SOLUTION

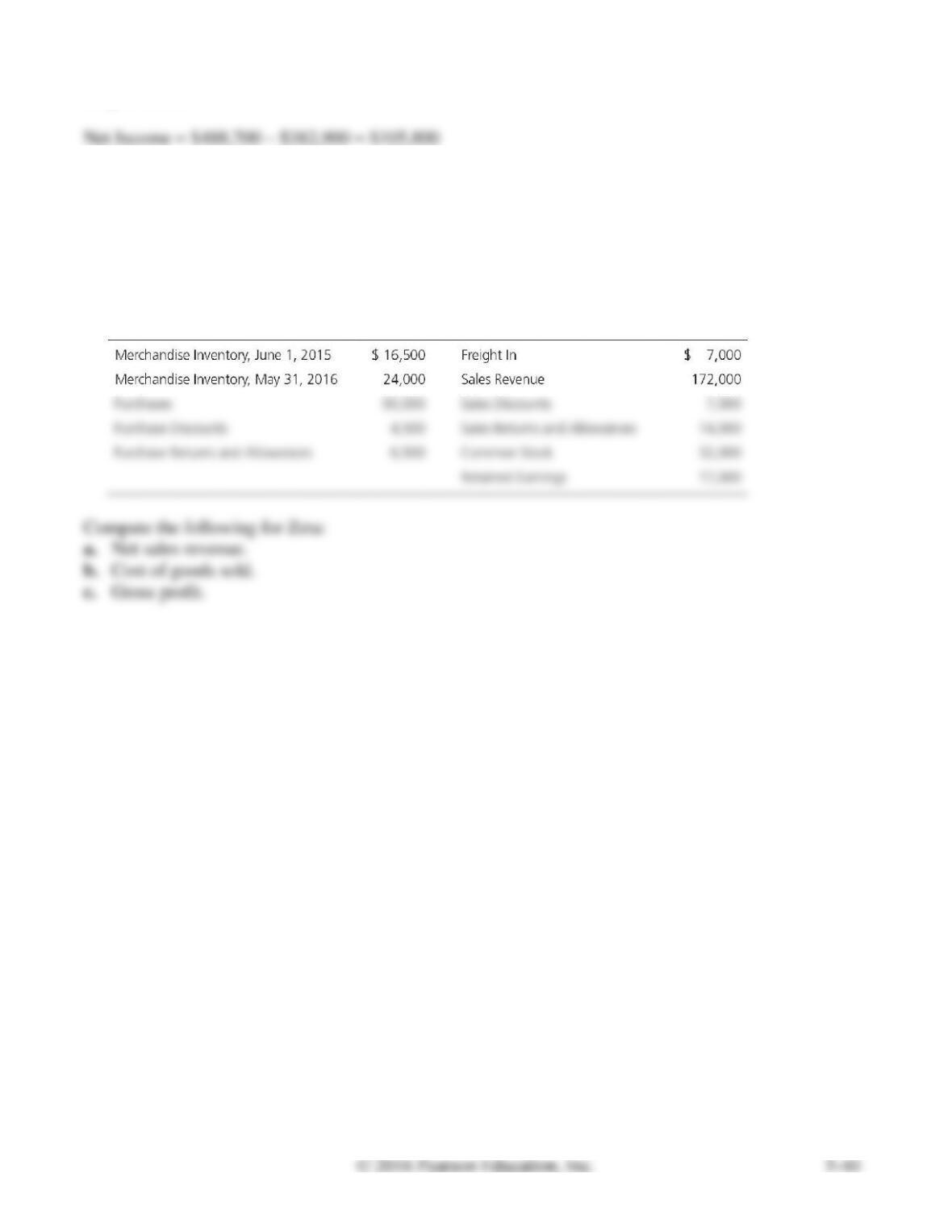

Requirements 1, 2, and 3

Date

Accounts and Explanation

Debit

Credit

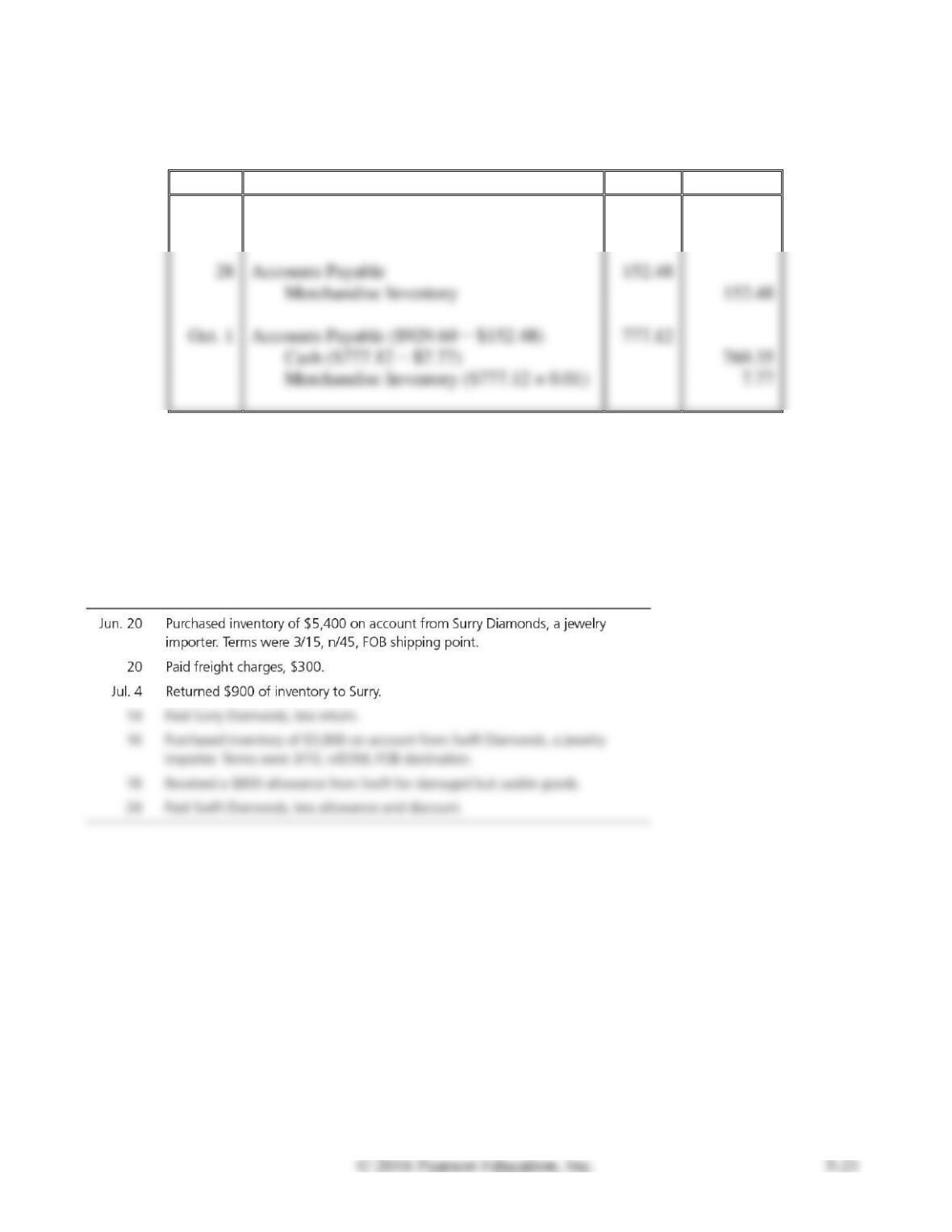

Sep. 23

Merchandise Inventory

929.60

Accounts Payable

929.60

Accounts Payable

152.48

Merchandise Inventory

152.48

Accounts Payable ($929.60 − $152.48)

777.12

Cash ($777.12 − $7.77)

769.35

Merchandise Inventory ($777.12 × 0.01)

E5-17 Journalizing purchase transactions

Learning Objective 2

July 24 Merch. Inv. $90

Hartford Jewelers had the following purchase transactions. Journalize all necessary transactions.

Explanations are not required.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

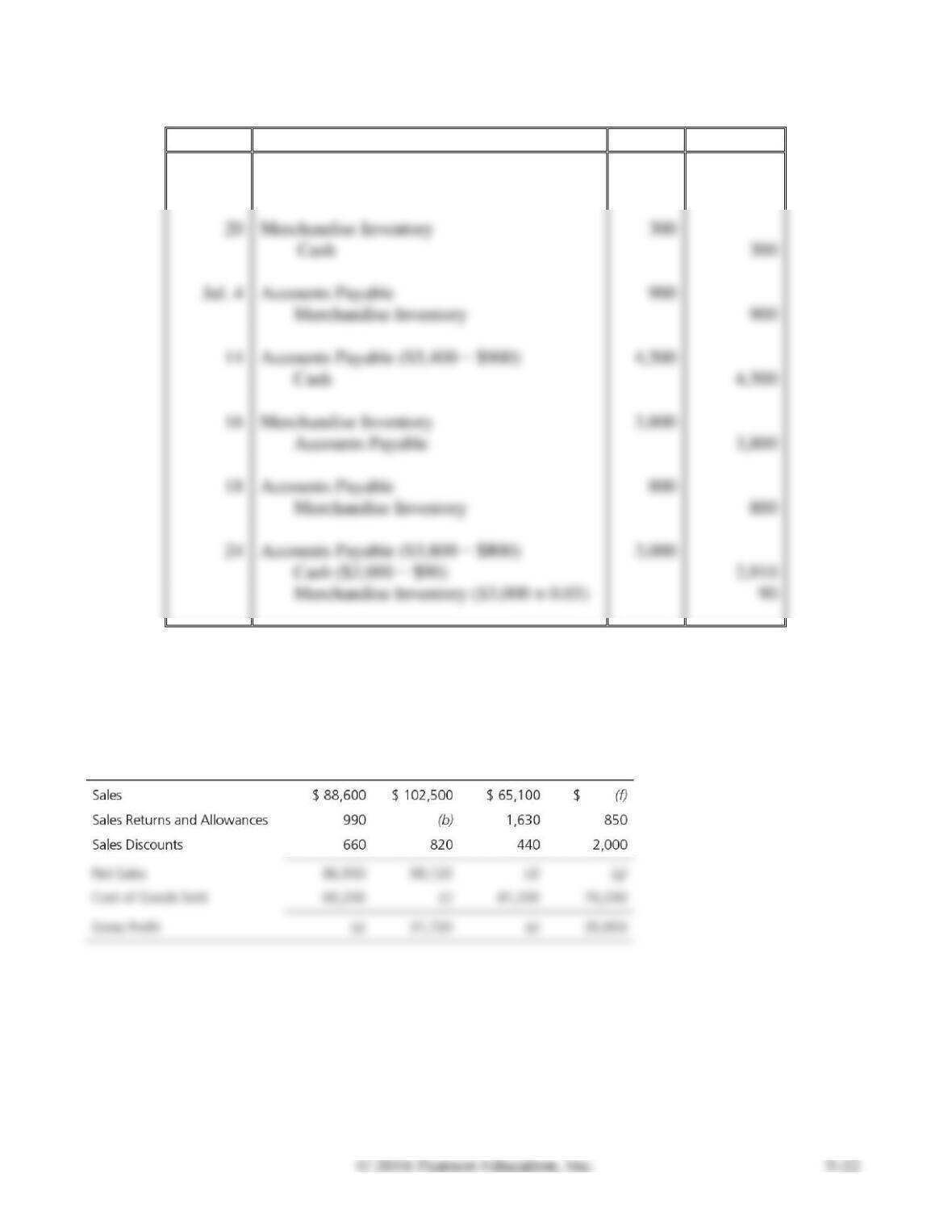

Jun. 20

Merchandise Inventory

5,400

Accounts Payable

5,400

Merchandise Inventory

300

Cash

Accounts Payable

Merchandise Inventory

Accounts Payable ($5,400 − $900)

4,500

Cash

4,500

Merchandise Inventory

3,800

Accounts Payable

3,800

Accounts Payable

Merchandise Inventory

Accounts Payable ($3,800 − $800)

3,000

Cash ($3,000 − $90)

2,910

Merchandise Inventory ($3,000 × 0.03)

E5-18 Computing missing amounts

Learning Objective 3

Consider the following incomplete table of merchandiser’s profit data. Calculate the missing amounts to

complete the table.

SOLUTION

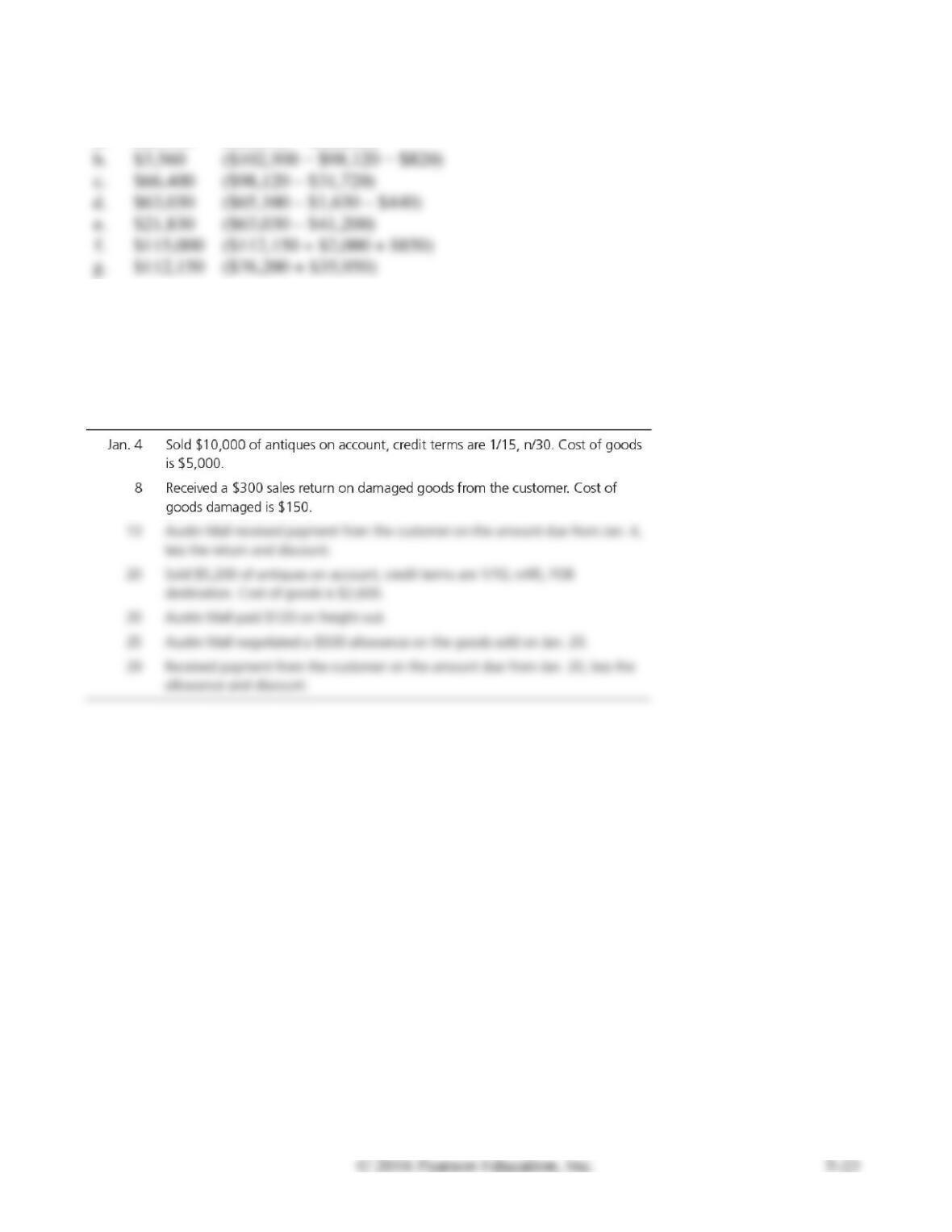

a.

$26,750 ($86,950 − $60,200)

b.

$3,560 ($102,500 − $98,120 − $820)

c.

$66,400 ($98,120 – $31,720)

d.

$63,030 ($65,100 – $1,630 – $440)

e.

$21,830 ($63,030 – $41,200)

$115,000 ($112,150 + $2,000 + $850)

g.

$112,150 ($76,200 + $35,950)

E5-19 Journalizing sales transactions

Learning Objective 3

Jan. 13 Sales Discounts $97

Journalize the following sales transactions for Austin Mall. Explanations are not required.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

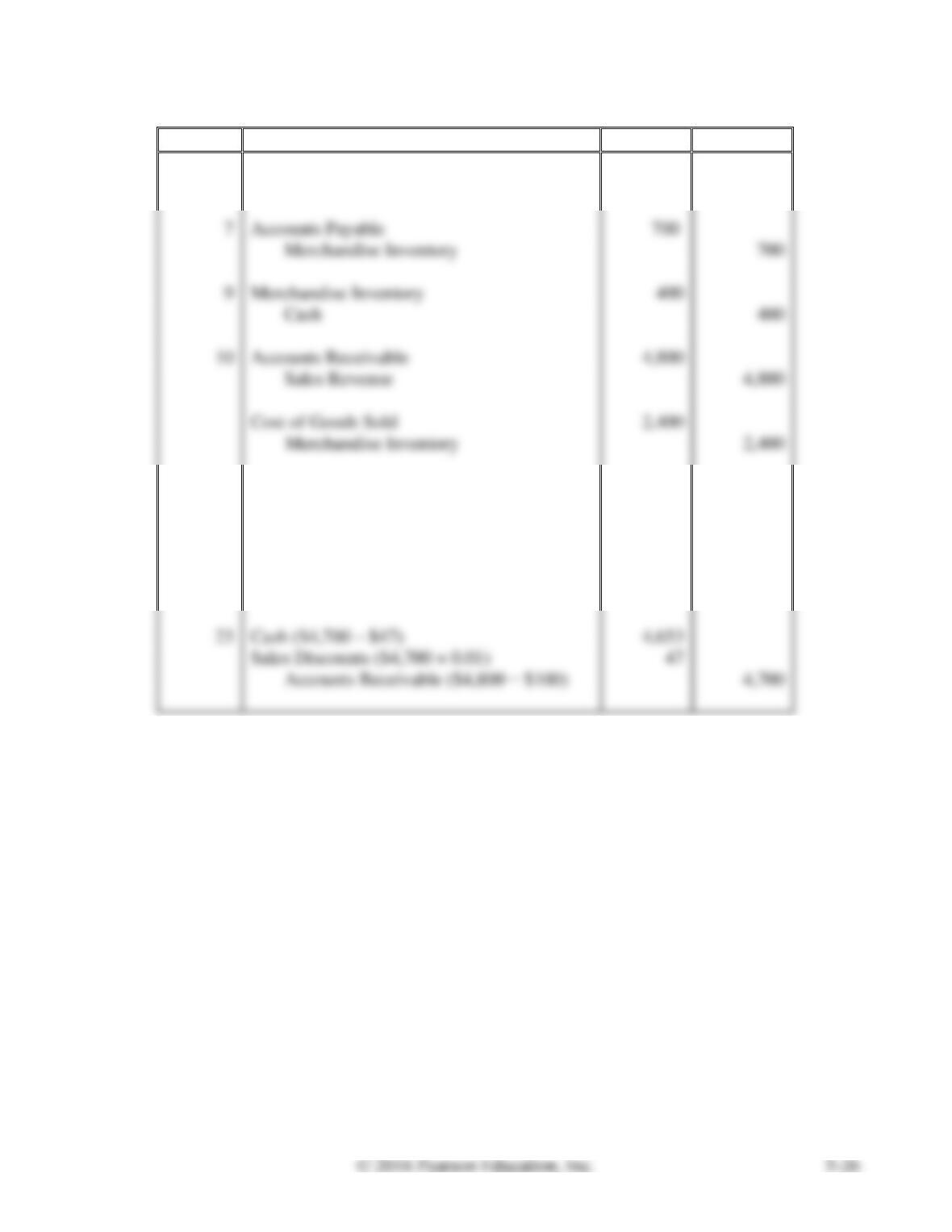

Jan. 4

Accounts Receivable

10,000

Sales Revenue

10,000

Cost of Goods Sold

5,000

Merchandise Inventory

5,000

Sales Returns and Allowances

300

Accounts Receivable

300

Merchandise Inventory

150

Cost of Goods Sold

150

13

Cash ($9,700 − $97)

9,603

Sales Discounts ($9,700 × 0.01)

97

Accounts Receivable ($10,000 − $300)

9,700

20

Accounts Receivable

5,200

Sales Revenue

5,200

Cost of Goods Sold

2,600

Merchandise Inventory

2,600

20

Delivery Expense

120

Cash

120

25

Sales Returns and Allowances

500

Accounts Receivable

500

29

Cash ($4,700 − $47)

4,653

Sales Discounts ($4,700 × 0.01)

47

Accounts Receivable ($5,200 − $500)

4,700

E5-20 Journalizing purchase and sales transactions

Learning Objectives 2, 3

Feb. 23 Cash $4,653

Journalize the following transactions for Santa Fe Art Gift Shop. Explanations are not required.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

Feb. 3

Merchandise Inventory

2,800

Accounts Payable

2,800

Accounts Payable

700

Merchandise Inventory

700

Merchandise Inventory

400

Cash

400

10

Accounts Receivable

4,800

Sales Revenue

4,800

Cost of Goods Sold

2,400

2,400

12

Accounts Payable ($2,800 – $700)

2,100

Cash ($2,100 – $63)

2,037

Merchandise Inventory ($2,100 × 0.03)

63

16

Sales Returns and Allowances

100

Accounts Receivable

100

23

Cash ($4,700 – $47)

4,653

Sales Discounts ($4,700 × 0.01)

Accounts Receivable ($4,800 − $100)

4,700

E5-21 Journalizing adjusting entries and computing gross profit

Learning Objectives 3, 4

2. Net Sales $71,400

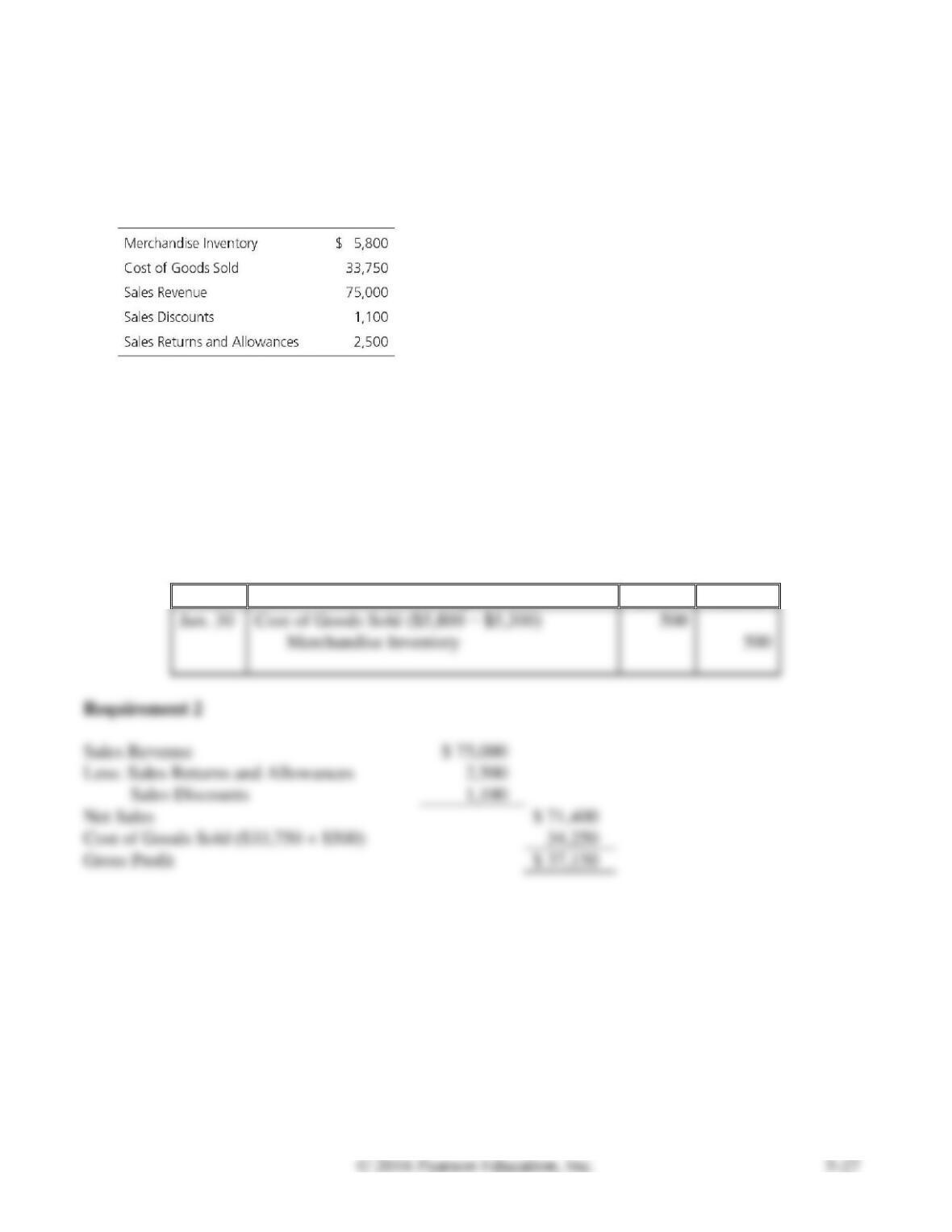

Dog-eared Book Shop’s accounts at June 30, 2016, included the following unadjusted balances:

The cost associated with the physical count of inventory on hand on June 30, 2016, was $5,300.

Requirements

1. Journalize the adjustment for inventory shrinkage.

2. Compute the gross profit.

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Use the following information to answer Exercises E5-22 through E5-24.

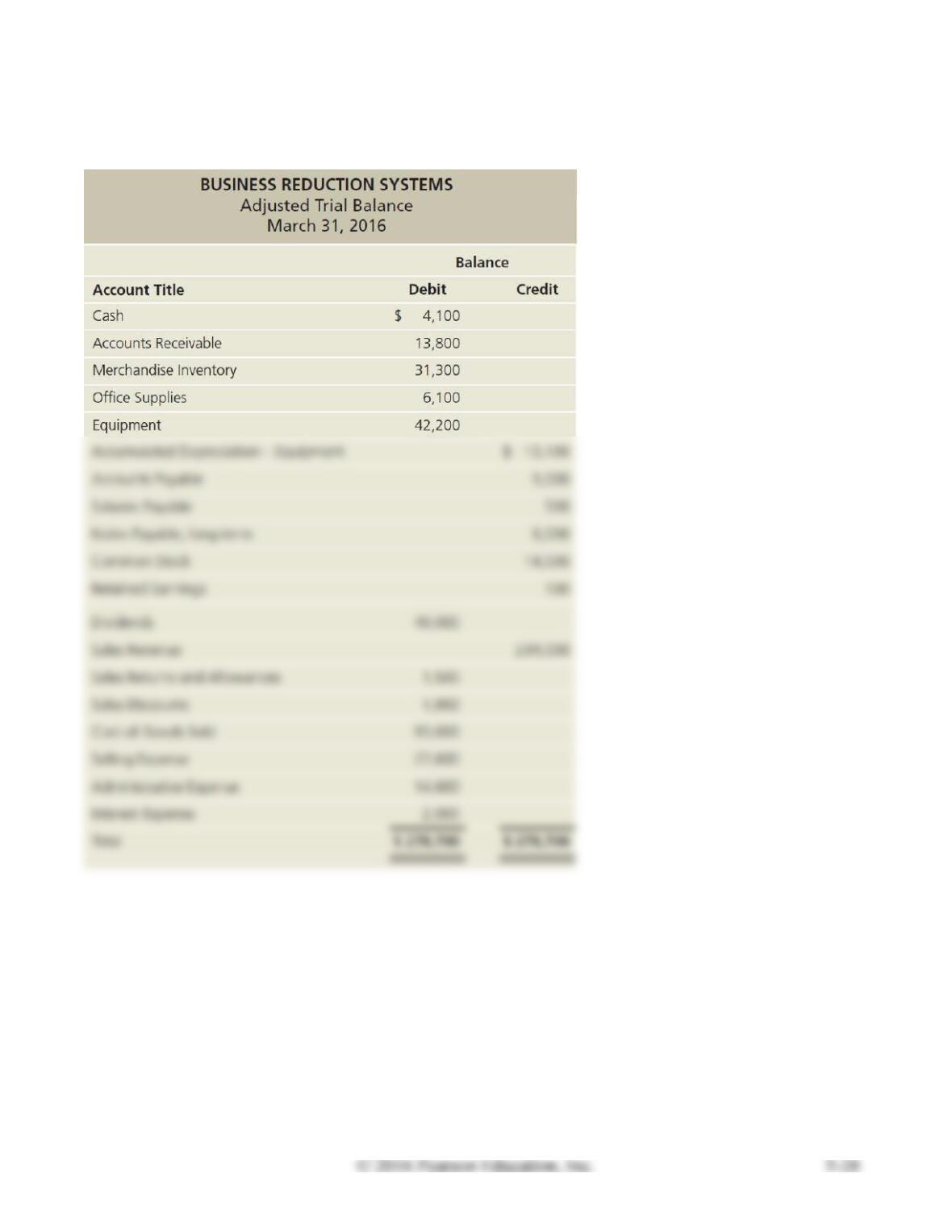

The adjusted trial balance of Business Reduction Systems at March 31, 2016, follows:

E5-22 Journalizing closing entries

Learning Objective 4

2. Ending Retained Earnings Balance $52,900

Requirements

1. Journalize the required closing entries at March 31, 2016.

2. Set up T-accounts for Income Summary; Retained Earnings; and Dividends. Post the

closing entries to the T-accounts, and calculate their ending balances.

3. How much was Business Reduction’s net income or net loss?

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Mar. 31

Sales Revenue

234,000

Income Summary

234,000

Income Summary

141,200

Income Summary

Retained Earnings

Requirement 2

92,800 Bal.

Clos. 4 40,000

92,800 Clos. 3

52,900 Bal.

40,000 Clos. 4

Requirement 3

Income Summary

Retained Earnings

Clos. 2 141,200

234,000 Clos. 1

100 Adj. Bal.

Dividends

E5-23 Preparing a single-step income statement

Learning Objective 5

Net Income $92,800

Prepare Business Reduction’s single-step income statement for the year ended March 31, 2016.

SOLUTION

BUSINESS REDUCTION SYSTEMS

Income Statement

Year Ended March 31, 2016

Revenues:

Net Sales Revenue

$ 230,600

Expenses:

Cost of Goods Sold

$ 93,600

Selling Expense

Administrative Expense

Interest Expense

E5-24 Preparing a multi-step income statement

Learning Objective 5

Gross Profit $137,000

Prepare Business Reduction’s multi-step income statement for the year ended March 31, 2016.

SOLUTION

BUSINESS REDUCTION SYSTEMS

Income Statement

Year Ended March 31, 2016

Sales Revenue

$ 234,000

Less: Sales Discounts

Net Sales Revenue

Cost of Goods Sold

Gross Profit

Operating Expenses:

Operating Income

Other Revenues and (Expenses):

Net Income

E5-25 Computing the gross profit percentage

Learning Objective 6

Gross Profit Percentage 39%

Cupcake Queen earned net sales revenue of $67,000,000 in 2016. Cost of goods sold was $40,870,000,

and net income reached $8,000,000, the company’s highest ever. Compute the company’s gross profit

percentage for 2016.

SOLUTION

Net Sales Revenue

$ 67,000,000

Less: Cost of Goods Sold

40,870,000

Gross Profit

$ 26,130,000

E5A-26 Journalizing purchase transactions—periodic inventory system

Learning Objective 7

Appendix 5A

Sep. 17 Cash $5,626

Landry Appliances had the following purchase transactions. Journalize all necessary transactions using

the periodic inventory system. Explanations are not required.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

Sept. 4

Purchases

6,200

Accounts Payable

6,200

Cash

Accounts Payable

Purchase Returns and Allowances

Accounts Payable ($6,200 – $400)

5,800

Cash ($5,800 – $174)

5,626

Purchase Discounts ($5,800 × 0.03)

Purchases

4,600

Accounts Payable

4,600

Accounts Payable

Purchase Returns and Allowances

Accounts Payable ($4,600 – $900)

3,700

Cash ($3,700 – $111)

3,589

Purchase Discounts ($3,700 × 0.03)

E5A-27 Journalizing sales transactions—periodic inventory system

Learning Objective 7

Appendix 5A

Aug. 24 Sales Discounts $50

Journalize the following sales transactions for Double Z Archery using the periodic inventory system.

Explanations are not required.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

Aug. 1

Accounts Receivable

7,800

Sales Revenue

7,800

Sales Returns and Allowances

Accounts Receivable

Cash ($7,500 – $150)

7,350

Sales Discounts ($7,500 × 0.02)

Accounts Receivable ($7,800 – $300)

7,500

Accounts Receivable

3,200

Sales Revenue

3,200

Delivery Expense

Cash

Sales Returns and Allowances

Accounts Receivable

Cash ($2,500 – $50)

2,450

Sales Discounts ($2,500 × 0.02)

Accounts Receivable ($3,200 – $700)

2,500

E5A-28 Journalizing purchase and sales transactions—periodic inventory system

Learning Objective 7

Appendix 5A

Nov. 22 Accounts Receivable $5,800

Journalize the following transactions for Moody Bicycles using the periodic inventory system.

Explanations are not required.

SOLUTION

Date

Accounts and Explanation

Debit

Credit

Nov. 2

Purchases

3,700

Accounts Payable

3,700

Accounts Payable

Purchase Returns and Allowances

Cash

Accounts Receivable

6,200

Sales Revenue

6,200

Accounts Payable ($3,700 – $600)

3,100

Cash ($3,100 – $93)

3,007

Purchase Discounts ($3,100 × 0.03)

93

Sales Returns and Allowances

Accounts Receivable

Cash ($5,800 – $58)

5,742

Sales Discounts ($5,800 × 0.01)

Accounts Receivable ($6,200 – $400)

5,800

E5A-29 Journalizing closing entries—periodic inventory system

Learning Objective 7

Appendix 5A

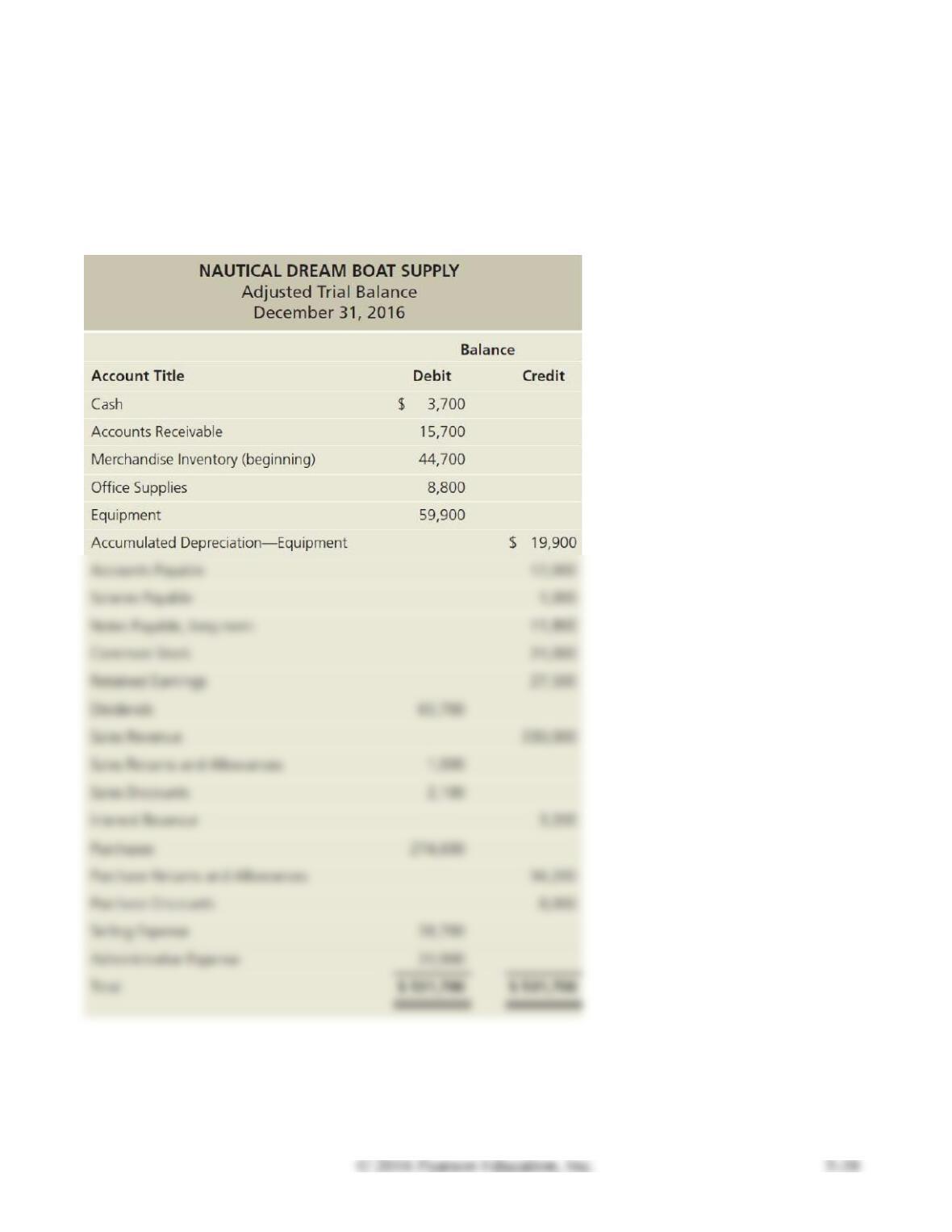

2. Ending Retained Earnings Balance $72,600

Nautical Dream Boat Supply uses the periodic inventory method. The adjusted trial balance of Nautical

Dream Boat Supply at December 31, 2016, follows:

Requirements

1. Journalize the required closing entries at December 31, 2016. Assume ending Merchandise

Inventory is $53,300.

2. Set up T-accounts for Income Summary; Retained Earnings; and Dividends. Post the closing entries

to the T-accounts, and calculate their ending balances.

3. How much was Nautical Dream’s net income or net loss?

SOLUTION

Requirement 1

Date

Accounts and Explanation

Debit

Credit

Dec. 31

Sales Revenue

330,000

Interest Revenue

3,200

Purchase Returns and Allowances

94,200

Purchase Discounts

8,000

Merchandise Inventory (ending)

53,300

Income Summary

488,700

Income Summary

382,900

274,600

Income Summary

105,800

105,800

Retained Earnings

60,700

Requirement 2

105,800 Bal.

105,800 Clos. 3

72,600 Bal.

Adj. Bal. 60,700

60,700 Clos. 4

Income Summary

Retained Earnings

Clos. 2 382,900

488,700 Clos. 1

27,500 Adj. Bal.

Requirement 3

E5A-30 Computing cost of goods sold in a periodic inventory system

Learning Objective 7

Appendix 5A

Zeta Electric uses the periodic inventory system. Zeta reported the following selected amounts at May

31, 2016: