assets on the year-end balance sheet will be

overstated.

3. The materiality of the obsolete inventory should be a major factor in a decision to

persist in the argument that the inventory be written down. If the inventory in

4. If the inventory is not written down, readers do not have information that is a faithful

representation. Under the lower-of-cost-or-market rule, readers assume that if

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-69

DECISION CASE 5-10 (Concluded)

5. Both U.S. GAAP and IFRS require the use of the lower-of-cost-or-market rule to

value inventories. However, the two sets of standards differ in two respects. The first

difference is the result of how market value is defined. U.S. GAAP define market