Chapter 5

Merchandising Operations

Review Questions

1. What is a merchandiser, and what is the name of the merchandise that it sells?

2. What are the two types of merchandisers? How do they differ?

Merchandisers are often identified as either wholesalers or retailers. A wholesaler is a merchandiser

3. Describe the operating cycle of a merchandiser.

The operating cycle of a merchandiser is as follows: It begins when the company purchases

4. What is Cost of Goods Sold (COGS), and where is it reported?

5. How is gross profit calculated, and what does it represent?

6. What are the two types of inventory accounting systems? Briefly describe each.

The two types of inventory accounting systems are the periodic inventory system and the perpetual

7. What is an invoice?

8. What account is debited when recording a purchase of inventory when using the perpetual inventory

system?

9. What would the credit terms of “2/10, n/EOM” mean?

The credit terms “2/10, n/EOM” means that the purchaser can deduct 2% from the total bill

10. What is a purchase return? How does a purchase allowance differ from a purchase return?

A purchase return is when businesses allow purchasers to return merchandise that is defective,

11. Describe FOB shipping point and FOB destination. When does the buyer take ownership of the

goods, and who typically pays the freight?

FOB shipping point means the buyer takes ownership (title) to the goods after the goods leave the

12. How is the net cost of inventory calculated?

13. What are the two journal entries involved when recording the sale of inventory when using the

perpetual inventory system?

The two journal entries involved when recording the sale of inventory when using the perpetual

14. When granting a sales allowance, is there a return of merchandise inventory from the customer?

Describe the journal entry(ies) that would be recorded.

15. What is freight out, and how is it recorded by the seller?

16. How is net sales revenue calculated?

Net Sales Revenue is calculated as Sales Revenue less Sales Returns and Allowances and Sales

Discounts.

17. What is inventory shrinkage? Describe the adjusting entry that would be recorded to account for

inventory shrinkage.

Inventory shrinkage is the loss of inventory that occurs because of theft, damage, and errors. The

18. What are the four steps involved in the closing process for a merchandising company?

The four-step closing process for a merchandising company are:

19. Describe the single-step income statement.

The single-step income statement is the income statement format that groups all revenues together

20. Describe the multi-step income statement.

21. What financial statement is merchandise inventory reported on, and in what section?

Merchandise inventory is shown as a current asset on the Balance Sheet.

22. What does the gross profit percentage measure, and how is it calculated?

23A. What account is debited when recording a purchase of inventory when using a periodic inventory

system?

24A. When recording purchase returns and purchase allowances under the periodic inventory system,

what account is used?

25A. What account is debited when recording the payment of freight in when using the periodic

inventory system?

26A. Describe the journal entry(ies) when recording a sale of inventory using the periodic inventory

system.

When recording sales of merchandise inventory using the periodic system you will debit Cash or

27A. Is an adjusting entry needed for inventory shrinkage when using the periodic inventory system?

Explain.

An adjusting entry is not needed for inventory shrinkage when using the periodic system. The

28A. Highlight the differences in the closing process when using the periodic inventory system rather

than the perpetual inventory system.

The two main differences in the closing entries are in the first two steps. With step 1 in the

accounts.

29A. Describe the calculation of cost of goods sold when using the periodic inventory system.

The Cost of Goods Sold account is calculated by adding Beginning Merchandise Inventory plus

Short Exercises

For all short exercises, assume the perpetual inventory system is used unless stated otherwise. Round

all numbers to the nearest whole dollar unless stated otherwise.

S5-1 Comparing periodic and perpetual inventory systems

Learning Objective 1

For each statement below, identify whether the statement applies to the periodic inventory system or

perpetual inventory system.

a. Normally used for relatively inexpensive goods.

b. Keeps a running computerized record of merchandise inventory.

c. Achieves better control over merchandise inventory.

d. Requires a physical count of inventory to determine the quantities on hand.

e. Uses bar codes to keep up-to-the-minute records of inventory.

SOLUTION

a.

Periodic

Perpetual

c.

Perpetual

Periodic

e.

Perpetual

S5-2 Journalizing purchase transactions

Learning Objective 2

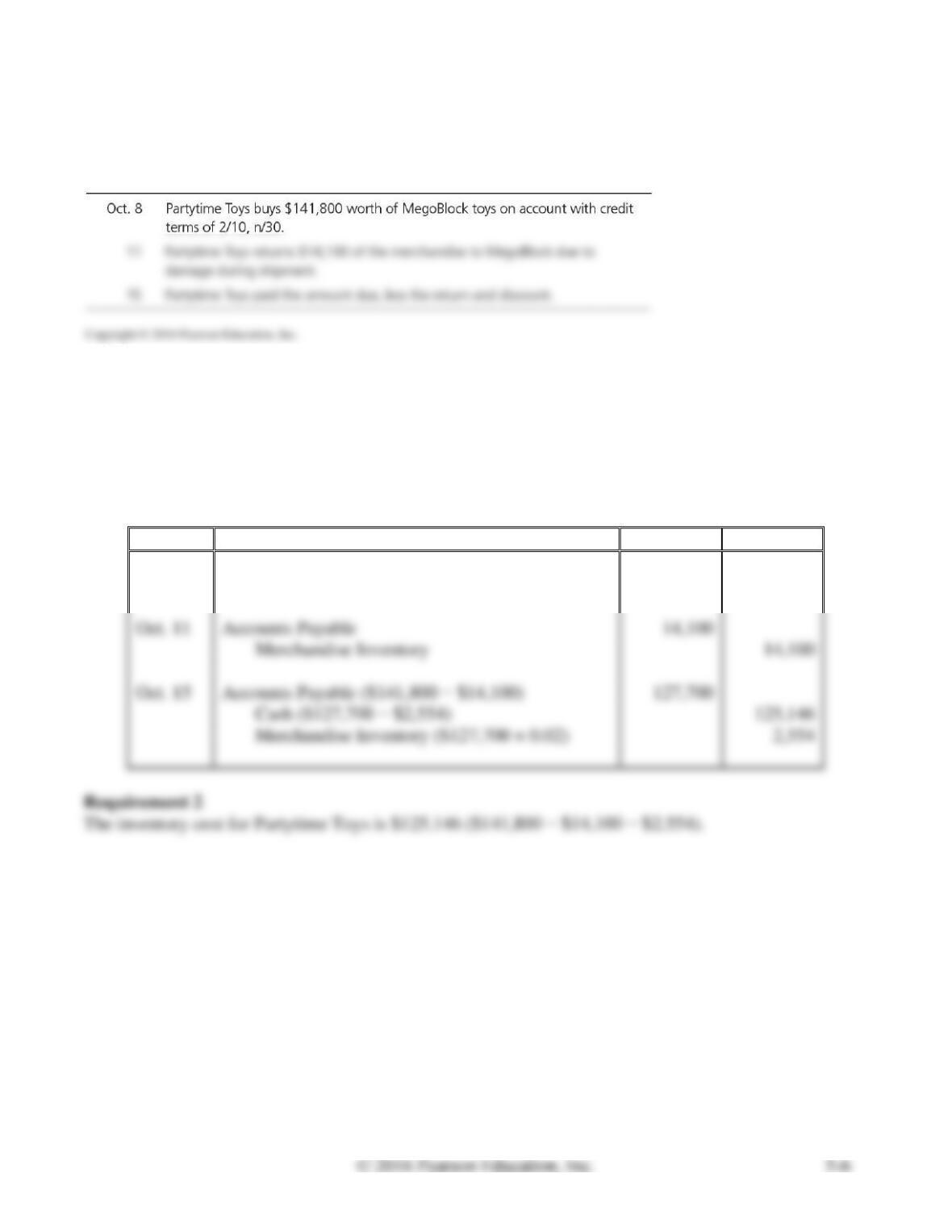

Consider the following transactions for Partytime Toys:

Requirements

1. Journalize the purchase transactions. Explanations are not required.

2. In the final analysis, how much did the inventory cost Partytime Toys?

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Oct. 8

Merchandise Inventory

141,800

Accounts Payable

141,800

Oct. 11

Accounts Payable

14,100

Merchandise Inventory

14,100

Oct. 15

Accounts Payable ($141,800 − $14,100)

127,700

Cash ($127,700 − $2,554)

125,146

Merchandise Inventory ($127,700 × 0.02)

S5-3 Journalizing purchase transactions

Learning Objective 2

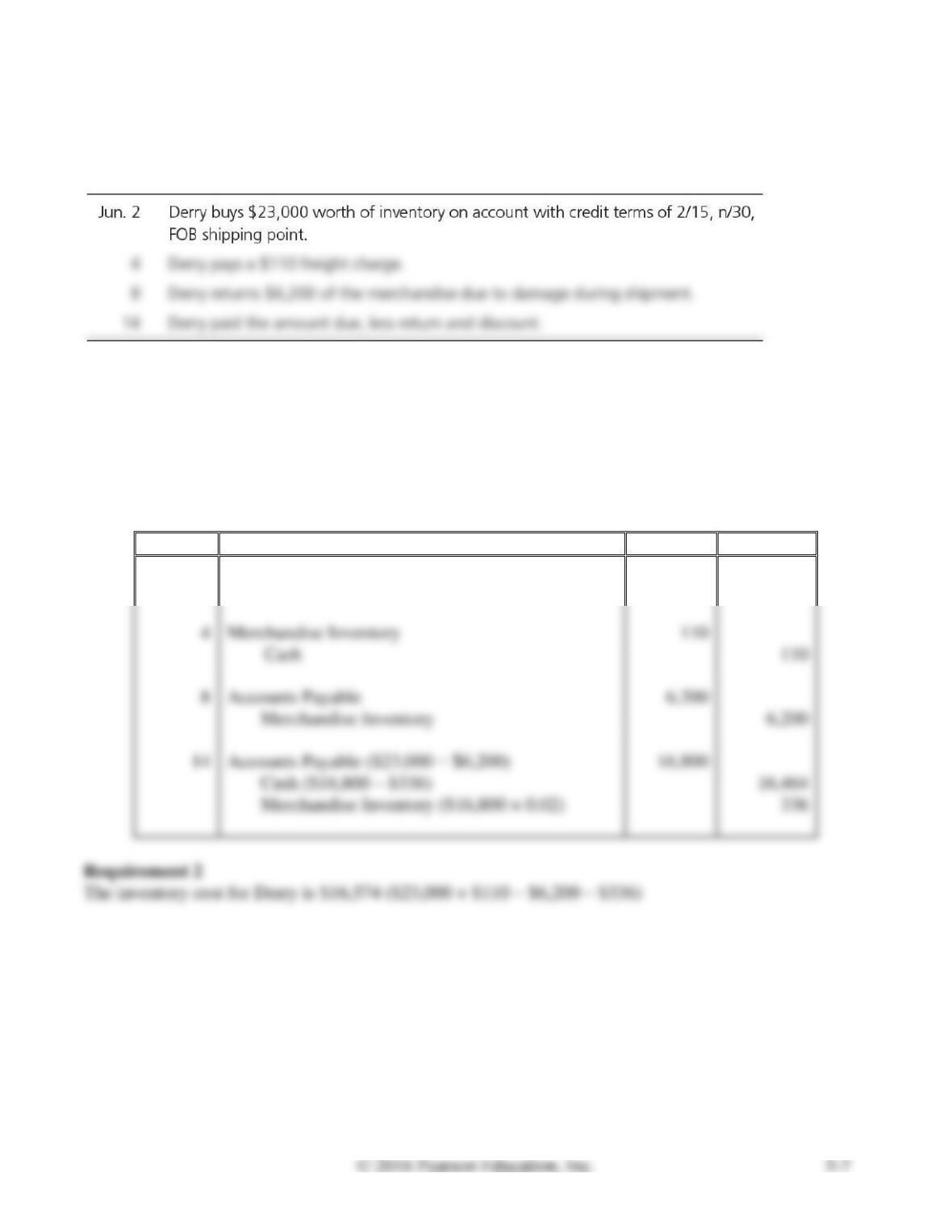

Consider the following transactions for Derry Drug Store:

Requirements

1. Journalize the purchase transactions. Explanations are not required.

2. In the final analysis, how much did the inventory cost Derry Drug Store?

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Jun. 2

Merchandise Inventory

23,000

Accounts Payable

23,000

Merchandise Inventory

110

Cash

Accounts Payable

6,200

Merchandise Inventory

Accounts Payable ($23,000 − $6,200)

16,800

Cash ($16,800 – $336)

16,464

Merchandise Inventory ($16,800 × 0.02)

S5-4 Journalizing sales transactions

Learning Objective 3

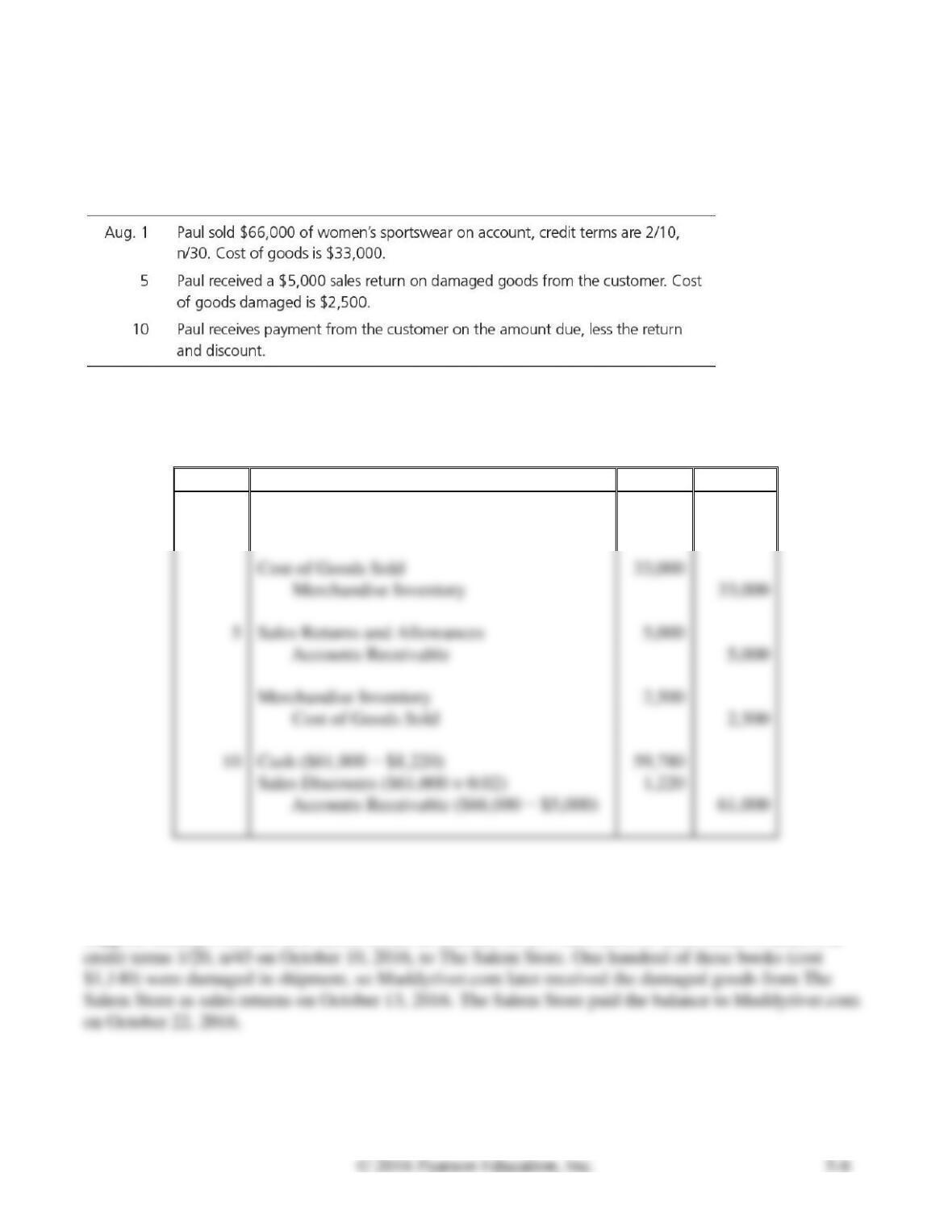

Journalize the following sales transactions for Paul Sportswear. Explanations are not

required.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

Aug. 1

Accounts Receivable

66,000

Sales Revenue

66,000

Cost of Goods Sold

33,000

33,000

Sales Returns and Allowances

Accounts Receivable

Merchandise Inventory

Cash ($61,000 − $1,220)

59,780

Sales Discounts ($61,000 × 0.02)

Accounts Receivable ($66,000 − $5,000)

61,000

S5-5 Journalizing purchase and sales transactions

Learning Objectives 2, 3

Suppose Muddyriver.com sells 2,000 books on account for $19 each (cost of these books is $22,800),

Requirements

1. Journalize The Salem Store’s October 2016 transactions.

2. Journalize Muddyriver.com’s October 2016 transactions.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Oct. 10

Merchandise Inventory (2,000 × $19)

38,000

Accounts Payable

38,000

Accounts Payable (100 × $19)

Merchandise Inventory

Accounts Payable ($38,000 − $1,900)

36,100

Cash ($36,100 – $361)

35,739

Merchandise Inventory ($36,100 × 0.01)

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Oct. 10

Accounts Receivable (2,000 × $19)

38,000

Sales Revenue

38,000

Cost of Goods Sold

22,800

22,800

Sales Returns and Allowances (100 × $19)

Accounts Receivable

Merchandise Inventory

Cash ($36,100 − $361)

35,739

Sales Discounts ($36,000 × 0.01)

Accounts Receivable ($38,000 − $1,900)

36,100

S5-6 Adjusting for inventory shrinkage

Learning Objective 4

Carla’s Furniture’s unadjusted Merchandise Inventory account at year-end is $62,000. The physical

count of inventory came up with a total of $60,800. Journalize the adjusting entry needed to account for

inventory shrinkage.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

Dec. 31

Cost of Goods Sold ($62,000 − $60,800)

S5-7 Journalizing closing entries

Learning Objective 4

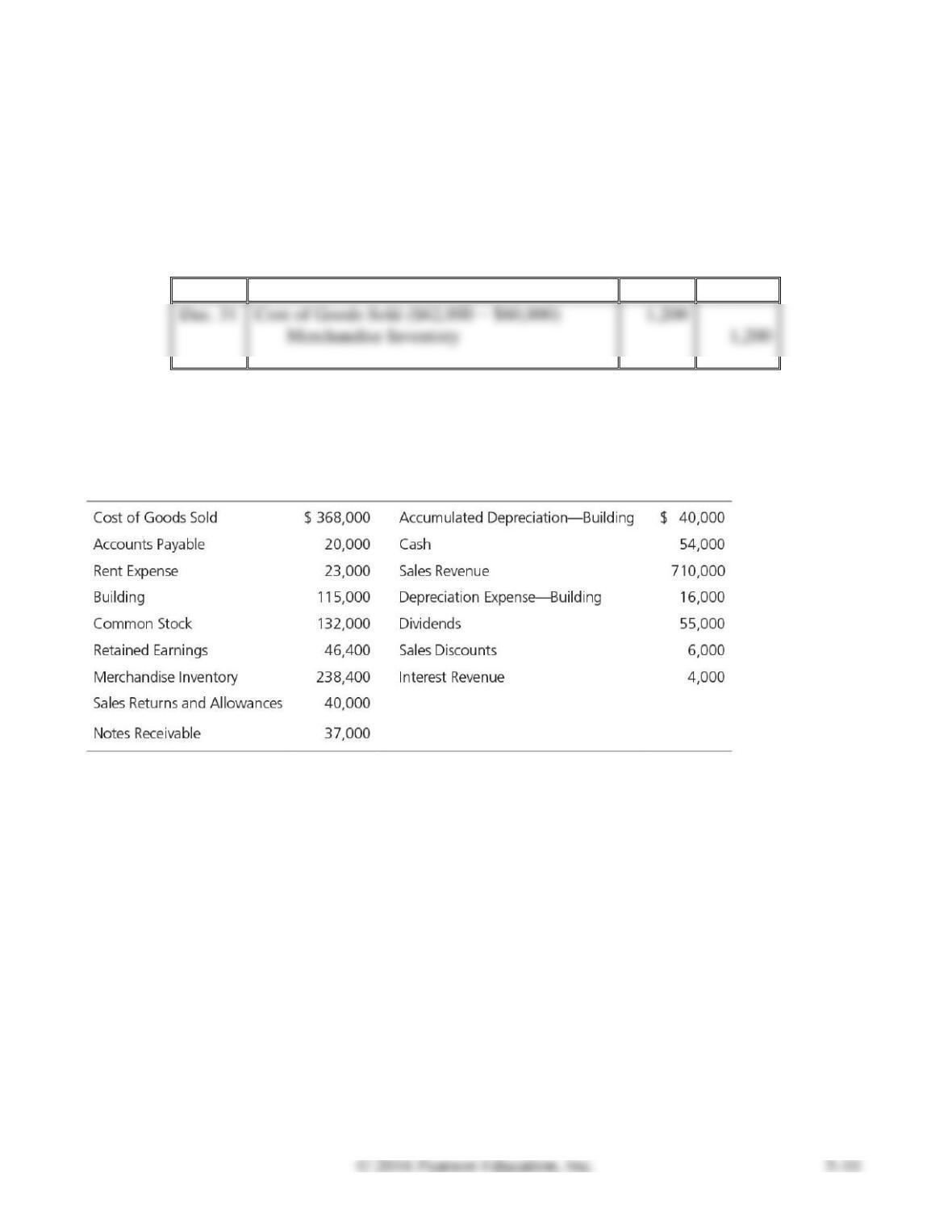

Rockwall RV Center’s accounting records include the following accounts at December 31, 2016.

Requirements

1. Journalize the required closing entries for Rockwall.

2. Determine the ending balance in the Retained Earnings account.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Dec. 31

Sales Revenue

710,000

Interest Revenue

4,000

Income Summary

714,000

Income Summary

453,000

368,000

Income Summary

261,000

261,000

Retained Earnings

Requirement 2

Ending Balance in Retained Earnings is $252,400 ($46,400 + $261,000 – $55,000)

Use the following information to answer Short Exercises S5-8 and S5-9.

Carissa Communications reported the following figures from its adjusted trial balance for its first year of

business, which ended on July 31, 2016:

S5–8 Preparing a merchandiser’s income statement

Learning Objective 5

Prepare Carissa Communications’s multi-step income statement for the year ended

July 31, 2016.

SOLUTION

CARISSA COMMUNICATIONS

Income Statement

Year Ended July 31, 2016

Sales Revenue

$ 42,000

Less: Sales Returns and Allowances

7,400

4,300

Net Sales Revenue

$ 30,300

Cost of Goods Sold

Gross Profit

Operating Expenses:

1,300

3,100

4,400

Operating Income

7,100

Other Revenues and (Expenses):

Net Income

$ 7,080

S5–9 Preparing a merchandiser’s statement of retained earnings and balance sheet

Learning Objective 5

Requirements

1. Prepare Carissa Communications’s statement of retained earnings for the year ended July 31, 2016.

Assume that there were no dividends declared during the year and that the business began on August

1, 2015.

2. Prepare Carissa Communications’s classified balance sheet at July 31, 2016. Use

the report format.

SOLUTION

Requirement 1

CARISSA COMMUNICATIONS

Statement of Retained Earnings

Year Ended July 31, 2016

Retained Earnings, August 1, 2015

Net income for the year

$ 7,080

Dividends

Retained Earnings, July 31, 2016

$ 7,080

Requirement 2

CARISSA COMMUNICATIONS

Balance Sheet

July 31, 2016

Assets

Current Assets:

Cash

$ 4,100

Accounts Receivable

3,400

Merchandise Inventory

1,200

Total Current Assets

$ 8,700

Plant Assets:

Equipment, Net

Total Plant Assets

Total Assets

$ 17,200

Current Liabilities:

Accounts Payable

$ 4,900

Accrued Liabilities

2,000

Total Current Liabilities

$ 6,900

Long-term Liabilities:

Total Liabilities

Common Stock

Retained Earnings

Total Liabilities and Stockholders’ Equity

$ 17,200

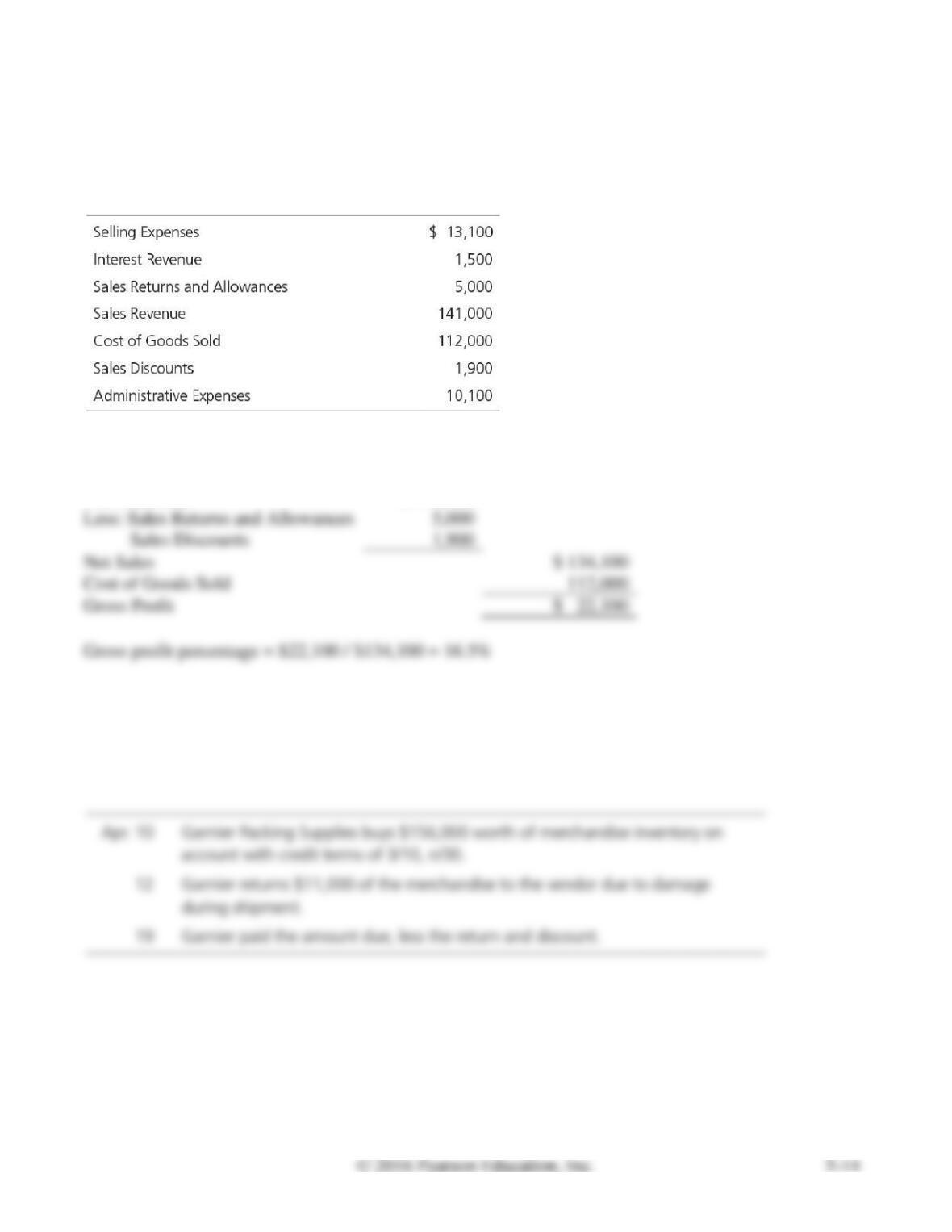

S5-10 Computing the gross profit percentage

Learning Objective 6

Morris Landscape Supply’s selected accounts as of December 31, 2016, follow. Compute the gross

profit percentage for 2016.

SOLUTION

Sales Revenue

$ 141,000

Less: Sales Returns and Allowances

Sales Discounts

Net Sales

Cost of Goods Sold

Gross Profit

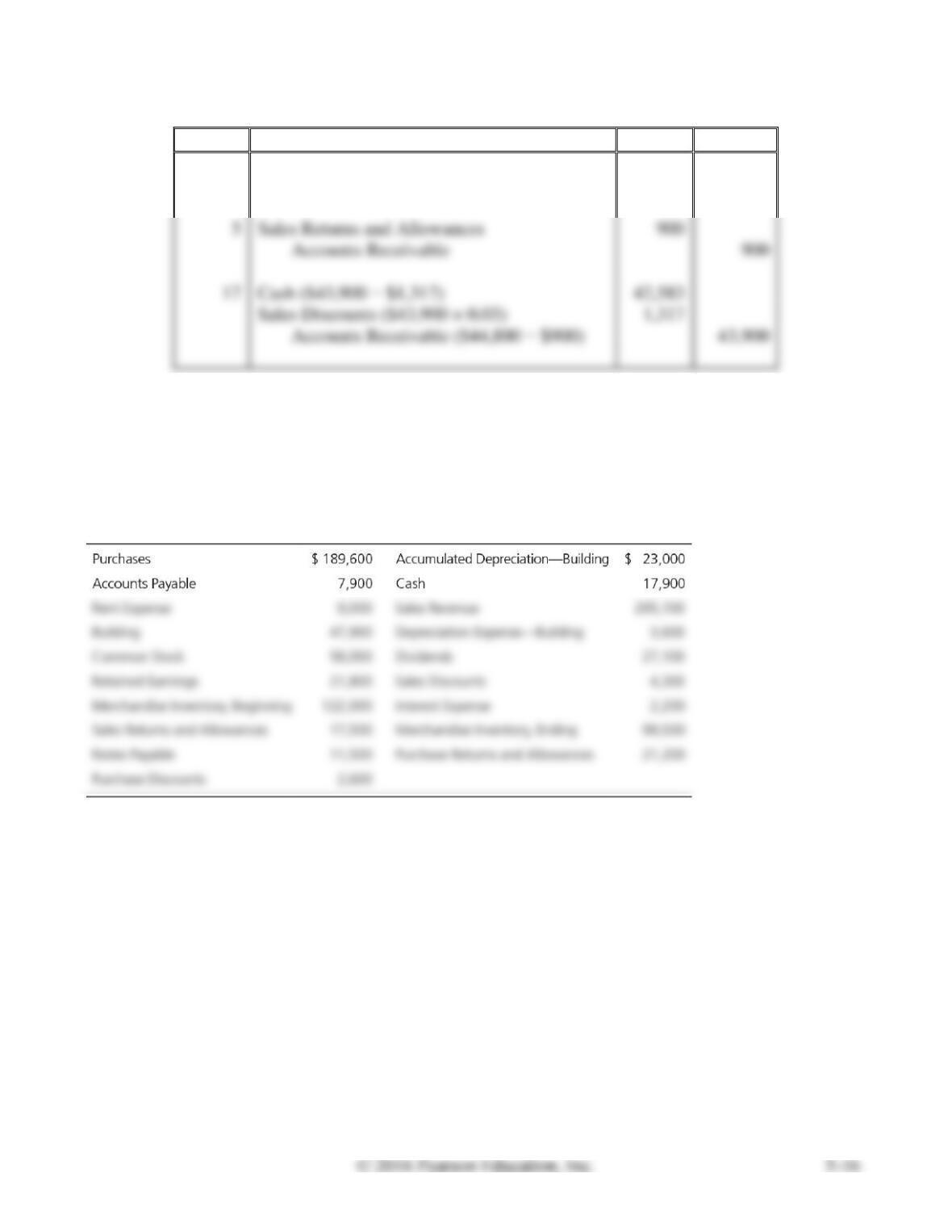

S5A-11 Journalizing purchase transactions—periodic inventory system

Learning Objective 7

Appendix 5A

Consider the following transactions for Garnier Packing Supplies:

Requirements

1. Journalize the purchase transactions assuming Garnier Packing Supplies uses the periodic inventory

system. Explanations are not required.

2. What is the amount of net purchases?

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Apr. 10

Purchases

156,000

Accounts Payable

156,000

Accounts Payable

Purchase Returns and Allowances

Accounts Payable ($156,000 – $11,000)

145,000

Cash ($145,000 − $4,350)

140,650

Purchase Discounts ($145,000 × 0.03)

Requirement 2

The amount of net purchases = $140,650 ($156,000 − $11,000 − $4,350)

S5A-12 Journalizing sales transactions—periodic inventory system

Learning Objective 7

Appendix 5A

SOLUTION

Date

Accounts and Explanation

Debit

Credit

Dec. 3

Accounts Receivable

44,800

Sales Revenue

44,800

Sales Returns and Allowances

Accounts Receivable

Cash ($43,900 − $1,317)

42,583

Sales Discounts ($43,900 × 0.03)

Accounts Receivable ($44,800 − $900)

43,900

S5A-13 Journalizing closing entries—periodic inventory system

Learning Objective 7

Appendix 5A

D & L Printing Supplies’s accounting records include the following accounts at

December 31, 2016.

Requirements

1. Journalize the required closing entries for D & L Printing Supplies assuming that D & L uses the

periodic inventory system.

2. Determine the ending balance in the Retained Earnings account.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Dec. 31

Sales Revenue

295,100

Purchase Returns and Allowances

21,200

Purchase Discounts

2,600

Merchandise Inventory (ending)

99,500

Income Summary

418,400

Income Summary

348,200

189,600

122,000

Income Summary

70,200

Retained Earnings

27,100

Requirement 2

S5A-14 Computing cost of goods sold in a periodic inventory system

Learning Objective 7

Appendix 5A

X Wholesale Company began the year with merchandise inventory of $11,000. During the year, X

purchased $93,000 of goods and returned $6,700 due to damage. X also paid freight charges of $1,200

on inventory purchases. At year-end, X’s ending merchandise inventory balance stood at $17,300.

Assume that X uses the periodic inventory system. Compute X’s cost of goods sold for the year.

SOLUTION

Beginning Merchandise Inventory

$ 11,000

Net Cost of Purchases

Cost of Goods Available for Sale

Less: Ending Inventory

Cost of Goods Sold

Exercises

For all exercises, assume the perpetual inventory system is used unless stated otherwise. Round all

numbers to the nearest whole dollar unless stated otherwise.

E5-15 Using accounting vocabulary

Learning Objectives 1, 2, 3

Match the accounting terms with the corresponding definitions.

SOLUTION

1.

h

2.

d

3.

j

4.

a

5.

i

6.

b

7.

g

8.

e

9.

f

c

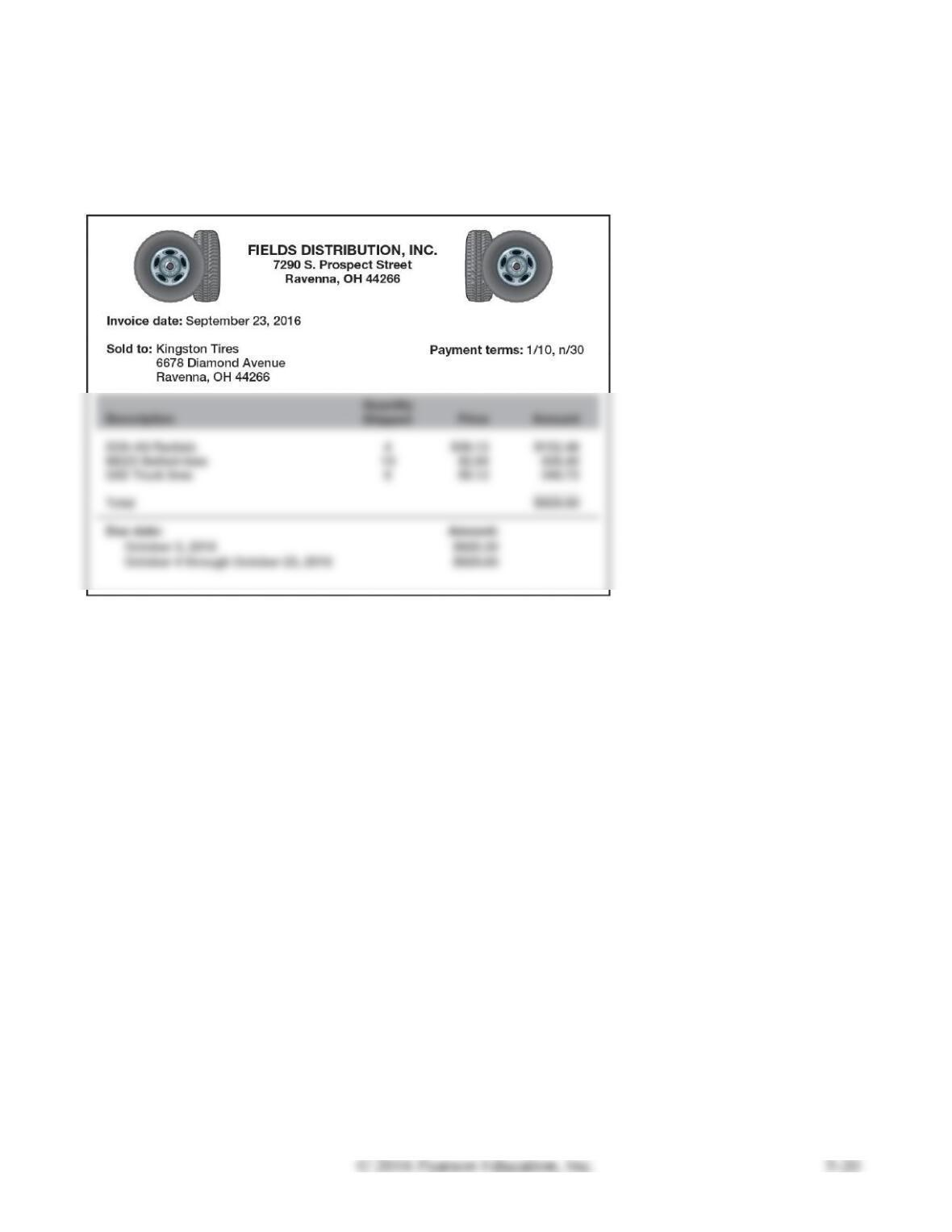

E5-16 Journalizing purchase transactions from an invoice

Learning Objective 2

3. Oct. 1 Cash $769.35

Kingston Tires received the following invoice from a supplier (Fields Distribution, Inc.):

Requirements

1. Journalize the transaction required by Kingston Tires on September 23, 2016. Do not round numbers

to the nearest whole dollar. Assume tires are purchased on account.

2. Journalize the return on Kingston’s books on September 28, 2016, of the D39–X4 Radials, which

were ordered by mistake. Do not round numbers to the nearest whole dollar.

3. Journalize the payment on October 1, 2016, to Fields Distribution, Inc. Do not round numbers to the

nearest whole dollar.