Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-21

EXERCISE 5-27 (Concluded)

3. Cost of goods sold:

LIFO ............................................................................................. $12,200

FIFO ............................................................................................. 11,400

PROBLEMS

LO 1 PROBLEM 5-1 INVENTORY COSTS IN VARIOUS BUSINESSES

Accounting Treatment

Expense of Inventory Other

Business Types of Costs the Period Cost Treatment

Retail shoe store Shoes for sale X

Shoe boxes X

Advertising signs X

Grocery store Canned goods on the shelves X

Produce X

Cleaning supplies X*

Cash registers X**

5-22 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 4 PROBLEM 5-2 MAKING BUSINESS DECISIONS: ANALYZING WAL-MART’S GROSS

PROFIT RATIO

Part A. Ratio Analysis Model

1. Formulate the Question:

How many cents on the dollar does Wal-Mart have available to cover expenses

other than cost of goods sold and to earn a profit?

3. Calculate the Ratio:

Gross Profit Ratio = Gross Profit

Net Sales

4. Compare the Ratio with Other Ratios:

Gross Profit Ratio

Wal-Mart Target

Year Ended Year Ended Year Ended Year Ended

January 31, 2014 January 31, 2013 February 1, 2014 February 2, 2013

24.3% 24.3% 29.5% 29.7%

Calculations:

Wal-Mart:

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-23

PROBLEM 5-2 (Continued)

5. Interpret the Ratios:

For every dollar of sales, Wal-Mart has 24.3 cents available after deducting the cost

Part B. Business Decision Model

1. Formulate the Question:

After considering all relevant information, should I invest in the common stock of

Wal-mart?

2. Gather Information from the Financial Statements and Other Sources:

The information will come from a variety of sources, not limited to but including:

a. The balance sheet provides information about liquidity.

3. Analyze the Information Gathered:

The information gathered in (2) above must be analyzed. Among the relevant ques-

tions that must be answered are the following:

a. Refer to part (5) of the Ratio Analysis Model for a comparison of the gross profit

ratios for Wal-Mart and its competitor, Target, over the last two years. Which

PROBLEM 5-2 (Concluded)

4. Make the Decision:

5. Monitor Your Decision:

If you decide to buy the stock, you will need to monitor your investment periodically.

During the time you hold the stock, you will want to assess the company’s continuing

profitability as well as other factors you considered before making the investment.

LO 7 PROBLEM 5-3 EVALUATION OF INVENTORY COSTING METHODS

1. Company B will have the newest costs in inventory because it uses first-in, first-out.

2. Company C will have the oldest costs in inventory because it uses last-in, first-out.

Because costs are rising, it will have the highest cost of goods sold and thus the

lowest income before taxes. Company C will pay the least in taxes.

3. This question does not lend itself to an easy answer. LIFO matches the most recent

4. Company C would have the oldest costs in inventory because it uses LIFO. Because

costs are falling, it will have the lowest cost of goods sold and the highest net

income.

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-25

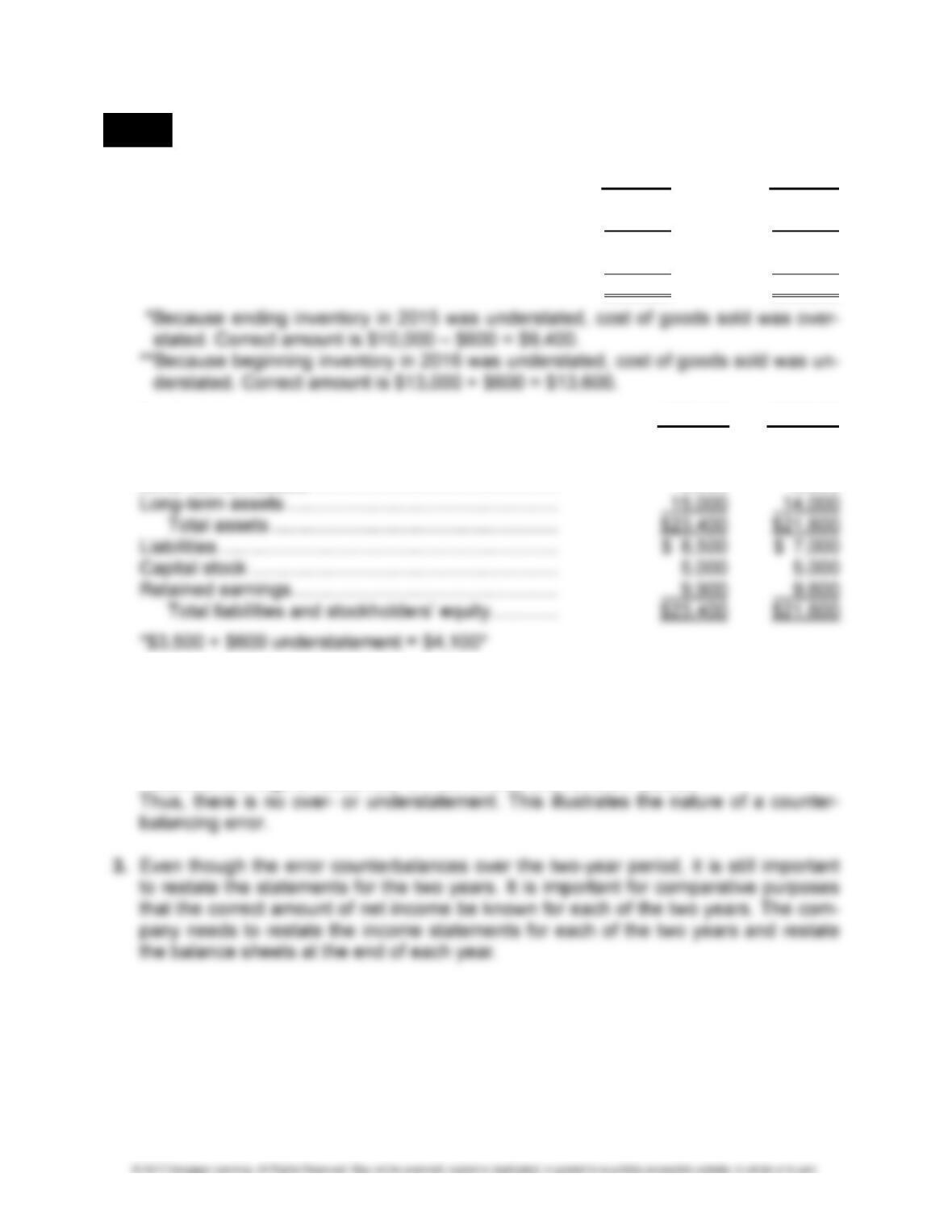

LO 8 PROBLEM 5-4 INVENTORY ERROR

1. Revised income statements: 2016 2015

Revenues .......................................................... $20,000 $15,000

Cost of goods sold ............................................. 13,600** 9,400*

Gross profit ................................................... $ 6,400 $ 5,600

Operating expenses .......................................... 3,000 2,000

Net income ................................................... $ 3,400 $ 3,600

Revised balance sheets: 12/31/16 12/31/15

Cash ....................................................................... $ 1,700 $ 1,500

Inventory ................................................................. 4,200 4,100*

Other current assets ............................................... 2,500 2,000

2. Net income for two years, before revision: $3,000 + $4,000 = $7,000

Net income for two years, after revision: $3,600 + $3,400 = $7,000

Thus, there is no net over- or understatement.

Retained earnings at December 31, 2016, before the revision: $9,900

Retained earnings at December 31, 2016, after the revision: $9,900

5-26 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

LO 10 PROBLEM 5-5 MAKING BUSINESS DECISIONS: ANALYZING APPLE’S INVENTORY

TURNOVER RATIO

Part A. Ratio Analysis Model

1. Formulate the Question:

How many times a year does Apple Inc. turn over its inventory?

2. Gather the Information from the Financial Statements:

3. Calculate the Ratio:

Inventory Turnover Ratio = Cost of Goods Sold

Average Inventory

4. Compare the Ratio with Other Ratios:

Inventory Turnover Ratio

Apple Inc. Hewlett-Packard

Year Ended Year Ended Year Ended Year Ended

September 27, 2014 September 28, 2013 October 31, 2014 October 31, 2013

57.9 times 83.4 times 9.1 times 9.0 times

Calculations:

Apple Inc.:

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-27

PROBLEM 5-5 (Continued)

5. Interpret the Ratios:

Apple Inc. turned over its inventory 57.9 times during the 2014 fiscal year. This

means that, on average, Apple sells its products every 6.2 days (360 days/57.9).

Part B. Business Decision Model

1. Formulate the Question:

After considering all relevant information, should I invest in the common stock of

Apple Inc.?

2. Gather Information from the Financial Statements and Other Sources:

The information will come from a variety of sources, not limited to but including:

a. The balance sheet provides information about liquidity.

3. Analyze the Information Gathered:

The information gathered in (2) above must be analyzed. Among the relevant ques-

tions that must be answered are the following:

a. Refer to part (5) of the Ratio Analysis Model for a comparison of the turnover

ratios for Apple Inc. and its competitor, Hewlett-Packard, over the last two years.

Which company turns over its inventory more often?

5-28 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 5-5 (Concluded)

4. Make the Decision:

5. Monitor Your Decision:

LO 11 PROBLEM 5-6 EFFECTS OF CHANGES IN INVENTORY AND ACCOUNTS PAYABLE

BALANCES ON STATEMENT OF CASH FLOWS

1. Statement of cash flows:

COPELAND ANTIQUES

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED DECEMBER 31, 2016

Net loss ........................................................................................ $(33,200)

Adjustments to reconcile net loss to net cash provided by

2. Memo to the president:

TO: President of Copeland Antiques

FROM: Student’s name

DATE: January 20, 2017

SUBJECT: Cash Flows

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-29

MULTI-CONCEPT PROBLEMS

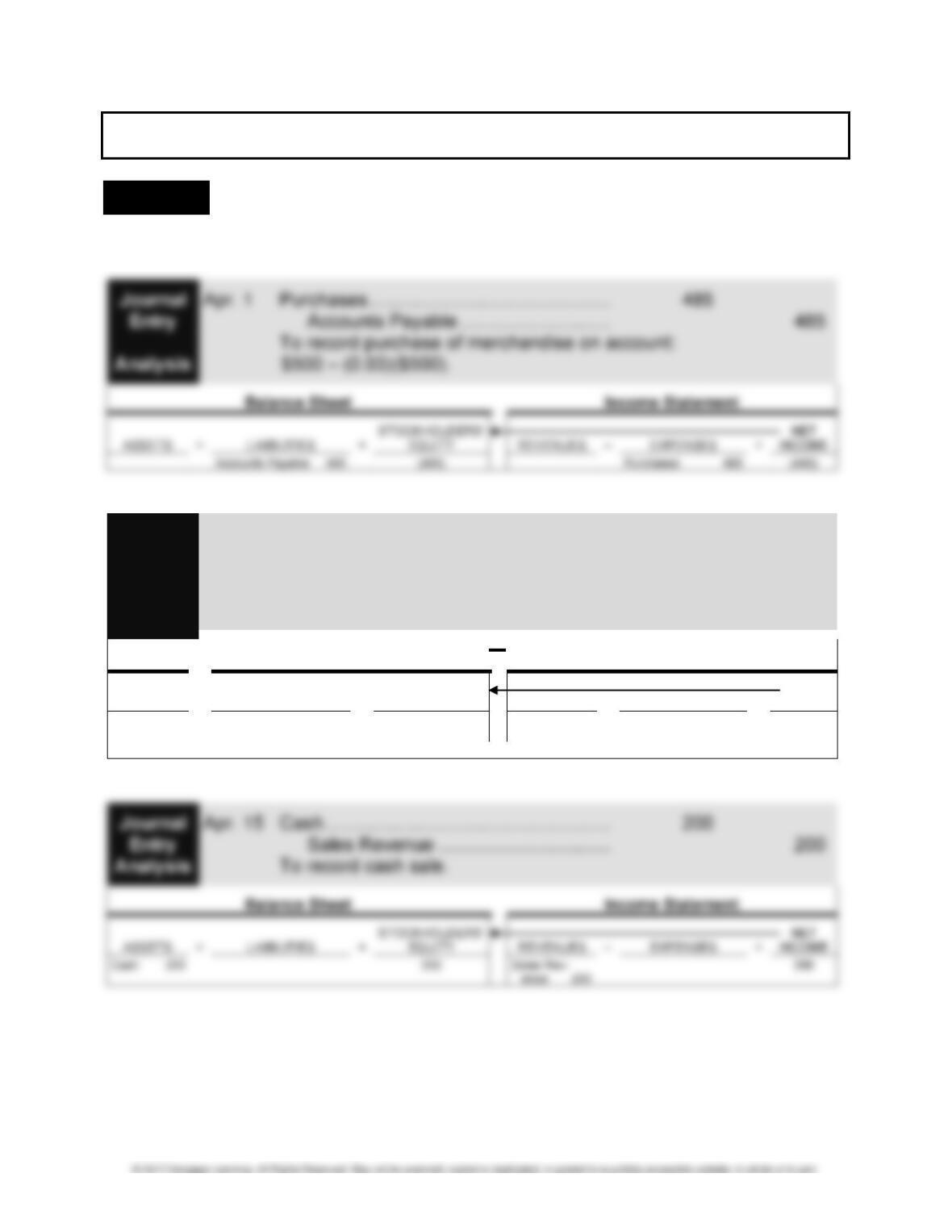

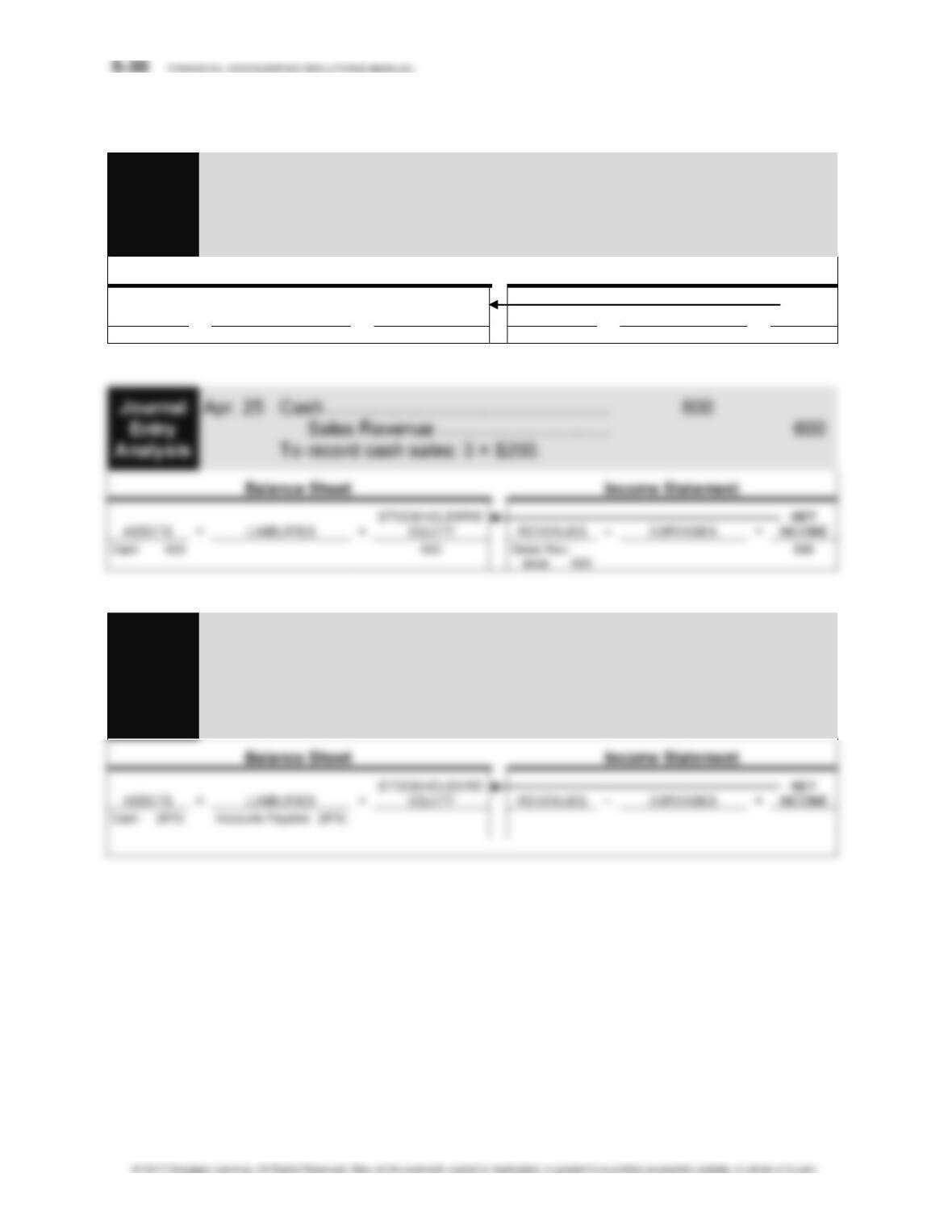

LO 2,3,11 PROBLEM 5-7 PURCHASES AND SALES OF MERCHANDISE, CASH FLOWS

1. Journal entries:

Journal Apr. 10 Accounts Payable .................................. 485

Entry Cash ................................................. 485

Analysis To record payment on account.

Balance Sheet Income Statement

=

ASSETS LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Cash (485)

Accounts Payable (485)

PROBLEM 5-7 (Continued)

Journal Apr. 18 Purchases .............................................. 873

Entry Accounts Payable ............................. 873

Analysis To record purchase of merchandise on account.

$900 – (0.03)($900).

Balance Sheet Income Statement

ASSETS = LIABILITIES +

STOCKHOLDERS’

EQUITY REVENUES – EXPENSES =

NET

INCOME

Accounts Payable 873 (873) Purchases 873 (873)

Journal Apr. 28 Accounts Payable .................................. 873

Entry Cash ................................................. 873

Analysis

To record payment on account.

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-31

PROBLEM 5-7 (Concluded)

2. Net income for April:

Sales revenue ($200 + $600) ............................ $ 800

Cost of goods sold:

Beginning inventory ...................................... $ 0

3. Net cash flow from operating activities for April:

Cash collected from sales ($200 + $600) .......... $ 800

Cash paid for:

4. Net income is $259. Net cash flow from operating activities is a negative $708. The

difference of $967 is attributable to inventory that has not been sold. That is, the

company has paid for $1,358 of inventory (a cash outlay) but has only recognized

cost of goods sold expense of $391. The difference is $967.

LO 2,3,4 PROBLEM 5-8 GAP INC.’S SALES, COST OF GOODS SOLD, AND GROSS

PROFIT

1. Apparently, Gap Inc. does not sell its merchandise on account. If customers want to

5-32 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

Journal Cash ................................................................... 16,435

Entry Sales ............................................................ 16,435

Analysis To record sales.

3. Gap Inc. would deduct sales returns and allowances from sales to arrive at the

amount of net sales reported on its income statement. Since Gap Inc. does not have

any accounts receivable on its balance sheet, it is unlikely that it offers sales

discounts to its customers.

4. Cost of Goods Sold section of 2014 income statement (millions of dollars):

Merchandise inventory, 2/1/14 ..................................................... $ 1,928

Cost of goods purchased1 ............................................................ 10,1074

5. Gross profit ratios:

(millions of dollars) 2014 2013

Sales ................................................................................. $ 16,435 16,148

Cost of goods sold ............................................................ 10,146 9,855

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-33

LO 2,3 PROBLEM 5-9 FINANCIAL STATEMENTS

1. Cost of goods sold for 2016:

Beginning inventory .......................................................... $ 6,400

2. Net income for 2016:

Net sales ........................................................................... $83,584

Cost of goods sold [from part (1)] ...................................... 38,675

Gross profit .................................................................. $44,909

5-34 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 5-9 (Concluded)

3. MAPLE INC.

BALANCE SHEET

AT DECEMBER 31, 2016

Assets

Current assets:

Cash ............................................................................ $ 590

Accounts receivable .................................................... 2,359

Inventory ...................................................................... 7,500

Interest receivable ...................................................... 100

Total current assets ................................................ $10,549

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-35

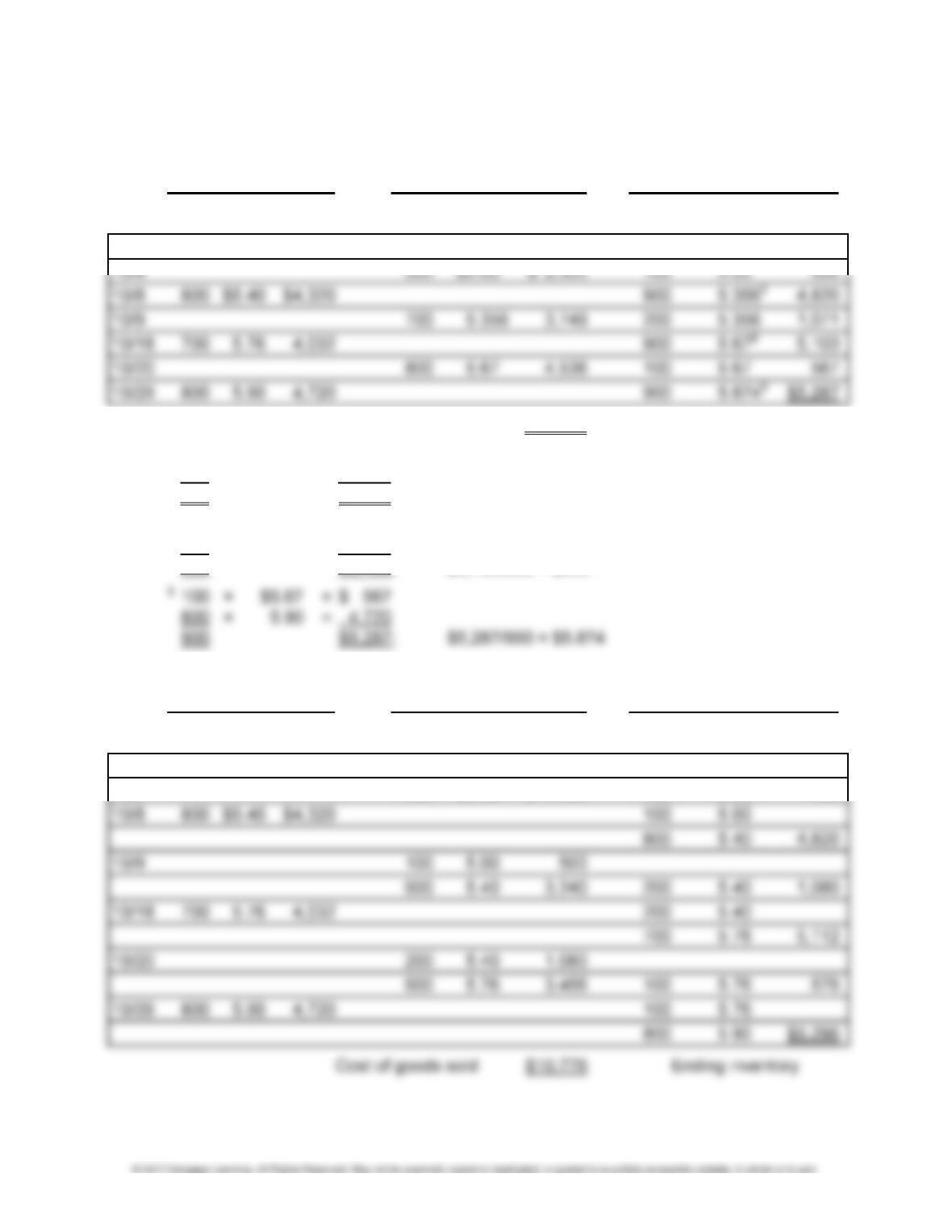

LO 5,6,7 PROBLEM 5-10 COMPARISON OF INVENTORY COSTING METHODS—

PERIODIC SYSTEM

1. Cost of Ending

Goods Sold Inventory Total

a. Weighted average ....................... $11,084 $4,988 $16,072

b. FIFO ............................................ 10,776 5,296 16,072

c. LIFO ............................................ 11,452 4,620 16,072

Cost of goods sold = 2,000 × $5.542 = $11,084

b. Ending inventory:

800 × $5.90 = $4,720

100 × 5.76 = 576

900 $5,296

5-36 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 5-10 (Concluded)

2. The Total column represents the pool of costs (beginning inventory plus purchases)

to be distributed between an asset, ending inventory on the balance sheet, and an

expense, cost of goods sold on the income statement. In accounting, this pool of

3. Income statements for the month of October:

Weighted

Average

FIFO LIFO

Sales* ............................................... $20,800 $20,800 $20,800

Cost of goods sold ............................ 11,084 10,776 11,452

4. The company will pay $203 more in taxes if it uses FIFO:

FIFO tax ................. $2,107

LIFO tax ................. 1,904

Difference .............. $ 203

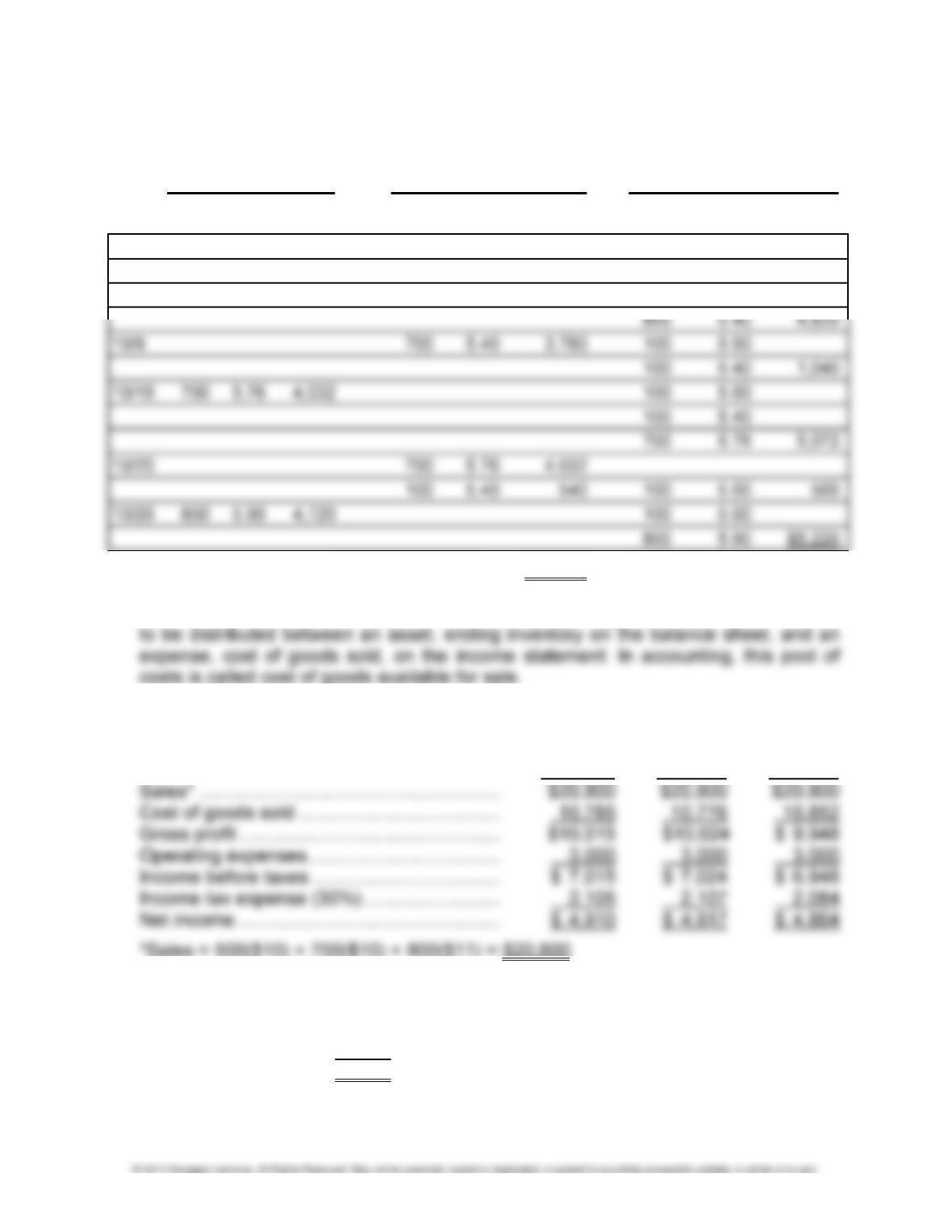

LO 5,7,12 PROBLEM 5-11 COMPARISON OF INVENTORY COSTING METHODS—

PERPETUAL SYSTEM (Appendix)

1. Cost of Ending

Goods Sold Inventory Total

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-37

PROBLEM 5-11 (Continued)

a. Moving average:

Purchases

Sales Balance

Unit Total Unit Total Unit

Date Units Cost Cost Units Cost Cost Units Cost Balance

10/1 600 $5.00 $3,000

Cost of goods sold $10,785 Ending inventory

1 100 × $5.00 = $ 500

800 × 5.40 = 4,320

900 $4,820; $4,820/900 = $5.356

2 200 × $5.356 = $1,071

700 × 5.76 = 4,032

900 $ 5,103; $5,103/900 = $5.67

b. FIFO:

Purchases

Sales Balance

Unit Total Unit Total Unit

Date Units Cost Cost Units Cost Cost Units Cost Balance

10/1 600 $5.00 $3,000

10/4 500 $5.00 $ 2,500 100 5.00 500

5-38 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 5-11 (Concluded)

c. LIFO:

Purchases

Sales Balance

Unit Total Unit Total Unit

Date Units Cost Cost Units Cost Cost Units Cost Balance

10/1 600 $5.00 $3,000

10/4 500 $5.00 $ 2,500 100 5.00 500

10/8 800 $5.40 $4,320 100 5.00

Cost of goods sold $10,852 Ending inventory

2. The Total column represents the pool of costs (beginning inventory plus purchases)

3. Income statements for the month of October:

Moving

Average FIFO LIFO

4. The company will pay $23 more in taxes if it uses FIFO:

FIFO tax ................. $2,107

LIFO tax ................. 2,084

Difference .............. $ 23

CHAPTER 5 • INVENTORIES AND COST OF GOODS SOLD 5-39

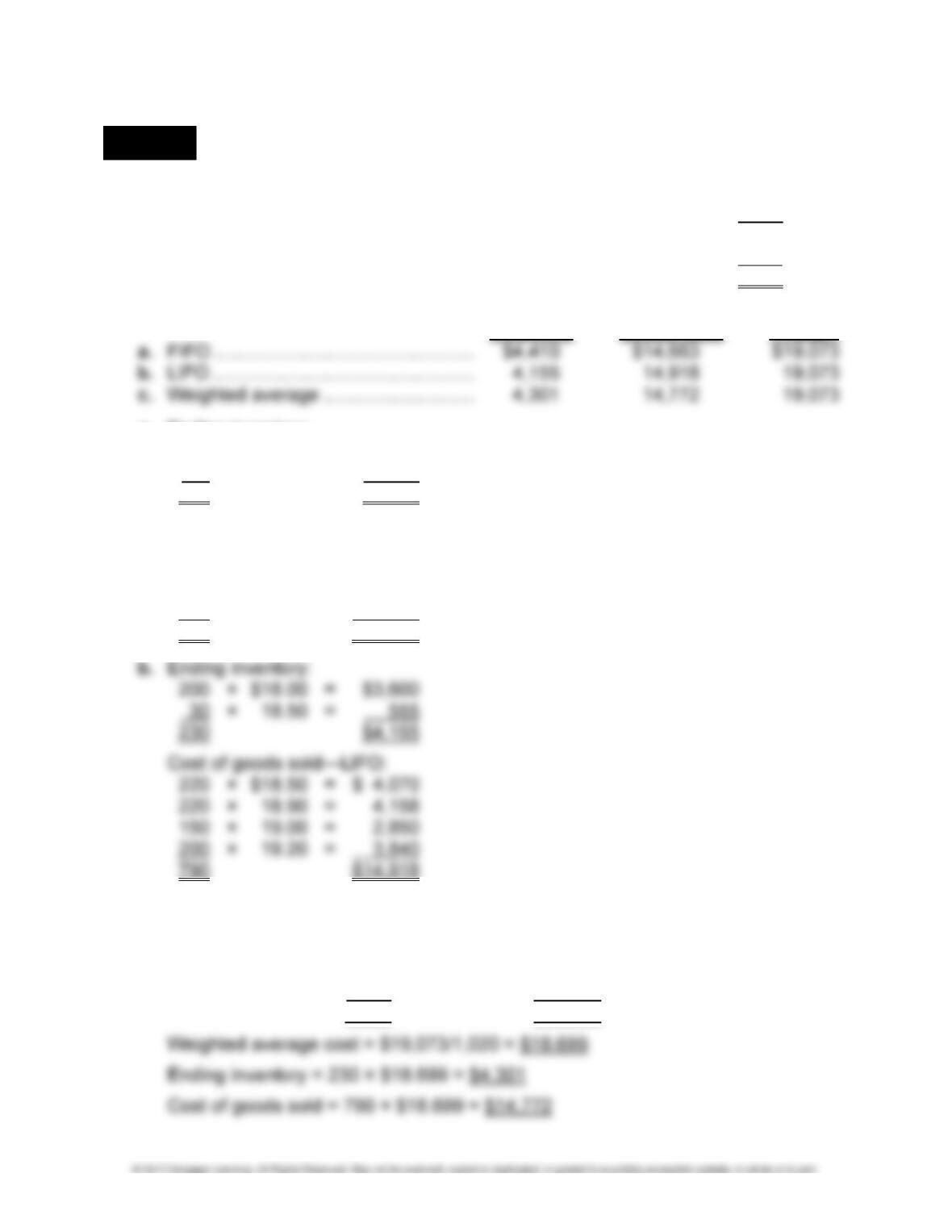

LO 5,6,7 PROBLEM 5-12 INVENTORY COSTING METHODS—PERIODIC SYSTEM

1. Units in beginning inventory ......................................................... 200

Units purchased (250 + 220 + 150 + 200) .................................... 820

Units available ............................................................................. 1,020

Units sold (300 + 380 + 110) ........................................................ (790)

Units in ending inventory .............................................................. 230

Ending Cost of

Inventory Goods Sold Total

a. Ending inventory:

200 × $19.20 = $3,840

30

× 19.00 = 570

230 $4,410

Cost of goods sold:

200 × $18.00 = $ 3,600

250 × 18.50 = 4,625

220 × 18.90 = 4,158

120 × 19.00 = 2,280

790 $14,663

c. Beginning inventory 200 × $18.00 = $ 3,600

Nov. 4 250 × 18.50 = 4,625

Nov. 13 220 × 18.90 = 4,158

Nov. 18 150 × 19.00 = 2,850

Nov. 24 200 × 19.20 = 3,840

1,020 $19,073

5-40 FINANCIAL ACCOUNTING SOLUTIONS MANUAL

PROBLEM 5-12 (Concluded)

2. Weighted

FIFO

LIFO Average

Sales* .......................................................... $33,480 $33,480 $33,480

Cost of goods sold ....................................... 14,663 14,918 14,772

3. Oxendine pays the least taxes under the last-in, first-out method since it has the

highest cost of goods sold.

4. If Oxendine Company prepares its financial statements in accordance with IFRS,

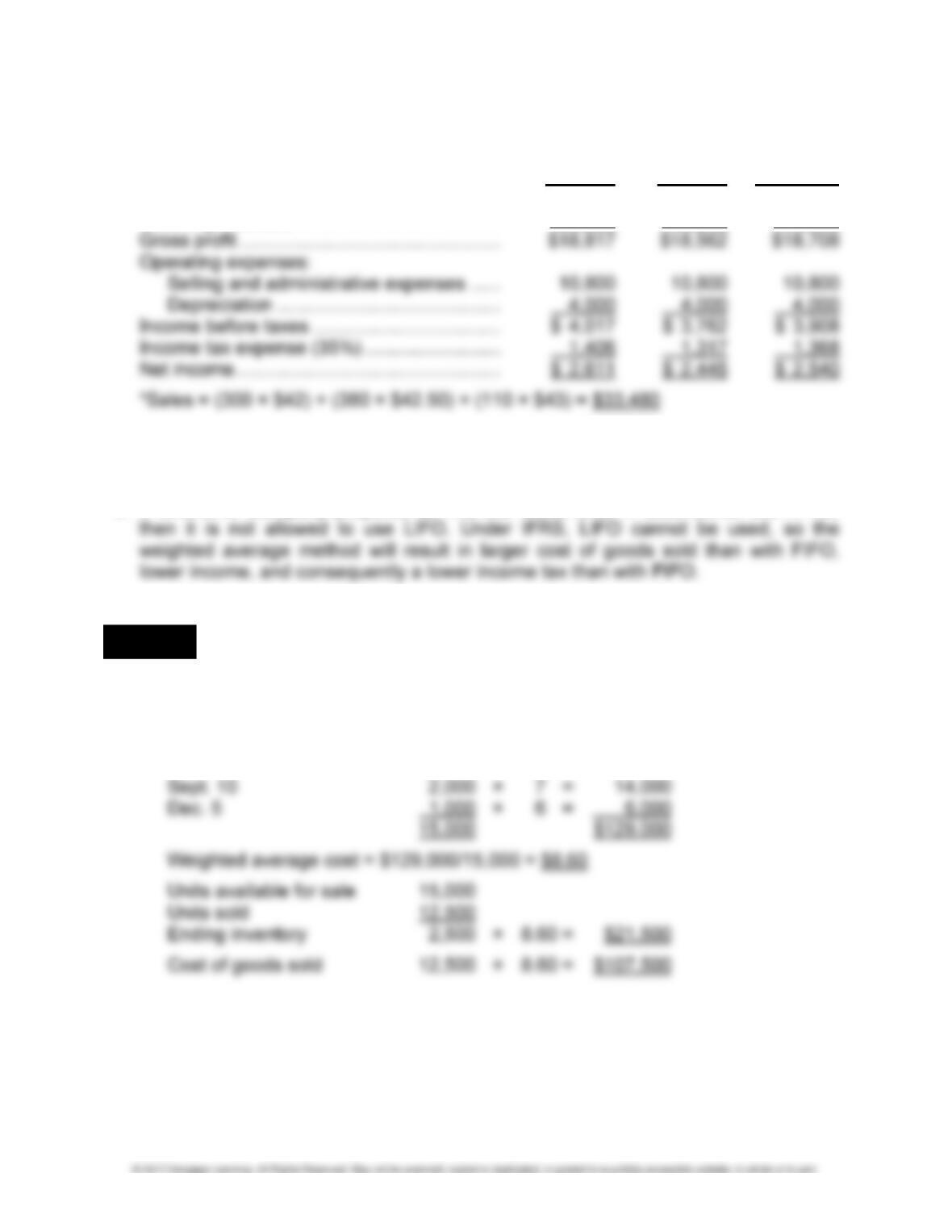

LO 5,6,7 PROBLEM 5-13 INVENTORY COSTING METHODS—PERIODIC SYSTEM

1. a. Weighted average:

Beginning inventory 5,000 × $10 = $ 50,000

Feb. 4 3,000 × 9 = 27,000

Apr. 12 4,000 × 8 = 32,000