CHAPTER 5

Accounting for Merchandising Operations

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

*1. Describe merchandising

operations and inventory

systems.

2, 3, 4

1, 2

1

1

perpetual inventory system.

inventory system.

*4. Apply the steps in the

1, 12, 13,

6, 7

4

6, 7, 8

3A, 4A, 5A

15, 16, 17,

5

6, 9, 10, 12,

2A, 3A, 5A,

*6. Prepare a worksheet for

11

15, 16

*7. Record purchases and sales

system.

22, 23

12, 13, 14,

17, 18, 19,

20, 21, 22

6A, 7A, 8A

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Journalize purchase and sales transactions under

a perpetual inventory system.

Simple

20–30

Journalize, post, and prepare a partial income statement.

closing entries.

Journalize, post, and prepare a trial balance.

Determine cost of goods sold and gross profit under

40–50

Calculate missing amounts and assess profitability.

income statement using periodic approach.

WEYGANDT FINANCIAL AND MANAGERIAL ACCOUNTING 2E

CHAPTER 5

ACCOUNTING FOR MERCHANDISING OPERATIONS

Number

LO

BT

Difficulty

Time (min.)

BE1

1

AP

Simple

4–6

BE2

1

AP

Simple

4–6

BE3

2, 3

AP

Simple

2–4

BE4

3

AP

Simple

6–8

BE5

2

AP

Simple

6–8

BE6

4

AP

Simple

1–2

BE7

4

AP

Simple

2–4

BE8

5

AP

Simple

2–4

BE9

5

Simple

4–6

BE10

5

AP

Simple

4–6

*BE11

6

Simple

2–4

*BE12

7

AP

Simple

4–6

*BE13

7

AP

Simple

4–6

*BE14

7

AP

Simple

3–5

*BE15

7

AP

Simple

6–8

*BE16

7

AP

Simple

4–6

DI1

1

AP

Simple

2–4

DI2

2

AP

Simple

2–4

DI3

3

AP

Simple

4–6

DI4

4

AP

Simple

4–6

DI5

5

AP

Simple

10–12

EX1

1

Simple

3–5

EX2

2

AP

Simple

EX3

2, 3

AP

Simple

EX4

2, 3

AP

Simple

EX5

3

AP

Simple

EX6

4, 5

AP

Simple

6–8

EX7

4

AP

Simple

6–8

EX8

4

AP

Simple

EX9

5

AP

Simple

EX10

5

AP

Simple

ACCOUNTING FOR MERCHANDISING OPERATIONS (Continued)

Number

LO

BT

Difficulty

Time (min.)

EX12

5

AP

Simple

8–10

EX13

5

AN

Simple

6–8

EX14

5

AN

Moderate

8–10

P1A

2, 3

AP

Simple

20–30

P2A

2, 3, 5

AP

Simple

30–40

P3A

4, 5

AN

Moderate

40–50

P4A

2–4

AP

Simple

30–40

P5A

4–6

AP

Moderate

50–60

P6A

5, 7

AP

Moderate

40–50

P7A

5, 7

Moderate

20–30

*P8A

7

AP

Simple

30–40

5

Simple

10–15

5

Simple

15–20

5

Simple

15–20

AP

Simple

10–15

5

Moderate

20–30

3

Simple

10–15

2

Simple

10–15

Simple

5–10

AP

Moderate

10–15

*EX15

6

AP

Simple

2–4

*EX16

6

AP

Simple

8–10

*EX17

7

AP

Simple

6–8

7

AP

Simple

8–10

7

AN

Moderate

10–12

7

AP

Simple

8–10

*EX21

7

AP

Simple

8–10

*EX22

7

AP

Simple

6–8

BLOOM’ S TAXONOMY TABLE

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

1. Describe merchandising

operations and inventory

systems.

Q5-2

Q5-3

Q5-4

DI5-1

E5-1

DI5-1

BE5-1

BE5-2

2. Record purchases under a

perpetual inventory system.

Q5-5

Q5-6

Q5-7

Q5-8

BE5-3

BE5-5

DI5-2

E5-2

E5-3

E5-4

P5–1A

P5–2A

P5–4A

E5–11

BE5-4

E5-3

P5–4A

a merchandising company.

BE5-11

E5–16

P5–5A

E5–20

E5–21

E5–22

Decision Making Across

Ethics Case

ANSWERS TO QUESTIONS

1. (a) Disagree. The steps in the accounting cycle are the same for both a merchandising company

and a service company.

(b) The measurement of income is conceptually the same. In both types of companies, net

income (or loss) results from the matching of expenses with revenues.

4. Income measurement for a merchandising company differs from a service company as follows:

(a) sales are the primary source of revenue and (b) expenses are divided into two main

categories: cost of goods sold and operating expenses.

5. In a perpetual inventory system, cost of goods sold is determined each time a sale occurs.

Questions Chapter 5 (Continued)

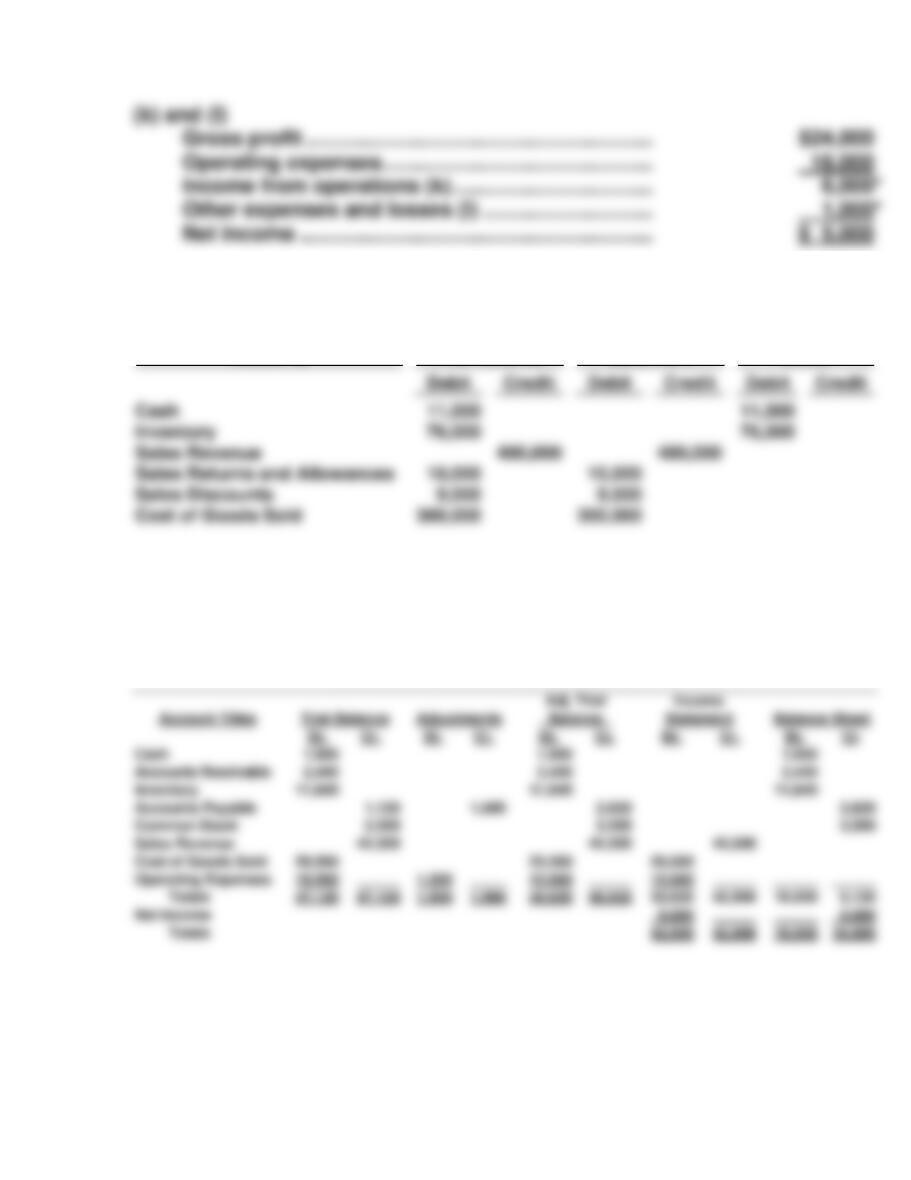

Accounts Receivable ($900 – $100) ………………………… 800

12. The perpetual inventory records for merchandise inventory may be incorrect due to a variety of

causes such as recording errors, theft, or waste.

13. Two closing entries are required:

Questions Chapter 5 (Continued)

*18. (a) The operating activities part of the income statement has three sections: sales revenues,

cost of goods sold, and operating expenses.

*22.

Accounts

Added/Deducted

Purchase Returns and Allowances

Purchase Discounts

Freight-In

Deducted

Deducted

Added

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 5-1

BRIEF EXERCISE 5-2

BRIEF EXERCISE 5-3

BRIEF EXERCISE 5-4

BRIEF EXERCISE 5-5

BRIEF EXERCISE 5-6

Inventory ……………………………………………………. 2,300

BRIEF EXERCISE 5-7

BRIEF EXERCISE 5-8

BRIEF EXERCISE 5-9

BRIEF EXERCISE 5-9 (Continued)

(2) Single-Step Income Statement

BRIEF EXERCISE 5-10

*BRIEF EXERCISE 5-11

*BRIEF EXERCISE 5-12

*BRIEF EXERCISE 5-13

*BRIEF EXERCISE 5-14

*BRIEF EXERCISE 5-15

*BRIEF EXERCISE 5-16

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 5-1

DO IT! 5-2

DO IT! 5-3

DO IT! 5-4

DO IT! 5-5

SOLUTIONS TO EXERCISES

EXERCISE 5-1

EXERCISE 5-2

EXERCISE 5-3

EXERCISE 5-4

EXERCISE 5-4 (Continued)

EXERCISE 5-5

EXERCISE 5-6

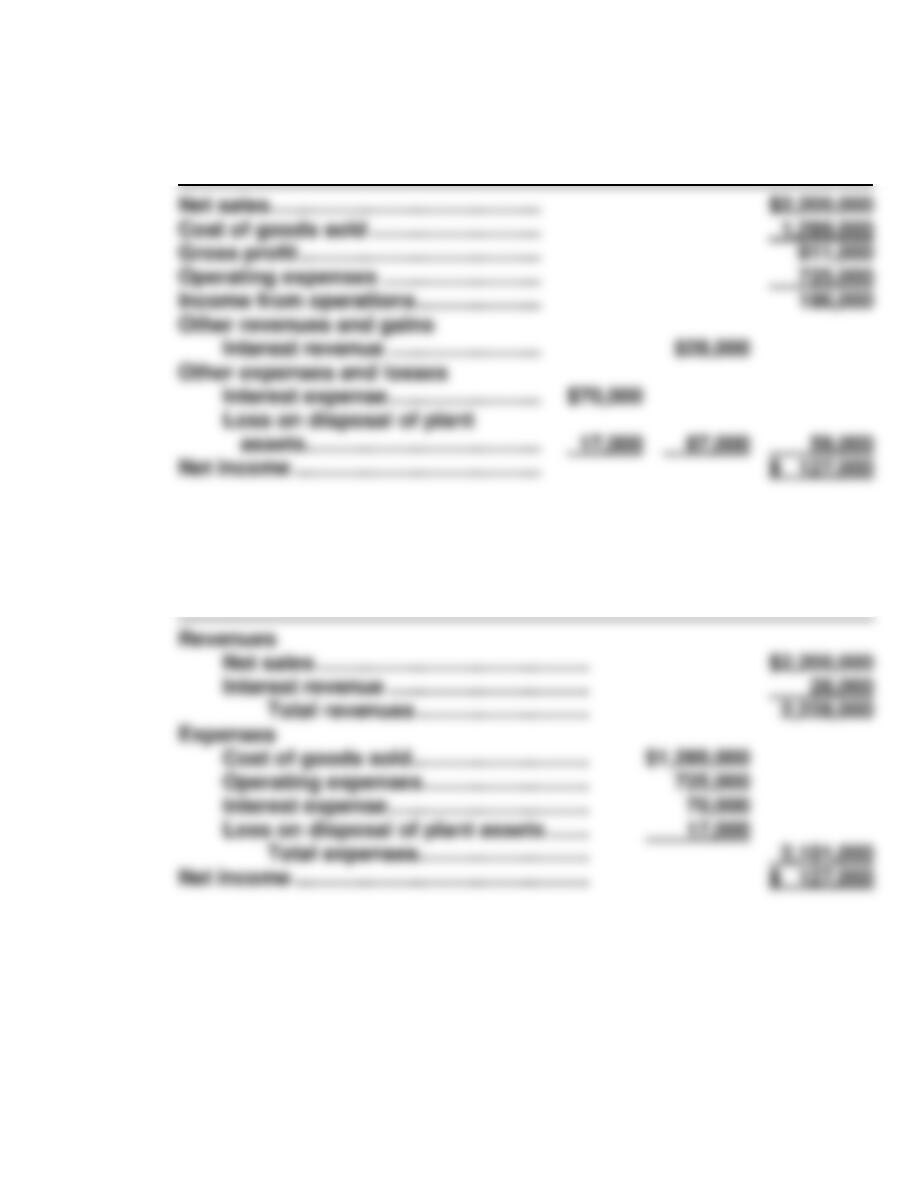

(a) TSAI COMPANY

Income Statement (Partial)

For the Year Ended October 31, 2017

EXERCISE 5-7

EXERCISE 5-8

EXERCISE 5-9

(a) FURLOW COMPANY

Income Statement

For the Month Ended March 31, 2017

EXERCISE 5-10

(a) LEMERE COMPANY

Income Statement

For the Year Ended December 31, 2017

(b) LEMERE COMPANY

Income Statement

For the Year Ended December 31, 2017

EXERCISE 5-11

EXERCISE 5-12

EXERCISE 5-13

EXERCISE 5-14

(*Missing amount)

EXERCISE 5-14 (Continued)

*EXERCISE 5-15

Accounts

Adjusted

Trial Balance

Income

Statement

Balance

Sheet

Sales Discounts

*EXERCISE 5-16

MARQUEZ COMPANY

Worksheet

For the Month Ended June 30, 2017

*EXERCISE 5-17

*EXERCISE 5-18

*EXERCISE 5-19

*EXERCISE 5-20

*EXERCISE 5-21

*EXERCISE 5-22

Accounts

Adjusted

Trial Balance

Income

Statement

Balance

Sheet

PROBLEM 5-1A

PROBLEM 5-1A (Continued)

PROBLEM 5-2A

(a)

General Journal J1

Date

Account Titles and Explanation

Ref.

Debit

Credit

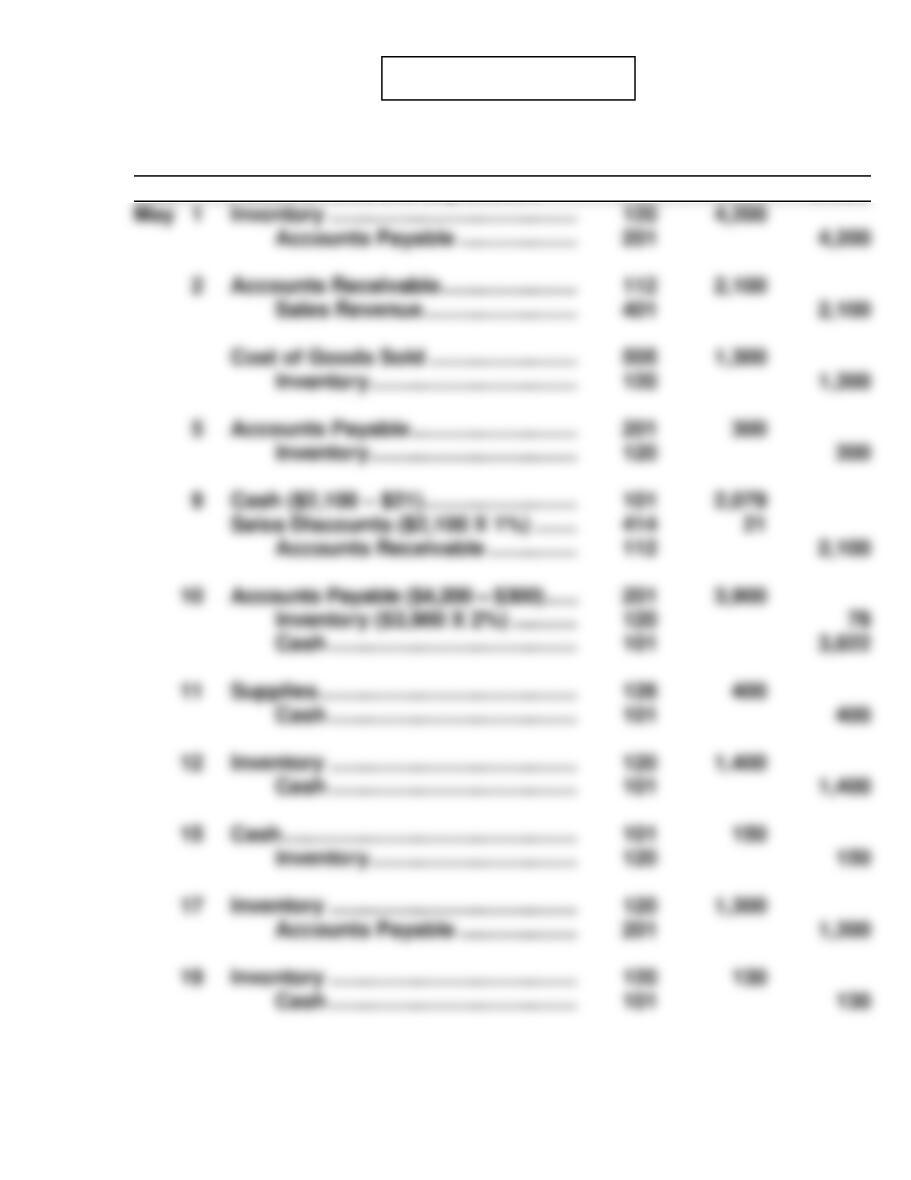

Accounts Payable ………………..

Inventory ……………………………..

Inventory ……………………………..

Accounts Receivable ……………

PROBLEM 5-2A (Continued)

General Journal J1

PROBLEM 5-2A (Continued)

(b)

Cash No. 101

Date

Explanation

Ref.

Debit

Credit

Balance

Accounts Receivable No. 112

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Ref.

Debit

Credit

Balance

PROBLEM 5-2A (Continued)

Supplies No. 126

Date

Explanation

Ref.

Debit

Credit

Balance

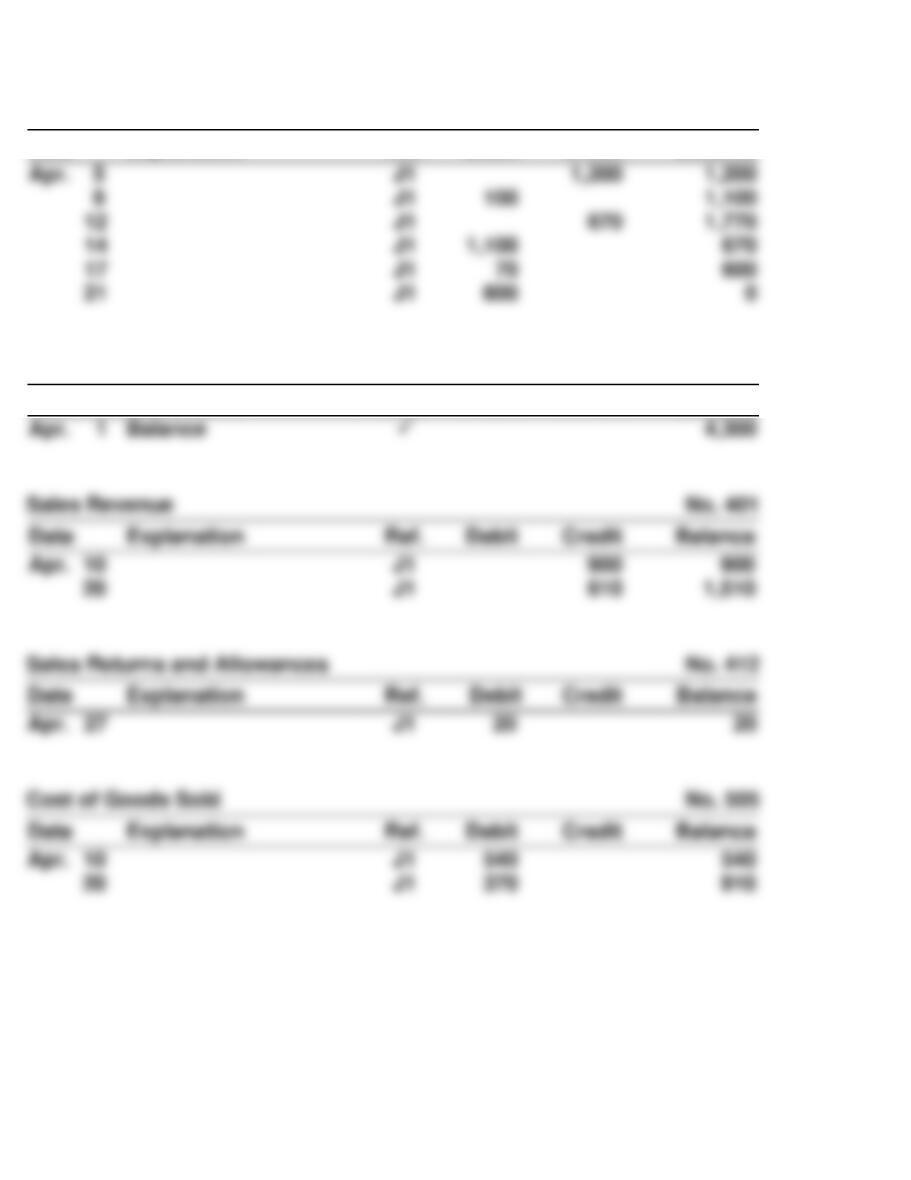

Sales Revenue No. 401

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Debit

Balance

Date

Explanation

Ref.

Debit

Date

Explanation

Debit

Credit

Balance

PROBLEM 5-2A (Continued)

Cost of Goods Sold No. 505

Date

Explanation

Ref.

Debit

Credit

Balance

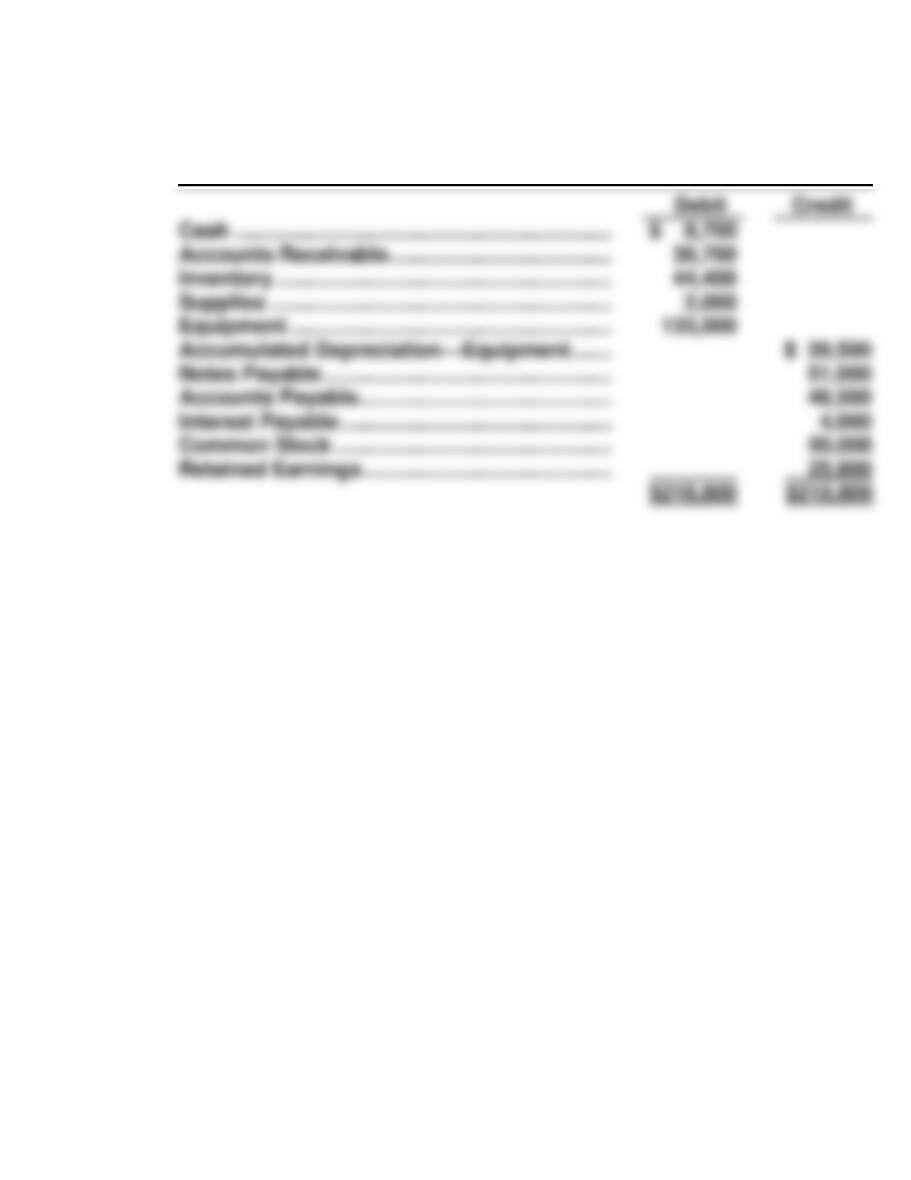

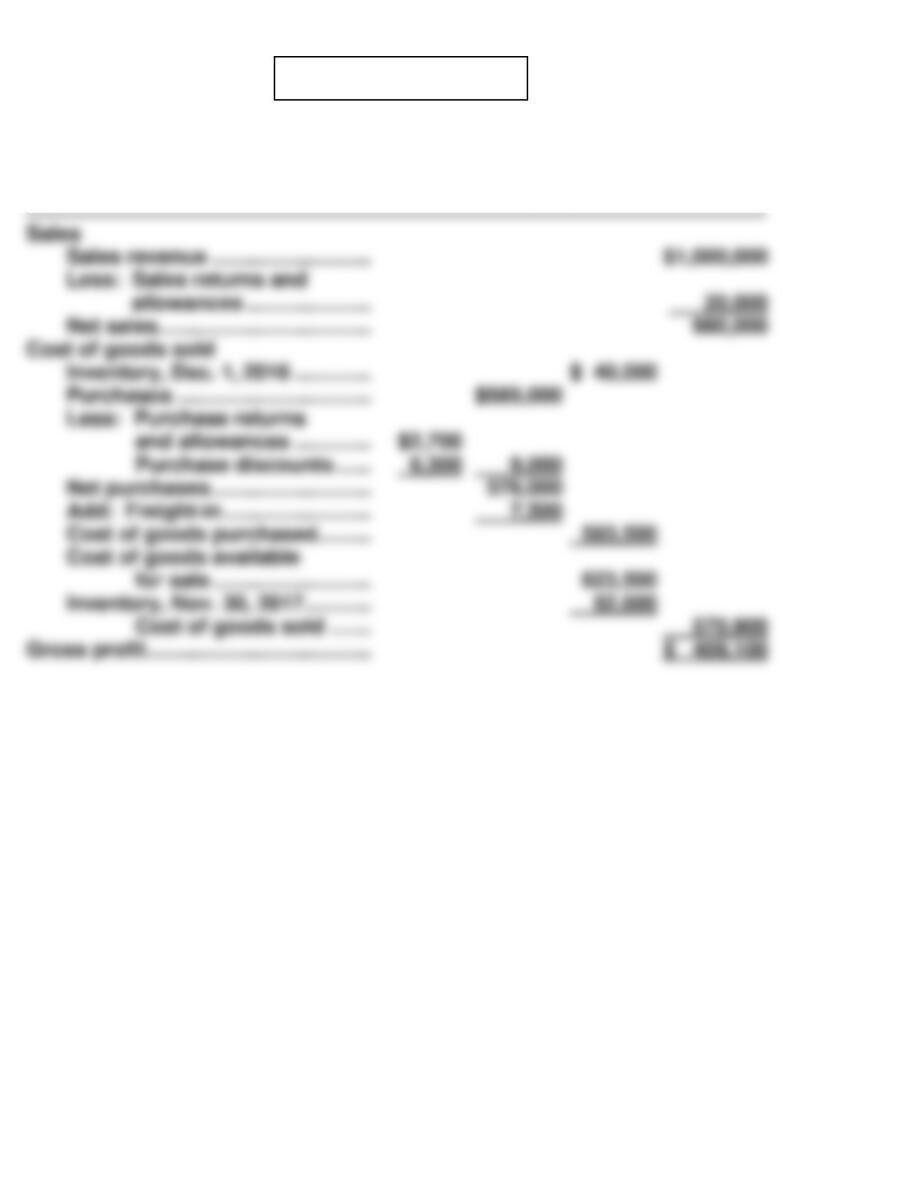

PROBLEM 5-3A

(a) THE DELUXE STORE

Income Statement

For the Year Ended November 30, 2017

PROBLEM 5-3A (Continued)

THE DELUXE STORE

Retained Earnings Statement

For the Year Ended November 30, 2017

PROBLEM 5-3A (Continued)

THE DELUXE STORE

Balance Sheet (Continued)

November 30, 2017

PROBLEM 5-3A (Continued)

PROBLEM 5-4A

(a)

General Journal J1

Date

Account Titles and Explanation

Ref.

Debit

Credit

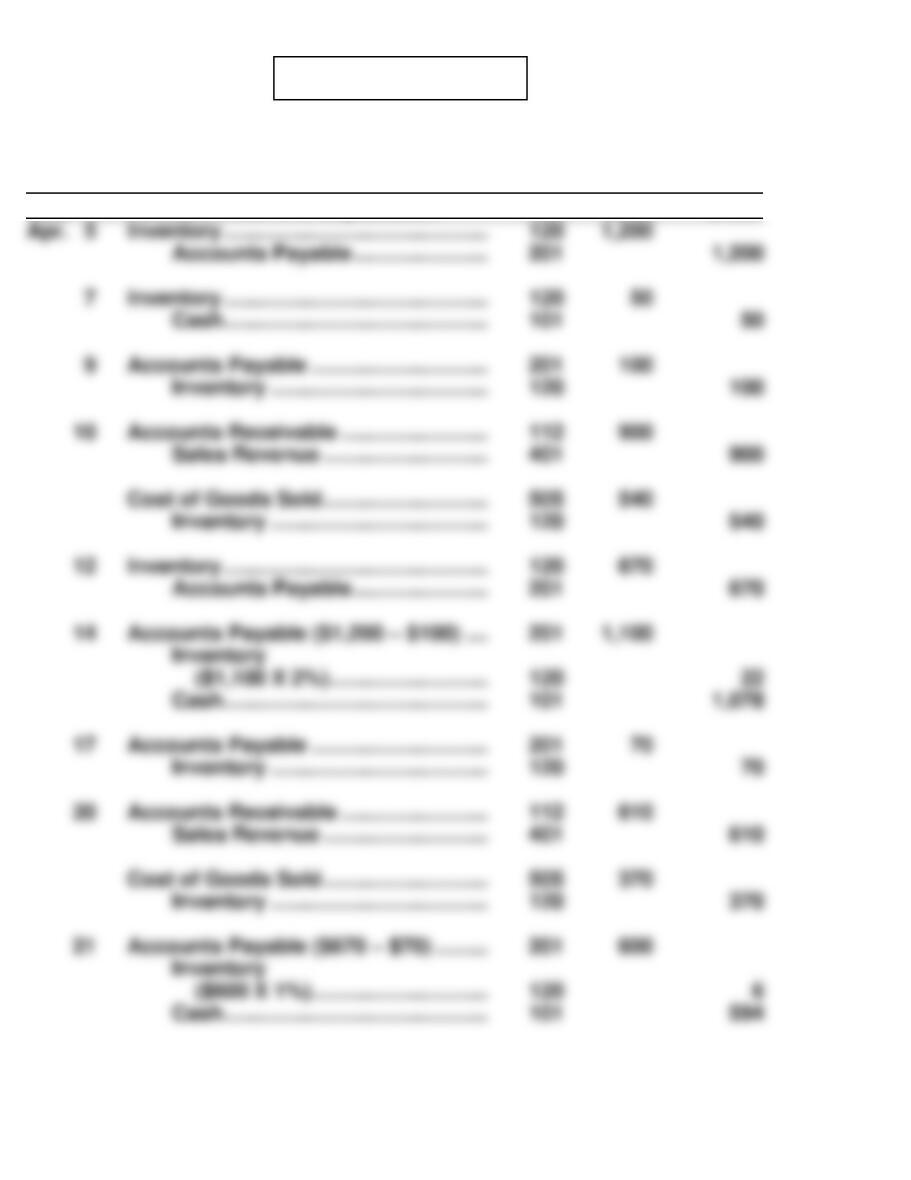

PROBLEM 5-4A (Continued)

J1

Date

Account Titles and Explanation

Ref.

Debit

Credit

(b)

Cash No. 101

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Ref.

Debit

Credit

Balance

Accounts Receivable …………..

PROBLEM 5-4A (Continued)

Accounts Payable No. 201

Date

Explanation

Ref.

Debit

Credit

Balance

Common Stock No. 311

Date

Explanation

Ref.

Debit

Credit

Balance

Date

Explanation

Ref.

Debit

Credit

Balance

PROBLEM 5-4A (Continued)

(c) ADAM’S DISCORAMA

Trial Balance

April 30, 2017

(a) VALDEZ FASHION CENTER

Worksheet

For the Year Ended November 30, 2017

Adjusted

Income

Key: (a) Store supplies used, (b) Depreciation expense—equipment, (c) Accrued interest payable, (d) Adjustment of inventory.

*PROBLEM 5-5A (Continued)

(b) VALDEZ FASHION CENTER

Income Statement

For the Year Ended November 30, 2017

*PROBLEM 5-5A (Continued)

VALDEZ FASHION CENTER

Retained Earnings Statement

For the Year Ended November 30, 2017

VALDEZ FASHION CENTER

Balance Sheet

November 30, 2017

*PROBLEM 5-5A (Continued)

VALDEZ FASHION CENTER

Balance Sheet (Continued)

November 30, 2017

*PROBLEM 5-5A (Continued)

*PROBLEM 5-5A (Continued)

(e) VALDEZ FASHION CENTER

Post-Closing Trial Balance

November 30, 2017

*PROBLEM 5-6A

DAYTON DEPARTMENT STORE

Income Statement (Partial)

For the Year Ended November 30, 2017

*PROBLEM 5-7A

*PROBLEM 5-7A (Continued)

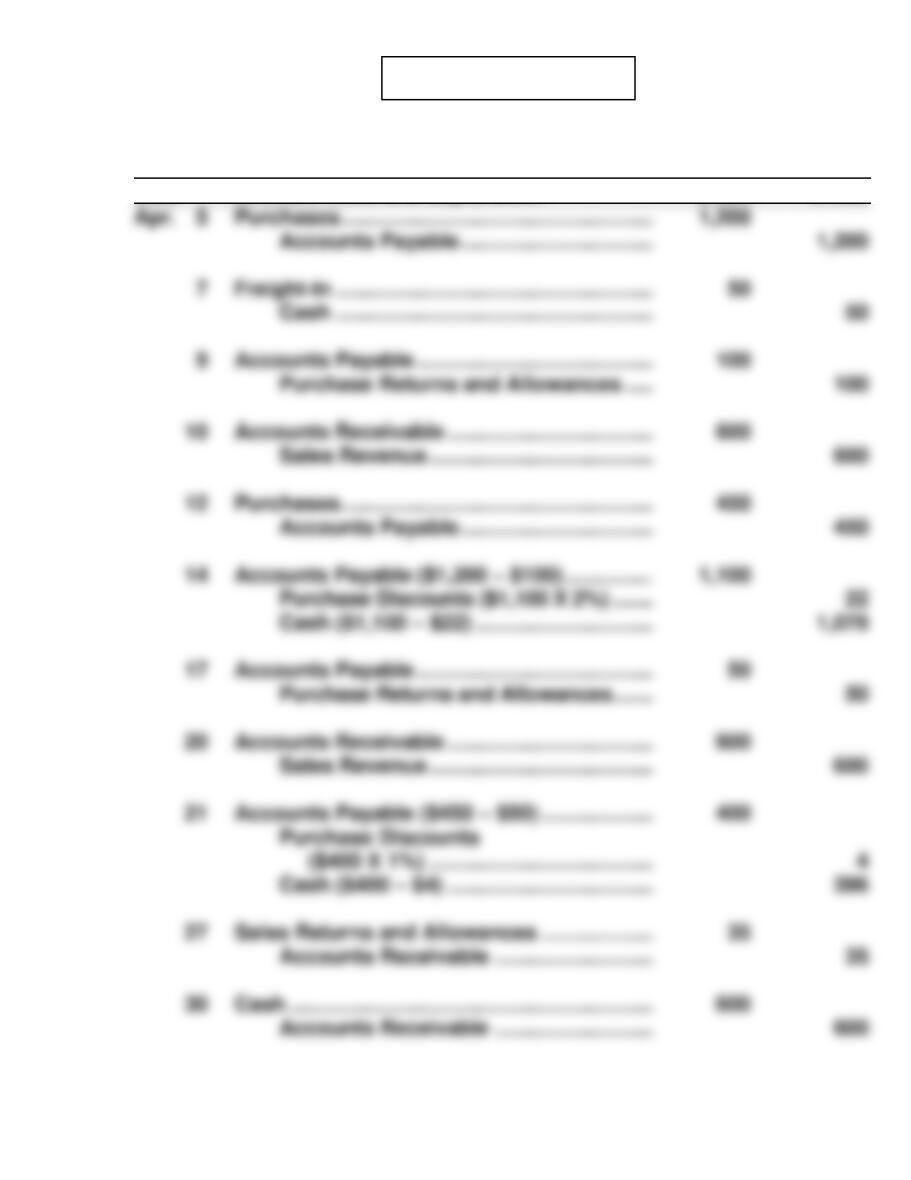

*PROBLEM 5-8A

(a)

General Journal

Date

Account Titles and Explanation

Debit

Credit

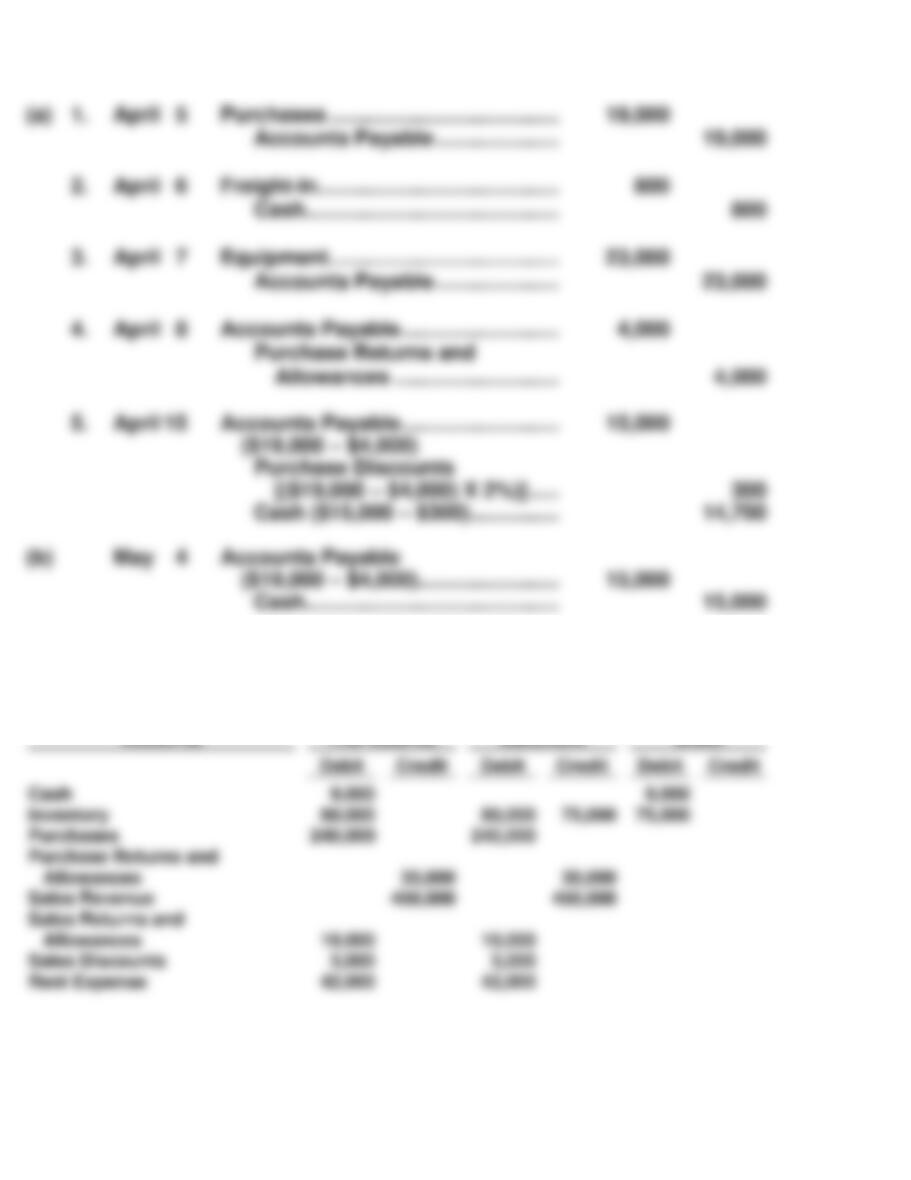

Accounts Payable …………………………...

1,200

Cash ………………………………………………

Purchase Returns and Allowances …..

Sales Revenue ………………………………..

600

Accounts Payable …………………………...

450

Cash ($400 – $4) ……………………………..

396

Accounts Receivable ………………………

Accounts Receivable ………………………

*PROBLEM 5-8A (Continued)

(b)

Cash

Sales Revenue

4/30 Bal. 35

4/1 Bal. 4,000

4/12 450

*PROBLEM 5-8A (Continued)

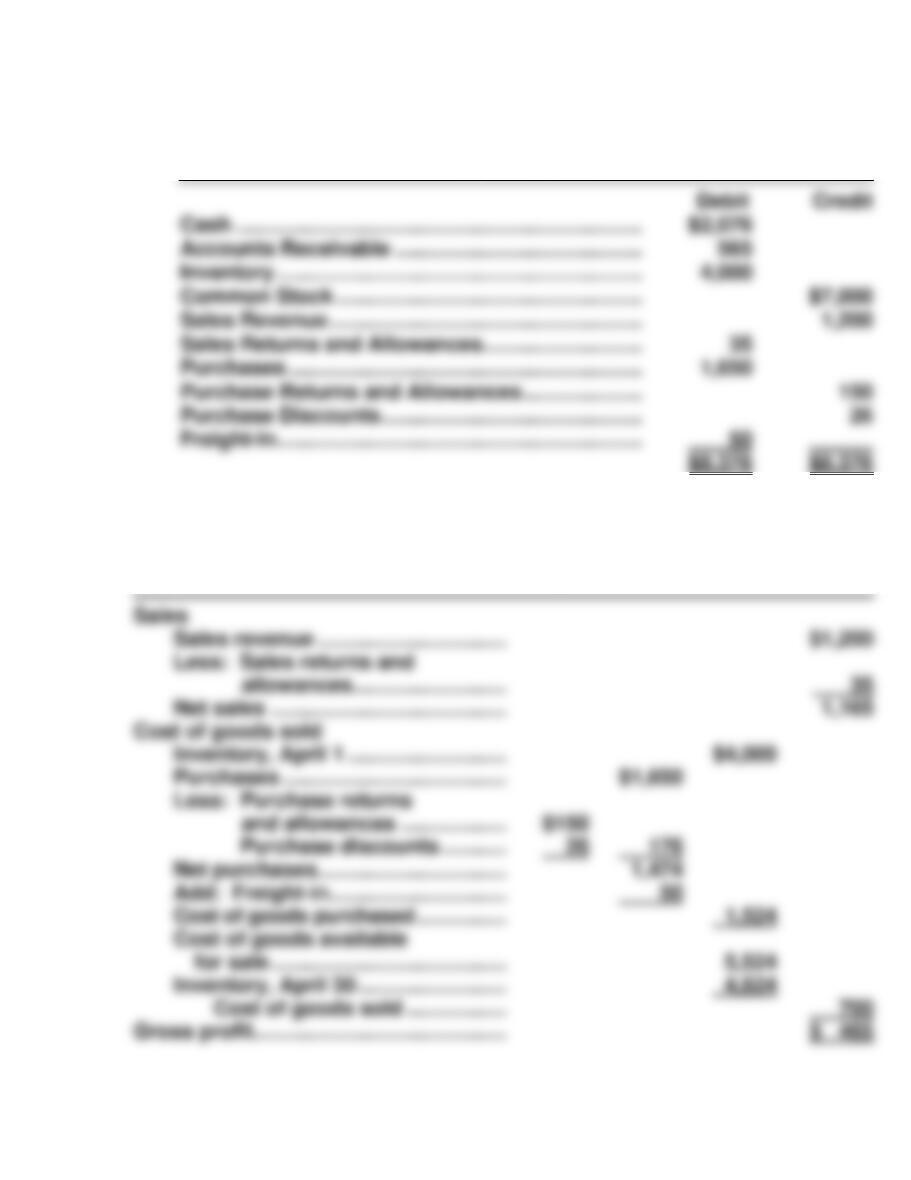

(c) KOKOTT PRO SHOP

Trial Balance

April 30, 2017

(d) KOKOTT PRO SHOP

Income Statement (Partial)

For the Month Ended April 30, 2017

COMPREHENSIVE PROBLEM SOLUTION

COMPREHENSIVE PROBLEM SOLUTION (Continued)

(b) & (c) General Ledger

Cash

12/23 180

12/15 2,000

12/1 Bal. 22,000

12/31 Bal. 2,400

12/31 Bal. 4,500

12/31 Bal. 800

Salaries and Wages Payable …………….

Equipment …………………………………….

Supplies ($3,200 – $1,500) ………………..

COMPREHENSIVE PROBLEM SOLUTION (Continued)

Common Stock

Cost of Goods Sold

COMPREHENSIVE PROBLEM SOLUTION (Continued)

(d) PROSEN DISTRIBUTING COMPANY

Adjusted Trial Balance

December 31, 2017

(e) PROSEN DISTRIBUTING COMPANY

Income Statement

For the Month Ending December 31, 2017

COMPREHENSIVE PROBLEM SOLUTION (Continued)

PROSEN DISTRIBUTING COMPANY

Retained Earnings Statement

For the Month Ended December 31, 2017

PROSEN DISTRIBUTING COMPANY

Balance Sheet

December 31, 2017

BYP 5-1 FINANCIAL REPORTING PROBLEM

2012

2013

2013 ($170,910 – $106,606) ÷ $170,910

2013 ($37,037 ÷ $170,910)

BYP 5-2 COMPARATIVE ANALYSIS PROBLEM

PepsiCo

Coca-Cola

BYP 5-3 COMPARATIVE ANALYSIS PROBLEM

Amazon

Wal-Mart

BYP 5-4 REAL-WORLD FOCUS

BYP 5-5 DECISION MAKING ACROSS THE ORGANIZATION

(a) (1) FAMILY DEPARTMENT STORE

Income Statement

For the Year Ended December 31, 2017

(2) FAMILY DEPARTMENT STORE

Income Statement

For the Year Ended December 31, 2017

BYP 5-5 (Continued)

(c) FAMILY DEPARTMENT STORE

Income Statement

For the Year Ended December 31, 2017

BYP 5-6 COMMUNICATION ACTIVITY

(a), (b)

President

Surfing USA Co.

Dear Sir:

BYP 5-7 ETHICS CASE

(a) Jacquie Boynton, as a new employee, is placed in a position of res-

(c) Jacquie’s alternatives:

BYP 5-8 ALL ABOUT YOU

BYP 5-9 FASB CODIFICATION ACTIVITY

(a) (1) Inventory is the aggregate of those items of tangible personal

(2) A customer is a reseller or a consumer, either an individual or a

BYP 5-9 (Continued)

IFRS EXERCISES

IFRS5-1

IFRS5-2

IFRS5-3

MATILDA COMPANY

Comprehensive Income Statement

For the Year Ended 2017

INTERNATIONAL FINANCIAL REPORTING PROBLEM

IFRS5-4