5-1

CHAPTER 5

Inventories and

Cost of Goods Sold

OVERVIEW OF EXERCISES, PROBLEMS, AND CASES

Estimated

Time in

Learning Objectives Exercises Minutes Level

Module 1

1. Identify the forms of inventory held by different types of 1 10 Easy

businesses and the types of costs incurred. 2 10 Mod

6 20 Mod

7 20 Mod

8 15 Mod

14 20 Mod

20* 25 Mod

21* 15 Mod

22* 10 Mod

26* 10 Mod

4. Use the gross profit ratio to analyze a company’s ability 9 10 Mod

to cover its operating expenses and earn a profit. 23* 10 Mod

Module 2

24* 25 Mod

7. Analyze the effects of the different costing methods on 12 15 Mod

inventory, net income, income taxes, and cash flow. 24* 25 Mod

27* 40 Mod

Module 3

8. Analyze the effects of an inventory error on various financial 13 25 Mod

statement items.

5-2 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

Estimated

Time in

Learning Objectives (Continued) Exercises Minutes Level

Module 4

10. Analyze the management of inventory. 15 20 Mod

16 10 Diff

Module 5

12. Explain the differences in the accounting for periodic and 27* 40 Mod

perpetual inventory systems and apply the inventory

costing methods using a perpetual system (Appendix).

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-3

Problems Estimated

and Time in

Learning Objectives Alternates Minutes Level

Module 1

1. Identify the forms of inventory held by different types of 1 25 Mod

businesses and the types of costs incurred. 14* 20 Mod

to cover its operating expenses and earn a profit. 8* 40 Mod

Module 2

5. Explain the relationship between the valuation of inventory 10* 45 Mod

and the measurement of income. 11* 60 Diff

12* 30 Mod

13* 30 Mod

Module 3

8. Analyze the effects of an inventory error on various financial 4 45 Diff

statement items. 14** 20 Mod

Module 4

10. Analyze the management of inventory. 5 30 Mod

Module 5

12. Explain the differences in the accounting for periodic and 11* 60 Diff

perpetual inventory systems and apply the inventory

costing methods using a perpetual system (Appendix).

5-4 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

Estimated

Time in

Learning Objectives Cases Minutes Level

Module 1

1. Identify the forms of inventory held by different types of 1* 25 Mod

businesses and the types of costs incurred.

2. Explain how wholesalers and retailers account for 4* 20 Mod

sales of merchandise. 5* 20 Mod

Module 2

5. Explain the relationship between the valuation of inventory

and the measurement of income.

9 30 Mod

Module 3

8. Analyze the effects of an inventory error on various financial 8 30 Mod

statement items.

Module 4

10. Analyze the management of inventory.

Module 5

12. Explain the differences in the accounting for periodic and

perpetual inventory systems and apply the inventory

costing methods using a perpetual system (Appendix).

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-5

EXERCISES

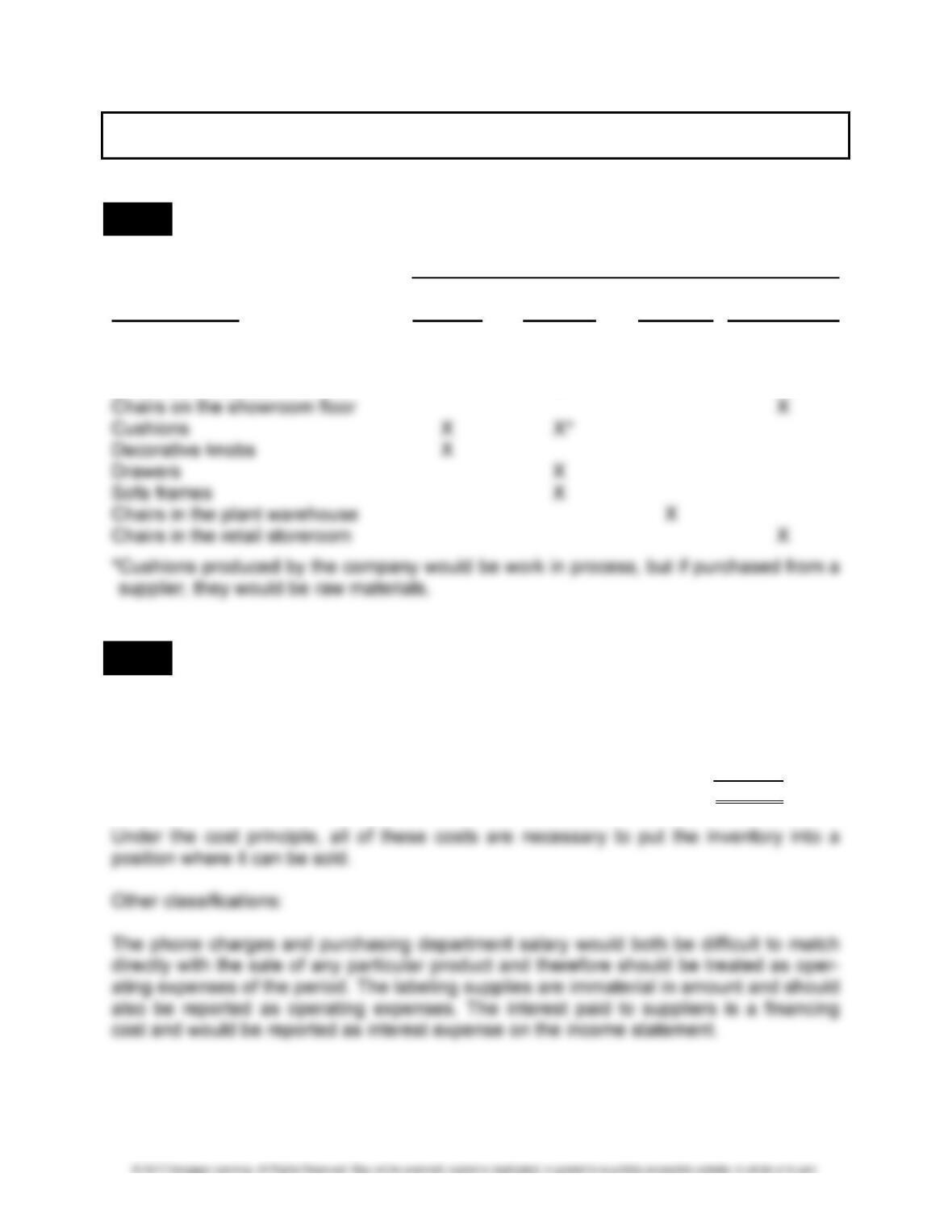

LO 1 EXERCISE 5-1 CLASSIFICATION OF INVENTORY COSTS

Classification

Raw Work in Finished Merchandise

Inventory Item Material Process Goods Inventory

Fabric X

Lumber X

Unvarnished tables X

LO 1 EXERCISE 5-2 INVENTORIABLE COSTS

List price: $100 × 200 units ……………………………………………………… $20,000

10% volume discount ……………………………………………………………… (2,000)

Freight costs ………………………………………………………………………….. 56

Insurance for goods in transit …………………………………………………… 32

Total cost …………………………………………………………………………. $18,088

5-6 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 2 EXERCISE 5-3 PERPETUAL AND PERIODIC INVENTORY SYSTEMS

1. Company A is using a perpetual inventory system because it has the account Cost of

Goods Sold. Company B is using the periodic inventory system because it uses the

accounts Purchases and Transportation-in.

LO 2 EXERCISE 5-4 PERPETUAL AND PERIODIC INVENTORY SYSTEMS

Perpetual—Appliance store

Perpetual—Car dealership

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-7

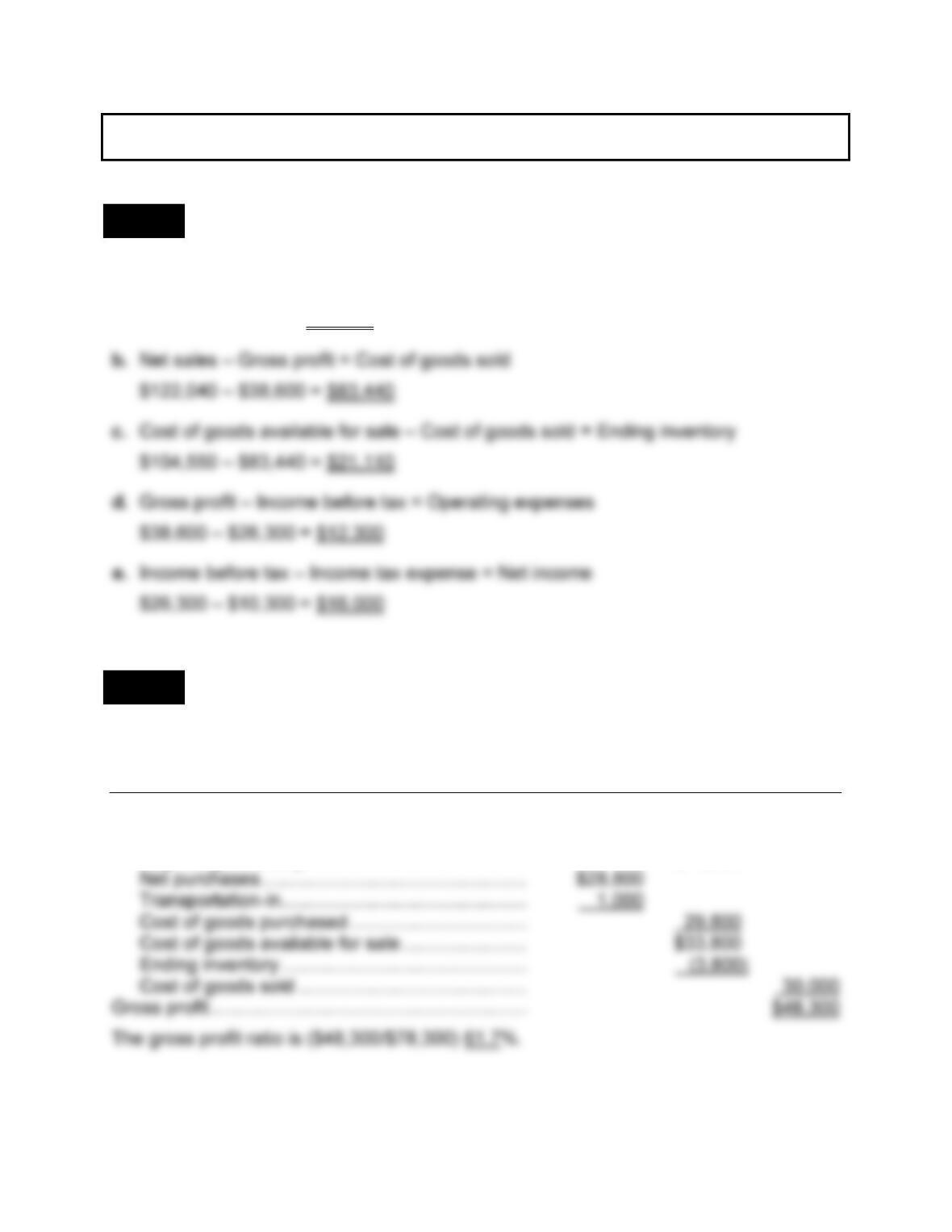

LO 3 EXERCISE 5-5 MISSING AMOUNTS IN COST OF GOODS SOLD MODEL

Case 1:

(a) Beginning inventory: cost of goods available for sale – cost of goods purchased =

$7,110 – ($5,560 + $150) = $7,110 – $5,710 = $1,400

Case 2: [must first solve (d), then (c)]

(d) Cost of goods available for sale: cost of goods sold + ending inventory = $5,570 +

$1,750 = $7,320

Case 3:

(e) Net purchases:

5-8 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 3 EXERCISE 5-6 PURCHASE DISCOUNTS

Journal July 3 Purchases ………………………………………. 3,465

Entry Accounts Payable ……………………….. 3,465

Journal July 12 Accounts Payable ……………………………. 3,465

Entry Cash …………………………………………. 3,465

Analysis To record payment on account.

LO 3 EXERCISE 5-7 SHIPPING TERMS AND TRANSFER OF TITLE

1. The seller pays shipping costs when merchandise is shipped FOB destination point.

2. The inventory should not be included as an asset on Michael’s December 31, 2016,

balance sheet because the terms of shipment indicate that the merchandise does

3. If the terms of shipment were FOB shipping point, the answers to both questions in

part (2) above would change. Under these terms, the inventory belongs to Michael

as soon as it is shipped, and because this is on December 23, 2016, the asset

should be recognized on the year-end balance sheet. Similarly, Miller would record a

sale in 2016.

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-9

LO 3 EXERCISE 5-8 TRANSFER OF TITLE TO INVENTORY

Purchases of merchandise that are in transit from vendors to Cameron Companies on

December 31, 2016:

LO 4 EXERCISE 5-9 WORKING BACKWARD: GROSS PROFIT RATIO

The prior year’s gross profit ratio was ($120,000 – $90,000)/$120,000 = 25%. The ratio

LO 5 EXERCISE 5-10 INVENTORY AND INCOME MANIPULATION

By ignoring the large order at year-end, and thus including the inventory in the year-end

count, the company will overstate ending inventory. This in turn will lead to an under-

5-10 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

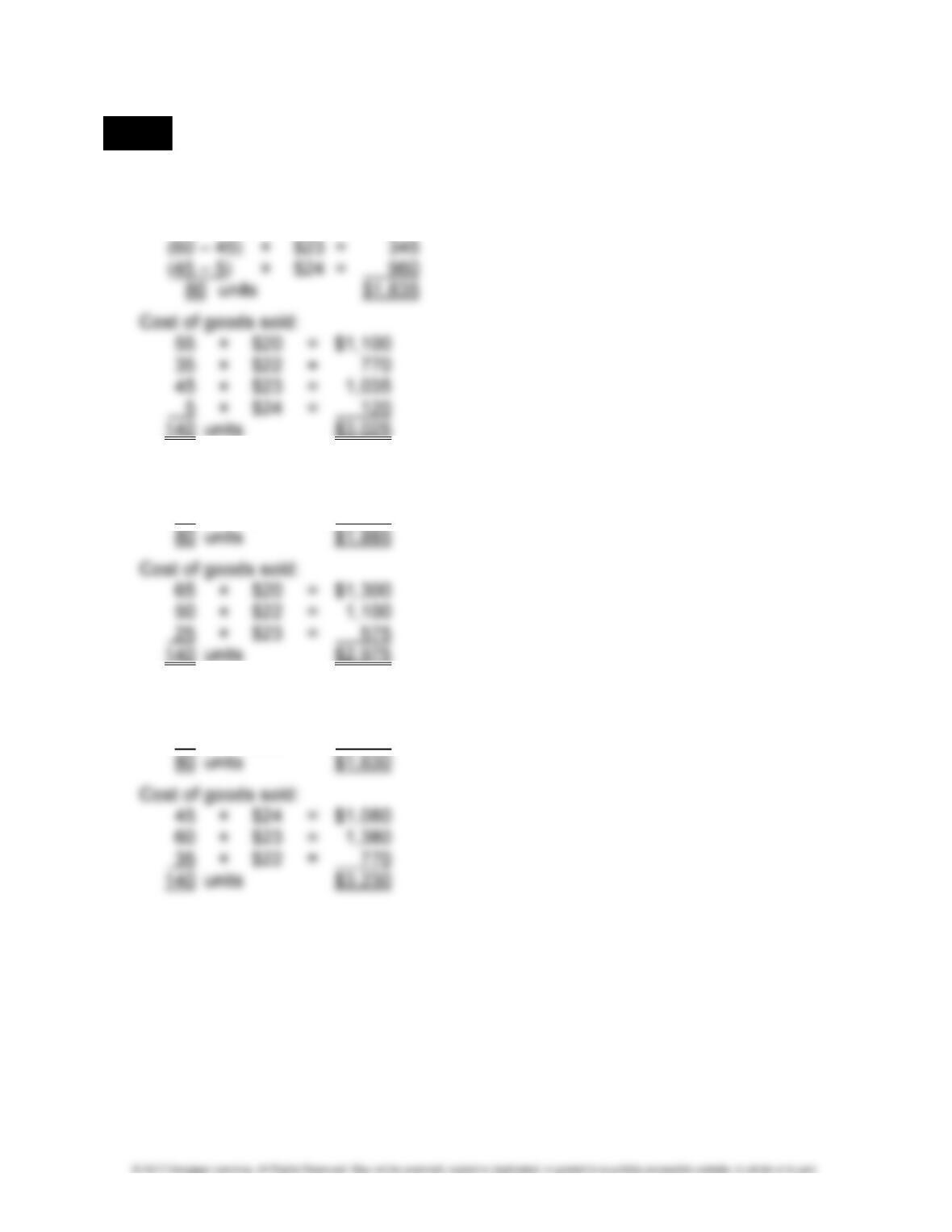

LO 6 EXERCISE 5-11 INVENTORY COSTING METHODS

1. Ending inventory:

(65 – 55) × $20 = $ 200

(50 – 35) × $22 = 330

2. Ending inventory:

45 × $24 = $1,080

35 × $23 = 805

3. Ending inventory:

65 × $20 = $1,300

15 × $22 = 330

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-11

EXERCISE 5-11 (Concluded)

4. Cost of goods available for sale and units available:

65 × $20 = $1,300

50 × $22 = 1,100

60 × $23 = 1,380

LO 7 EXERCISE 5-12 EVALUATION OF INVENTORY COSTING METHODS

1. a 4. c 7. b

LO 8 EXERCISE 5-13 INVENTORY ERRORS

Balance Sheet Income Statement

Retained Cost of Net

Inventory Earnings Goods Sold Income

1. U U O U

2. O O U O

3. U U O U

Hint: To summarize, if ending inventory is understated, then cost of goods sold is over-

5-12 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 3 EXERCISE 5-14 TRANSFER OF TITLE TO INVENTORY

1. Michelson should include the costs in its inventory since the merchandise had not

arrived at its destination, PJ’s, by the end of the year and it belongs to Michelson

until arrival.

LO 10 EXERCISE 5-15 INVENTORY TURNOVER FOR NORDSTROM

1. Inventory turnover for 2013 = Cost of goods sold/Average inventory = $7,737/

[($1,531 + $1,360)/2] = $7,737/$1,445.5 = 5.35 times

LO 10 EXERCISE 5-16 WORKING BACKWARD: INVENTORY TURNOVER

If it takes the company 90 days to sells its inventory, the inventory turnover ratio is

360/90 = 4 times per year. The inventory turnover ratio is:

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-13

LO 11 EXERCISE 5-17 IMPACT OF TRANSACTIONS INVOLVING INVENTORIES ON

STATEMENT OF CASH FLOWS

Increase in accounts payable: A

LO 11 EXERCISE 5-18 EFFECTS OF TRANSACTIONS INVOLVING INVENTORIES ON THE

STATEMENT OF CASH FLOWS—DIRECT METHOD

Cash payments for inventory to be reported in the operating activities of Masthead’s

2016 statement of cash flows (direct method):

Inventory, December 31, 2015 ………………………………………….. $ 180,400

Purchases during 2016 ……………………………………………………. X

LO 11 EXERCISE 5-19 EFFECTS OF TRANSACTIONS INVOLVING INVENTORIES ON THE

STATEMENT OF CASH FLOWS—INDIRECT METHOD

Cash flows from operating activities:

Net income ……………………………………………………………… $ xx,xxx

5-14 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

© 2017 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

MULTI-CONCEPT EXERCISES

LO 2,3 EXERCISE 5-20 INCOME STATEMENT FOR A MERCHANDISER

a. Cost of goods purchased – Transportation-in = Net purchases

$81,150 – $6,550 = $74,600

LO 2,3 EXERCISE 5-21 PARTIAL INCOME STATEMENT—PERIODIC SYSTEM

LAPINE COMPANY

INCOME STATEMENT

FOR THE YEAR ENDED DECEMBER 31, 2016

Net sales ………………………………………………………. $78,300

Cost of goods sold:

Beginning inventory …………………………………… $ 4,000

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-15

LO 3,6 EXERCISE 5-22 COST OF GOODS SOLD, FIFO, AND LIFO

Cost of goods available for sale:

200 units × $5 = $1,000

LO 4,6 EXERCISE 5-23 WEIGHTED AVERAGE COST METHOD AND GROSS PROFIT

RATIO

1. Beginning inventory 2,000 units × $ 6 = $ 12,000

Purchases:

5,000 units × $ 8 = 40,000

8,000 units × $10 = 80,000

2. Sales = $15 × 9,000 units = $135,000

Cost of goods sold expense (from above) 79,200

5-16 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 6,7 EXERCISE 5-24 INVENTORY COSTING METHODS—PERIODIC SYSTEM

1. a. Weighted average method:

Cost of goods available for sale and units available:

200 × $10 = $ 2,000

300 × $11 = 3,300

400 × $12 = 4,800

b. FIFO method:

Ending inventory cost:

150 × $15 = $2,250

150 × $13 = 1,950

300 $4,200

c. LIFO method:

Ending inventory cost:

200 × $10 = $2,000

100 × $11 = 1,100

300 $3,100

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-17

EXERCISE 5-24 (Concluded)

2. LIFO cost of goods sold …………………………………… $12,500

FIFO cost of goods sold …………………………………… 11,400

Difference in expenses ……………………………………. $ 1,100

3. If Carter Inc. prepares its financial statements in accordance with IFRS, it is not

allowed to use LIFO. Under IFRS, LIFO cannot be used; so the weighted average

method will result in the largest cost of goods sold, the lowest income, and conse-

quently the lowest income tax for Carter.

LO 5,9 EXERCISE 5-25 LOWER-OF-COST-OR-MARKET RULE

Conservatism is the rationale for carrying inventory on the balance sheet at an amount

less than its cost. It is a departure from the historical cost principle and is used when the

utility of the inventory, as measured by the cost to replace it, is less than the original

cost.

LO 3,11 EXERCISE 5-26 WORKING BACKWARD: COST OF GOODS SOLD AND THE

STATEMENT OF CASH FLOWS

Because the change in the Inventory account during the period of $6,000 was added on

the statement of cash flows, the inventory decreased during the period by this amount.

5-18 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

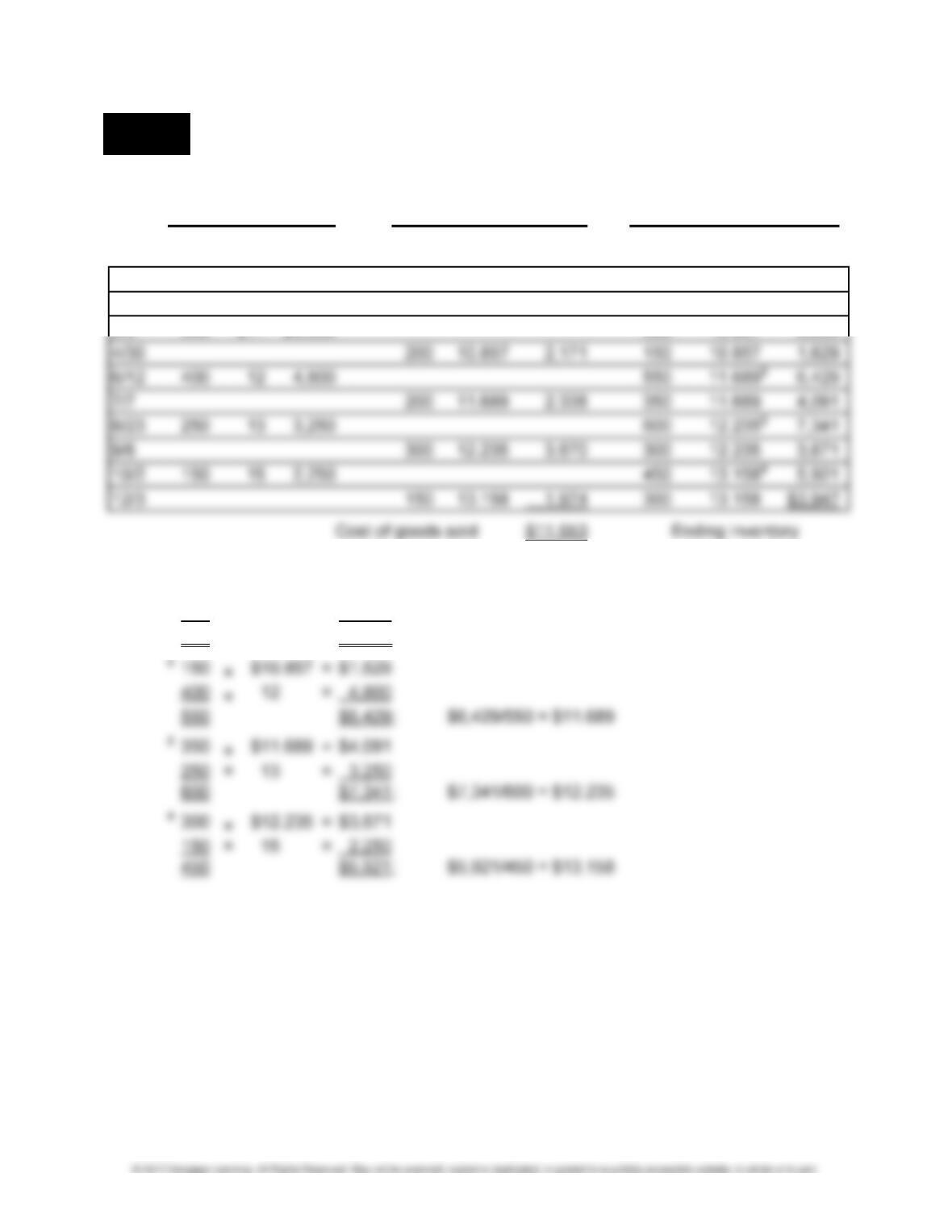

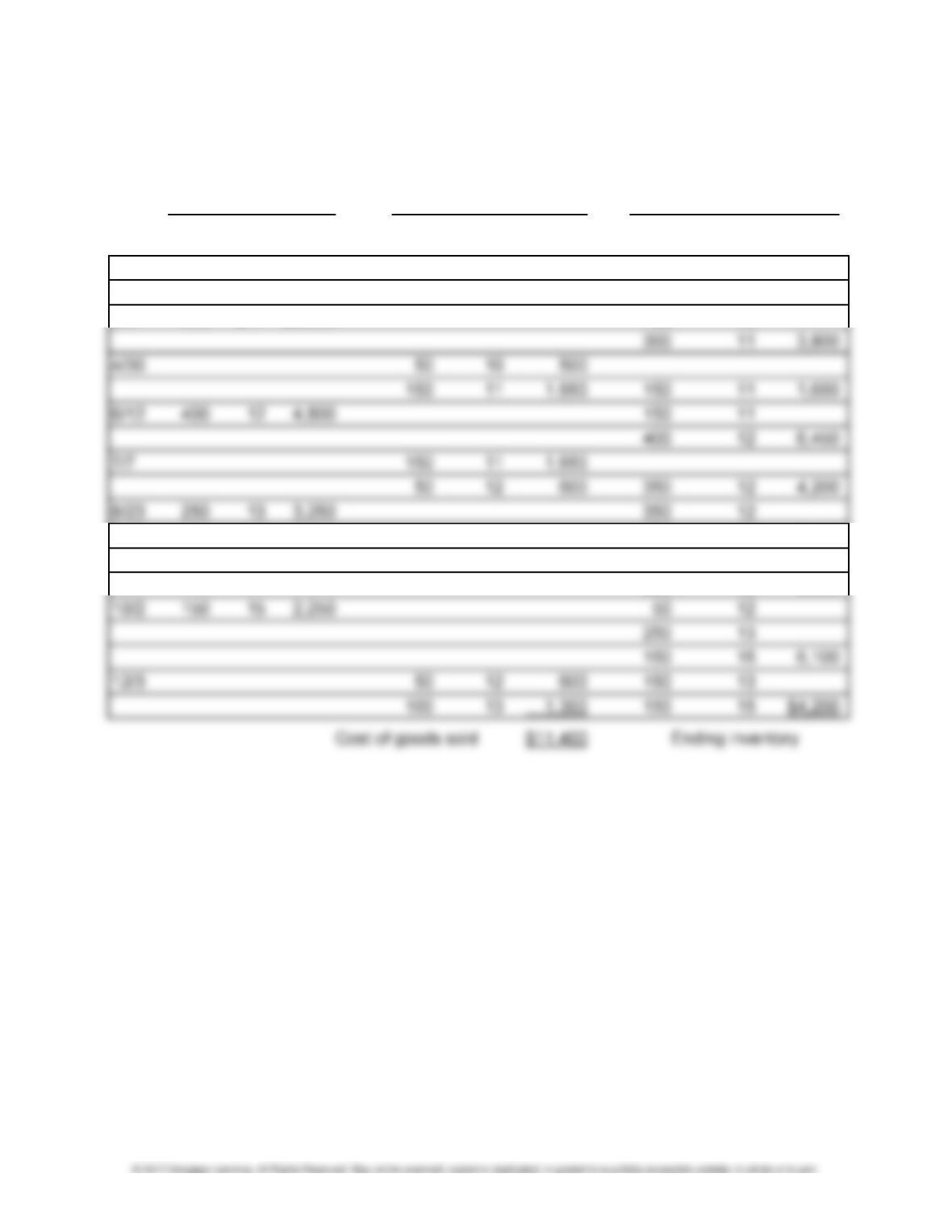

LO 7,12 EXERCISE 5-27 INVENTORY COSTING METHODS—PERPETUAL SYSTEM

(Appendix)

1. a. Moving average:

Purchases

Sales Balance

Unit Total Unit Total Unit

Date Units Cost Cost Units Cost Cost Units Cost Balance

1/1 200 $10 $2,000

2/12 150 $10 $ 1,500 50 10 500

3/5 300 $11 $3,300 350 10.8571 3,800

All amounts rounded to agree with total cost.

1 50 × $10 = $ 500

300 × 11 = 3,300

350 $ 3,800; $3,800/350 = $10.857

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-19

EXERCISE 5-27 (Continued)

1. b. FIFO:

Purchases

Sales Balance

Unit Total Unit Total Unit

Date Units Cost Cost Units Cost Cost Units Cost Balance

1/1 200 $10 $2,000

2/12 150 $10 $ 1,500 50 10 500

3/5 300 $11 $3,300 50 10

250 13 7,450

9/6 300 12 3,600 50 12

250 13 3,850

5-20 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

EXERCISE 5-27 (Continued)

1. c. LIFO:

Purchases

Sales Balance

Unit Total Unit Total Unit

Date Units Cost Cost Units Cost Cost Units Cost Balance

1/1 $200 $10 $2,000

2/12 150 $10 $ 1,500 50 10 500

3/5 300 $11 $3,300 50 10

100 11

200 12 4,000

8/23 250 13 3,250 50 10

100 11

200 12

250 13 7,250

2. EXERCISE 5-24: EXERCISE 5-27:

E/I CGS E/I CGS

Average cost $3,600 $12,000 $3,947 $11,653 Different

FIFO 4,200 11,400 4,200 11,400 Same

LIFO 3,100 12,500 3,400 12,200 Different