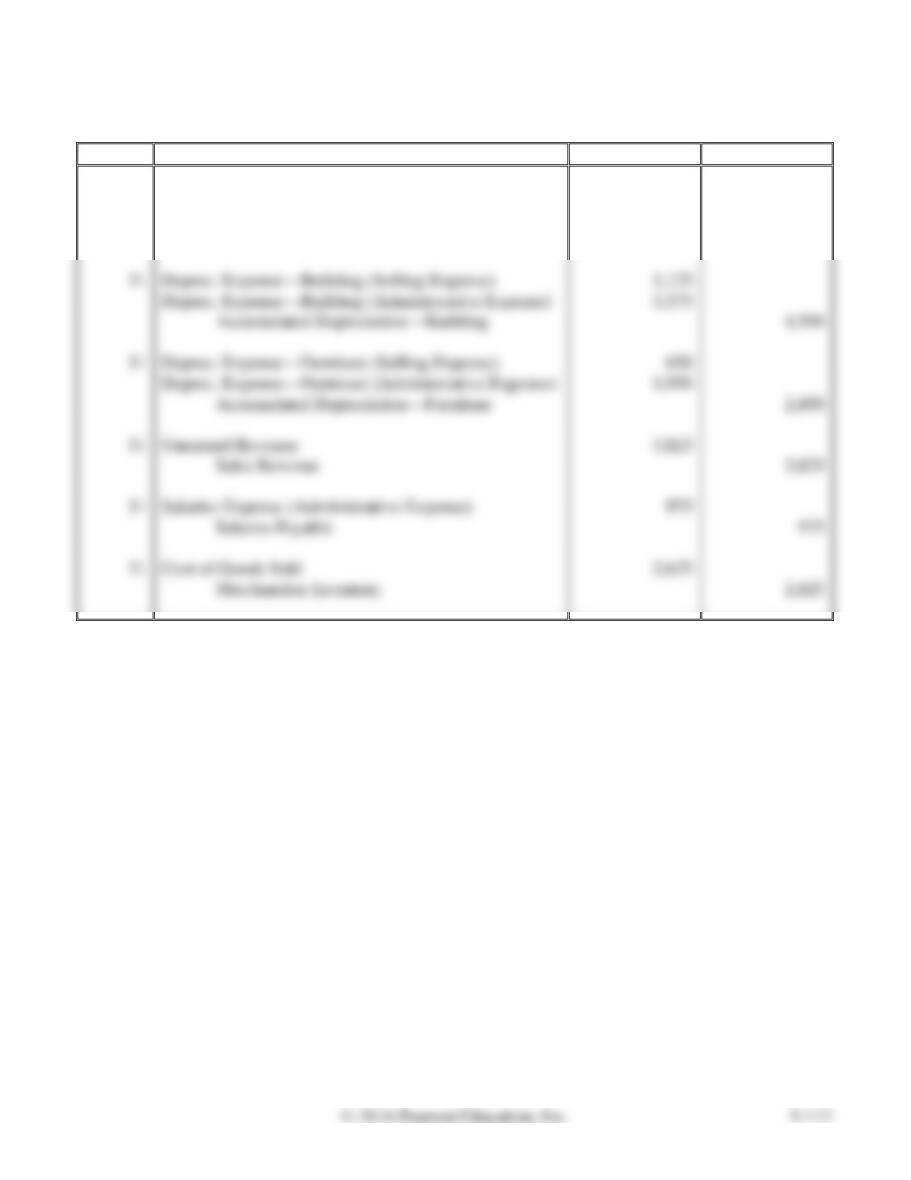

Comprehensive Problem, cont.

Requirement 2

Date

Accounts and Explanation

Debit

Credit

Adjusting Entries

Jan. 31

Office Supplies Expense (Selling Expense)

890

Office Supplies Expense (Administrative Expense)

890

Office Supplies

1,780

Deprec. Expense—Building (Selling Expense)

1,125

Deprec. Expense—Building (Administrative Expense)

3,375

Accumulated Depreciation—Building

4,500

Deprec. Expense—Furniture (Selling Expense)

650

Deprec. Expense—Furniture (Administrative Expense)

1,950

Accumulated Depreciation—Furniture

2,600

Unearned Revenue

3,825

Sales Revenue

3,825

Salaries Expense (Administrative Expense)

975

Salaries Payable

975

Cost of Goods Sold

2,625

Merchandise Inventory

2,625

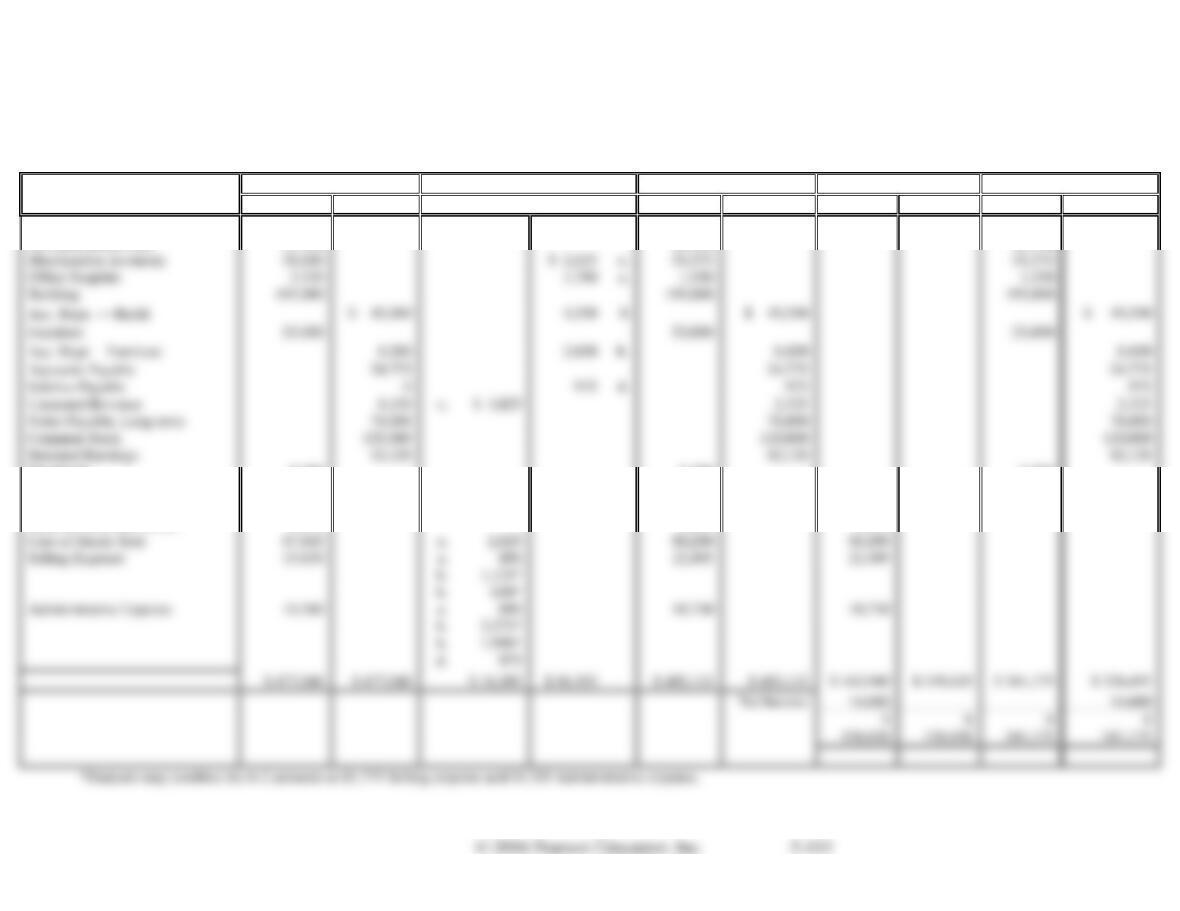

Comprehensive Problem, cont.

Requirement 3

ST. JOHN TECHNOLOGY

Worksheet

January 31, 2016

Account Names

Unadjusted Trial Balance

Adjustments

Adjusted Trial Balance

Income Statement

Balance Sheet

Debit

Credit

Debit

Credit

Debit

Credit

Debit

Credit

Debit

Credit

Cash

$ 12,660

$ 12,660

$ 12,660

Accounts Receivable

15,390

15,390

15,390

Merchandise Inventory

55,375

Office Supplies

1,550

1,550

Building

Furniture

Accounts Payable

24,775

24,775

Salaries Payable

0

Unearned Revenue

$ 3,825

Notes Payable, Long-term

78,000

78,000

Common Stock

120,000

120,000

Retained Earnings

42,120

42,120

Dividends

8,200

8,200

8,200

Sales Revenue

154,795

3,825

c.

158,620

$158,620

Sales Discounts

7,350

7,350

7,350

Sales Returns and Allow.

5,075

5,075

5,075

Cost of Goods Sold

2,625

90,290

Selling Expense

890

22,495

1,125*

Administrative Expense

890

18,730

3,375*

975

$ 477,040

$ 16,305

$ 158,620

$ 326,495

Comprehensive Problem, cont.

Requirement 4

St. John Technology

Income Statement

Month Ended January 31, 2016

Revenue:

Sales Revenue

$ 158,620

Less: Sales Returns and Allowances

$ 5,075

Net Sales Revenue

Cost of Goods Sold

Gross Profit

Operating Expenses:

Net Income

St. John Technology

Statement of Retained Earnings

Month Ended January 31, 2016

Retained Earnings, January 1, 2016

$ 42,120

Net income for the month

14,680

Retained Earnings, January 31, 2016

$ 48,600

Comprehensive Problem, cont.

Requirement 4, cont.

St. John Technology

Balance Sheet

January 31, 2016

Assets

Current Assets:

Cash

$ 12,660

Accounts Receivable

15,390

Merchandise Inventory

55,375

Office Supplies

1,550

Total Current Assets

$ 84,975

Plant Assets:

Building

$195,000

Accumulated Depreciation—Building

145,500

Furniture

Accumulated Depreciation—Furniture

Total Plant Assets

Total Assets

$ 274,675

Liabilities

Current Liabilities:

Accounts Payable

$ 24,775

Salaries Payable

975

Unearned Revenue

2,325

Total Current Liabilities

$ 28,075

Long-term Liabilities:

Note Payable, Long–term

Total Liabilities

Common Stock

Retained Earnings

Total Liabilities and Stockholders’ Equity

$ 274,675

Comprehensive Problem, cont.

Requirement 5

Date

Accounts and Explanation

Debit

Credit

Closing Entries

Jan. 31

Sales Revenue

158,620

Income Summary

158,620

Income Summary

143,940

Cost of Goods Sold

Selling Expense

Administrative Expense

Sales Discounts

Income Summary

Retained Earnings

Retained Earnings

Dividends

Critical Thinking

Decision Case 5-1

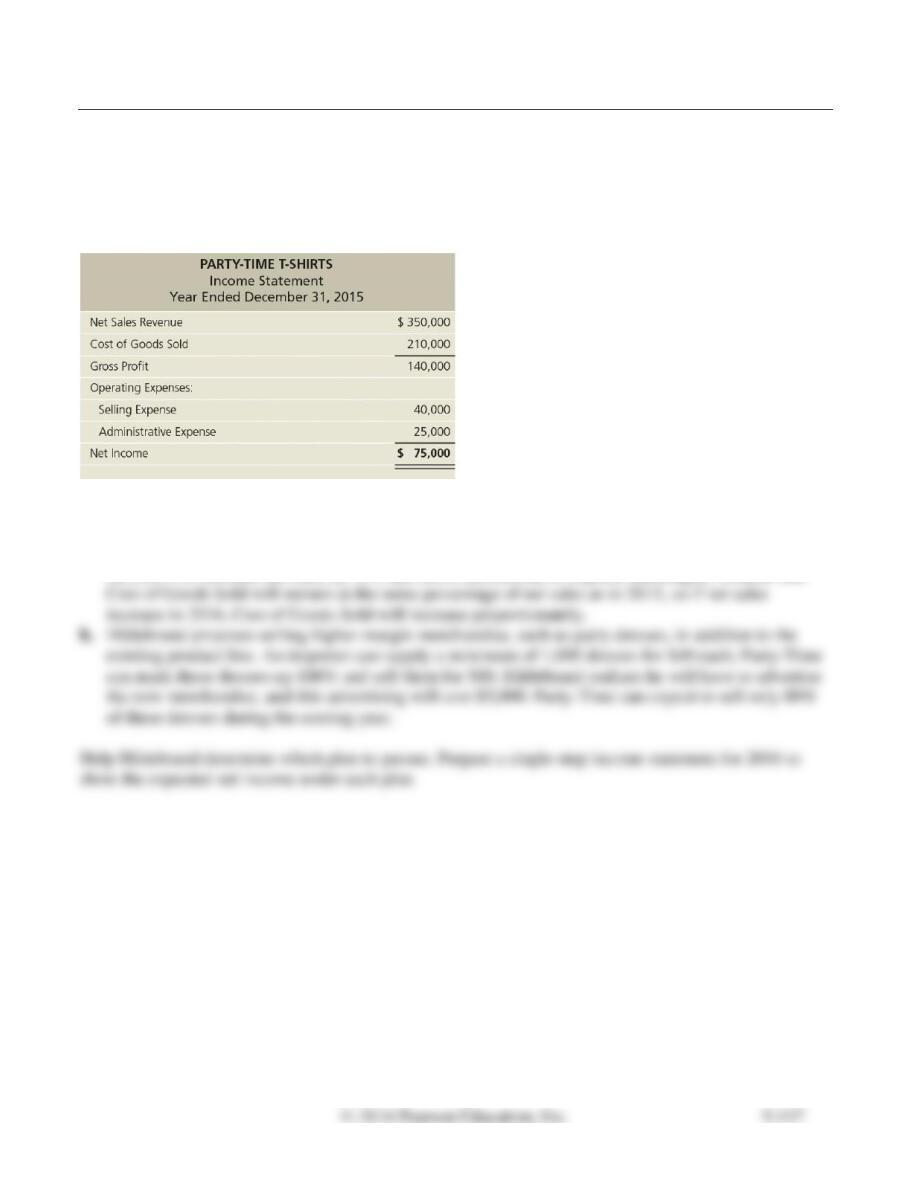

Party-Time T-Shirts sells T-shirts for parties at the local college. The company completed the first year

of operations, and the shareholders are generally pleased with operating results as shown by the

following income statement:

Bill Hildebrand, the controller, is considering how to expand the business. He proposes two ways to

increase profits to $100,000 during 2016.

a. Hildebrand believes he should advertise more heavily. He believes additional advertising costing

$20,000 will increase net sales by 30% and leave administrative expense unchanged. Assume that

SOLUTION

Plan a:

PARTY-TIME T-SHIRTS

Expected Income Statement

Year Ended December 31, 2016

Net Sales Revenue

($350,000 × 1.3)

$ 455,000

Expenses:

($210,000 × 1.3)

($40,000 + $20,000)

Net Income

$ 97,000

Plan b:

PARTY-TIME T-SHIRTS

Expected Income Statement

Year Ended December 31, 2016

Net Sales Revenue

($350,000 + (800 dresses × $80))

$ 414,000

Expenses:

($210,000 + (800 dresses × $40))

($40,000 + 5,000)

Net Income

Ethical Issue 5-1

Dobbs Wholesale Antiques makes all sales under terms of FOB shipping point. The company usually

ships inventory to customers approximately one week after receiving the order. For orders received late

in December, Kathy Dobbs, the owner, decides when to ship the goods. If profits are already at an

acceptable level, Dobbs delays shipment until January. If profits for the current year are lagging behind

expectations, Dobbs ships the goods during December.

Requirements

1. Under Dobbs’s FOB policy, when should the company record a sale?

2. Do you approve or disapprove of Dobbs’s manner of deciding when to ship goods to customers and

record the sales revenue? If you approve, give your reason. If you disapprove, identify a better way

to decide when to ship goods. (There is no accounting rule against Dobbs’s practice.)

SOLUTION

Requirement 1

Requirement 2

This is a difficult ethical issue because there is no single correct answer. There is no rule of accounting,

law, or ethics to govern when a business should ship the goods. Therefore, students can legitimately

Fraud Case 5-1

Rae Philippe was a warehouse manager for Atkins Oilfield Supply, a business that operated across eight

Western states. She was an old pro and had known most of the other warehouse managers for many

years. Around December each year, auditors would come to do a physical count of the inventory at each

warehouse. Recently, Rae’s brother started his own drilling company and persuaded Rae to “loan” him

80 joints of 5-inch drill pipe to use for his first well. He promised to have it back to Rae by December,

but the well encountered problems and the pipe was still in the ground. Rae knew the auditors were on

the way, so she called her friend Andy, who ran an- other Atkins warehouse. “Send me over 80 joints of

5-inch pipe tomorrow, and I’ll get them back to you ASAP,” said Rae. When the auditors came, all the

pipe on the books was accounted for, and they filed a “no–exception” report.

Requirements

1. Is there anything the company or the auditors could do in the future to detect this kind of fraudulent

practice?

2. How would this kind of action affect the financial performance of the company?

SOLUTION

Requirement 1

Auditors should arrive unannounced, so that the local manager cannot make an arrangement like this in

Financial Case 5-1

This case uses both the income statement (consolidated statement of earnings) and the balance sheet of

Starbucks Corporation. Visit http://www.pearsonhighered.com/ Horngren to view a link to the

Starbucks Corporation Fiscal 2013 Annual Report.

Requirements

1. What was the value of the company’s inventory at September 29, 2013, and September 30, 2012?

2. Review Note 5 (specifically Inventories) in the Notes to Consolidated Financial Statements. What do

Starbucks’ inventories consist of?

3. What was the amount of Starbucks’s cost of goods sold (cost of sales) for the year ending September

29, 2013, and the year ending September 30, 2012?

4. What income statement format does Starbucks use? Explain.

5. Compute Starbucks’s gross profit percentage for the year ending September 29, 2013, and the year

ending September 30, 2012. Did the gross profit percentage improve, worsen, or hold steady?

Assuming the industry average for gross profit percentage is 58.58%, how does Starbucks compare

in the industry?

SOLUTION

Requirement 1

Starbucks Inventory Value

September 29, 2013

$ 1,111.2 (in millions)

September 30, 2012

$ 1,241.5 (in millions)

Starbucks Cost of Goods Sold

September 29, 2013

$ 6,382.3 (in millions)

September 30, 2012

$ 5,813.3 (in millions)

Requirement 5

September 29, 2013 (in millions)

September 30, 2012 (in millions)

Net Revenues

$ 14,892.2

$ 13,299.5

Cost of Sales

6,382.3

5,813.3

Gross Profit

8,509.9

7,486.2

Gross Profit %

57.14%

56.29%